Monetary policy is boring. That’s good.

You’ve probably noticed that I no longer do as many posts on monetary policy. That’s partly because I put my better posts over at Econlog and partly because there’s currently not much to talk about. NGDP growth has been in the 3% to 5% range for 9 years, and I see no sign of anything changing in the near future (except perhaps a bit slower NGDP growth after this year, which is currently featuring above 4% growth.) While boring is bad for me, it’s good for the economy.

Today, interest has turned to the question of when the next recession will occur. The short answer is the same as always—no one can predict recessions. But I’d like to talk about the issue anyway, since everyone seems interested in the question.

I’ve recently been catching up on David Beckworth’s podcasts, and listened to a very interesting discussion he had with Michael Darda. Michael is a market monetarist who works in the investment area, and is known for having an excellent grasp of macroeconomics. He knows the data quite well and he has a rare ability to interpret macro data correctly. Lots of people are good at one, but he’s extremely good at both—no doubt partly due to his upbringing in Madison, Wisconsin.

At one point they began discussing the yield spread, which has been one of the better recession forecasting tools. I’d like to put in my two cents worth.

At one point they began discussing the yield spread, which has been one of the better recession forecasting tools. I’d like to put in my two cents worth.

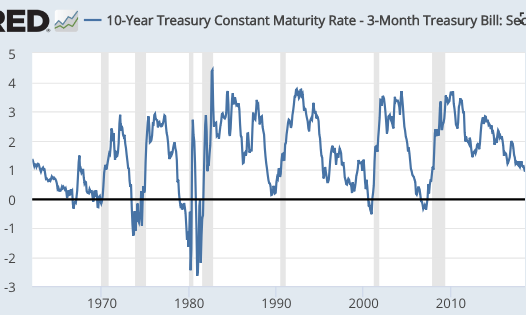

As you can see from the following graph, the yield curve often inverts before a recession. Here it’s important not to over interpret the correlation, as US expansions never last more than 10 years, and yield curves typically don’t invert until well into an expansion, and the lag between inversion and recession varies somewhat over time. Furthermore, yield curves did not invert before recessions in the 1933-58 period. Still it’s one of our most reliable forecasting tools.

Here are a few observations:

Here are a few observations:

1. Over at Econlog, I argued that while the yield spread is pretty good at predicting recessions, it’s much less good at indicating when money is too tight.

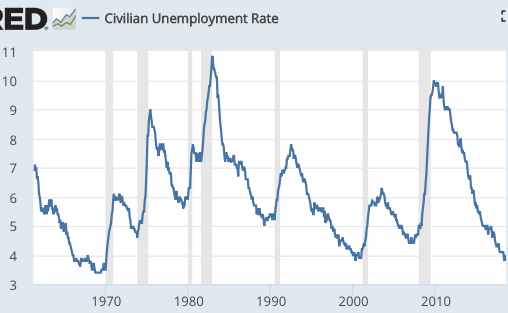

2. It’s possible that the yield spread is reacting to changes in the unemployment rate. Consider the following hypothesis. The yield spread gets relatively flat whenever the unemployment rate falls to a level close to the natural rate of unemployment. Let’s also assume that the unemployment rate falling close to the natural rate is a good predictor of recessions:

In that case we should be worried, as the unemployment rate has recently fallen to a level that is probably close to the natural rate.

In that case we should be worried, as the unemployment rate has recently fallen to a level that is probably close to the natural rate.

Interestingly, there is one notable case when unemployment falling close to the natural rate did not lead to a recession. In 1966, unemployment fell to 3.8% and there was no recession until 1970. But that false signal is equally true of the yield spread, which also inverted in 1966. Coincidence?

[On the other hand, the natural rate of unemployment is time varying (higher during 1975-95) and hard to measure, which makes the yield spread a better forecasting tool.]

When the unemployment rate is trending lower, it’s rational to expect the expansion to continue. It may not always continue (consider 1981) but it’s a rational forecast. And when unemployment is trending lower, the yield spread tends to be positive. That’s because investors expect the future economy to be stronger than the current economy, and interest rates are highly correlated with the strength of the economy.

Conversely, when unemployment has fallen close to the natural rate, it’s no longer rational to expect lower unemployment in the future. Indeed it’s quite likely that we’ll soon enter a recession. That’s why the yield curve gets flat, and sometimes inverts. In plain English, we never seem to achieve soft landings. But Australia frequently does, and thus it’s not impossible. The UK achieved a soft landing in 2001, and hence their 1990s expansion lasted until 2008. If they can do it, so can we.

Memo to Jerome Powell: Your mission, should you decide to accept it, is to avoid the hard landings that so often occur, but also avoid the 1966 scenario, where the Fed pulled up too soon, never landed at all, and instead soared off into the Great Inflation. To do this, you need to avoid an excessively expansionary policy, which sometime triggers the inflation that later causes overly tight policy, and also avoid overly tight policy, which can directly cause a recession. Let’s see . . . how about 4% expected NGDP growth?

Given that we’ve never had an expansion last for more that 10 years, you might wonder why I expect this one to go beyond a decade. Well, until 2006-12 we’d never had a housing crash. Until 2016, we’d never elected a lunatic as President. Until 2018, we’d never adopted a wildly expansionary fiscal policy during a period of peace and prosperity. None of those examples have any bearing on how long this expansion will last, rather they show that it’s really common for things to happen that have never happened before in the US. And notice that other countries have had housing crashes before 2006, and lunatic presidents, and reckless fiscal policies during peace and prosperity. That’s why I mentioned Australia and the UK (and there are many other such examples.) They provide an important clue that there is no inherent age limit on expansions.

Inductive reasoning can be useful, but must be handled with care.

PS. The Hypermind NGDP prediction market is currently forecasting 4.8% NGDP growth from 2018:Q1 to 2019:Q1. However, since the 2nd quarter is already in and growth was quite strong, this implies (annualized) 3.9% NGDP growth from 2018:Q2 to 2019:Q1. Monetary policy is right on course.

PPS. Because money is now boring, and my Trump posts are always stupid, please feel free to recommend other topics. On the other hand, money is the only topic on which I have anything interesting to say.

Tags:

25. August 2018 at 13:44

Hi Scott … There is one extremely interesting question out there and that involves China’s potential responses to the trade tariffs via its own monetary policy levers (and whether they will do any good). China has been in a deleveraging cycle since 2017 and is now pulling out of that a bit. Can it do any good — not just for China but for the emerging world? There is some sort of conveyor belt mechanism whereby capital going into China gets recycled and spread around the EM universe. All that is collapsing now.

Related question involves the issue that the tariffs (going both ways) cover perhaps $400 billion of trade out of an $80 trillion global economy. Yet that $400b is going to be very economically sensitive and intense (with multiplier effects). So can this be Smoot Hawley 2 or a smaller version of it? I can’t quite tell but EM stocks sure act like it.

25. August 2018 at 14:03

Topics/prompts that I’d be interesting in reading your thoughts on:

-What determines the risk-free rate?

-Where have you found meaning in life?

-How do you think historians will look back on this period?

-What will money look like in 100 years? In 1,000 years? In 10,000 years?

-What’s a book or TV show or movie or podcast you liked? Why?

-How do you fight against selection bias as you consume information about the world?

-What are topics we should be talking about more?

-Maybe a high-level tour through periods in history that illustrate something about monetary policy (aimed at people like me who are too lazy to read books where this already written down)

-What are topics you wish you knew more about?

-What are questions that are both important and difficult to answer?

-What constitutes your information diet? What sources of information do you strongly recommend?

-More posts on how public opinion isn’t real (for me, this was a big takeaway from your writing)

-Thoughts on macro hedge funds

-How you have thought about death and how you wish you thought about death

-Questions that you have for your readers

25. August 2018 at 14:54

Is it really that boring? Care to comment on David Andolfatto’s question on Twitter:

“Market-based measure of inflation expectations remain anchored close to target. Key Q: is this b/c Fed is threatening to tighten further; or does this give Fed room not to tighten further?”

To which Nick Rowe replied:

“Simplest interpretation: inflation expectations (roughly) equalling 2% suggest that people trust the Fed will tighten further if and only if it’s necessary to tighten further.”

25. August 2018 at 14:59

I realise this is consistent with your answer that monetary policy is currently right on course, but what does that mean in concrete steppes when at least commentators are expecting the Fed to raise rates in September and again in December.

25. August 2018 at 17:21

Your Trump posts are not stupid and your predictions for how his administration would were pretty dead-on so far. Institutions have held up somewhat better than I expected. I hope that continues to be the case.

I noticed recently that China’s productivity growth has been down since the Great Recession, again making me wonder what might be going on in many countries in the world in this respect, assuming obvious demographic changes, shifts to service sector, and measurement problems don’t explain the whole problem.

I can’t help but think it’s related to the recession and may be partly demand-related.

25. August 2018 at 18:11

Well, I think a 5% NGDPLT target is better.

So one question could be, what would be the worst result of a 5% target?

I think the worst result would be a 1% higher inflation rate then you see with a 4% target and no increase in real output.

The best result of course would be a 1% increase in real output.

My guess is that the likely result is some split of the difference, and a policy and chance worth taking.

Another observation: US macroeconomists of a certain generation frame every macroeconomic discussion in terms of possibly too high inflation. Of course the words Weimar Republic are never too far from some lips.

But consider Japan and most of Europe. Consider that mainland China does not reach its inflation ceiling, or that the US gave up trillions in real output while staying below its inflation target for nearly ten years. Nations such as Thailand have almost no inflation and almost no reported unemployment.

Is fighting inflation fighting the last war? Should the Fed take more chances to promote real growth?

Lastly, if we are concerned about inflation then we are concerned about housing prices caused by artificial shortages.

I conclude that US policymakers are determined to fight inflation, but not in any way that would disrupt the advantages of the rentier class

25. August 2018 at 18:21

Another great topic would be, if QE does not cause inflation why not use QE to reduce or offset the national debt?

This seems to work in Japan.

The Federal Reserve Dallas has released reports suggesting QE actually strengthens the currency and reduces inflationary concerns. They say the currency becomes backed by the bonds of the US government.

The Federal Reserve St. Louis has released reports suggesting that QE has almost no effect on inflation.

We all know the US Congress will run huge deficits for as long as the eye can see. This is a premise for any future policymaking.

So why not a constant program of QE?

25. August 2018 at 19:36

Hi Prof. Sumner, I’d like to see your opinion of GMU economics in a future post particularly how they teach monetary economics.

25. August 2018 at 20:44

Maybe a post on why you pick a 4% NGDP growth target for the US vs any other number. And what target might you pick for China, or Japan, or Britain, or really any country that has an independent monetary policy.

25. August 2018 at 20:48

Despite trump’s craziness I see some positive things in his policies and Scott many of your opinions about him are not crazy.

25. August 2018 at 22:28

Query: Why are black South Africans, or Zimbabweans, never described as “xenophobic” or “racist” is their attitudes towards white residents?

Yes, I am broadly aware of the history of those two nations.

But if context is justification, then what of other situations, where the extant population feels threatened by immigrants?

26. August 2018 at 00:13

Benjamin,

Come on, don’t be naive.

Whitey is always bad.

That’s why they must not be allowed any form of collective action (also known as “white supremacy”).

When any other group of people does it, it’s A-OK.

When whitey does it, they’re bunch of Nazis whose heads must be bashed in with bike locks.

It’s almost as if Lee Kuan Yew was right all along.

You can’t have both democracy and multiculturalism.

For, as we can see in real time, it quickly becomes a slugfest along ethnic lines.

Which makes prof Sumner’s position all the more interesting.

In advocating for more immigration, he’s pushing for more racial violence.

Either his ivory tower is too tall for him to see how the hoi polloi live.

Or that must be his vision of a golden future. A nature red in tooth and claw.

26. August 2018 at 04:52

Maybe choose a topic on California. Now that you live there, have you made any observations that would be a good post? Anything surprise you?

26. August 2018 at 06:00

Topic: why haven’t we abolished the penny?

26. August 2018 at 07:02

My guess is that as long as nothing happens that pushes inflation targeting policy away from what a NGDP targeting regime would pursue there will be no recession. A negative supply shock would probably cause a recession.

26. August 2018 at 08:09

Off topic:

– Tighter lending standards from the australian commercial banks mean that borrowing power shrinks by some 35% to 40%. And that in turn means that the price of australian houses are bound to go down by some 35% to 40% as well. 35% to 40% fall in home prices is the best signal of a housing bubble.

https://www.bloomberg.com/news/articles/2018-04-15/tougher-lending-standards-put-australia-property-on-shaky-ground

http://www.abc.net.au/news/2018-04-05/home-buyers-borrowing-capacity-to-be-cut-by-35-per-cent/9621696

– Is one Scott “I see no bubble” Sumner still convinced that bubbles don’t exist ? Markets are actually VERY efficient. Pump more money/credit in the system and some things will go up in price. And bubbles are part of those “Efficient Markets”.

– In regard Australia has/could have turned a corner. Australia is, since say 6 months running a Trade Surplus. This makes Australia less dependent on the generosity of foreigners. But it makes Australia more dependent on the willingness of other asian countries to buy australian commodities.

– When I use the formula developed by one Steve Keen then Australia is already in a recession.

26. August 2018 at 08:51

Proposed topics for new posts:

If the U.S. implemented Irving Fisher’s Chicago Plan for 100% reserves and NGDPLT at the same time, would that be a improvement over the current monetary system?

If the U.S. replaced all tariffs and non-tariff barriers with a 5% flat tariff and used the increased revenue to cut payroll taxes, would that be an improvement on current trade policy? What about 10%? 15%?

Which historical U.S. monetary system do you think was the best?

1792-1836: The Bank of the United States and bimetallism

1836-1860: no national bank and bimetallism

1861-1873: US Notes and private National Bank Notes

1873-1913: Gold Standard, US Notes,National Bank Notes

1914-1933: Gold Standard with Federal Reserve

1933-1944: Federal Reserve

1945-1971: Federal Reserve, international Gold Standard

1971-present: Federal Reserve

Or do you categorize our systems differently than I do?

What do you think of the Elam ending for basketball to reduce the incentive for intentional fouling? https://www.si.com/nba/2018/04/26/tbt-basketball-nick-elam-jon-mugar-earl-boykins

26. August 2018 at 08:52

Maybe you have interesting things to say about the following article

https://www.ft.com/content/7f000b18-ca44-11e3-bb92-00144feabdc0

called “Strip private banks of their power to create money”

26. August 2018 at 09:16

Kgaard, I’m still a bit skeptical of the notion that there will be an intense trade war for an extended period of time. Anything severe enough to badly hurt China would also badly hurt the US. I suppose the nominal effects can be offset with PBOC policies, but of course that doesn’t offset the real effects.

Ted, Good questions. I’ll address them in separate posts, some at Econlog.

Rajat, Yes, I agree with Nick. The market currently expects roughly the appropriate amount of rate increases.

Michael, It’s entirely natural and expected that China’s productivity growth is slowing, although with supply-side reforms it might slow less rapidly.

John, I have no idea how they teach money, but I do think GMU has taken from Chicago the crown of “most interesting econ department”.

Jerry, I’ve done many posts on that. All those countries you mention would do fine with a 4% NGDP target, or a 5% target. The actual rate is not that important (within reason), it’s the stability that matters.

JMCSF, I did a post entitled “Tesla Town” soon after I arrived, but maybe another post in in order.

Bill, Because we are stupid.

Willy2, As I’ve said many times, Australian housing will eventually have a price decline, but it’s not a bubble. Even normal markets go up and down. That’s what markets do.

Bubbles don’t exist.

Australia’s RGDP is growing at 3%/year—is that your definition of recession?

Negation, Probably an improvement, but only because of NGDPLT.

On the NBA, why not just the first team to 100? Also, change the rule to where refs can choose not to call “reaching” fouls on fast breaks, if calling the foul helps the defense.

I think the best system is 1991-present, (inflation targeting.)

26. August 2018 at 09:17

Negation, Your 5% tariff would likely be an improvement; as the rate rises it’s less and less likely to be an improvement.

26. August 2018 at 09:38

Rob, I agree. I live in Orange County, which is 35% Hispanic and 20% Asian, and I’m terrified to go outside of my house. It’s a hellish war-zone, with bullets whizzing by everywhere.

Ilverin, The problem is not their ability to create money, it’s their ability to take risks with taxpayer insured bank deposits.

26. August 2018 at 11:31

Topic ideas:

1) more movie posts, these are gold. I always find at least 1-2 movies I had not seen, and I have never regretted a viewing.

2) a thorough take down of MMT. Could be source bias, but I am seeing this crop up more. A good explanation of why it’s built on a house of lies/cards would be useful.

3) maybe a thorough explanation on why laws against foreigners purchasing real estate are so stupid. If NZ runs a consistent trade deficit with China and prevents Chinese from buying assets…etc.

4) Trump posts are entertaining, keep em coming.

5) A post about Taiwan, should the US dissolve the treaty and stop selling arms? Or do we maintain status quo and hope that China liberalizes to such an extent that Taiwan can be absorbed without destroying a 1st world democracy?

6) How much of manufacturing production data is so skewed as to be useless? Maybe this one is too far outside your wheelhouse, but it’s an interesting topic. By this I mean computers and imports heavily skew the data to the point where it’s hard to truly establish domestic production.

7) in a hypothetical future US where it becomes truly de-industrialized, is there ever a point in which it makes sense to conduct industrial policy? My first answer would be no, but it would be interesting to hear your thoughts.

Just my 2c

26. August 2018 at 14:23

Scott,

Yes, ceteris paribus, we should expect productivity growth to gradually fall as a developing economy develops, but I have a nagging feeling that it’s not a coincidence that we saw productivity slowdowns that have continued in so many economies since 2008. It’s easy to point to potential supply-side causes, and undoubtedly, there are supply-side causes in every case. However, I think it’s unlikely those are the only causes.

While I’ve seen other economists make similar points in recent years, like Dean Baker, they seem to be in the minority.

My only proposed solution/diagnostic would be to adopt a 5% NGDP target instead of 4%.

26. August 2018 at 17:46

What causes the Fed to let NGDP growth crash? It seems to me that the adjustments required by somewhat higher inflation are less troublesome than those by a declining price level. Is there any reason to think that, absent some real shock to the economy, that we would have a recession with monetary policy that gets us to 3-5% NGDP growth? Also, is a real shock truly inflationary? I worry that some things that would statistically look like a higher price level or inflation is just a higher real cost of import d goods, like say oil.

26. August 2018 at 21:29

Scott,

I’ll just post my earlier comments on the yield curve below, but I now have a new hypothesis called the “Sumner Effect,” which I alluded to before….

What I said was, “And BTW with effective monetary policy, the yield curve would always be flat”

So the hypothesis is that thanks to the teachings of Scott Sumner, the market believes there is a better chance the Fed won’t f up again.

MY PREVIOUS COMMENTS..

On the yield curve.

Very briefly it comes down to is it cheaper to borrow (or conversely can I get a better investment yield) now or in the future. So as a concrete example, if borrowers expect a recession (and corresponding lower rates), they will borrow short term now (raising short term rates) and hold off on borrowing longer term (lowering long term rates) with the net effect being a flattening of the yield curve.

It’s important to remember that borrowers and investors are looking at real rates. Thus a positive yield curve can also be an indicator that the market expects a continuing buoyant economy to result in higher future inflation so that a nominally positive yield curve actually corresponds to a flat real yield curve and an expectation of steady real economic growth.

Now let’s consider the current flat yield curve. I believe that a reasonable argument could be advanced that with a) reduced tax rates, b) a low LFPR (i.e. still high unemployment), and c) relatively low inflation numbers, the market believes that the new normal is steady high growth with relatively steady inflation.

And BTW with effective monetary policy, the yield curve would always be flat and bond traders would be out of job.

Come to think of it, the FOMC and most monetary economists would also be out of work. Maybe that’s why the profession has been slow to embrace NGDPLT.

And BTW …. your Trump posts aren’t stupid…. just boring. Money is always interesting even if you’re repeating yourself. Cinema and meaning are great topics too.

27. August 2018 at 00:33

Prof Sumner in short

“I live in an expensive neighborhood, and everything is just fine (for ME). Therefore, everything is fine for everyone else”

27. August 2018 at 06:51

At the moment, monetary policy is boring…in the US. It’s much less boring in a number of other jurisdiction. I certainly would be interested in reading your opinion about those.

For example, do you have thoughts about Venezuelan dollarization?

27. August 2018 at 08:19

Hmmm, I’ve never seen a clear explanation of MMM. Whenever I attacked it the proponents said I was misrepresenting the theory. Do they even believe the Fed can target inflation at 2%? If not, why has inflation averaged 2% since 1990?

I’m not a fan of industrial policy.

Burgos, I have some posts on your first question. It was partly the Fed “reasoning from a price change”. Partly ignoring market signals. Partly a failure to do level targeting.

dtoh, That’s one way of describing it, but it’s simpler to say that long rates are the average of expected future short rates (plus a risk premium). I’m not sure the yield curve would be completely flat with effective monetary policy, but it would probably be a bit flatter.

Rob, Things are not fine in Detroit, Cleveland and St Louis. They are not fine in West Virginia. Those areas lack immigrants.

LK, I haven’t followed that closely. But aren’t the problems in Venezuela so obvious that there’s no need to even talk about it? Socialism leads to bankruptcy, which leads to printing money to pay the bills. Or am I missing something.

27. August 2018 at 12:01

So if the times when the Fed lets NGDP growth crash are when they start reasoning from a price change, ignoring market signals, and aren’t signaling a commitment to a steady NGDP growth path (failure to do level targeting), I would guess those would be the things to look for in predicting the next recession. For some reason, that doesn’t make me confident in the future performance of the Fed, but I would grant that is just a knee-jerk reaction.

27. August 2018 at 13:48

Gladly. Philosophy, other economic history, trade policy, other economics, growth theory, etc.

Blatantly untrue for the Detroit area, at least. Maybe the city proper within its borders, but that situation is changing.

27. August 2018 at 14:04

Is there any difference in a yield curve flattening/inverting from rising short term rates versus falling long term rates? Or is focusing on that sort of thing just reasoning from a price change thinking?

There’s been talk in South Africa of redistributing land from wealthy farmers to historically disadvantaged people. Do you think some sort of high national property tax would accomplish the same thing, but in a much more rule of law friendly way? A lot of human history has been the struggle to redistribute the wealth of landed elites, so the solution is probably more complex than a simple property tax. I just can’t think of why.

27. August 2018 at 14:57

Sumner-sensei

>please feel free to recommend other topics.

As an eternal young economist(me),

I would like to read your some phenomenology.very interesting.

example:

http://www.themoneyillusion.com/the-mysterious-japanese-economy/

> I’ve always been a bit skeptical about the optimists, as I watch lots of Japanese films and occasionally read their novels. I definitely get a sense that the economy has done poorly since 1993.

28. August 2018 at 01:08

Things are not fine in Detroit, Cleveland and St Louis. They are not fine in West Virginia. Those areas lack immigrants.

They may lack immigrants, but there’s a certain demographic they’re full of.

A demographic conspicuously absent from your community.

28. August 2018 at 06:16

“LK, I haven’t followed that closely. But aren’t the problems in Venezuela so obvious that there’s no need to even talk about it? Socialism leads to bankruptcy, which leads to printing money to pay the bills. Or am I missing something.”

How they got there is pretty obvious, I agree.

What is less obvious to me is how to go from there. Zimbabwe had moderate success by dollarizing. You could also argue that participation in the Euro zone–which is a similar to dollarizing–keeps socialists in check in Europe.

I certainly would be interested in your thoughts about this.

28. August 2018 at 15:43

Harding, I meant city proper. I agree that things are getting better in Detroit as immigrants move in. (A rare time I agree with you.)

Tom, I think redistributing farmland is a bad idea.

Rob, What West Virginia demographic is missing from Mission Viejo?

LK, They need a new government, then things will get much better. Even a government at the 35 percentile (say Argentina or Brazil) would be a vast improvement. Tinkering with the currency is beside the point.

29. August 2018 at 01:30

Prof Sumner,

Put your money where your mouth is and move to Kinshasa/Bangladesh/Mogadishu.

29. August 2018 at 01:32

Or, if you want to keep it closer to home, you can just take up residence near a gypsy camp.

31. August 2018 at 15:51

Rob, Why would I want to live in a poor country. I prefer rich countries.

21. October 2018 at 14:50

[…] est temps que Ted parle à nouveau. Le commentateur Ted m'a posé un tas de questions intéressantes, […]