Nick Rowe on the New Keynesian model

Here’s Nick Rowe:

I understand how monetary policy would work in that imaginary Canada (at least, I think I do). Increasing the quantity of money (holding the interest rate paid on money constant) shifts the LM curve to the right/down. Increasing the rate of interest paid on holding money (holding the quantity of money constant) shifts the LM curve left/up. Done.

It’s a crude model of an artificial economy. But it’s a helluva lot better than a simple New Keynesian model where money (allegedly) does not exist and the central bank (somehow) sets “the” nominal interest rate (on what?).

I think this is right. But readers might want more information. Exactly what goes wrong if you ignore money, and just focus on interest rates? Let’s create a simple model of NGDP determination, where i is the market interest rate and IOR is the rate paid on base money:

MB x V(i – IOR) = NGDP

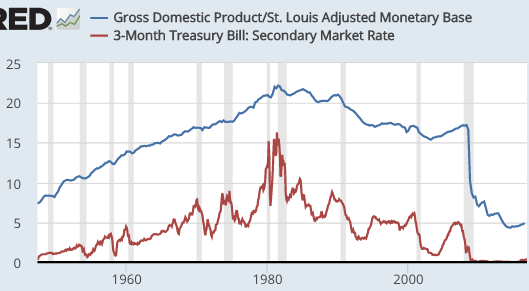

In plain English, NGDP is precisely equal to the monetary base time base velocity, and base velocity depends on the difference between market interest rates and the rate of interest on reserves, among other things. To make things simple, I’m going to assume IOR equals zero, and use real world examples from the period where that was the case. Keep in mind that velocity also depends on other factors, such as technology, reserve requirements, etc., etc. The following graph shows that nominal interest rates (red) are positively correlated with base velocity (blue), but the correlation is far from perfect.

[After 2008, the opportunity cost of holding reserves (i – IOR) was slightly lower than shown on the graph, but not much different.]

What can we learn from this model?

1. Ceteris paribus, an increase in the base tends to increase NGDP.

2. Ceteris paribus, an increase in the nominal interest rate (i) tends to increase NGDP.

Of course, Keynesians often argue that an increase in interest rates is contractionary. Why do they say this? If asked, they’d probably defend the assertion as follows:

“When I say higher interest rates are contractionary, I mean higher rates that are caused by the Fed. And that requires either a cut in the monetary base, or an increase in IOR. In either case the direct effect of the monetary action on the base or IOR is more contractionary than the indirect effect of higher market rates on velocity is expansionary.”

And that’s true, but there’s still a problem here. When looking at real world data, they often focus on the interest rate and then ignore what’s going on with the money supply—and that gets them into trouble. Here are three examples of “bad Keynesian analysis”:

1. Keynesians tended to assume that the Fed was easing policy between August 2007 and May 2008, because they cut interest rates from 5.25% to 2%. But we’ve already seen that a cut in interest rates is contractionary, ceteris paribus. To claim it’s expansionary, they’d have to show that it was accompanied by an increase in the monetary base. But it was not—the base did not increase—hence the action was contractionary. That’s a really serious mistake.

2. Between October 1929 and October 1930, the Fed reduced short-term rates from 6.0% to 2.5%. Keynesians (or their equivalent back then) assumed monetary policy was expansionary. But in fact the reduction in interest rates was contractionary. Even worse, the monetary base also declined, by 7.2%. NGDP decline even more sharply, as it was pushed lower by both declining MB and falling interest rates. That’s a really serious mistake.

3. During the 1972-81 period, the monetary base growth rate soared much higher than usual. This caused higher inflation and higher nominal interest rates, which caused base velocity to also rise, as you can see on the graph above. Keynesians wrongly assumed that higher interest rates were a tight money policy, particularly during 1979-81. But in fact it was easy money, with NGDP growth peaking at 19.2% in a six-month period during late 1980 and early 1981. That was a really serious error.

To summarize, looking at monetary policy in terms of interest rates isn’t just wrong, it’s a serious error that has caused great damage to our economy. We need to stop talking about the stance of policy in terms of interest rates, and instead focus on M*V expectations, i.e. nominal GDP growth expectations. Only then can we avoid the sorts of policy errors that created the Great Depression, the Great Inflation and the Great Recession.

PS. Of course Neo-Fisherians make the opposite mistake, forgetting that a rise in interest rates is often accompanied by a fall in the money supply, and hence one cannot assume that higher interest rates are easier money. Both Keynesians and Neo-Fisherians tend to “reason from a price change”, ignoring the thing that caused the price change. The only difference is that they implicitly make the opposite assumption about what’s going on in the background with the money supply. Although the Neo-Fisherian model is widely viewed as less prestigious than the Keynesian model, it’s actually a less egregious example of reasoning from a price change, as higher market interest rates really are expansionary, ceteris paribus.

PPS. Monetary policy is central bank actions that impact the supply and demand for base money. In the past they impacted the supply through OMOs and discount loans, and the demand through reserve requirements. Since 2008 they also impact demand through changes in IOR. Thus they have 4 basic policy tools, two for base supply and two for base demand.

PPPS. Today interest rates and IOR often move almost one for one, so the analysis is less clear. Another complication is that IOR is paid on reserves, but not currency. Higher rates in 2017 might be expected to boost currency velocity, but not reserve velocity. And of course we don’t know what will happen to the size of the base in 2017.

Tags:

17. December 2016 at 08:07

Interest on EXCESS reserves is just a tool to help control the Federal funds rate, as the Fed itself (and Bernanke) has repeatedly made clear, and as is constantly pointed out to you. Why do you continue to make a big deal over this?

17. December 2016 at 08:10

Stalin, Did you leave this at the wrong post, or are you just trying to copy Ray Lopez?

17. December 2016 at 08:10

(A small point:) “Monetary policy is central bank actions *or inactions* that impact the supply and demand for base money” (my insertion). The distinction between *action* and *inaction*, however precisely that is to be drawn, is not significant for assessing monetary policy.

17. December 2016 at 08:14

Philo, Fair point.

17. December 2016 at 09:57

Thanks Scott. Lovely and clear.

17. December 2016 at 11:27

The decision to start paying IOR in 2008 is one of the biggest unforced, policy blunders in history.

17. December 2016 at 11:59

As you’ve often said with monetary policy, it all depends on the yardstick or counterfactual. With your examples, because you’ve put the focus on interest rates, the reader naturally assumes that the counterfactual is no change in official interest rates. For example, in (1), surely the cut in the Fed Funds rate from 5.25% to 2% was less contractionary than if the Fed did not lower the rate? The money supply may not have risen in 2007-08, but wouldn’t it have fallen if rates were kept at 5.25%, as the market devoured the short-term securities the Fed offered at that yield? I understand that the reduction in official rates was not expansionary in any meaningful sense (ie against a benchmark of ideal monetary policy under inflation or NGDP targeting).

17. December 2016 at 12:37

‘To summarize, looking at monetary policy in terms of interest rates isn’t just wrong, it’s a serious error that has caused great damage to our economy. We need to stop talking about the stance of policy in terms of interest rates….’

That sounds familiar.

It’a also what should be put into that open letter to President Trump, you’re going to write for the WSJ.

17. December 2016 at 12:55

Or, in other words, don’t reason from a price change 🙂

17. December 2016 at 13:02

Very good post.

It’s also what should be put into that open letter to President Trump, you’re going to write for the WSJ.

They got Larry Kudlow in Team Trump now. This is not about letters to the WSJ anymore. They should be aiming for Scott Sumner as FED chairman in 2018. Anything less than that would be a bummer. I take this post as his first letter of application. Call up Trump, the deal is settled.

17. December 2016 at 14:20

Rajat, See my new post.

17. December 2016 at 15:32

“To summarize, looking at monetary policy in terms of interest rates isn’t just wrong, it’s a serious error that has caused great damage to our economy”

————

It’s more incongruous than that. Interest is the price of loan-funds. The price of money is the reciprocal of the price-level. And the money stock can never be managed by any attempt to control the cost of credit. The Gurley-Shaw liquidity dogma is specious.

Money times velocity = AD (not N-gDp – as Keynesian economists define it).

Thus, using rates-of-change in M*Vt, i.e., the proxy for inflation, Greenspan NEVER tightened (despite 14 raises in the target rate, FFR: June 30, 2004 until January 31, 2006) and Bernanke NEVER eased (despite the 7 reductions in the target, FFR (which began on 9/18/07 until 4/30/08).

And the perverse focus on rates, and not AD, is also the source of secular strangulation.

DD Vt peaked in 1981, coterminous with interest rates.

During the acceleration in money velocity from 1965-1981, principally due to financial innovation (the monetization of time deposits), Vt increased at an average annual rate of approximately 5 percent per year. During the same period, Vi increased at an average annual rate of approximately 2 percent per year.

But what is more material, and has been concealed since Larry Summer’s secular stagnation hypothesis: Vi, a contrived metric, didn’t change, but Vt fell by 62 percent over the next (same) 15 year period (until the G.6 release was discontinued, due to Bill Clinton’s Paperwork Reduction Act of 1995).

– Michel de Nostredame

17. December 2016 at 18:15

Flow5 (aka Michel de Nostredame)…all I want to know is this.. …do you have any stock picks for the upcoming year? You said this was a fool’s rally…where are you putting your money?

I am quite sure that the 300 PhDs at the FED have no idea. What about the 3000 quants on Wall Street…they don’t seem to have a clue either…

17. December 2016 at 18:51

“It’s a crude model of an artificial economy” – says Nick Rowe, and Sumner analyzes this crude model. But why bother with crude models when you can do an econometrics analysis of every Fed shock from 1959 to 2001, as Ben S. Bernanke et al did in their 2002 FAVAR paper, and find that Fed shocks account for a mere 3.2% to 13.2% (out of 100%) of the change of a variety of economic variables, including GDP, over this period? In other words, money is largely neutral short term and long. Accept it, deal with it, move on. The quantity theory of money was invented well over 200 years ago by David Hume et al. We don’t believe in mercantilism anymore, nor bleeding in medicine, yet you cultards believe in what your guru Sumner says uncritically about an obsolete doctrine disproved by modern statistics? Wow. Friedman might even roll out of his grave on that one (well, maybe not, he was pretty closed minded too).

19. December 2016 at 10:54

You’re, once again lost Mr. Lopez. And you quote an economist who should be in prison for treason, for being solely responsible for the GR. Bernanke doesn’t know money from mud pie. Neither do you or Nick Rowe.

Go fish.

19. December 2016 at 10:57

You, Nick Rowe, and Bankrupt u Bernanke can’t forecast.

19. December 2016 at 10:58

If you can’t forecast, you don’t understand economics. It’s that simple.

19. December 2016 at 11:04

Every year, the seasonal factor’s map, or scientific proof, is demonstrated by the product of money flows.

Scientific evidence “is proof, which serves to either support or counter a scientific theory or hypothesis. Such evidence is expected to be empirical evidence and in accordance with scientific method” – Wikipedia

Scientific method is “a method or procedure…consisting in systematic observation, measurement, and experiment, and the formulation, testing, and modification of hypotheses” – Wikipedia

“The scientific evidence for the last 100 years is irrefutable. I.e., the trajectory in the roc (proxy for real-output indices), for M*Vt (the scientific method), projected a bottom in economic activity in February (signal to buy stocks).”

– Michel de Nostradame

19. December 2016 at 11:11

Bankrupt-u-Bernanke, a Harvard graduate, Summa Cum Laude, and Phi Beta Kappa, (with 1975’s best undergraduate economic thesis), a MIT Ph.D. graduate student (where he “taught a highly mathematical economics course to undergraduates”, “the perfect place for a blossoming of quantitative approaches”), and a Stanford Graduate School of Business from 1979 until 1985, was a visiting professor at New York University and went on to become a tenured professor at Princeton University in the Department of Economics, didn’t understand “leverage” (but claimed he understood “the notion that wages and at least some prices are “sticky”).

The Fed Chairman drained Yale Professor Irving Fisher’s “price-level” or bank’s, non-bank’s, and E-$, liquidity for 29 contiguous months. Then as the FOMC deliberated, the “Hawks” prevailed, and the rate-of-change in money flows, proxy for real-output, was allowed to collapse after July 2008, creating a 4th qtr. negative roc in R-gDp. Then BuB destroyed non-bank lending/investing by remunerating IBDDs.

“The central bankers did precious little to prevent the financial crisis”, indeed, BuB was the sole cause of the GR:

2006 jan ,,,,,,, 0.04

,,,,, feb ,,,,,,, 0.01

,,,,, mar ,,,,,,, -0.02

,,,,, apr ,,,,,,, -0.03

,,,,, may ,,,,,,, -0.02

,,,,, jun ,,,,,,, -0.01

,,,,, jul ,,,,,,, -0.03

,,,,, aug ,,,,,,, -0.06

,,,,, sep ,,,,,,, -0.08

,,,,, oct ,,,,,,, -0.08

,,,,, nov ,,,,,,, -0.06

,,,,, dec ,,,,,,, -0.07

2007 jan ,,,,,,, -0.11

,,,,, feb ,,,,,,, -0.09

,,,,, mar ,,,,,,, -0.11

,,,,, apr ,,,,,,, -0.09

,,,,, may ,,,,,,, -0.05

,,,,, jun ,,,,,,, -0.05

,,,,, jul ,,,,,,, -0.08

,,,,, aug ,,,,,,, -0.07

,,,,, sep ,,,,,,, -0.07

,,,,, oct ,,,,,,, -0.04

,,,,, nov ,,,,,,, -0.04

,,,,, dec ,,,,,,, -0.04

2008 jan ,,,,,,, -0.07

,,,,, feb ,,,,,,, -0.05

,,,,, mar ,,,,,,, -0.04

,,,,, apr ,,,,,,, -0.03

,,,,, may ,,,,,,, -0.01

,,,,, jun ,,,,,,, -0.04

,,,,, jul ,,,,,,, -0.03

19. December 2016 at 11:49

The Fact is that BuB caused the GR all by himself. And then he remunerated IBDDs.

Anyone that advocates the remuneration of IBDDs doesn’t know:

1 the difference between the supply of money & the supply of loan funds.

2 the difference between means-of-payment money & liquid assets.

3 the difference between financial intermediaries & money creating institutions.

4 doesn’t recognize that interest rates are the price of loan-funds, not the price of money

5 doesn’t recognize that the price of money is represented by the various price (indices) level.

19. December 2016 at 14:16

“Fed shocks account for a mere 3.2% to 13.2% (out of 100%) of the change of a variety of economic variables, including GDP, over this period?”

————-

Here’s who caused our recessions since the Great-Depression:

Period…………… Chairman

Nov 1948 – Oct 1949… Thomas B. McCabe

July 1953 – May 1954… William M. Martin

Aug 1957 – Apr 1958… William M. Martin

Apr 1960 – Feb 1961… William M. Martin

Dec 1969 – Nov 1970… William M. Martin

Nov 1973 – Mar 1975… Arthur Burns

Jan 1980 – July 1980… Paul Volcker

July 1981– Nov 1982… Paul Volcker

July 1990 – Mar 1991… Alan Greenspan

Mar 2001 – Nov 2001… Alan Greenspan

Dec 2007 – Jun 2009… Ben Bernanke

I.e., all these recessions were both predictable and preventable.

19. December 2016 at 14:18

Monetary policy objectives should be formulated in terms of desired rates-of-change, roc’s, in monetary flows, M*Vt (our means-of-payment money times its velocity of circulation), relative to roc’s in R-gDp.

Roc’s in N-gDp (though “raw materials, intermediate goods and labor costs, which comprise the bulk of business spending are not treated in N-gDp”), can serve as a proxy figure for roc’s in all transactions, P*T, in Yale Professor Irving Fisher’s truistic “equation of exchange” (where the proper index # provides clues to the overall economies’ “price-level”).

Roc’s in R-gDp have to be used, of course, as a policy standard.

This is inviolate and sacrosanct (tested with time for over 100 years (unbeknownst to the 300 Ph.Ds. employed on the Fed’s technical/research staff).

– Michel de Nostradame

19. December 2016 at 14:20

“Accept it, deal with it, move on.”

———-

You’ve got life back asswards. You have absolutely no proof. You’ve just got a big mouth.

25. December 2016 at 16:02

Thought: without further planned action, won’t reducing the interest rate increase the monetary base in and of itself (and the other way around)? So, won’t cutting the rate be expansionary in the short-term (larger base right now) and actually reduce (all right, let it increase by less) NGDP in the longer-term? Once you start cutting rates to get out of a tight spot, won’t you need to cut again once said long term arrives. And then again, again, again until you hit zero? If that is so, playing with the interest rate and leaving the base to adjust on its own is a self-defeating game.