Last laughs, etc.

In a recent post I criticized a headline on cryptocurrency bubbles. Ryan Avent (who wrote the piece) told me to read the entire article, which is indeed much more nuanced in its discussion of whether Bitcoin is a bubble. I should have pointed that out.

I’m not sure when I first predicted that (misdiagnosed) bubbles would be the new norm of the 21st century. This is from January 2014:

I’ve also argued that low rates will create more “bubbles” in the 21st century.

And here’s what I said in July 2011:

My most important argument is that low real interest rates might be the “new normal.” . . .

But (seriously) are stocks now overvalued? Because I’m an efficient markets-type, the only answer I can give is no. So why does Robert Shiller say yes? Apparently because the P/E ratio is relatively high by historical standards. And he showed that for much of American history investors did better buying stocks when P/Es were low than when P/E ratios were high. Of course hindsight is 20-20.

[I feel so sorry for people who make their investment decisions based on Robert Shiller’s public statements.]

So how has my prediction held up? Are so-called “bubbles” the new normal of the 21st century?

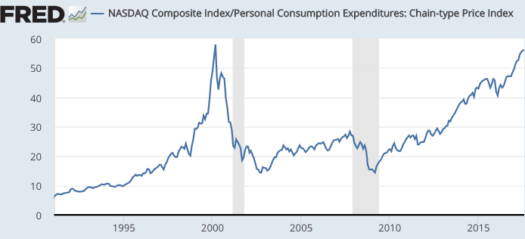

Here’s the real NASDAQ index:

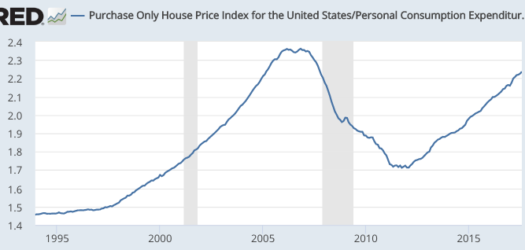

And real house prices:

And real house prices:

(Both indices deflated by the PCE price index.)

(Both indices deflated by the PCE price index.)

And Bitcoin:

All three major “bubbles” occurred after my predictions.

All three major “bubbles” occurred after my predictions.

Bubbles, bubbles, as far as the eye can see.

Tags:

2. November 2017 at 09:46

Scott, how does this logic work:

If bubbles are real, it means the economy itself is a bubble. Why do oil or wheat have the value they do? Is it because they have “true” value? No. It’s because people believe in their value, and the measure of belief — informed by factors like usage of the products — determines the quantity/quality of the value. Likewise, a stock bubble is like when investors believe one thing and then change into believing another thing. They may one day believe a stock is worth $2 then another day believe it’s worth $1. The rationalization for the change in belief could come from a reduction in asymmetry of information such that investors now “know better” and “know” the stock “should” be valued less. Voila, it’s a “bubble.” But what really happened is belief changed (this holds true even if the belief change doesn’t emerge from information asymmetry reduction).

2. November 2017 at 11:57

I think you’re being generous to compare only real values. The $20 Bill in my pocket since 2009 has lost real value and so has my money market fund. People who think everything is a bubble have to invest somewhere.

2. November 2017 at 13:03

Why all the gnashing of teeth over the b-word? Setting aside the word, do people really not believe that an asset can be temporarily overvalued and prone to drop sharply (before perhaps one day recovering)?

2. November 2017 at 13:51

My financial koan: There is no such thing as money because there is no such thing as value.

2. November 2017 at 13:55

msgkings,

I don’t get what you mean be “overvalued”. There’s always a buyer and a seller at a given point in time and they determine the price. It’s simple supply and demand. Sure the price will most likely raise and fall in the future (and frequently by a lot) but why in the world would this mean that the price was “overvalued” at this certain point in time when the price was established?

Were housing prices “overvalued” in 2007? Were they “undervalued” in 2011? And now are they “overvalued” again? Which price is the “eternal” correct one according to you?

A price is just a neutral piece of information about supply and demand at a certain point in time. Nothing more and nothing less. There is no right and wrong (as long as there is no illegal price manipulation, I guess).

2. November 2017 at 14:12

Came across this attempt to reconcile Austrian and monetarist views of business cycles. Includes a notion of bubbles, but seems to be try to be EMH friendly about it.

https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2616057

2. November 2017 at 15:48

Crypto currencies are money.

The mentality of “dollars is the standard, therefore anything sold for dollars is an investment if there is going to be an investment” is over.

2. November 2017 at 16:34

Yes, but how about a chart on gold or on certain art pieces, or briefly hip Shaker furniture?

Bitcoins? The night is still young.

How about those Franklin Mint collectibles?

Was it just as wise to invest in a Franklin mint collectible as to invest in an ETF of the S&P 500?

2. November 2017 at 16:38

My point is “investments” such as gold or Franklin Mint collectibles can have bubbles. The value is arbitrary.

2. November 2017 at 20:51

NASDAQ and housing got back to their previous PCE-deflated levels mainly because of decline in interest rates. At both of their peaks (1999 and 2005), other assets had far better returns. 10-year Treasury rates in 1999 peaked near 7%. In 2005, they were 5%. This much more than kept with PCE over the next 10 years.

It’s debatable whether “bubble” is the right term, but yes I do think these assets were mispriced. You would have lost money if you invested in them at their peaks. The fundamentals foretold as much (P/E for 1999 stocks, price/rent for 2005).

2. November 2017 at 21:30

Bitcoin is like gold, I guess. Its “value” depends on how much people psychologically value it.

Gold was hot in 2012. It went from $1800 in 2012 to $1400 now, while S&P went from $1400 to $2600. In 1980, gold did even worse. Gold went from $600 to $300 1980-2001, while S&P went from $100 to $1200. In the end, S&P did 24x better than gold.

The EMH can give a circuitous defense. Gold was priced right because its value is what people paid for it. But in the end gold’s demand was fickle. There has to continually be the same level of demand to sustain the same price.

Stocks give dividends, which ultimately have sustainable underlying demand. For example, people will keep reliably buying iPhones, gasoline, airplanes, etc. Pure land and buildings have sustainable demand from future rents.

Gold and bitcoin just show much more fluctuating and fickle demand. Maybe when this demand is very low, they will be a good investment betting on demand returning to mean. This is much more likely for gold than bitcoin, and demand has to be very low to offset the fact it doesn’t pay interest or dividends.

3. November 2017 at 05:52

With respect to the argument that the price recoveries are driven by low rates, I’d propose that the counterfactual has to be that the Fed reacts better in 2008 and that our NGDP growth continued along the 5% path that had been in place for the prior 25 years. In that case, NGDP today would be $23.7 trillion instead of $19.5. My guess is that housing prices and stock prices today would be even higher today in that counterfactual world (nominally speaking).

3. November 2017 at 09:59

bill,

That’s a decent point about NGDP growth. However, the alternative assets would have still done better under a normal NGDP growth path. To be sure, buying houses in 1999 and stocks in 2005 did better than vice versa under any NGDP growth path.

Some EMH advocates would dismiss that as ex post. But the mispricings were called contemporaneously based on fundamentals. Then they turned out to be correct.

3. November 2017 at 11:49

Thanks Matt,

Who called those bubbles contemporaneously?

Especially anyone who called both.

3. November 2017 at 13:52

bill,

Off the top of my head, here is Warren Buffett in 1999.

http://archive.fortune.com/magazines/fortune/fortune_archive/1999/11/22/269071/index.htm

Krugman in 2005 on housing.

Running Out of Bubbles https://www.nytimes.com/2005/05/27/opinion/running-out-of-bubbles.html

I disagree with Krguman’s general analysis that the economy “needed” a bubble to keep economic growth going. That gets more technical. But he was correct that housing was mispriced.

Many others called a bubble as well. I have vague memories of arguing with people that housing wasn’t a bubble in 2005 or 06, when I first started reading economics blogs. Whoops.

3. November 2017 at 14:48

Matt,

Thanks for the links.

I actually remember reading the Fortune article at the time. I agree with Buffett. But I don’t see where he called the market a bubble? He simply said that returns over the next 17 years wouldn’t be like the prior 17 years (which had been 19% per year!).

I went (link below) and calculated that the S&P 500 returned just over 5% since this article was written. For people like me, who just left the 401k contributions on auto-pilot (so only a modest percentage of our investments happened around the peak), the best thing to do was just ignore the talk of bubbles and continue dollar cost averaging.

http://politicalcalculations.blogspot.com/2006/12/sp-500-at-your-fingertips.html#.WfzrGFtSyUk

I think the 5% is very close to Buffett’s prediction.

Regarding Krugman’s prediction, let’s assume that this is the first time he made the call. I say that because even Krugman references Shiller’s Irrational Exuberance call as a great call, but Shiller started making that call in 1995 or 1996. The graph I found on FRED has a May 2005 value of 169.35 and a Sept 2017 value of 192.47. A 13.6% increase over 12 years, 4 months. About 1% per year with compounding. Add in a “dividend” of occupying the house and the return is decent. Most other housing bubble predictors did a good bit worse than PK. Baker made his call in August of 2002. I feel sorry for people that listened to him then.

https://fred.stlouisfed.org/series/CSUSHPISA

And most of the people that argued with you in 2005/2006 couldn’t do anything with that info anyway. OK, if you’re about to buy the first house, you can wait (a friend of mine did that. He waited from 2003 until January 2007, so that wasn’t a good move). And retirees can sell and move to rentals. But most of us have a house and just have to ride it out. Transaction costs are too big.

If I haven’t convinced you, that’s fine. I’m sticking with my EMH, index fund, ignore the news mindset. Keeping it simple.

3. November 2017 at 15:08

Matthew Waters,

housing was mispriced

When exactly was housing “mispriced”?

Give a specific date or year, please.

3. November 2017 at 19:56

I said the year 2005 numerous times in my posts.

3. November 2017 at 20:08

Matthew, What evidence do you have that housing was mispriced in 2005?

3. November 2017 at 21:58

Price-to-rent in 2005 went up 50% from 2002 to 2005. Even today, with much lower interest rates than 2005, price-to-rent in 2005 was 28% higher than 2016.

https://1.bp.blogspot.com/-tRDWvBqh3xg/WJCsZb2WK5I/AAAAAAAAqCI/Z4rgXBerW6of0ejOMLcXeKATbDLSM3HywCLcB/s1600/PriceRentNov2016.PNG

Like with the 1987 crash, either the market is inefficient today or it was inefficient in 2005. For buyers to be completely efficient both times just does not make sense. Rent-to-price ratios should be higher today as long-term interest rates are lower.

Anti-EMH arguments are tough to make because what the EMH is moves around a lot. I learned it in school as “market prices reflect all publicly available information.” But the goalposts often move to “it’s tough to beat the market.” Those are two very different things.

Mispricings can be very difficult to impossible to capitalize on. Shorts have margin calls and short squeezes. It would be very difficult to short Bitcoin and hold on for years. But it’s simple to not invest in Bitcoin. Same with buying stocks in 1999 or housing in 2005-06. It matters if a market is mispriced, even if you can’t make unlimited amounts of money betting against it.

10. November 2017 at 12:27

Matthew, You said:

“Like with the 1987 crash, either the market is inefficient today or it was inefficient in 2005.”

Even if true, that has no bearing on the bubble theory.