May you avoid periods of interesting monetary policy

You may have heard of the old Chinese curse, “May you live in interesting times.” The same concept applies to monetary policy—boring is better.

Today, stocks rose sharply in response to Jay Powell’s speech. This worries me. Not the fact that stocks went up—which is fine—rather the fact that these large market reactions after Fed announcements suggest that there is still enormous uncertainty about the future path of monetary policy. A sensible monetary regime is predictable and boring.

David Beckworth directed me to this tweet:

But the Fed is taking its time in addressing the inflation problem, as Powell himself admitted:

I could answer this question by pointing to the inflation forecasts of private-sector forecasters or of FOMC participants, which broadly show a significant decline over the next year. But forecasts have been predicting just such a decline for more than a year, while inflation has moved stubbornly sideways.

Later, Powell suggested that the labor market will remain tight:

Looking back, we can see that a significant and persistent labor supply shortfall opened up during the pandemic—a shortfall that appears unlikely to fully close anytime soon.

That’s an interesting prediction given that most economists expect a recession in the near future, indeed Bloomberg’s panel insists the probability of recession within the next 11 months is 100%.

Here is some more data:

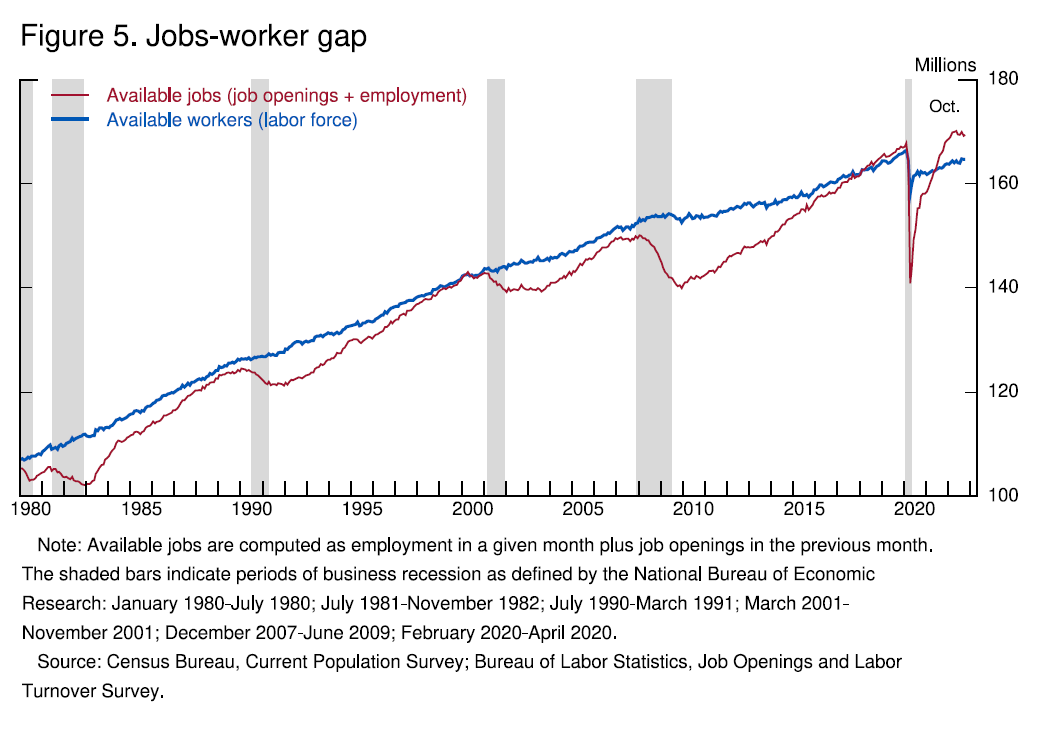

Currently, the unemployment rate is at 3.7 percent, near 50-year lows, and job openings exceed available workers by about 4 million—that is about 1.7 job openings for every person looking for work (figure 5). So far, we have seen only tentative signs of moderation of labor demand. With slower GDP growth this year, job gains have stepped down from more than 450,000 per month over the first seven months of the year to about 290,000 per month over the past three months. But this job growth remains far in excess of the pace needed to accommodate population growth over time—about 100,000 per month by many estimates. Job openings have fallen by about 1.5 million this year but remain higher than at any time before the pandemic.

{kind=link}

It’s interesting to think about what would happen if the Fed completely failed to bring inflation down—if PCE inflation stayed at 6% forever. According to the Natural Rate Hypothesis, real variables such as employment and output would eventually return to their natural rate. Now let’s turn that around, and assume that the labor market normalizes in a year or so. Even in that case, there’s no reason to expect inflation to fall. In other words, to have any success against inflation it’s likely that the Fed will have to bring new job creation to well below 100,000/month.

To be clear, I don’t believe the Fed should target real variables and I don’t view them as reliable indicators of the stance of monetary policy. My point is that it probably won’t be enough to bring the economy back to equilibrium. The Fed’s slow response to inflation will make the inevitable pain that much greater. I hope I’m wrong.

Tags:

30. November 2022 at 16:56

I dont understand why the fed doesn’t just raise to whatever the equilibrium rate is to get this over with and, if there is a recession, so be it, but it ought to be temporary.

It seems like an addition issue is that the longer this drags on, with the economy currently falling, there is going to be additional political pressure to not raise rates so fast, which I hope the fed isn’t already giving into but perhaps it is?

Idk, my industry, tech, is falling apart and people around me are growing increasingly frustrated at the fed but I’m just like, you all knew what was coming and you made your bed, now your sleeping in it, and its rather selfish to subject the entire country to continous inflation just to continue the mania you already knew was unrealistic.

But I’m a minority, those voices will grow louder, and I honestly have no idea what will happen then.

30. November 2022 at 17:25

It is interesting that people are already complaining about tight money at a time when money is actually pretty loose and unemployment is 3.7%. I can’t even imagine how they’ll complain if we actually get tight money.

30. November 2022 at 19:43

Because I’m dumb and stubborn I’m doubling down on my prediction that we’re going to have a repeat of 1990’s era NGDP growth—a bit hot, but not disastrous. However, based on recent events I think the timeline is going to be compressed so that things that took a decade to unfold will play out this time in 3 to 4 years.

I’m maintaining this position because I see different conditions than in the 70’s and 80’s. That period had sclerotic industries and trade unions and a hapless Fed that ran money much looser and longer than Powell’s Fed.

30. November 2022 at 22:58

Scott,

Not making any predictions, but I think it may be a mistake to extrapolate from the 80’s for two reasons.

1. LFPR might now be the a better indicator of tightness in the labor market than the unemployment. Drifting in and out of the labor force seems more fluid than it was 40 years ago.

2. You can capital on stream a LOT faster than you could 40 years ago.

3. There is a much greater ability to substitute capital for labor than there was 40 years ago.

Ultimately inflation boils down to a supply and demand imbalance. Supply may be a lot more elastic than it was during our last dance with inflation.

1. December 2022 at 03:16

Whatever I once knew about monetary policy, I know less now.

The extreme Covid whipsaw diversion and the subsequent spending explosion must have had something to do with the unusual monetary and macro situation. (I am also so glad Powell wants to get this “inflation” thing over “quickly”. Like FAIT—-that got over quickly too).

Let’s pretend that inflation stays at 6% forever—-is that bad? Well, it would be bad if the Fed wanted 3%. I assume. But pretend they didn’t care. It’s volatility and uncertainty that is bad —-at least I always thought that. Income would presumably not lag under such inflation constancy.

When 100% of a Bloomberg subgroup believes something———that seems ridiculous to me.

The political world is changing too. The Cold War, while dangerous, was stable. Climate change policies seem truly weird——particularly since we will never do what the ESG people want to do. It has always been pretend and will stay pretend. Russia is dying if not already dead. Politics is controlled by very odd and strange people.

The

1. December 2022 at 03:26

PS—-continued.

There are people who believe we live in a simulation. Musk uses the statistical trick that applies infinity to get to his belief. And I like Musk—-but he is missing the boat.

We have physicists who believe in parallel universes—-as if that matters—-also a math trick.

Biden, Trump, Xi, . Massive drug cartels. Social media. “i wish that for just one time they could stand inside my shoes……..”

1. December 2022 at 03:51

did you notice that yesterday’s release had ngdi up only 4.6pct QoQ in q3? are you surprised the labor market has remained so strong with ngdi rates having declined from 14pct (post having reached the pre covid trend line) to 4.6? i am.

1. December 2022 at 07:12

Hi Scott – the Personal Income Wage and Salary Disbursements release today shows nominal income growth at 6.7% on a y-o-y basis and 5.9% on a 3-month basis. Still a bit hot but trending toward the pre-COVID average. You don’t take any comfort in that trend considering the Fed five-year forward has remained well anchored? Thanks for all your insight!

1. December 2022 at 07:26

Everyone, I concede that there are data points that indicate some slowing in nominal aggregates. But the pace of slowing is way too gradual. And I worry about forecasts that Q4 will be quite hot. We need 3.5% NGDP growth in the long run to hit the Fed’s inflation target. Yes, nominal growth has slowed from late 2021, but that was bounce back growth from Covid, in some ways 2022 is more worrisome.

dtoh, If anything, trend productivity growth is slowing. Trend RGDP growth is down to about 1.5%. I’ve been a growth pessimist for a decade, and I think events have vindicated my pessimism.

1. December 2022 at 11:42

M2 hasn’t changed for c. 1 year. But DDs have risen. I.e., the composition of M2 has changed. So, the “demand for money” has fallen, and thus velocity has risen (dis-savings).

So, short-term money flows are rising at the same time long-term money flows are falling. Until short-term money flows reverse, a recession will not happen. But it’s harder to predict now that Powell has delayed the reporting of the money stock by a month.

Atlanta gDp nows’ downgrade: latest estimate: 2.8 percent — December 1, 2022 Now a recession seems imminent in the 1st qtr. of 2023.

With the personal savings rate decline, dis-savings, the economy looks to fall off a cliff in the 1st qtr (Xmas blowoff).

https://fred.stlouisfed.org/series/PSAVERT

Alan Blinder says that “food shocks and OPEC ii (supply shocks) deserve much more blame for the alarming rise in inflation in 1979-1980.” But I disagree. Long-term money flows are down. I wouldn’t trade against them.

1. December 2022 at 12:04

AD, money times velocity, is still too high in the 4th qtr. So, the target for N-gDp in the 4th qtr. is still too high.

Economists don’t understand money and Central banking. Milton Friedman, for instance, explains that “Fisher, in his original version, used T to refer to all transactions – purchases of final goods and services…, intermediate transactions…, and capital transactions (the purchase of a house or a share of stock).

In current usage, the item has come to be interpreted as referring to purchases of final goods and services only, and the notation has been changed accordingly, T being replaced by y, as corresponding to real income” (Friedman, 1990, p. 38).

Monetarism involves controlling total legal reserves, not excess reserve balances, not just nonborrowed reserves either. A decrease in required reserve balances (which Powell eliminated), has an immediate dampening impact on AD, on the economy, on N-gDp.

Under monetarism, the monetary authorities use two tools to control the money supply — legal reserves and reserve ratios. If these tools are to be effective, all legal reserves of all money creating institutions have to be in a form which the monetary authorities can quickly ascertain and absolutely control. The only type of bank asset that fulfills this requirement is interbank demand deposits in the District Reserve banks owned by the member banks (like the ECB).

Similarly, the monetary authorities have to have complete discretion over changes in reserve ratios. This is essential since under fractional reserve banking (the essence of commercial banking) these ratios determine the minimum volume of legal reserves a bank must hold against a specific volume and type of deposit liability.

1. December 2022 at 18:00

Something doesn’t add up for me. If the markets think that we will have a recession soon, doesn’t that mean the Fed already has inflation beat? Doesn’t a recession mean fewer people employed, and hence lower demand, and with lower demand lower NGDP growth? If a recession is already a near certainty, and the markets predict inflation falling to the Fed’s preferred level in the same time period that the markets predicts a recession, shouldn’t the Fed just stand pat and congratulate themselves on getting the job done? Or do they need to reduce what little uncertainty remains about the recession and try to get one started as soon as possible? I guess I don’t see what more the Fed can do to lower inflation now except to explicitly say that they guarantee a recession, that a recession is their goal. But wouldn’t that just be gauche, and unnecessarily earn them enemies among politicians? Powell said that they will keep tightening, and will not prematurely loosen policy, which I take to mean that they aren’t going to lower rates as unemployment rises until inflation is back below target. They just don’t know when the recession is going to start. But that speech read to me like Powell promising to keep unemployment elevated until inflation is tamed. I don’t understand why stocks would rally on that message, so maybe I should place less confidence in market forecasts of a recession.

1. December 2022 at 18:08

One possibility I haven’t considered is a fall in real GDP combined with continued job growth. Also, another is that Powell is a poor communicator, sending mixed messages. If the labor market isn’t going to get in balance soon, why worry about going too fast with tightening policy? Or if you are worried about tightening policy too much, shouldn’t you believe that the labor market will come into balance very soon?

1. December 2022 at 19:40

Lizard,

I think the market is rallying because there are many signs inflation is quickly going back to 2 percent (look at Tips). JP is finally signaling that they are data dependent therefore as this happens hikes will slow drastically. Right now it looks more like soft landing or very mild recession (sorry Scott). Market will quickly look through a mild recession to next cycle. Combine that with extreme bearish and underweight positioning.

1. December 2022 at 21:36

Scott,

“If anything, trend productivity growth is slowing.”

I’m not sure that has anything to do with it. I think the issue is that we don’t know much about how inflation works. We kind of know how it worked 40 years ago, but a lot has changed.

Under Volcker, it took negative growth of 2% to bring inflation down. Maybe now, all it takes is slowing growth from 1.5% to 1.3%. The problem is that no one really knows.

1. December 2022 at 21:39

Scott,

“I’ve been a growth pessimist for a decade, and I think events have vindicated my pessimism.”

There was a 60% increase (15% go 23.8%) in the federal capital gains tax rate a decade ago. Not exactly rocket science.

1. December 2022 at 22:19

TF, Just to be clear, I am NOT forecasting a recession in 2023. I don’t believe that recessions are forecastable.

2. December 2022 at 03:08

You are essentially subsidizing the banking system by forcing mom and pop to pay an additional 6% tax (assuming inflation remains at 6%) and even if you reach your proposed target of 2% it’s still unjust and unethical.

Great economies improve purchasing power, they don’t destroy purchasing power.

Deflation is better than inflation, and it should be allowed.

GDP doesn’t matter. What matters is what you can buy for your money, and U.S. citizens live in poverty when compared to the real incomes of most of the world, particularly in middle income countries like Thailand, where $1500 dollars per month can give you a pretty great lifestyle or in Vietnam where $500 a month is enough to be considered middle class: i.e, enough to see movies once a week, dine out twice a week, afford a pretty good house/apartment, etc.

You and these monetary guru’s, these thugs in disguise, these megalithic, monolithic, neolithic gangsters, need to stop intervening in the marketplace, creating busts and bubbles, through manufacturing investment. If you keep interests rates near zero, then one doesn’t have to be an economist to know that any investor will buy up equities they don’t want and don’t need, but do so anyway because its the only damn choice they have. They certainly aren’t going to buy negative rate bonds. This inflates the market price well above equilibrium, and at some point it has to come back down to earth. The credit will come due. The loans will need to be repaid. The interest rates will climb. Bankruptcy will ensue in dramatic fashion, and thugboys like Sumner will be laughing at Mr. Joe the plumber, asking him to pay for their bad mistakes through more quantitative easing or to bail out AIG because they insured bad bonds.

You’re a tyrant. A utilitarian mega thug. A benthamite hoodlum, a hooligan who thinks the rules don’t apply to him.

And there is nothing I despite more than a egotistical, self rightous, golden pedestal mobster, sitting in his ivory tower, using people as a means to his end.

2. December 2022 at 07:37

Sara, You said:

“U.S. citizens live in poverty when compared to the real incomes of most of the world”

Hmmmm . . .

2. December 2022 at 14:40

Sara

“or in Vietnam where $500 a month is enough to be considered middle class: i.e, enough to see movies once a week, dine out twice a week, afford a pretty good house/apartment, etc.”

ROFL. I live in Vietnam. You’re ignorant and an idiot.

2. December 2022 at 16:35

Scott, any reaction to the recent fall in the Atlanta GDPNow estimate of 4th quarter (real) growth? From 4.1% to 2.8%