Are “normal” yield curves actually normal?

The US yield curve usually slopes upward. Hence positively sloped yield curves are termed ‘normal’ and negatively sloped yield curves are termed ‘inverted’. But are “normal” yield curves actually normal?

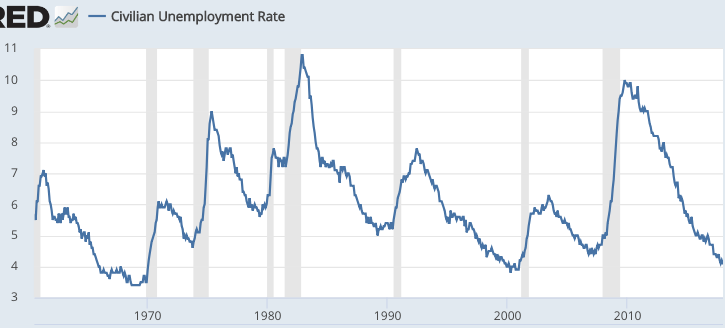

The US business cycle has an unusual feature, an absence of soft landings. A soft landing is when unemployment recovers to the natural rate, and then stays low for at least four years. The only plausible example is 1966-69, but that wasn’t really a soft landing because it came at the expense of rapidly accelerating inflation. The plane soared off into the stratosphere before the wheels even touched the runway. Otherwise, we have only a year or two of stable and low unemployment, before the next recession.

So 90% of the time we are either recovering (mostly with a normal yield curve) or in recession (mostly with a normal yield curve.) Inverted curves tend to occur right before a recession, when unemployment is low. But what if we did have a true soft landing—persistent low unemployment without accelerating inflation? Would the yield curve be flat? After all, when output is already near the natural rate, you don’t expect further recovery. You don’t expect the future economy to be better (stronger) than the present.

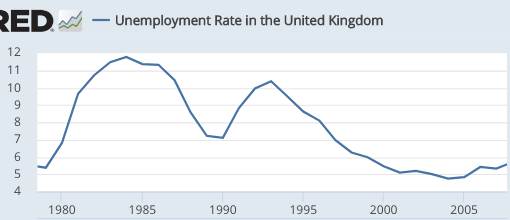

So I decided to seek out a country that did have a soft landing—Britain from 2001-08:

Notice that in 1991, the UK entered recession almost immediately after the unemployment rate stopped falling—the US pattern. But in 2001, unemployment reached the low 5s and stayed near there until mid-2008. So how about the UK yield curve? Below I have data from 2000-08, using June data in each case. The first number is the nominal yield on 6-month UK T-bonds, and the second number is the yield on 10-year bonds. I’m not used to using UK data, so someone tell me if I made a mistake:

2000: 6.0%, 4.13%

2001: 5.33%, 4.92%

2002: 4.38%, 4.80%

2003: 3.19%, 4.87%

2004: 4.89%, 4.93%

2005: 4.16%, 4.28%

2006: 4.70%, 4.47%

2007: 5.85%, 4.94%

2008: 5.26%, 5.12%

During these 9 years, the UK yield curve was slightly inverted, on average. But pretty close to flat. This suggests that a flat yield curve might be expected when the economy is still expanding, but the unemployment rate is not expected to fall much further.

Note that the US yield curve was pretty flat in May 2006, when unemployment had fallen to 4.6% and was expected to stay around that level. And unemployment did stay around that level for another 18 months. The yield curve was also fairly flat in 1966. The yield curve today slopes gradually upward, but it’s flat between 2 years and 5 years, which suggests to me that markets may be expecting the US to achieve a soft landing.

The unemployment rate today (4.0%) is not much different from 15 months back (when it was 4.1%.) I expect it to fall a few more ticks (the trend is actually in the high 3s), but then stop falling. If I’m right that the US will achieve its first ever non-inflationary soft landing, then I’d expect a pretty flat yield curve to be the new normal. There’d still be a slight tendency for an upward slope, but not much.

Of course this happy scenario assumes that the Fed keeps NGDP growing at a reasonably steady rate (say a range of 3% to 5%). There are no guarantees, but they seem to be trying to do something like that in recent years, even if they don’t admit it.

Tags:

25. February 2019 at 13:22

I’m sympathetic to the non-inflationary soft landing story.

25. February 2019 at 13:37

Good post.

“If I’m right that the US will achieve its first ever non-inflationary soft landing, then I’d expect a pretty flat yield curve to be the new normal. There’d still be a slight tendency for an upward slope, but not much.”

I think we’re there. Good job Fed.

Better than May of 2006, when the Fed responded to a flat yield curve with yet another hike in the FFR (to 5.25%!), creating the inversion. Because, you know, we had to store up ammo for the recession we were precipitating.

25. February 2019 at 15:53

This may be another case in which empirical observations trump economic theory.

Or we need a new theory as to why people would be willing to lend short or long at the same interest-rate. What happened to the term premium?

There has been the emergence and rapid growth of bond funds.

This allows investors to invest short, that is stay liquid, while invested in long-term bonds. I suppose if such bond funds are large and ubiquitous, they could help blur the difference between long and short-term rates.

As an aside, Fitch Rating has fretted that such bond funds may collapse, if for some reason they suffer an investor run. The bond funds would be attempting to sell bonds into an illiquid market for long-term bonds, or sell at a large loss.

25. February 2019 at 16:28

“The Phillips curve is the connective tissue between the Federal Reserve’s dual mandate goals of maximum employment and price stability.”

FRBNY President John C. Williams, USMPF Discussion, February 22, 2019.

“The White House wants highly capable, competent people who understand that you can have strong economic growth without higher inflation.” White House National Economic Council head Lawrence Kudlow, cited in The Wall Street Journal, January 24, 2019

–30–

So who is right on this one? The dunderheads in the Trump White House or the New York Fed president?

Egads….

https://www.moneyandbanking.com/commentary/2019/2/24/inflation-risks-and-inflation-expectations

25. February 2019 at 16:28

Scott,

A priori, why should a yield curve be flat? Sure, maybe flat is normal if real potential GDP growth is expected to be lower in the future, but that certainly wouldn’t have applied in the 60s as it night today. Shouldn’t there be temporal discounting of future interest payments?

26. February 2019 at 05:13

Risk premium will be normal as long as human nature values profit. The BOJ’s ZIRP has tried to contravene the profit motive for 2 decades – causing stagnation (and multiple recessions, btw).

It’s true that the Fed thinks prosperity somehow boosts prices. But the ’70s saw simultaneously high unemployment and high inflation; the ’90s saw neither. But the Fed’s choice of complexification over empirics and analytic parsimony renders it unable or unwilling to distinguish causes from consequences. That’s why Yellen found inflation of 1.9% and unemployment of 4.4% “a mystery” some 16 months ago (and hiked rates anyway). Those who rely on the Fed and its false textbook theories will get burned.

https://imfcinc.com/main/how-to-forecast-inversion-recession/

26. February 2019 at 09:33

Michael, I’m not saying perfectly flat, just relatively flat. And I’m saying that only if we have a soft landing, which so far the US has never had. Thus we have zero US evidence on what the yield curve would look like with a soft landing, only UK evidence.

26. February 2019 at 10:32

Scott,

Yes, the more I look at data, the more I respect what you’ve been saying for years about interest rates. The time value of money implicit in yield curves is just another hidden variable. How does it vary over time, if it does, and under what circumstances? This is what makes macro such a challenging field, along with the paucity of relevant data.

26. February 2019 at 11:17

This makes sense to me. On average in the low unemployment and stable I think the yield curve should have a little steepness to it. Just for risks premium reasons.

However, a lot of it depends on the risks preferences of a lot of different financing vehicles. Are there more borrowers who want to borrow long and remove risks than insurance companies that want to lock in yield? (it becomes a thing of summing up the risks between borrowers and lenders).

It should also oscillate slightly around the normal interest rate that generates stable NGDP growth with 2% long-term inflation. Small fluctations in the short term rate to even out small moves in the economy and keep it on track.

26. February 2019 at 13:44

1995 was a soft landing. At least it was considered a soft landing a the time.

26. February 2019 at 14:13

Doug, Yes, it was viewed that way, but it wasn’t. Unemployment kept falling for 5 more years.

26. February 2019 at 16:05

You know, the rapid emergence of bond funds, which allow investors to invest short but obtain long-term yields, should flatten the yield curve. As a larger portion of bond investors attempt to invest short but get the long-term yields, the long-term yields will migrate lower.

Fitch Ratings says the emergence of such bond funds promises financial instability. They can be subject to runs, which would force the bond funds to unload bonds. If everybody heads for the exits at once…

I wonder if because the US now goes a long time between recessions, financial institutions emerge which are in fact very vulnerable to a recession, but have never been tested. This means in the US that each recession will result in the collapse of certain financial institutions as well.

26. February 2019 at 17:13

Australia’s yield curve is also pretty flat today. 10 year minus central bank rate is only 0.56%.

I’m sure the Fed Funds rate/NGDP growth rate graph has been posted somewhere here before. I’m sure it has and I missed it, but the correlation between Fed Funds rate and NGDP growth rate is often eerily strong in the short-run.

https://fred.stlouisfed.org/graph/?g=n6ul

The Fed also did a poor job moderating NGDP. Expansions were overheated and recessions underheated. Paradoxically, *willingness* to more quickly adjust Fed Funds rates in the past would have smaller swings in Fed Funds rates.

The market in 2006 and today assumes the Fed has less institutional conservatism giving rise to these lags. The 2006 market could have been correct if the natural rate did not go below the zero-bound in Sep 2008. Hopefully the market is correct today.

27. February 2019 at 06:59

Ben,

“You know, the rapid emergence of bond funds, which allow investors to invest short but obtain long-term yields…”

This animal does not exist. CDs and GICs do, but you can’t get long-term yields without some lock-up provision.

27. February 2019 at 12:11

Brian,

Mutual Fund bond funds have to redeem at NAV every day.

For the Reserve Primary Fund, the custodian bank State Street suspended withdrawals. Investors got 96 cents on the dollar a few months later. All mutual fund prospectuses have provisions for in-kind redemptions in case of a run on the fund.

I do not think the same bank run dynamics exist for long-term bond funds though.

27. February 2019 at 15:48

https://en.m.wikipedia.org/wiki/Bond_fund

Brian….?

Why is Fitch Ratings issuing reports that there is a danger of bond fund runs?

27. February 2019 at 18:07

Brian:

Fitch Ratings: Open-Ended Bond Funds a Potential Risk to Financial Stability

06 FEB 2019 03:30 AM ET

Link to Fitch Ratings’ Report(s): The Coming Storm: Bond Funds’ Potential Impacts on Financial Stability

“Fitch Ratings-London/New York-06 February 2019: Open-ended bond funds are a potential risk to global financial stability given their rapid growth and increasing liquidity mismatches and credit risk, Fitch Ratings says in a new report.

Open-ended bond funds provide daily liquidity for investors but are increasingly investing in longer-dated or lower-quality securities as bank regulation has reduced the supply of market liquidity and investors are seeking extra yield while interest rates remain low. This exposes funds to liquidity pressure if there is a spike in redemptions, potentially leading to forced asset sales and a run on the fund as investors pull out. The risks are most pronounced in purely credit-focused funds with less-liquid underlying assets, such as corporate loans and bonds. We estimate pure credit funds are about 15% of total global bond funds.

A market stress emanating from open-ended bond funds could spread to other financial institutions and affect financial stability, given the interconnectedness among funds, banks, non-bank financial institutions (NBFIs) and the rest of the financial market. Transmission to other institutions could be as a result of market value declines in the types of collateral that they have in common with the funds. Banks and NBFIs could also be exposed through their short-term funding reliance on the funds or other counterparty exposure to them.”

—30—

Brian, maybe Fitch is mistaken? Please explain.

BTW, my point is that if a new financial instrument emerges and becomes very prominent, such as open-ended bond funds that intermediate between short-term lenders and long-term borrowers, then you can have a blurring of short and long-term rates—-a flattening of the yield curve.

In this way, an institutional evolution and market-reality will undercut the theoretical norm that there should be a term premium, or higher long-term rates.

This seems to make sense to me…..

28. February 2019 at 06:41

It sounds like these funds are trying to deliver long-term yields plus liquidity plus capital preservation.

This is not something offered in any capital market, so by definition, there are other, unconsidered, risks in this bundle.

28. February 2019 at 08:12

Brian–

Indeed, Fitch ratings says such bond funds are risky not only to investors but to the entire financial system.

But who knows, long-term rates may continue to fall ’till they reach zero also, along with short-term rates. Then the paper dollar bill and a 30 year bond will be the same.

The federal government can buy back all the debt, and presto-changoh we get a “Get out of Debtor’s Prison Free Card.”

Well, something close to that is going on in Japan.

28. February 2019 at 11:45

“This is not something offered in any capital market”

It *should* not be offered in any capital market, but borrow short and lend long is the perpetual vice of capital markets.

For example, I came across this paper on AIG by Mercatus. AIG’s fall is blamed on AIGFP, but a bigger story was the securities lending by the insurance subsidiaries. The major life insurance subsidiaries essentially became banks which took in overnight deposits from Wall Street and invested in residential MBS.

https://www.mercatus.org/publication/securities-lending-and-untold-story-collapse-aig

MMFs and the five big investment banks also borrowed short and lent long. True banks (with OCC or state charters) borrow short and lend long, but they had access to the discount window. In 2007-08, non-bank banking essentially caused the financial crisis.

I do not know if bond fund investors have similar mentality to MMF. If they do, then they should take losses as MMF investors should have taken losses in 2008. The Fed can offset the panic in such bond funds, should such a panic occur.

28. February 2019 at 12:37

Thanks Scott for some additional info on the yield curve issue.

I’m curious about the quantities. Do these different yield-curve regimes (sloping, flat, inverted) correspond to different relative quantities across the different terms? We don’t want to reason from a price change, after all.

28. February 2019 at 16:17

Matthew Waters—

You summed it up nicely.

The best idea is to get a hold of some capital, leverage up 100 to 1, and then invest in the spread between short and long-term rates.

28. February 2019 at 18:01

myb6, I’d expect quantity plays some role, indeed QE was trying to change the relative quantities.

28. February 2019 at 20:26

When paper cash is a 10-year Treasury note.

The above seems like gibberish. Maybe it is. Or maybe it should read, “When paper cash offers a higher return that a 10-year bond.”

But in Japan right now the interest rate on 10-year sovereign bond is…negative 0.017%.

Japanese get a better return on paper money in a desk drawer, than on a 10-year government bond. And that is before transaction costs.

Europe seems to be getting close to Japan. In the next recession, the US?

When a nation pays negative interest to borrow money, what means the national debt? Could the national debt just be wiped out?

Does conventional macroeconomics answer such riddles?