This morning I read a post by noted MMTer Stephanie Kelton, which responded to some questions by Paul Krugman. I predicted that he’d be pulling out his hair, as her responses were a complete mess—as if she didn’t understand the simple questions he was asking. Here’s an excerpt from my Econlog post:

I can’t even imagine Krugman’s reaction to all this. First of all, although she says “no” in answer to question #1, her explanation makes it quite clear that she is actually answering “yes”, especially when you combine the answers to questions #1 and #2. Krugman is asking whether, assuming a given macroeconomic situation (including a given level of private spending), there is only one budget deficit consistent with full employment. She clearly thinks the answer is yes. So why does she answer “no”. I suspect she doesn’t understand Krugman’s question (which is pretty straightforward.)

Now Krugman has responded and he’s every bit as frustrated as I expected. Here is his response to the first point I raised:

Her response to my first question totally misses the point; I was asking if *given private behavior* there’s a unique level of the deficit needed for full employment, and argued that there wasn’t. She just assumes that there is

And here’s how Krugman summarizes his twitter thread:

Sorry, but this is just a mess. Kelton’s response misrepresents standard macroeconomics, my own views, the effects of interest rates, and the process of money creation. Otherwise I guess it’s all fine. See what I mean about Calvinball? 6/

MMT desperately needs a spokesperson capable of conversing with economists like Paul Krugman, if they want to be taken seriously. When they give bizarre answers to serious questions from a highly respected economist on their side of the ideological spectrum, it’s a problem.

Not surprisingly, I think it’s perfectly fine to be heterodox, but first you need to understand orthodox.

The US yield curve usually slopes upward. Hence positively sloped yield curves are termed ‘normal’ and negatively sloped yield curves are termed ‘inverted’. But are “normal” yield curves actually normal?

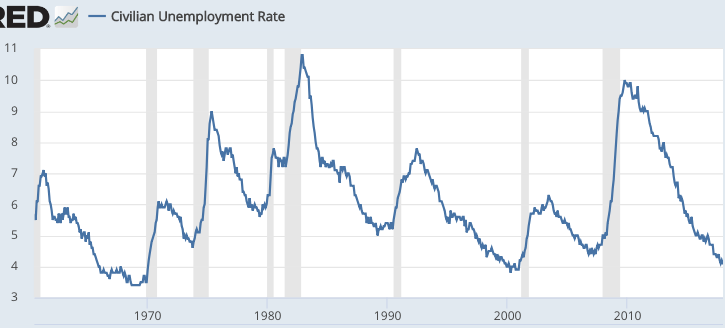

The US business cycle has an unusual feature, an absence of soft landings. A soft landing is when unemployment recovers to the natural rate, and then stays low for at least four years. The only plausible example is 1966-69, but that wasn’t really a soft landing because it came at the expense of rapidly accelerating inflation. The plane soared off into the stratosphere before the wheels even touched the runway. Otherwise, we have only a year or two of stable and low unemployment, before the next recession.

He not busy being born is busy dying — B. Dylan

So 90% of the time we are either recovering (mostly with a normal yield curve) or in recession (mostly with a normal yield curve.) Inverted curves tend to occur right before a recession, when unemployment is low. But what if we did have a true soft landing—persistent low unemployment without accelerating inflation? Would the yield curve be flat? After all, when output is already near the natural rate, you don’t expect further recovery. You don’t expect the future economy to be better (stronger) than the present.

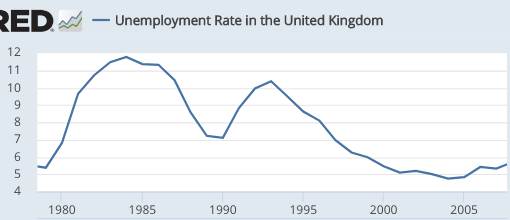

So I decided to seek out a country that did have a soft landing—Britain from 2001-08:

2001-08: Not busy being born or busy dying

Notice that in 1991, the UK entered recession almost immediately after the unemployment rate stopped falling—the US pattern. But in 2001, unemployment reached the low 5s and stayed near there until mid-2008. So how about the UK yield curve? Below I have data from 2000-08, using June data in each case. The first number is the nominal yield on 6-month UK T-bonds, and the second number is the yield on 10-year bonds. I’m not used to using UK data, so someone tell me if I made a mistake:

2000: 6.0%, 4.13%

2001: 5.33%, 4.92%

2002: 4.38%, 4.80%

2003: 3.19%, 4.87%

2004: 4.89%, 4.93%

2005: 4.16%, 4.28%

2006: 4.70%, 4.47%

2007: 5.85%, 4.94%

2008: 5.26%, 5.12%

During these 9 years, the UK yield curve was slightly inverted, on average. But pretty close to flat. This suggests that a flat yield curve might be expected when the economy is still expanding, but the unemployment rate is not expected to fall much further.

Note that the US yield curve was pretty flat in May 2006, when unemployment had fallen to 4.6% and was expected to stay around that level. And unemployment did stay around that level for another 18 months. The yield curve was also fairly flat in 1966. The yield curve today slopes gradually upward, but it’s flat between 2 years and 5 years, which suggests to me that markets may be expecting the US to achieve a soft landing.

The unemployment rate today (4.0%) is not much different from 15 months back (when it was 4.1%.) I expect it to fall a few more ticks (the trend is actually in the high 3s), but then stop falling. If I’m right that the US will achieve its first ever non-inflationary soft landing, then I’d expect a pretty flat yield curve to be the new normal. There’d still be a slight tendency for an upward slope, but not much.

Of course this happy scenario assumes that the Fed keeps NGDP growing at a reasonably steady rate (say a range of 3% to 5%). There are no guarantees, but they seem to be trying to do something like that in recent years, even if they don’t admit it.

As time goes by, it becomes increasingly obvious that global populism has no coherent governing philosophy. Or if it does, it has no serious intention to implement those policies.

The most recent Economist has a number of articles discussing recent politics in Britain and France, which are both wracked by populist turmoil. It’s now clear that the Brexit hardliners have no governing vision for the UK, and that their ideology is essentially nihilistic. The same is true of the yellow jacket protesters in France. As with many other populist movements throughout the world, the yellow jackets began with a set of economic grievances and soon morphed into a crude nativist movement, full of racism and anti-Semitism.

Trump’s only major policy successes have been in adopting the traditional “Mitt Romney” GOP agenda, cutting taxes for big corporations, easing environmental regs, and nominating conservative judges. According to the FT, the rumored China trade deal is likely to continue that trend:

Yet there is scant evidence that Beijing has offered to make a big change in course, or to provide a mechanism to assure Washington that it will stick by any commitments. . . .

For Mr Trump, there is a clear desire to reassure markets and extend the momentum in the US economy ahead of his re-election bid in 2020. He wants to fulfil a key campaign promise to reset trade relations with China, especially as the prospects for other commitments, such as building a wall on the Mexican border, have faded.

The risk for the president is a backlash from China hawks both on the left and the right of the political spectrum, who are already grumbling that Mr Trump will settle for a weak deal. To them, he squandered much of his leverage by delaying the tariff increase.

“Lighthizer’s ability to get binding MoUs on the key non-trade barrier issues such as forced technology transfers can only occur if you execute the 1 March tariffs — otherwise the pressure comes off the Chinese,” Steve Bannon, Mr Trump’s former senior adviser, said in an email on Saturday.

China’s stock market was up 5.6% today. Good.

Obviously this rumored agreement won’t address the underlying economic issues that concern protectionists like Navarro and Bannon. It won’t reduce our trade deficit and it won’t bring manufacturing jobs back to America. But this is one of those rare occasions where I side with Trump, and I also believe this will be good for him politically. Most of his base doesn’t care about any actual policy changes, they are just interested in seeing him look like a leader who “owns the libs”. They don’t want to see empty shelves when they shop at Walmart. And a stock market crash would look bad to Trump’s upper middle class white supporters.

There are much worse things than a demagogue being a “market politician”, guided by stock market sentiment like an ox with a nose ring being pulling along by a farmer. Imagine if he were actually a 1930s-style populist, implementing actual populist policies.

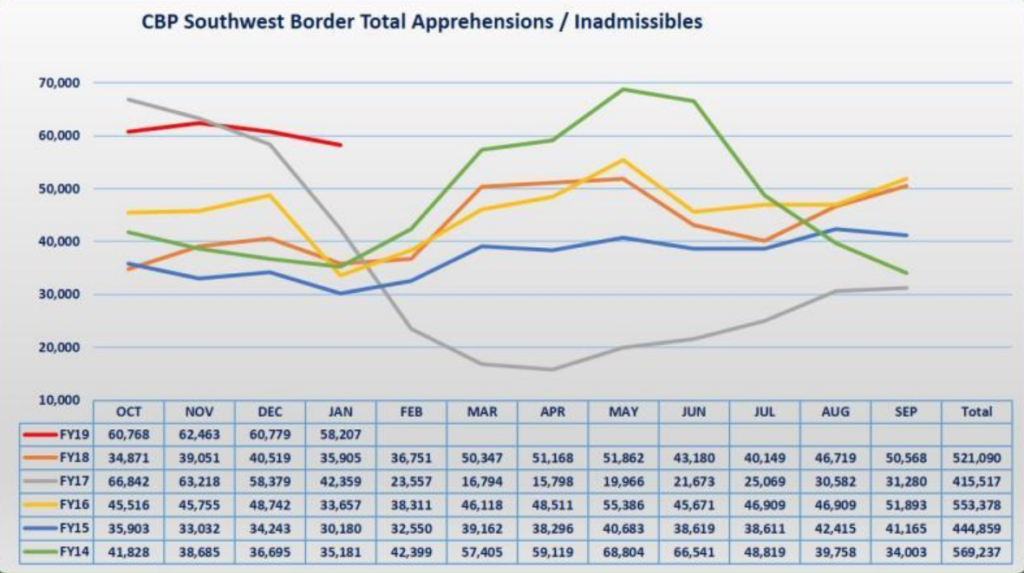

Meanwhile, Trump’s attempt to close the southern border has failed, at least according to the metric used by the Trumpistas to claim success in early 2017. This NYT article provides numerous quotes of Trump gloating over the drop in detentions at the border, which occurred during the first half of 2017 (grey line):

Trump succeeded before he failed

By fiscal year 2018, things were back to normal according to this very same data source, and detentions are now well above the levels of previous years (red line).

As with Trump’s failure to achieve the Navarro/Bannon trade agenda, and as with his failure to get a big federal infrastructure program, this border failure is actually good news. We need more illegal workers to “Make America Great Again”. After all, poor Americans on welfare have zero interest in picking vegetables all day in the hot sun, unless you raised their wage so high that American consumers switched to imported vegetables and we started growing wheat in California. Illegal Mexican immigrants in construction will make new Texas homes more affordable for blue collar workers moving from Buffalo, fleeing New York state’s nightmarish fiscal policies and cold weather.

The Dems were willing to give Trump the wall in exchange for a DACA agreement, something overwhelmingly supported by his base. But ultimately his base cares more about Trump continuing to fight the elites, so he opted to forego the wall. Trump cares more about having the “fighting for the wall” issue than he does about stopping the flow of illegals.

I still think that Trump’s unique mixture of stupidity, cruelty, and dishonesty makes him the worst president in US history. But it would be even worse if he took seriously the demagogic populist agenda that he ran on. Instead, his primary goal seems to be propping up the stock market. We’ll see how the Dems react to that reality.

We live in the global era of populism, but actual populist policies are hard to find, outside of Venezuela.

PS. Next up is an entirely symbolic meeting with Trump’s love interest in North Korea. More “leadership” for his base.

PPS. For you alt-rightists depressed by all of this, consider that the new populist socialism on the left is every bit as empty of actual policy content as is Trumpism. No, America’s not about to become socialist, and, “You can keep your private health care plan.” I promise.

We keep reading pundits opine that neoliberalism is passé, and that we need a new model for the 21st century. So what is the new model being adopted in Ethiopia? Here’s the FT:

Ethiopia aims to complete a multibillion-dollar privatisation of its telecoms sector by the end of this year, followed by a sell-off of stakes in state energy, shipping and sugar companies, according to the new prime minister Abiy Ahmed.

The government also plans to launch a domestic stock exchange in 2020, part of a gradual but decisive shift towards economic liberalisation in the fast-growing east African country of 105m people.

“My economic model is capitalism,” Mr Abiy said in an interview with the Financial Times, conducted in his refurbished headquarters in Addis Ababa. “If you give me $100bn now, I can’t use it. There is not only money, there is talent and experience. That’s why we need the private sector.”

Don’t worry socialists, Marx assured us that capitalism is just an unfortunate phase that Ethiopia must pass through before they achieve the glories of North Korea, Cuba and Venezuela.

PS: Off topic, I have a new piece in The Hill defending my Fed accountability and transparency proposal.

The Fed plans to hold a conference in Chicago during June, with the goal of developing improved tools, targets and strategies. Obviously the major issue will be how to deal with the zero bound, which is expected to reoccur during the next recession. In my view the second goal should be to develop procedures that avoid the mistakes made during 2008 (before the zero bound was hit), which were acknowledged in Bernanke’s memoir.

One key lesson from the Great Recession is that when rates are zero it’s very difficult to be too expansionary. Almost everywhere in the world, at all times in history, central banks at the zero bound adopt policies that in retrospect look too contractionary. Contemporaneous fears of inflation prove groundless. So that’s one important lesson.

Next recession, the Fed needs to immediately stop paying IOR and be far more aggressive with QE than last time. We know that inflation isn’t the real problem at the zero bound. A recent Yahoo article suggests that bond yield pegging is another option being considered:

Fed officials would also reassess how well their policy toolkit worked in combating the deep recession that followed the financial crisis of 2008-09, and consider what additional tools might be added to prepare for the next downturn. He mentioned a crisis-time policy implemented by the Bank of Japan, which would seek to establish a temporary ceiling for Treasury debt yields at longer maturities, as a tool that might be considered.

That’s a reasonable option, but it’s not enough by itself. Indeed, doing more concrete steps at ultra-low interest rates is not enough, as ultra-low interest rates represent a sort of prediction of policy failure, a prediction that NGDP will grow too slowly to achieve the Fed’s dual mandate. The goal should be to prevent the zero bound from occurring in the first place, not just to deal with it appropriately. Once you are there, you have already (accidentally) adopted an inadequate policy.

One option for avoiding the zero bound it to raise the inflation target, but the Fed has ruled that out:

In reviewing its fundamental strategies, Clarida made clear the Fed wouldn’t change its target for inflation from the current 2 percent level. Policy makers would consider, however, whether the central bank should introduce a strategy that seeks to make up for periods of below-target inflation with periods of above-target price rises.

Level targeting is the sort of regime that makes it less likely you’ll hit the zero bound, but the devil is in the details. A promise to do whatever it takes to get back to the price level trend line in 10 years is far less effective than a promise to get back there in 4 years. Partly because the quicker rebound is more expansionary, and partly because it’s more credible that the Fed chair would still be around in 4 years.

Although I’d prefer 4% NGDPLT with no 2% inflation target, it is possible to combine NGDPLT with a flexible 2% inflation target, which puts weight on both inflation and employment. You simply set the NGDP target equal to 2% plus the Fed’s estimate of trend RGDP growth, and adjust the growth estimate periodically to reflect new estimates of trend RGDP growth. That’s not as good as a simple NGDP level targeting (inflation actually doesn’t matter), but it still gets you 95% of the benefits of NGDPLT and it’s also consistent with the Fed’s interpretation of its inflation mandate. Inflation will average 2% in the long run.

Ironically, the regime I just proposed would probably get you closer to a 2% long run trend rate of inflation than our current inflation targeting regime, which has repeatedly missed on the low side and then let “bygones be bygones”.

As noted, they also need to learn from their mistakes of 2008, and for that I recommend more reliance on market forecasts. I certainly don’t expect them to talk about NGDP futures markets, but recommending that the Treasury issue bonds indexed to NGDP growth might be a modest first step. Perhaps the NGDP bond payoffs could be based on the third GDP announcement, which occurs roughly 3 months after the quarter ends. That data is fairly complete, although of course there are occasionally later revisions as well.

The BLS might be instructed to keep two GDP series when there is a major definitional change (such as adding software to investment), to allow an internally consistent series for bond indexing. That’s a bit messy, but these major definitional changes don’t occur very often. Don’t let the perfect be the enemy of the good.

Welcome to a new blog on the endlessly perplexing problem of monetary policy. You’ll quickly notice that I am not a natural blogger, yet I feel compelled by recent events to give it a shot. Read more...

My name is Scott Sumner and I have taught economics at Bentley University for the past 27 years. I earned a BA in economics at Wisconsin and a PhD at Chicago. My research has been in the field of monetary economics, particularly the role of the gold standard in the Great Depression. I had just begun research on the relationship between cultural values and neoliberal reforms, when I got pulled back into monetary economics by the current crisis.

"I watched Satantango on video over 3 days. I found it absolutely gripping, but one must surrender for a time one's idea of what a movie should be. Instead, you..."

"Couldn't find the substack and if it's moderated just as well... Voted for Trump and he won. Sorry liberal Scott Sumner who believes in money non-neutrality, which is akin to..."