Keynesians should have supported the 2014 Japanese tax increase

Perhaps because the recent recession was so deep, many people seem to have forgotten the distinction between cyclical and long run issues. Aggregate demand policies are important in certain respects, and you’d be hard pressed to find any blogger who has complained more than I have about AD shortfalls. But nonetheless AD is a cyclical problem, a short run problem. AD can’t fix structural unemployment, and it has nothing to do with income inequality. It also has nothing to do with big government. It also has nothing to do with “interventionism.” When I read that some conservatives are suspicious of AD, it makes me think they are suspicious of reality. Any possible policy regime, including complete laissez faire, has very important implications for the path of AD over time.

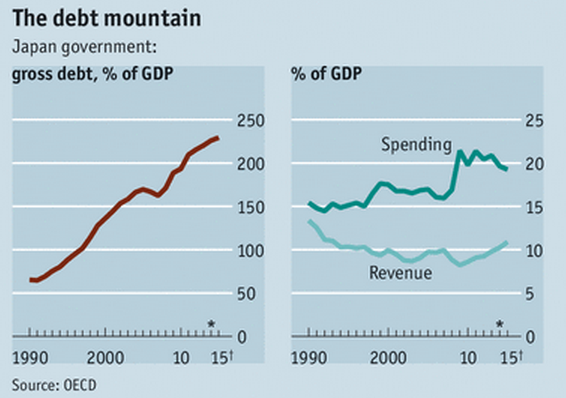

I was particularly dismayed to see that some Keynesian economists opposed the 2014 Japanese tax increase, and then later claim the policy failed. Both views are absurd. Here’s the budget situation in Japan:

The central government is only collecting about 10% of GDP in taxes? You have to be kidding me. And the problem has been going on for decades, and it’s getting worse? That’s not the Keynesian economics that is taught in the textbooks. I was taught you run deficits when unemployment is high, and surpluses when unemployment is low. Is there some new theory I haven’t heard about yet?

OK, but doesn’t Japan have lots of unemployment? Everything is relative, but I’d say their unemployment problem is less today than at any other time in the past 18 years, with an official rate of 3.3%.

Yes, in the 1980s it was even lower, at around 2%. But if not now, then when? And how do the Keynesians claim that this policy failed? In the Keynesian model a tight fiscal policy fails if it is done when unemployment is high, or if it is done when the rate is low, but the policy sends unemployment much higher. But neither is true in this case. Unemployment was low when the tax was enacted, and has since fallen even lower. How is that a failure? Perhaps some of the Keynesians that got the facts wrong in the US in 2013, and also in Britain, will now step up and admit they were wrong in claiming that the Japanese tax increase failed. Japan’s policy was an almost perfect example of Keynesian economics in action. You fix the roof while the sun is shining. You fix your long run fiscal shortfalls when the unemployment rate is low. Sales surged right before the tax increase and dropped sharply immediately after (affecting RGDP), but firms knew this was just consumers beating the tax increase, and hence companies did not lay off workers.

And please don’t say that deficits are no problem because interest rates are low, and will remain low for many years. “Many years” is not forever. Suppose the Japanese debt eventually gets up to 400% of GDP, and interest rates rise to 5%. Then it would take 20% of GDP to simply service the debt. But they only collect 10% of GDP for all central government activities! (I know, they can borrow 20% of GDP each year to service the debt. Why didn’t I think of that?)

The other argument is that the net debt is lower, as the BOJ has bought up a lot of debt. But modern central banks no longer “monetize the debt”, they swap interest-bearing reserves for interest-bearing bonds. If interest rates rise they’ll either have to sell off the debt (which increases the stock of net debt held by the public) or pay interest on the debt (and remember that central banks are de facto part of the government), or let hyperinflation occur.

When something seems too good to be true, it usually is. The idea that the Japanese can keep financing a modern welfare state with more and more elderly people by collecting barely over 10% of GDP in taxes at the federal level seems too good to be true. I submit that the reason it seems too good to be true, is because it is too good to be true.

PS. Any commenter who criticizes this post loses the right to ever again criticize me for anti-Keynesian views on fiscal policy. This post is 100% consistent with standard textbook Keynesian economics.

Tags:

24. June 2015 at 10:39

Usually you think that the market is smarter than you. Do you really think that without increasing VAT the market would have expected Japan to have hyperinflation? That 1 USD would have been worth 200 or 300 JPY (because market players should calculate even far future scenarios).

24. June 2015 at 10:48

According to Simon Wren Lewis, taxes aren’t part of Keynesian stimulus/austerity, so they definitely should have supported it. Of course, it’s unclear if he actually means that or only when it’s convenient.

24. June 2015 at 11:13

There was only one year when unemployment in Japan was higher than in the U.S.: 2000

https://research.stlouisfed.org/fred2/graph/?g=1kp1

24. June 2015 at 11:40

Jonathan, You said:

“Do you really think that without increasing VAT the market would have expected Japan to have hyperinflation?”

No.

Robert, You said:

“According to Simon Wren Lewis, taxes aren’t part of Keynesian stimulus/austerity”

If so, then why pay attention to what he says? Taxes are a part of the Keynesian model.

E. Harding, Yes, they usually have lower unemployment than we do.

24. June 2015 at 11:41

Whenever I hear the US is going down some king of Goldbug fiscal failure, I always point out Japan goes first and then a bunch of European nations (Germany?) follow the next ten years. Then other East Asian nations, Korea, and China will have their big bust and finally, the US has the great Social Security bust in ~2050. (Ain’t that comforting to say we go last although India goes way after!)

Taking economics in the Bush Sr. administration, watching Japan the last 25 years appears to breaking all the rules of my old Macroeconomic Textbook. Has government spending crowded out the private sector? It seems not as interest rates have been low forever. Did Japanese suddenly lose productivity and competitiveness? Maybe but what made them so competitive in 1988 and uncompetive in 1998? The culture did not change that much.

I still it is something far deeper and Krugman identified years ago with the 1970s their Baby Bust. So having a small population at first increases your nation’s competitiveness (Japan 1980s/China Today). Then in 20 years it is impossible to increase AD because your working population turns 50 and spends less while there is limited young people increasing the AD curve. Then in 30 years, the AS curve goes down as the labor population starts decreasing. And they have hit some kind of demographic spiral. In reality, I believe Ukraine actually hit this spiral first in 2013 but the sort of Civil War/Russia invasion crisis hit first.

24. June 2015 at 12:48

“But modern central banks no longer “monetize the debt””

It very much looks like that’s what the Bank of Japan is doing: http://www.project-syndicate.org/commentary/japan-monetization-government-debt-by-adair-turner-2015-03

24. June 2015 at 13:01

I think that generally speaking Keynesians don’t like sales taxes as they are regressive. And it’s easy to call the sales tax a failure as it lead to a recession.

Unemployment may be low but isn’t’ that due supposedly to the the fact that Japan allegedly engages in ‘crony capitalism’ that is in need of reform?

Japan unemployment is always low, the problem is no growth not employment. After all Japan is said to have had 20 years of stagnation. During the entire period there UR was low.

24. June 2015 at 13:23

Why are you lashing out at me? Maybe I’m being sensitive, but I thought it was clear I was tweaking him, with the charge of only believing it when convenient for his argument.

24. June 2015 at 15:00

I have an idea. How about stopping the redefining of the phrase “interventionism” so as to arbitrarily exclude rigid, unchanging, “peg” like….intervention?

The meaning of intervention is not ad hocism, or discretionary intervention. It means government activity in what would otherwise be a free market economy.

Intervention does not become intervention only when there is a recession. It occurs when there would otherwise be a laissez faire economy.

Rigid mechanical price targeting by the government (via the governmental counterfeiting institution) is an intervention.

Rigid mechanical aggregate spending targeting is an intervention.

Just because an intervention is rules based, does not mean it is no longer an intervention.

It is more useful to define intervention as government activity in what would otherwise be a free market, so that we can identify what the government is doing as opposed to what private property owners are doing.

The claim that central banks targeting aggregate spending is not an intervention on the unstated, implicit, definitional grounds that Sumner wants people to believe that we should not consider his socialist intervention as intervention simply because the intervention is based on an unchanging rule set by the Sumner. He does not want to be viewed as pro-interventionist, even though that is what he is. Pro-interventionist. He does not want the free market process to decide aggregate spending. He wants the government to decide itz and impose it, and he wants the government to agree with his socialist rule.

Any rule set by the government, which Summer’s NGDPLT would have to be, is very much intervention, because that activity intervenes in what would otherwise be laissez faire.

Yes ladies and gentlemen, contrary to “true libertarian” Sumner, the counterfactual to intervention is laissez faire.

—————–

Let nobody be misled into believing the lie that central bank intervention according to ANY rule somehow “has nothing to do” with inequality. When the activity of the central bank consists of increasing the bank balances of the “member” banks first, the claim of a so-called economist that inequality is not associated with it constitutes academic fraud.

24. June 2015 at 16:08

I don’t understand the data cited in the charts. According to the OECD Japan government spending is 42.3% of GDP, so I’m not sure where the 19% comes from. Perhaps these are taxes and spending net of transfers? That’s plausible, but if so I can’t find that info on the OECD website.

24. June 2015 at 18:26

Excellent blogging.

But this post reminds that much about “monetarism” is some sort of “theo-monetarism” or psuedo-religious genuflection to monetary icons.

Why can central banks only place reserve into commercial banks, when they buy bonds? Is that a divinely inspired rule?

Why not have central banks simply monetize tax revenues and grant tax breaks?

Why not have a FICA tax holiday, and have the Fed print up the lost revenues and place them into the Social Security and Medicare trust funds?

Would that “cause inflation”?

Answer:

1. Isn’t that the idea (in part).

2. FICA tax breaks might not cause inflation—the cost of business would go down, not up.

3. Is placing assets into the SS and Medicare trust funds more inflationary than giving assets to banks, who might lend them out?

It seems to me that much about monetary policy is th result of regulatory capture.

Gee, the Fed conducts QE, and the primary dealers earn transaction fees on literally trillions of dollars of transactions, and the commercial banks get $4 trillion in interest-bearing deposits.

Oh, sure, but tax monetization is a bad idea. Why?

It is not part of accepted theomonetarism.

24. June 2015 at 18:44

Britonomist, That article is wrong for reasons I spelled out in this post.

And the claim that the problem can be “solved” by raising reserve requirements is an EC101 level mistake.

Robert, Sorry, I certainly didn’t mean to lash out at you, I must have worded that poorly. The claim was ludicrous, and so if he made that claim I was lashing out at him. Maybe even that was a mistake, before I saw the exact wording of what he said. But obviously tax changes are a big part of Keynesian economics, I think almost all Keynesians accept that fact.

dbeach, I assumed it was just central government spending, but I’m not sure.

24. June 2015 at 19:41

“Suppose the Japanese debt eventually gets up to 400% of GDP, and interest rates rise to 5%. Then it would take 20% of GDP to simply service the debt. But they only collect 10% of GDP for all central government activities!”

If they tax interest income at 50%, just like Amurika does, then tax receipts will surge by 10% of GDP.

Ok, that only solves half the problem. 100% interest income tax?

24. June 2015 at 22:02

I’m Ray Lopez and I approve this (Sumner) message.

Now if Sumner can only make the logical next step and renounce NGDPLT, and embrace the gold standard, as well as 100% reserve banking (full reserve banking), we can be friends. Why do I have to sound like a movie villain when I type this?

24. June 2015 at 22:38

– Keynesians overlook the fact that any keynesian stimulus can run into a brick wall called “Demographics”.

– Japan has run into that brick wall around 1995. The US, Europe & Australia have run into that brick wall in 2008 & 2009. And all won’t be able to “break down” that brick wall.

– Yes, income inequality does have major impact on AD.

– Japan has A LOT OF hidden unemployment. If all large companies would fire the workers they don’t need then unemployment would shoot higher.

25. June 2015 at 05:39

Steve, But wouldn’t investors demand a higher before tax rate to offset the tax? (Yes, I know you were half kidding.)

25. June 2015 at 07:19

In “Sachs and the age of diminished expectations” he excluded taxes and transfers from calculations. In comments of it he said Ricardian Equivalence makes it debatable whether to include taxes or not. He may be right (though I doubt it), but it seems like he’s doing Wren-esian analysis, not Keynesian analysis. Haven’t seen Krugman criticize or even note his tax exclusion in any of his references to SWL’s work.

25. June 2015 at 10:30

“And the claim that the problem can be “solved” by raising reserve requirements is an EC101 level mistake.”

Please elaborate, Adair Turner is definitely not the sort of person that makes ‘EC101’ mistakes.

25. June 2015 at 21:17

Britonomist:

The Adair Turner piece is nonsensical. “The bigger economic stimulus derives from the government’s continued large fiscal deficits”. These deficits have been running for years and years but have provided no stimulus, but mostly stagnation and sometimes recession.

“Funding” them via the BoJ is monetary stimulus not fiscal stimulus. And it’s so obviously not monetisation, just look at the price of money. Inflation has barely budged. Is Adair Turner blind?

26. June 2015 at 00:39

@James in London

‘ “These deficits have been running for years and years but have provided no stimulus, but mostly stagnation and sometimes recession.

“Funding” them via the BoJ is monetary stimulus not fiscal stimulus.’

So ‘monetary stimulus’ has ‘provided no stimulus’?

26. June 2015 at 09:30

@James

“These deficits have been running for years and years but have provided no stimulus, but mostly stagnation and sometimes recession.”

I cannot evaluate this claim without a counter-factual.

“”Funding” them via the BoJ is monetary stimulus not fiscal stimulus.”

I don’t care whether it’s fiscal or monetary stimulus, to me that’s just unimportant semantics.

“And it’s so obviously not monetisation, just look at the price of money. Inflation has barely budged. Is Adair Turner blind?”

A) The ‘monetisation’ maybe offsetting highly deflationary forces, causing the net effect on inflation to be marginal.

B) Aggregate supply may not be a linear slope, and may be flat in some places (excess capacity etc…), meaning that monetisation wont necessarily cause excessively high inflation in some circumstances.

26. June 2015 at 10:35

Am sure Scott could answer but I can’t resist trying.

Postkey:

Only when Abenomics, or rather Kurodanomics, started did Japan get monetary stimulus. Up until Kurodanomics the BoJ was offsetting fiscal stimulus thanks to its IT obsession. And if you don’t have the IT obsession you don’t need fiscal stimulus.

Britonomist:

How simple do we have to make this?

Japan had been running big fiscal deficits with no stimulus affect. Keynesians should have been in 7th heaven as the debt to GDP rose to over 200%. But they weren’t because it wasn’t working. Japan loosens monetary policy by targeting higher inflation, using QE (despite the mythical constraint of the ZLB), tanking the currency, and suddenly the stock market roars, inflation starts to rise and unemployment falls even further, all despite a withdrawal of some fiscal deficit “stimulus” via a VAT rise. Official RGDP was hit a bit by that VAT rise but a recession it clearly was not. The markets have made all this very clear.

If you are not devaluing money then you are not monetising. Any deflationary forces would be seen off in no time by a government set on inflation. Those forces are puny compared to a monopoly of the printing press.

26. June 2015 at 13:58

Robert, If deficit reduction is not contractionary, then why do the Keynesians keep complaining about the deficit hawks?

Britonomist, Reserve requirements are simply a tax, and raising them is simply fixing a revenue shortfall by raising taxes.

Postkey, Japan didn’t start doing any monetary stimulus until about 2013, before that the currency injections were temporary.

27. June 2015 at 06:11

James:

Economics is rarely simple. Again, you can’t say it had no stimulative effect without making a plausible case first that the counter-factual of no deficit would have resulted in the same or more growth and/or inflation, which you haven’t done.

“If you are not devaluing money then you are not monetising. Any deflationary forces would be seen off in no time by a government set on inflation. ”

You just literally said that the currency ‘tanked’, this is becoming pure sophistry. Your whole position is incoherent because you’re essentially saying that the recent QE isn’t monetization because if it was monetization the currency would be devalued – while at the same time holding that QE … caused the currency to devalue.

27. June 2015 at 06:21

Scott, Adair said reserve requirements could be used curtail excessive credit growth – why is that wrong? It has nothing to do with raising revenue. This paper finds a strong link between reserve requirements and loan growth: http://eaf.ku.edu.tr/sites/eaf.ku.edu.tr/files/erf_wp_1416.pdf

27. June 2015 at 08:54

Why 2012 to 2013 debt decrease so much?

1) The revenues increased from $2.45T to $2.77T which was a surprise with improving economy if memory is correct. (Some of which was a large surplus from Frannie in 2013.)

2) Expeditures dropped $3.54T to $3.45 which came falling recession tools (and yes I did support the Unemployment Insurance), less war spending and the sequestor.

I don’t remember any kind of major tax increase in 2013 that drove revenue total.

28. June 2015 at 06:42

Britonomist, Sure it can be used, but it’s not costless, as he implies. It’s a tax on banks.

Collin, There were two major tax boosts, income and payroll, so your memory is apparently not too good.

28. June 2015 at 11:42

Scott, forgive me if I’ve completely missed your point, but are you saying essentially that Adair is wrong to imply it is monetization because the reserve requirements are effectively a tax which is being used to pay down the debt in this scenario?

1. July 2015 at 06:37

Britonomist:

Not sure if you are still there, but no need to resort to accusations of sophistry. We can just disagree, robustly or otherwise.

When I said “devalue money” I meant against goods and services, not against another currency. Apologies if I wasn’t clear. The tanking currency is another matter, a good sign of monetary easing but not necessarily the devaluation of money itself, that comes later hopefully.

And I can say something caused something else without a plausible counterfactual. People do all the time. However, Keynesians say deficits are good, the bigger the better, it seems. Japan did poorly with a big and growing deficit. It might have done worse without, but no one is arguing that line.