Mark Sadowski on monetary stimulus, currency depreciation, and trade balances

Before beginning, let me point out that many people seemed to misread my previous post. I was making no claims about causality. God knows I’m no expert in criminology! I was making a joke about people with a certain blind spot—incentive effects.

Over at Econlog I have a post discussing Edward Hugh’s recent piece on Abenomics. At the end I cited a comment by Mark Sadowski. This post will be another of his excellent comments:

Scott,

Off Topic.This claim by Edward Hugh reveals he really doesn’t get it.

“But it’s worse, the monetary expansion has driven down the value of the yen but in the context of the second arrow – a double digit fiscal deficit – this drop in value is leading to a growing not a declining trade deficit. The FT’s Tokyo bureau chief, Jonathan Soble, has an enlightening recent piece on this…”

Although Japanese nominal exports have surged by 15.2% between 2012Q4 and 2013Q3, nominal imports are up by even more, or by 16.5%:

http://research.stlouisfed.org/fred2/graph/?graph_id=149566&category_id=0

Devaluation improves a country’s trade balance only if the Marshall-Lerner condition on trade elasticities holds, and research shows that they’re not met in the majority of cases, either past or present:

http://www.emeraldinsight.com/journals.htm?articleid=17056473

That’s not to say that currency devaluation isn’t beneficial, of course it is, but the benefit flows primarily from increased domestic demand. Here is a study of the competitive devaluations of the Great Depression by Barry Eichengreen and Douglas Irwin:

http://www.nber.org/papers/w15142.pdf

An examination of Figure 4 on page 48 reveals that the only countries that experienced import growth from 1928 to 1935 (the UK, Japan, Sweden and Norway) were members of the sterling block that devalued early (1931). In most of these countries net exports actually declined over the period because imports rose more than exports.

The order of recovery from the Great Depression follows the order in which they abandoned the gold standard perfectly:

http://fabiusmaximus.files.wordpress.com/2009/03/gold.png

But this wasn’t because of increased net exports.

The US devalued in 1933 which immediately led to a swift recovery from the Great Depression. Nominal exports doubled from 1933 to 1937. But nominal imports increased by 110.5%:

https://research.stlouisfed.org/fred2/graph/?graph_id=120991&category_id=0

As a result net exports went from a small surplus (about 0.2% of nominal GDP) to being roughly in balance.

France was part of the Gold bloc of countries that devalued late (1936). From 1936 to 1938 nominal exports increased by 95.4% and nominal imports increased by 80.9%:

https://research.stlouisfed.org/fred2/graph/?graph_id=120992&category_id=0

However, since imports were already substantially greater than exports, the nominal deficit actually increased by 55.4%.

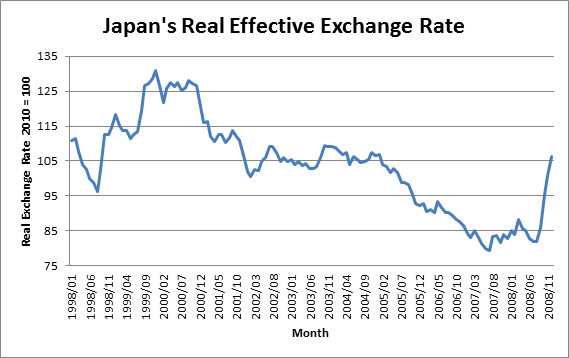

Japan’s original ryÅteki kin’yÅ« kanwa (QE) was officially announced in March 2001 and concluded in March 2006. The following is a graph of the BOJ’s estimate of Japan’s real effective exchange rate which is trade weighted with respect to 16 different currencies and takes into account their relative inflation rates:

http://thefaintofheart.files.wordpress.com/2013/06/sadowski2b_1.png

The real effective exchange rate fell from 116.25 in February 2001 to 91.09 by March 2006, when the BOJ announced the completion of QE, a decline of 21.6%.

Exports rose from 10.2% of nominal GDP in 2001Q4 to 19.3% of GDP in 2008Q3. Imports rose from 9.4% of GDP in 2001Q4 to 19.5% of GDP in 2008Q3. From 2002Q1 to 2008Q1 real (adjusted by the GDP implicit price deflator) grew at an average annual rate of 11.0%. Real imports grew at an average annual rate of 12.1%.

So there was boom in both exports and imports. But imports grew faster than exports, and net exports actually moved from surplus (0.8% of GDP) to deficit (-0.2% of GDP) between 2001Q4 and 2008Q3:

http://research.stlouisfed.org/fred2/graph/?graph_id=120989&category_id=0

It’s very telling that today the only major currency area up against the zero lower bound in interest rates that hasn’t done QE (the Euro Area) is also the only major currency zone where the trade balance has improved substantially since 2009, going from 0.6% of GDP in 2009Q1 to 3.3% of GDP in 2013Q3:

https://research.stlouisfed.org/fred2/graph/?graph_id=149559&category_id=0

But this has occurred in large part because nominal imports have been falling since 2012Q3 due to falling domestic demand. Nominal exports have barely changed since 2012Q3.

{kind=link}

{kind=link}

I’d add that Greece has done an especially good job of “improving” its trade balance.

Tags:

3. March 2014 at 09:09

If the effect of a market driven decline in domestic nominal spending is lower exports relative to imports in the world market stage, then that suggests investment in export industries was unduly expanded prior.

Speaking of blind spots, those partial to MM are blind to the negative effects to the real economy caused by inflation. As a result, they treat all output reductions associated with NGDP reductions to be ipso facto unnecessary, such that the domestic central bank has a “duty” to inflate more to ensure that the same undue relative expansion of exports continue towards the point at which further accelerated inflation of the mpney supply is unable to keep the malinvestment going, where central banks are faced with the inevitable and ultimate choice of hyperinflation or recession.

Thankfully, the ECB has, like the Fed, chosen recession. But we don’t need to keep being inflicted with recession. The CB can be abolished.

3. March 2014 at 09:32

Of course, the same argument is true for imports falling relative to exports.

If domestic nominal demand changes were the cause, then we should see roughly equal declines on both imports and exports when there are changes to domestic nominal demand.

And, for that matter, should also sew roughly equal relarive changes to the various stages of production.

Of course, in reality we typically see significant relative changes to imports versus exports, as well as the various of production. And, because it takes time for such errors to be corrected, and for capital and labor to be reallocated, it is not evidence against the credit circulation theory of the business cycle that we see temporary declines in (aggregate) output. It is expected, for the same reason that a homebuilder who half finishes a house before realizing he made miatakes in calculation, that we don’t see him instantly take over another half finished project and go on as if there should be no change to his output.

NGDP changes isn’t the cause for the business cycle. NGDP changes are an effect of real errors being exposed, and corrections take time which of course leads to temporary reductions in spending. It makes sense that a home builder will not instantly change his spendong from housin materials and labor, to something else. It takes time for him to find out the new plans of others who also made mistakes. It is expected that his spending would temporarily decline as he readjusts with others.

MM theory is based on false inferences from observed data. It is too mechanical. Too superficial. To data driven. There is little to no understanding of how the market process works. Understanding how the market process works explains everything we observe. It explains why there was a reduction in spending 2008-2009. It explains why capital and labor didn’t instantly be reallocated to new projects such that spending did not fall.

It is not the job of a CB to prevent NGDP from falling. Its job is to benefit the banks. Gradual price inflation was thought to help not the working class, but fractional reserve banks, because it helps them expand credit ex nihilo at roughly the same rate, which is required to avoid bank runs bankrupting a particular bank due to relative overexpansion of credit compared to other banks.

3. March 2014 at 11:44

John Williams projects that the first rate hike will come with unemployment at 6%, inflation 1.5%. Emphasizes the risk of overshooting.

http://www.ft.com/intl/cms/s/0/b122500c-a1ee-11e3-87f6-00144feab7de.html#axzz2uvkjt3CF

3. March 2014 at 13:03

To follow up on Michael Byrnes’ comment above, Williams’ most recent estimate of NROU is 6.6%:

http://www.frbsf.org/economic-research/files/el2011-05-update.pdf

Aren’t you glad the economy has fully recovered? (Hint: that’s sarcasm.)

3. March 2014 at 13:15

Scott,

Off Topic.

Carlo Rosa and Andrea Tambalotti take a closer look at the effects of unconventional monetary policy and conclude that it’s a lot like…conventional monetary policy.

http://libertystreeteconomics.newyorkfed.org/2014/03/how-unconventional-are-large-scale-asset-purchases.html

“…From this evidence, we conclude that LSAPs have effects on financial conditions that are very similar to those of more conventional approaches to providing monetary stimulus; they move asset prices in the same direction and in roughly similar proportions. This conclusion does not guarantee, of course, that LSAPs are similar to conventional policy in their effects on the macroeconomy, which is the ultimate target of any monetary policy intervention. However, changes in broad financial conditions are one of the main conduits through which monetary policy impulses are transmitted to the rest of the economy, which suggests that the macroeconomic effects of this unconventional policy might also be fairly conventional after all.”

So evidently an open market operation by any other name is still an open market operation.

Can we stop with the pretense that QE is something totally strange and new? Central banks have been quantitative easing for over 350 years.

3. March 2014 at 14:20

Scott,

For some reason the link to the Eichengreen & Irwin paper is going to the wrong paper (the link reads correctly). Please replace it with the following link when you can:

http://www.nber.org/papers/w15142.pdf

3. March 2014 at 14:41

Mark Sadowski needs his own blog.

3. March 2014 at 15:18

Arnold Kling reviews Calomiris’s new book:

http://www.econlib.org/library/Columns/y2014/Klingbanks.html

4. March 2014 at 03:36

No HT huh, though Mark became aware of the fist full of dollars piece over here?

http://diaryofarepublicanhater.blogspot.com/2014/03/morgan-warstler-says-he-knows-how-i-can.html?showComment=1393797582676#c6935537912778039187

4. March 2014 at 03:57

OK it’s possible he heard of it elsewhere LOL.

4. March 2014 at 04:02

This is a very good post, I am glad that (unsurprisingly) you acknowledge that most of the positive effect of expansive monetary policy in form of currency depreciation (as in other forms too) comes from rising domestic demand and not from export.

Which is in a way contrary to another post of yours “Oh, so it’s stimulus you need” where supposedly cutting wages while increasing VAT does a similar job.

In the same vein there were some theories that Argentina got out of the worst mostly thanks to bullish commodity markets in oughts. In reality exports (and comodity exports) were responsible only for few percentage points of recovery (in real terms), most of the work in reemploying labor was done domestically. If you are interested here is more: http://www.cepr.net/documents/publications/greece-2012-02.pdf

4. March 2014 at 16:08

Reasoning from a price change:

http://www.businessinsider.com/5-questions-for-richard-bernstein-2014-3

“The issues in EM actually benefit the US economy. Lower commodity prices, a stronger dollar, and a rush to US assets are all good for the US. Certainly, it’s not all good for US multinationals, but it could be a very good environment for domestic US stocks.”

4. March 2014 at 17:18

Reasoning from a price change is flawed.

Reasoning from a spending change is flawed.

5. March 2014 at 17:22

Mark, I’m seeing lots of really high estimates of the natural rate. Even the administration has unemployment at 6.7% in 2015. What’s going on?

I like that piece you linked to on QE being “conventional.”

Travis, Love that Kling review, I agree with everything.

Good catch on reasoning from a price change.

JV, Good point about Argentina

11. July 2016 at 14:16

[…] early 2014 in a discussion about Abenomics Scott re-posted a classic comment from the legendary Mark Sadowski. The punchline is very […]