Monetary policy isn’t what you think it is

Most people judge monetary policy in terms of the level of interest rates. Low rates are easy money and high rates are tight money. More sophisticated pundits suggest that you need to look at the expected path of interest rates over time. If one knew the exact path of interest rates from now to the end of time, wouldn’t that describe the path of monetary policy?

Not really.

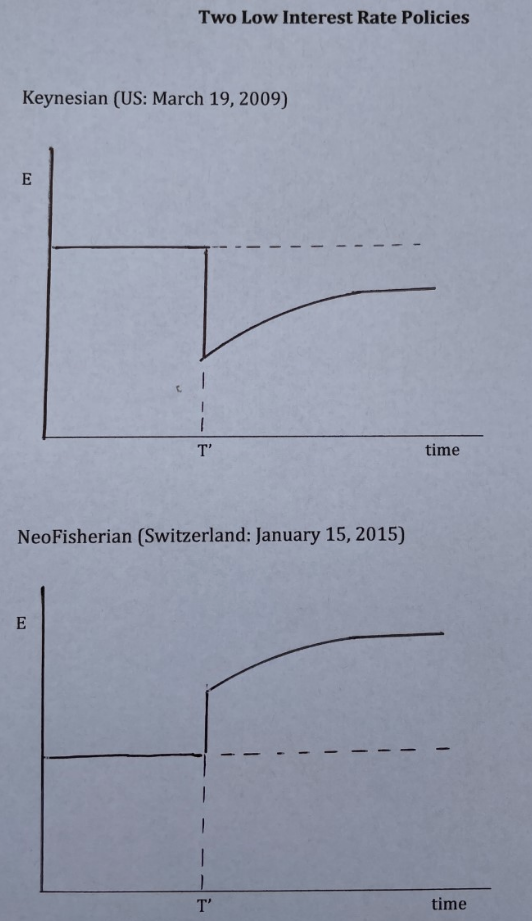

Consider two central banks. Assume that both use exchange rates as the instrument of monetary policy. At time T’, each announces an unexpected change in the path of the (formerly stable) nominal exchange rate (not interest rate) as follows:

In the first case, the exchange rate depreciates sharply in the short run, and somewhat less so in the long run. It’s an unambiguously expansionary monetary policy. In the second case, the exchange rate appreciates sharply in the short run, and even more so in the long run. It’s an unambiguously contractionary monetary policy.

Now here’s what might surprise you. In both cases, the change in the nominal interest rate is exactly the same from T’ to the end of time. In both cases, short-term nominal interest rates fall and long run forward interest rates are unchanged. If you think of monetary policy as a path of interest rates, then the two policies are absolutely identical. (This is due to the interest parity condition, which implies that nominal interest rates reflect the expected change in the exchange rate.)

I often see people talk about how a particular monetary policy shock impacted interest rate futures. They might see a rise in the three or six-month forward fed funds rate and assume that means that markets interpreted the shock as the Fed intending to tighten monetary policy.

You cannot do that! It’s just wrong. Interest rates do not describe the stance of monetary policy, and they do not describe changes in the stance of monetary policy.

And don’t say, “The monetary policy is the same in both cases above, but there was a non-monetary shock that caused the two macro outcomes to differ.” In this case, the different outcomes is obviously due to differences in the initial change in the exchange rate, but we are assuming the central bank uses the exchange rate as the policy instrument, so one certainly cannot argue that this is a “non-monetary shock”. Indeed that argument is equivalent to making the equation of interest rates and monetary policy into a tautology. If you define monetary policy as nothing but the path of interest rates, then you will be correct in claiming that monetary policy is nothing but the path of interest rates. And you will have a completely useless model.

Suppose the Fed has been struggling with its control of inflation. Markets view Powell as being too dovish, lacking in credibility. There’s speculation that the Fed will have to raise rates by another 300 basis points to get ahead of the curve, to control inflation. Then Powell makes a forceful statement at a press conference. With anger in his voice, he insists the Fed will do whatever it takes to bring inflation down rapidly, even if it results in recession.

Suddenly, the markets begin to believe he’s serious. Expectations of recession rise sharply. As recession fears mount, the expected future natural rate of interest falls rapidly. If the expected path of the Fed’s interest rates falls less sharply than the expected natural rate, then two things happen:

1. The path of interest rates falls.

2. Monetary policy has become tighter.

Everything Powell does is monetary policy. His votes are monetary policy. His words are monetary policy. The stern tone of his voice is monetary policy—separate from the words. And these words are not monetary policy because they impact the future path of interest rates, or at least not entirely for that reason. They are monetary policy because they also move the expected path of the economy, and hence the expected path of the natural rate of interest. (Think of Powell’s FOMC vote on the interest rate target as the Keynesian part of his policy, and the stern tone of his voice as the NeoFisherian part of his policy.)

I can’t emphasize enough that all this speculation about how high the Fed will need to raise rates is utter nonsense. The path of interest rates is not monetary policy. If the Fed has a credibly effective anti-inflation policy then it will end up raising rates by much less than if it drifts into a sort of G. William Miller-style passivity.

PS. These two graphs are not mere theoretical curiosities; they are stylized representation of actual real world monetary shocks in 2009 and 2015.

PPS. The central bank of Singapore uses exchange rates as its policy instrument. As (in a sense) do countries on a fixed exchange rate regime, such as Hong Kong and Denmark.

Tags:

24. July 2022 at 11:21

Expectations are misleading. Inflation is a math equation, but not Steve H. Hanke’s WSJ Feb. 23, 2022

Monetary policy is backwards. Monetarism has never been tried. If you wanted to get rid of inflation, you should stop expanding the money supply, indeed drain the money stock, and then gradually drive the banks out of the savings business (increasing velocity).

The 1966 Interest Rate Adjustment Act is prima facie evidence. M1 peaked @137.2 on 1/1/1966 and didn’t exceed that # until 9/1/1967. Deposit rates of banks decreased from a high range of 5 1/2 to a low range of 4 % (albeit not enough). A .75% interest rate differential was given to the nonbanks.

A recession, as Powell claimed (“Powell cited 1965, 1984 and 1994 as examples where the FED corrected the economy without a recession.”), was avoided.

24. July 2022 at 13:41

“Exchange rate” seems to me to be a strange term. Just because some term is commonplace does not mean that it cannot be strange from my point of view. “Currency value” or “the value of a currency” seem to be more useful terms. “Exchange rate depreciation” is ambiguous because the reciprocal is simultaneously changing. “Foreign exchange” is a silly qualified noun. “Currency” is a useful noun.

24. July 2022 at 15:50

“ I can’t emphasize enough that all this speculation about how high the Fed will need to raise rates is utter nonsense. The path of interest rates is not monetary policy. If the Fed has a credibly effective anti-inflation policy…”

Isn’t the speculation about rates basically speculation about what actions the Fed needs to take to achieve credibility regarding inflation?

24. July 2022 at 17:33

I’m not getting this one.

In the currency depreciation case the CB will have to create more money which will (other things equal) require interest rates to fall.

But why in the currency appreciation case (where the CB will need to shrink the money supply) will interests rates also fall ? Logically the decreased money supply would cause them (other things equal) to rise.

Perhaps its the “interest parity condition, which implies that nominal interest rates reflect the expected change in the exchange rate” bit that I’m not getting.

24. July 2022 at 18:00

It does seem a bit curious to me that, of all the things you consider monetary policy—including, for example, Powell’s tone of voice—I haven’t heard you acknowledge that there are real, if difficult to specify, limits to the Fed’s own ability to set monetary policy. Fed independence is a nice idea, in principle, but Powell is not immortal, and none of the Fed members have lifetime appointments. They may be able to make more or less credible promises about what they personally will do in future FOMC meetings, but they certainly cannot commit Congress or future Presidents to select individuals to replace them who will share those views. You can even imagine scenarios where Fed forward guidance, if perceived as overly austere, “competes” with forward guidance from the political branches, or even from political candidates.

All the signaling and forward guidance in the world is useless if some of the possible interest rate paths they entail are politically untenable. You can grow monetary aggregates very very high, accompanied by lots of stern statements saying you will nevertheless do whatever that takes to keep inflation under control should it materialize. While inflation is in fact low, this guidance may be believed.

But assume, for whatever reason, that it is politically infeasible to raise interest rates to more than 15%. If inflation has been 2% for some time, market participants may judge the likelihood of needing to raise interest rates to greater than 15% to control inflation to be very small, if not negligible. In these circumstances, you can expand your balance sheet rather easily, with little pushback from markets, because your guidance is perceived as credible.

However, the very fact of adding to monetary aggregates in this way grows, ever so slightly, that segment of the probability distribution that finds you needing, at some point in the future, to raise interest rates to greater than what is politically feasible. If inflation is 9%, the need for 15% interest rates at some point in the future may no longer seem so improbable. You know that, should you get unlucky and find yourself in that situation, you will be unable to keep your promises regarding inflation. Importantly, market participants, if they stop to think about it, realize this as well. Every addition to your balance sheet, in particular your long-term debt, means that your promise to do “whatever it takes” is a little bit less credible and a little bit more of a bluff.

It seems to bear an uncanny resemblance to the story of AIG before the financial crisis. They were able to sell a lot of CDS, for a handsome profit, against the debt of major US financial institutions when the likelihood of either AIG or those institutions facing default was perceived to be extraordinarily small. Each CDS that was sold, however, raised ever so slightly the probability that the commitments themselves would not be able to honored, at least not without some sort of bailout or external intervention. Every new CDS was a little bit less of a promise and a little bit more of a bluff. As soon as the probability of default in the financial sector ticked up, the natural instability of the arrangement meant that the situation spiralled out of control rather quickly.

25. July 2022 at 05:27

Sidebar to Jeff re: AIG. I do not see the analogy to Scott’s point (which he has been making for at least 10 years) and the AIG situation. Her was the AIG situation.

AIG extended credit via CDS mostly on the very senior portions of structured mortgage securities. Goldman was one of the largest suppliers to AIG of laying off this credit risk.

GS biggest credit mistake (if it really was a “mistake” given they could take up upfront fees—for bonuses—on the securities that were being hedged by AIG) was not requiring—like the futures’ markets generally——daily (or frequent) collateral postings by AIG. If Goldman had done this AIG would NOT have been able enter into as many CDS agreements with GS and others——as AIG did not have had enough cash as the market fell. But here is where it gets interesting.

It is unclear the “marks” would have fallen nearly as much had AIG’s counter parties required collateral—-(implicit per your point).

Counter parties instead required massive collateral calls once it became obvious AIG would not have been able to pay. The latter tried to negotiate on the argument there would be very few if any defaults ——but Goldman would have been required to also take mark to market losses—-so the latter got bailed out when the Fed’s took over AIG.

I raise these hypotheticals because, in fact, the default rate at AIG was, for all practical purposes, zero, on the underlying senior securities they wrote CDS on.

The Fed—and AIG—never took a loss—and not because they became the backstop. No, for those securities to default half of the homes in America would have had to default.

In other words——the market’s knowledge that AIG was increasingly likely to have a huge collateral call caused the securities to decline more——cause and effect was backward. The Fed knew this——-they stayed quiet while Bush—already a Gone Girl—-let his Treasury Secretary do what he wanted.

25. July 2022 at 05:36

Do you think the FED does have a credible policy?

I would say no, since they have abandoned AIT but not replaced it with anything else.

I am not sure if it is correct to use such metric, but the breakeven rate going down seems that the market think the FED does have a credible policy.

25. July 2022 at 07:32

PS—-@ Jeff

In other words—-it was the equivalent of a short squeeze—-a dangerous game—-unless you have the government backing the trade—like GS did and others.

25. July 2022 at 08:42

Lizard, You said:

“Isn’t the speculation about rates basically speculation about what actions the Fed needs to take to achieve credibility regarding inflation?”

Yup, and that’s the problem. Don’t confuse rate changes with “action”.

Market, You said:

“In the currency depreciation case the CB will have to create more money”

That’s not at all clear. It depends how the Fed’s announcement impacts the demand for money. For instance, in Lars Svensson’s foolproof plan for Japanese reflation, currency depreciation would have been associated with a smaller money supply.

If you are targeting the path of the exchange rate, it’s the expected change in the exchange rate that determines interest rates, not the money supply.

Jeff, I think you misunderstand what I’ve been arguing. I’m trying to get the Fed to start down a road that makes those dilemmas LESS likely to occur. I certainly do understand that gaining credibility is difficult for political reasons. It’s not an issue that I’ve ignored. But it’s also not impossible. Every Fed chair since 1990 has bought into the 2% inflation target, even if the execution has been uneven.

That’s why I wish the Fed had stuck with FAIT. The switch to discretion makes their job that much harder.

Marco, It’s a matter of degree. Less credible than I would like, less credible than in 2019, but vastly more credible than in the 1970s.

25. July 2022 at 11:08

“I often see people talk about how a particular monetary policy shock impacted interest rate futures. They might see a rise in the three or six-month forward fed funds rate and assume that means that markets interpreted the shock as the Fed intending to tighten monetary policy.”

Ok, substitute “Fed intending to tighten monetary policy” with “Fed intending to raise policy rates”. That’s consistent.

What about evaluating a potential monetary policy shock based on a number of variables? For instance, what happens to bond yields, TIPs, equities, the dollar, etc., particularly over a relatively short period of time where we can hold most other variables relatively constant?

25. July 2022 at 15:10

Sheila Bair, a senior fellow at the Center for Financial Stability has it right:

“It should replace the shock and awe of major interest rate hikes with new targets based on money supply, and aggressively shrink its portfolio, selling securities at a loss to do so, if necessary.”

25. July 2022 at 15:54

Love to get your thoughts on Luskin’s WSJ piece.

25. July 2022 at 15:57

John, Yes, that’s much better.

Larry, I think inflation will fall, but I don’t put much weight on short run M2 figures.

25. July 2022 at 18:22

You discuss how monetary policy is much more than just interest rates (or any other single metric). In your view, is the current monetary policy (consisting of all the factors you discuss) sufficiently hawkish to combat inflation?

25. July 2022 at 20:19

Scott,

I followed your blog since the beginning. It was a crazy world back then and you were one of the few making sense.

It seems we are entering a crazy monetary world again.

Great to see you are still keeping the blog alive.

25. July 2022 at 20:44

Dr Sumner,

This is a crazy request, but most of the public debate these days is happening on Twitter, and your voice and perspective is very much missing there. I read your blog posts (and your books) and it seems to me yours is the only analytical framework that clearly ties everything together. I wish it had a more prominent presence in the public discourse.

26. July 2022 at 07:04

re: “That all dropped straight into the bank accounts that are part of M2, which also grew about $6 trillion over precisely the same period.”

That’s wrong. You can activate monetary savings, giving it an income velocity, but otherwise, unless the FRB-NY’s trading desk monetizes the fiscal deficits, open market operations of the buying type, no new money is created.

re: “On Wednesday, the Fed should do nothing.”

link: Daniel L. Thornton, Vice President and Economic Adviser: Research Division, Federal Reserve Bank of St. Louis, Working Paper Series “Monetary Policy: Why Money Matters and Interest Rates Don’t” bit.ly/1OJ9jhU

26. July 2022 at 09:08

AJ, It’s a matter of degree. The TIPS spreads suggest inflation will fall over time to a level close to 2%. I month later I might give you a different answer.

Thanks Jay.

Backward, I find it hard to make my points with tweets. Especially since my views are so far outside the mainstream. I don’t think twitter discussion is even framing the issues correctly. There’s this obsession with “concrete steps”. But I’ll consider it.

26. July 2022 at 09:31

Backward is right. Twitter is in vogue. That’s where the market heavyweights hang out. And I won’t be there.

26. July 2022 at 12:37

@Jeff:

Very good comment above. If there was a ‘like’ button I’d give you one.

26. July 2022 at 16:16

yep it’s confusing to almost everyone when someone knowledgeable refers to Powell’s statements on forward guidance (as opposed to the guidance itself) as “monetary policy” but it’s no less a part of the process than the famous Fed funds rate

expectations uber alles

27. July 2022 at 13:54

I think Trump was right: ““The Fed is like a powerful golfer who can’t score because he has no touch,” he wrote. “He can’t putt!”

The last figures for the 2nd qtr. GDPnow are out. Latest estimate: -1.2 percent — July 27, 2022. There’s no way this could be correct without a major error in the money stock #s. Stop/go monetary mis-management under Powell has never been worse. The FED has lost control.

27. July 2022 at 14:01

Is it possible to assume that Powel speaks something and as a result inflation converges down to the target without a recession and the monetary policy rate remained unchanged?

28. July 2022 at 05:35

“Jerome Powell downplayed the significance of early GDP figures, which can be revised “significantly,” and said “it doesn’t make sense that the economy would be in recession” given the labor market’s strength in the first half of the year, with some 2.7 million people hired and unemployment remaining near pre-pandemic lows.”

U * is a moving target. See: “The Great Demographic Reversal” by Charles Goodhart and Manoj Pradhan.

28. July 2022 at 06:27

https://www.ft.com/content/23c3a3a7-b2da-412c-8050-bdad986fde21

Mohamed El-Erian “The risk of a flip-flopping Fed”

“Good central bank policymaking calls for the Fed to lead markets rather than lag behind them”

28. July 2022 at 07:38

Once again, Powell eases. Hard to figure him out

28. July 2022 at 10:37

Everyone, I comment on Powell over at Econlog.

7. August 2022 at 22:44

Can you think of a situation where the central bank caused the exchange rate to appreciate now and then depreciate over the long run, but still end up higher than before? Pretty much a mirror image of the first scenario

8. August 2022 at 08:04

tpeach, That’s easy. The dollar just surged against the yen, but is expected to depreciate again over the next decade.

5. October 2022 at 14:02

[…] of family resemblance. I thought of this when reading a twitter exchange, which was triggered by a recent post I did over at TheMoneyIllusion:There are a number of different ways that one could address this […]