Natural experiments: Can we handle the truth?

Natural experiments are being conducted all the time. And yet I often feel like people really don’t care about the outcome of these experiments.

Let’s consider 5 popular hypotheses:

1. The mortgage interest deduction has a major impact on the housing market.

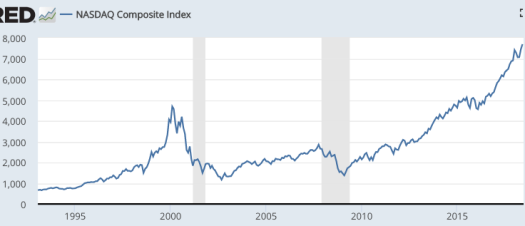

2. The NASDAQ was obviously wildly overvalued in 2000.

3. Switzerland was forced to revalue its currency in January 2015.

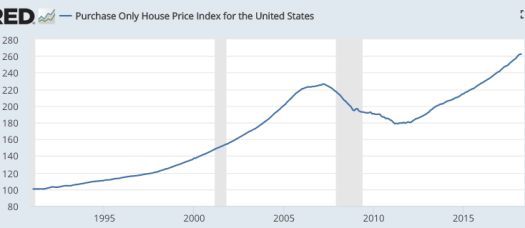

4. The US housing market was obviously wildly overvalued in 2006.

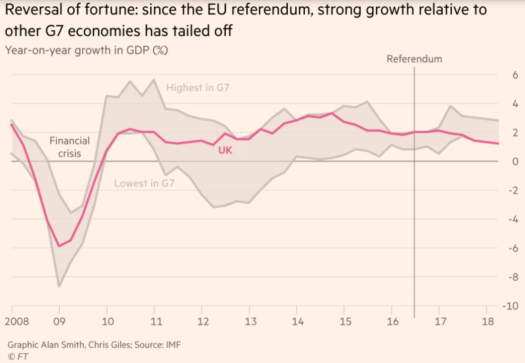

5. Brexit would cause a recession in the UK economy.

In my view, natural experiments have strongly suggested that all 5 of these hypotheses are false. And these are not trivial unimportant hypotheses, they were widely held views about some really important issues.

1. The tax bill that passed last year sharply cut back on the mortgage interest deduction. Before that happened I read about 1000 articles warning that if we took away this deduction it would severely hurt the housing market. We didn’t completely eliminate the deduction, but it’s more than half gone. And yet housing continues to boom. I have yet to see a single news article discussing this important natural experiment.

2. The Nasdaq is now far higher than in 2000. Of course it could be wildly overvalued today. Unlike in 2000, however, there is no widely held view that it is wildly overvalued today. That’s a problem for the hypothesis that it was wildly overvalued in 2000. If true, why don’t people feel that way about the current stock market? And you can’t point to changing economic circumstances, such as lower nominal interest rates, as those factors are linked to other changing economic circumstances, such as an unexpected slowdown in trend NGDP growth. I.e. where would Nasdaq be today if NGDP had grown during 2000-18 as rapidly as people expected back in 2000? Maybe 10,000?

3. Tyler Cowen correctly noted that Denmark would provide a good test of whether Switzerland was forced to revalue in January 2015. We now know that Denmark was not forced to revalue. Even worse, evidence suggests that the Swiss revaluation did not have the intended impact on the SNB balance sheet, which kept growing. That was claimed as the reason the Swiss needed to revalue. And yet despite this natural experiment, experts continue to claim that the Swiss were forced to devalue, as in this recent podcast. It seems obvious to me that the Swiss simply made a mistake—are there any good counterarguments?

4. There are two powerful pieces of evidence against the claim that the US housing market was overvalued. First, many who made that claim also said the same thing about housing markets in Canada, Australia, the UK, and other countries. And yet many of those other countries did not crash. Even worse, America’s housing market has mostly recovered, and yet I see almost no one currently saying “America’s in a huge housing bubble, and when it crashes we’ll have another Great Recession”. So why continue to claim the 2008 recession was caused by a housing bubble that no longer even looks like a bubble at all? (And don’t point to housing construction; that’s shifting the goalposts. In 2008, everyone pointed to the historically high level of house prices in 2006; housing construction never reached unusual levels during the boom.)

5. This one hasn’t been entirely ignored, as the Brexit supporters pointed to a strong economy after the June 2016 vote. The Financial Times claims that Brexit is now slowing British growth:

In my view it’s too soon to claim that Brexit is slowing growth. I expect it will, but the graph the FT presents does not look statistically significant to me.

Ditto on the recent corporate tax cut—it’s too soon. Both supply-siders and Keynesians expected a short term boost to growth, for different reasons. Only the supply-siders predicted a longer term boost. My own view was somewhere in between. I expect some sort of long run supply-side boost, but much less that the Larry Kudlows of the world expect. I see perhaps an extra 2% in RGDP growth spread out many years, with most of the boost coming soon after the tax cut. Supply-siders see the growth rate rising to a new trend of roughly 3%/year, which seems unlikely to me. If growth is still running at 3% in late 2019, then I clearly will have underestimated its impact. I hope I did.

I’ve done a number of previous posts on this general topic, discussing earlier experiments such as the 2013 fiscal austerity, and the 2014 elimination of extended unemployment benefits. Those who suggested that these would be good natural experiments often ignored the results when they didn’t go as expected. (GDP growth accelerated in 2013, and job growth accelerated in 2014.)

Many pundits can’t handle the truth, unless it confirms their prior beliefs.

Tags:

28. June 2018 at 22:26

The FT should be comparing UK growth against the predictions of the Treasury, which it reported uncritically at the time:

‘The analysis in this HM Treasury document quantifies the impact of that adjustment

over the immediate period of two years following a vote to leave… The central conclusion of the analysis is that the effect of this profound shock would be to push the UK into recession and lead to a sharp rise in unemployment.’

It’s quite a read at this point

https://www.gov.uk/government/publications/hm-treasury-analysis-the-immediate-economic-impact-of-leaving-the-eu

28. June 2018 at 23:30

For NASDAQ, it includes dividends. From the very peak in 2000, the return has been 2.3% or (1.6)^(1/18) – 1. T-bills yielded 6%. A 100% return over 18 years is 3.9%. A 10 year bond bought in 2000 appreciated by 60%, with zero reinvestment.

Housing has “dividends” through actual or imputed rent. Housing prices also have more interest rate sensitivity, since future rents are nearly a perpetuity. In 2006, 10 year Treasuries were 5%. So that’s a 50% return with no reinvestment.

With reinvesting, these returns go way up.

29. June 2018 at 02:18

I’m sceptical of stock market indices like NASDAQ. How can an index like NASDAQ not rise when you kick out the losers all the time?

Those indices are like: “We kicked all the big losers in hindsight and to our enormous surprise that lead to a really nice graph with a lot of big winners but no big losers.”

Really surprising indeed. I’m shocked.

29. June 2018 at 02:39

US GDP growth was 2,224% in 2012 and 1,677% in 2013 (World Bank). I don’t understand why you say that growth accelerated.

29. June 2018 at 02:58

Silly question: if the housing bubble didn’t cause the great recession, what did?

29. June 2018 at 06:45

I think you should consider the Nasdaq level in light of 18 years worth of a (compounded) discount rate.

29. June 2018 at 07:19

Professor, I am generally in completer accord with your views but I am feeling a little different about your thoughts in the NASDAQ. Many e-commerce, or what people thought would be e-commerce stocks, were shooting up a thousand percent in a span of a couple of days to subsequently come crashing down and eventually to zero. I don’t believe in bubbles but I do believes the market was being priced to irrational expectations at the time. So why can’t one say the market is “overpriced” at a particularly point in time? I don’t think its accurate to answer the questions saying that the market is now higher, because its only natural in a growing economy with a rising and somewhat stable NGDP that “the market” eventually continue higher. What I am trying to get at, is the following: you sometimes dismiss downturn rationalizing the drop by saying “We simply went down to where we were a couple of months ago”. The problem I see with this arguments is that we can’t compare price points over large time frames because the company economics are much different. If it where acceptable to referee to the markets price in absolute terms, then how bad would a market drop have to be to be considered “significant”? Would you not consider a drop to 2014 levels significant? Even if it would represent about the same percentage drop to the 2008 recession, but in absolute terms it would be higher than the 2007 high. Also, I am not trying to say stocks were a bubble or overpriced in 2008, just using it because its the most recent market drop I would consider significant.

Your thoughts are much appreciated.

29. June 2018 at 07:22

Regarding the housing market, the changes to SALT deduction seem like a bigger deal than MI ded going from 1M to 750k.

Maybe we’ll start to see some effects here when tax filers get smaller refunds in 2019.

29. June 2018 at 07:33

I was doubly wrong on the mortgage interest thing. I thought it would be a massive political battle to get rid of it, or even cut it. And I thought it would have big effects on house prices, at least temporarily. I can live with getting the politics wrong, but I can’t figure out the economic effects (or apparent absence or small size thereof).

I wasn’t so wrong about the others.

29. June 2018 at 08:03

Regarding NASDAQ, I’m not so confident that graph supports the idea that the circa-2000 level was a reasonable price. Certainly, if you had given that graph to me in 2000 I would not have thought “buy and hold” a reasonable strategy.

Regarding the mortgage interest deduction, it might be that would-be homeowners are insensitive to the deduction so it acts inframarginally.

This might make sense if homeowners are collectively greedy and want to buy the largest home they can loan-qualify for. Do mortgage lenders take the interest deduction into account when setting qualification standards? If not, the mortgage interest deduction can act only via the income effect.

Note that this seems to be consistent with the Canadian experience, where regulations that force tighter loan standards have modestly slowed the real-estate market.

29. June 2018 at 08:04

Christian, You said:

“How can an index like NASDAQ not rise when you kick out the losers all the time?”

I think you’d really benefit from taking a course in finance, with a special focus on the EMH.

Arilando, You are using year over year figures, which are inappropriate for an austerity that began in January 2013. Look at the quarterly data and you’ll see what I mean.

Much of the 1.677% figure you cite occurred in the second half of 2012, before the austerity.

Gabriel, A tight money policy which caused NGDP to fall 8% below trend.

Brent, I did.

Rodrigo, You asked:

So why can’t one say the market is “overpriced” at a particularly point in time? ”

In retrospect it may be overpriced. My point is that the bubble theory claims it was OBVIOUSLY over priced at the time. And that doesn’t seem clear at all.

Nick, I also didn’t expect the real estate lobby to lose on this issue.

I didn’t have a good sense of how much it would slow the housing market, but so far it’s been less than I would have expected. Of course there’s always the ceteris paribus problem (i.e. RGDP growth is strong), so it’s hard to know for sure. But I suspect the impact was pretty mild.)

29. June 2018 at 08:14

The 2008 financial collapse was the symptom of a fundamentally unstable mortgage finance system and over-levered banking sector. It has been been this way for at least a decade or two. It only took a small shock to tip it over. Housing did not have to be radically over valued to trigger this shock.

I seem to remember our professor arguing that the Swiss had to devalue. I didn’t follow the logic. But all of those arguments should be archived somewhere on this site. It would be cool if someone with more energy than I were to make a round-up of the comments at the time, in light of today’s post.

29. June 2018 at 08:15

Majromax, The absolute peak of 5000 still seems a bit high, but the general bubble theory now seems wrong. The bubble theorists of 2000 claimed that the high NASDAQ only made sense if you assumed that internet/tech firms would eventually dominate the economy, earning massive profits and surpassing mainstream corporate giants like Procter and Gamble, GM, GE, Exxon, etc. Well, now internet/tech firms like Amazon, Google, Microsoft, Apple and Facebook do dominate the economy, and do earn huge profits. What the bubble theorist denied would happen has actually happened. The NASDAQ should have soared to very high levels in 2000, once the bright future of tech became apparent. Maybe it overshot a bit on a few trading days, but there was no extreme bubble in the late 1990s. A very high NASDAQ was appropriate in 2000, even if 90% of the companies eventually failed.

29. June 2018 at 08:18

Regarding #1, what counts as impact on the housing market – the amount of housing built or the average price of that housing? (Or both?) I’d expect the deduction to have more of an impact on the prices than on number built/sold.

I also don’t know how long the process of building new housing takes. Is it possible that new housing coming on the market today was already approved before the tax bill and housing developers simply haven’t had a chance to adjust yet?

(I don’t have a WSJ subscription, so my apologies if that article already answers my questions)

29. June 2018 at 08:32

Doug, You said:

“I seem to remember our professor arguing that the Swiss had to devalue.”

You have a bad memory. I argued in many posts that the Swiss did not have to revalue (they did not devalue), and I argued that they made a mistake in doing so. It appears I was correct.

The financial collapse you describe was roughly equal parts tight money and the flawed financial system you describe.

29. June 2018 at 08:52

Scott, are you aware of any academic or non-news investigations on US housing price sensitivity to mortgage interest rates? It seems to me that various features of the US housing market (tight supply, historically low but rising interest rates – since buyers can still get loans cheaply but owners might not like the prospect of having to get a new higher-cost loan, low unemployment, etc) are upward pressures on prices. It could easily be the case that the mortgage interest tax deduction removal is simply lessening the effect on housing prices, but it would be nice if there was some solid evidence either way.

29. June 2018 at 08:54

The EMH’s primary hypothesis is that you can not predict future prices based on today’s prices. Or that you cannot beat the market as it is a random walk—or that today’s prices reflect all available information. This means today’s price is the best guess of the market’s value. This is my default position generally.

But occasionally, for the price of the market to be valid (and I think this held true in 2007 where we definitely undervalued housing— and in 2000 where we definitely overvalued Nasdaq), it is important to understand the implication of the price. I.E., for the price to make sense what else do we have to accept as true? For example, the price of Cisco in 2000 “implied” that it would be larger than the GDP within 20 years (I cannot go thru how I came up with this number now—it was just an approximation anyway—-but for argument’s sake assume I know something about finance). Since that is impossible, we, therefore, would need to change our assumption of GDP growth for CSCO’s price to make sense. At the time, under a certain set of assumptions, this implied GDP would grow between 8-10% for 20 years for CSCO’s price to be reasonable. While that was possible—as anything is possible—it is what you would have to believe. I am sure I could have come up with other kinds of assumed beliefs. But I chose instead to believe the price was wrong. Nasdaq declined 83% in the next 3 years—which happened to be about my personal forecast—which was a coincidence to be so close.

Housing was similar. A lot went wrong in 2007—-mostly bad risk management, real declines in housing prices in California and Nevada, but the mark to market panic (not unlike 2000) required one to believe certain things given the implication of the prices. Using AIG as a proxy (as CSCO was used as a proxy) for the market, what did one have to believe in order to accept the mark to market value of AIG’s credit derivative book? As an approximation, you would have to believe that about 40% of all mortgages would default. That was possible because anything is possible– but I did not think that was anywhere close to plausible. I was against TARP etc etc. I eventually met with the FED and I told them (this was in about 2010 or so) I did not think they had one default in the AIG book they now had possession of. The admitted they had ONE default.

My point is, I think the EMH is partially flawed for the reasons (given by example) given above. I do not think the above analysis is useful except at wild extremes. These are the only times I thought prices were wildly off—and also the only time I did any analysis of this sort. I have no idea if the S&P is worth 2700 or not. To me anywhere between 1500-4000 is “reasonable” based on “value”. But 10000 or 1000 is likely not.

29. June 2018 at 10:42

On point #2, there is no such thing stock market bubbles, at least in the US. The correlation between the S&P 500 since 1950, for example, and GDP is more than .97. And, if one takes the discounted earnings approach to valuing the S&P 500, how could one reach a different conclusion?

I think that also means I have no reason to believe the Fed can’t level-target the S&P 500, as a means of NGDP targeting.

29. June 2018 at 10:49

“Many pundits can’t handle the truth,” or (more likely) they don’t want to handle it, because they don’t really care about it. Punditry isn’t about truth.

29. June 2018 at 11:19

I don’t know how you can really believe #2. Anyone who bought the NASDAQ at its peak, even holding for 18 years, would sorely regret that decision today. Given that you understand that equity returns are expected to have a decent yield, I’m not sure why you’ve convinced yourself the price at peak was fine or nearly fine. I suspect it has something to do with the subsequent crash overshooting.

Regarding the mortgage deduction, taking away half of the nominal amount available impacts far less than half of the market. So I don’t think this case is at all clear on what we should expect the magnitude of the net impact to be.

29. June 2018 at 13:57

The portion of the housing market affected by the loss of mortgage interest and real estate tax deductions is the upper middle end of the market, a relatively small portion of the market as measured by transactions though a much higher portion measured in dollars. The 0.1% will not experience a noticeable lifestyle change from the loss of these deductions. The rest of the top 1% will grumble but feel little more than annoyance. The rest of the top 10% will feel it if they live in high tax high priced locations. If you have multiple homes and are in an upper middle class household in the midwest making 250-750,000 per year and paying 40-60,000 in real estate taxes, plus personal income tax to state and/or local government, it is going to hurt. Probably hurt if you are a $250,000/year NYC subway conductor too. If you are in a less than extravagant home and paying <$15,000 in real estate and other state/local taxes, not much effect on your lifestyle either.

Where I live its hard to sell a pricey home in Illinois or Wisconsin, so transactions have been fewer among the affected population here. Few people want a million dollar home in Lake County Il with a $35,000 annual property tax expected to rise and the Democratic candidate for governor running on changing the state constitution to allow a graduated income tax.

29. June 2018 at 17:44

Re No 1.

“Nick (Rowe), I also didn’t expect the real estate lobby to lose on this issue.

I didn’t have a good sense of how much it would slow the housing market, but so far it’s been less than I would have expected. Of course there’s always the ceteris paribus problem (i.e. RGDP growth is strong), so it’s hard to know for sure. But I suspect the impact was pretty mild.)” —Sumner.

Egads! What ever happened to, “Never reason from a price change.” Or lack of one.

1. Maybe house prices, especially in upper income brackets, would have soared even more and far higher without the cut in mortgage interest tax deductions.

2. The cities where there are strong housing markets are defined by market perversions, such as property zoning. Zoning, while stagnant, is likely a tightening noose in relation to demand.

Ergo, the hit on mortgage deductions might be having a very strong effect, but it is invisible, as it is merely retarding an upward march in house prices, in general.

29. June 2018 at 19:05

I wouldn’t stake too much on the mortgage deduction point. All income tax benefits to owners probably add up to about a 25% increase in total value. The largest factor is that owner-occupiers don’t pay taxes on their imputed rental income. The mortgage deduction accounts for maybe a third of the total, and this was only a partial elimination.

These benefits are highly regressive, so I would expect little change in low end markets, and the scale of the relative change at the high end to be about 5%.

It so happens that up until a year or so ago, in a regression of all zip codes in the Zillow database, high end real estate was appreciation slightly more than low end real estate – a couple percentage points annually. This shifted so that over the past 12 months, high end prices have appreciated by a couple percentage points less than low end prices.

This isn’t definitive. I’m not sure if anyone could definitively parse this effect out of the data, because the scale of the effect is relatively small, and there are many influences on home prices. But, the null hypothesis certainly hasn’t been rejected. In fact, the relative shift is prices is roughly what you should have expected.

While the mortgage deduction should be eliminated, the scale of it as an effect on housing prices tends to get inflated in the national imagination. The GSEs are similar. Getting rid of the GSEs would probably also have such a small effect on home prices that it would be hard to notice.

29. June 2018 at 19:47

mpowell, You may have forgotten, but people didn’t just claim that NASDAQ 5000 was a bubble, they claimed that even 3000 or 4000 was a bubble, which is not at all clear.

Yes, if you look at a long time series, and pick the absolute peak of a spike, which might have just lasted for a couple days, that peak price will often look excessive in retrospect. But that doesn’t prove it’s a bubble.

It would be like saying that the bitcoin price of $19000 was a bubble, or the gold price of $1900 was a bubble. Only in retrospect do we know that those were peak prices.

My point is that the entire late 1990s were viewed as a bubble by 2002, and it now seems that period was not, except perhaps a few days at the absolute peak.

29. June 2018 at 20:12

I personally think there is a decent (>50%) chance we are in another housing bubble.

Your graph only shows prices since ~1990, but if you look back historically [1], the Case-Shiller index has only risen much faster than inflation twice since the Great Depression:

(1) post WWII with a massive shift in culture and government policeis

(2) 2000s housing bubble.

Between the mid 1950s and the mid 1990s, the price of existing homes increased at the rate of inflation, so what makes the 2010s so special that they buck this half-century trend?

1. https://docs.google.com/spreadsheets/d/1EgliBbpzeE2Bk5-aNF4yUFcBzF2bPJ71sg18q3HGLt8/edit?usp=sharing

29. June 2018 at 22:23

“It would be like saying that the bitcoin price of $19000 was a bubble, or the gold price of $1900 was a bubble. Only in retrospect do we know that those were peak prices.”

Since there are always accusations of hindsight bias, here’s what I said on 12/7/2017. On that day, Bitcoin was at $14,000.

““Bubble Theory” just says: don’t buy Bitcoin.”

http://www.themoneyillusion.com/bubblemongers-dont-get-a-second-chance/

Bitcoin went under $6,000 yesterday. I couldn’t predict exactly when the peak was hit. It was hit 10 days later, at $19k. I also couldn’t predict that it would be down 57% after I wrote this. I just knew I didn’t want to touch the stuff. Buffett on gold in 2012 gives the basic argument, which applies to bitcoin as well. Buffett’s advice on gold also would have saved substantial money, compared to buying index funds.

By contrast, NASDAQ gives very poor evidence in support of the EMH. The 2002-2007 peak was $2,800. Buying NASDAQ at $3,000 would have earned a return of -7%. A 10-year Treasury yielded 6%. So with no coupon reinvestment, that $3,000 would be close to $4,350 with two years left. T-bills averaged maybe 3% 1999-2007. Even with T-bills, a compounded 3% rate gave $3,800 in 2007.

30. June 2018 at 05:51

Good Post. I agree that 99% of people using “bubble” or dismissing the difficulty of out-predicting markets land somewhere between not useful and incoherent. But I also think you tend to overstate your case when you make this particular argument.

Here are the total, 17.5 year real annualized returns from December 1999 (not the 5K peak) of some of the most common domestic investments:

20-Year Treasury Bond: 4.5%*

Russell 2000 Index: 5.7%

S&P 500 Index: 3.1%

Gold: 6.5%

High Yield Bonds: 5.3%

Nasdaq: 2.1%

Nasdaq 100: 1.1%

*This is just the total real return of buying and holding a 20-Year Treasury Bond in 1999.

As you point out, the market was in many ways more right than the naysayers back then, sometimes in shocking ways. Amazon’s market cap is 7X GE and 4X Proctor and Gamble. But even given that, risk adjusted returns in the Nasdaq and Nasdaq 100 (large Nasdaq companies excluding financials and the most heavily traded Nasdaq proxy) have been pathetic, despite higher average volatility. These are horrific risk adjusted real returns compared to other domestic choices over a long period in which tech basically did take over the world. Imagine the counterfactual where it took a little longer.

This is especially so for risk free bonds, which earned much better returns with much less risk.

I’d say these results are somewhere in between. They don’t offer good support for people who defined Bubble as akin to a ponzi scheme (i.e. Nasdaq was 80% overvalued), but it still does offer some support to those who define Bubble as an asset with predictably terrible risk adjusted returns versus alternatives. Of course, this alone doesn’t prove anything because some were screaming it from 1996. But it also doesn’t overthrow the argument that the market had it pretty wrong in 1999. It still looks pretty bad.

30. June 2018 at 08:42

For Nasdaq and the housing market, you make the same mistake. Both markets will grow organically with time, as the US economy continues to expand. Some simple fact checking backs this up. In late 1999 the Nasdaq 100 P/E ratio hit 150. Today it’s 25. We should not compare the actual value of the Nasdaq to 1999. The P/E ratio is a much better gauge of market value than market cap.

Similar logic can be applied to the housing bubble of the mid-2000s. One really only has to glance at the chart to see that housing prices raised at a rate that far outstripped the historic average, but the key piece missing from your discussion is the easy credit that was available. Low interest rates that did not require background checks at all, most of them ARMs, artificially inflated the market. It’s a classic bubble.

30. June 2018 at 09:09

Andy, it’s understandable that you would reference ARMs because the public discussion about the housing bubble has been aggressively sloppy. But, I’d like to point out that the private mortgage market you reference was strong from the beginning of 2004 to mid 2007. This was a rising rate environment. In fact, for half that time, the yield curve was inverted. Many canonized facts about housing are like this

30. June 2018 at 10:22

Matthew, Seriously? People were predicting Bitcoin was a bubble when it was $30. Bitcoin bubble predictions have been some of the most useless utterances in all of human history. No one has any idea what it’s worth.

dlr, Those are ex post figures.

Andy, The P/E ratio is almost worthless in a fast growing sector.

30. June 2018 at 10:31

dlr, I should clarify that bonds have done far better than expected because of an unexpected plunge in real and nominal rates, which boosted the relative return of long term bonds. Ditto for gold. It would make more sense to compare to T-bills. What has their real return been?

30. June 2018 at 11:25

Growth of $10K since 1/1/2000:

QQQ (Nasdaq-100 ETF): $21K.

DIA (Dow ETF): $32K.

The Nasdaq was not the worst of it. The Neue Markt (an emerging tech focused stock market in Germany) closed down after losing 99%.

You would be on firmer footing if you pointed out that the “bubble watchers” spotted a bubble long before 2000 – so they should get partial credit at best.

30. June 2018 at 14:56

not to be melodramatic but that’s a disappointing response. when you argue that ex post nasdaq returns refute previous bubble claims and someone responds ‘not exactly’ it’s pretty vacuous to say “well that’s ex post.” One minute nasdaq 7500 is a natural experiment the next it’s a single roll of the multiverse dice containing no ex ante information. Sure maybe inflation could have wiped out bond returns or maybe we could be at Nasdaq 2500 and Netflix could be the name of a movie I just rented at Blockbuster.

And the decline in real rates is irrelevant, because if you were in dec 99 and were choosing between a 20 year nominal bond and the QQQ you earned 4.5pct real with low risk or 1 pct real with high risk. That bond return is a buy-and-hold until maturity return, it does not benefit from declining real rates (although the QQQ return might, ironically, and subject to what caused the decline in real rates). Inflation of 2.3pct in the ensuing 17 years was almost exactly what breakevens were forecasting, so there was no positive inflation surprise in returns. The only implicit surprise (implicit in the high real low risk yields) was that competitive risky returns like Nasdaq stocks wasn’t higher.

1. July 2018 at 04:46

OT comment:

Has anyone ever had the chance to appoint so many people to the FOMC and the Supreme Court, so quickly, as Trump?

We live in a Trump reality show.

1. July 2018 at 09:46

dlr. I think you missed the point. Let’s take a more extreme example. Long term T-bonds yielded 15% (nominal) back in 1981, based on expectations of really high NGDP growth. Suppose you bought an alternative more risky investment that ex post yielded 12% (nominal). Disappointing. Does that mean the more risky investment was overpriced in 1981, or might the T-bond holders have gotten a huge windfall from the unexpected slowdown in NGDP growth?

The risky investment might have been rationally priced, given reasonable expectations of NGDP growth. The T-bond nominal return is locked in, regardless of what happens to NGDP growth. Most investments will see their nominal returns fall unexpectedly as NGDP growth slows sharply.

1. July 2018 at 14:04

re: the housing market was wildly overvalued in 2006.

We bought a house in 1997 for about $240,000. We sold that same house with a few minor improvements in 2005 for $640,000.

It was either wildly overvalued or the dollar had depreciated significantly.

Made my retirement much easier.

1. July 2018 at 19:15

Scott, Larry’s comment is an excellent example of my point that much of the extracted home equity during the boom was saved, not consumed.

2. July 2018 at 05:05

I didn’t say I knew what Bitcoin was worth. That’s almost a pure Keynesian beauty contest. The fundamental nature of Bitcoin did not change from $30 to $19k. Nor did it change from $19k to $6k.

I will stop arguing these EMH posts after this.

I will say these EMH posts are completely alien to anybody who has worked in markets. Many market participants, such as Buffett, DO say most people should invest in index funds. But that’s very different from saying “Market prices reflect all publicly available information.” Money actually moves around in a very different way than textbooks say it should.

IMO, the EMH has two different I’ll effects:

1. The inherent circularity of “the market says it’s worth this much, then I will value it this much.” Very basic fundamental analysis has outperformed the market generally, such as buying stocks in 2009 and not 1999. This analysis goes back to Graham and the 50’s. It’s just not a data snooping, ex post finding.

2. The implicit deference to financial institutions, especially with regards to regulation. Options and broker-dealer dergulation had a strong element of “These big banks must know what they’re doing, because of how sophisticated they are.” Arguments in that vein.

The deregulation still had socialized elements under the surface. Even if Lehman, AIG, etc. were long-term solvent, they got large subsidies from borrowing short and lending long. The interest rate spread would have been much less if their assets and liabilities were truly matched. Lehman’s broker-dealer also still got discount window loans. Just not the holding company.

The deregulation has ultimate roots in undeserved deference to markets, through things like the EMH.

2. July 2018 at 05:12

> where would Nasdaq be today if NGDP had grown during 2000-18 as rapidly as people expected back in 2000? Maybe 10,000?

I say 14000

6. July 2018 at 23:23

– On the topic UK: I look at the exchange rate between the GBP on the one hand and the EUR and USD on the other hand. The UK is a net food importer from the Eurozone. Then a falling GBP/EUR and/or GBP/USD (think: oil products) will hurt purchasing power of british consumers and will lead to a recession. Unless british consumers are willing to take on A LOT OF more debt (think: more demand).

– The Trump taxcuts won’t lead to a growing economy, IMO. Because some 90% of the taxcuts benefit the corporate sector and only 10% of the taxcuts benefit the workers, families and households. It means that demand isn’t going to increase too much. It’s not enough to justify expanding production and hiring more workers/employees.

6. July 2018 at 23:27

– O yes, the US housing markets were still wildly overvalued in 2005 and 2006.

– The US housing market peaked in mid 2005, NOT 2006. Home prices started to go down in mid 2005.