Kevin Erdmann on LFPR

Here’s Kevin Erdmann (aka kebko):

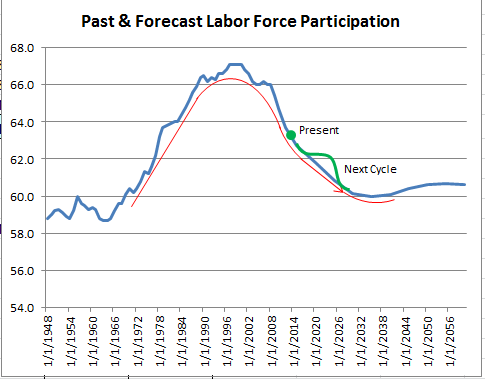

Here is the forecast, appended to actual past LFP rates (in blue):

..................The most important thing to note here is that the current slope of the line basically tracks the slope we have seen since 2000. You don’t need a disillusioned labor force that’s given up in order to explain this decline.

There are periods in the late 70’s, late 80’s, late 90’s, and mid-oughts, where LFP goes above trend during especially strong labor markets. The sharp curvature of the curve makes it hard to see these, but once we correct for this trend, there is nothing special about LFP behavior.

One mistake I see a lot of people making is that they compare the current LFP rate to the rate at the peak of 2007, so they are capturing all of the cyclical variation plus 6 years of a very sharp secular decline. Because the secular decline started in the late 90’s, conventional wisdom also attributes the secular trend in the labor market of the 2002-2007 recovery to a weak recovery. In truth, the LFP in 2007 was well above trend, and a very strong labor market was masked by demographics. So the demographic factors here tend to be dismissed as a result of placing errors on top of errors in our analysis.

I don’t have strong views on this subject, but his analysis seems plausible to me.

This also reminded me that it can be misleading to compare “depressions” in tiny countries with depressions in huge countries. A tiny country like Latvia can produce at a level much further above it’s natural rate than a very large economy like the US. Thus a 25% drop in RGDP from the peak might lead to a milder depression in Latvia than in the US.

PS. The labor market is still in bad shape. But if it was in as horrendous shape as the employment numbers suggest, then I very much doubt Obama would have easily been re-elected. The 7.4% unemployment rate captures the current situation pretty well. And that’s still a bad economy.

Tags:

16. August 2013 at 23:15

Correct my confusion.

The claim is that there has been no structural change in the LFPR since 2000 and this cause people to reject Romney?

Seriously, this is good stuff.

However, the truth be told there are large cyclical factors behind the LFRP, and this is supported by the literature; The Fed, EPI, Macroeconomic Advisors.

Obama was re-elected since Republicans have strayed too far to the right. They need to re-embrace their Eisenhower roots, not this libertarian, gold-buggery nonsense.

I am calling Poe’s Law on this. I dunno if this is joke or sincerity.

17. August 2013 at 00:12

I don’t buy this one, at least all of it. Sure, an older society will have more retirees. I get that. And lower LFP rates, in general.

But LFP dropped 5 percent in 2008, very quickly, and never recovered. Anybody who looked for work 2008-present knows why. The job market is pathetic.

I think a lot of people quit looking for work post-2008, especially if they could get SSDI, or claim VA post traumatic stress syndrome disability (something like a third of returning vets are signing up for this form of disability), or could do some under-the-table cash-work until they hit 65.

Human societies are mutable. If there was a robust job market, seniors would postpone retirement, moms (and housedads) would go to work, the claims for SSDI would fall. We could use some boom-times, of the type central bankers have a squeamish aversion to.

Employers who post jobs are swamped, even yet. I have not heard of any employers who are struggling to fill positions, excepting perhaps certain slots in North Dakota, or highly skilled specialities.

Employers who claim trouble finding employees usually have a problem with laws of supply and demand—that is, agriculture businesses who need illegals to work for the wages they offer. I am sure ag businesses that paid $15 an hour would be full up. (BTW, why is it there is still plenty of illegal labor on our farms? Is Homeland Security/Border Patrol a giant joke?)

There is the Obamacare angle, and the move by employees to hire only part-timers.

Mostly, people cannot get jobs and that is why LFP rates are way down.

17. August 2013 at 03:06

Antiderivative:

“Obama was re-elected since Republicans have strayed too far to the right. They need to re-embrace their Eisenhower roots, not this libertarian, gold-buggery nonsense.”

It’s always amusing to me when libertarians and free market money advocates are blamed for either the state of the economy, or believed to be the underlying force within the establishment GOP.

It’s also amusing to internet posters attempt to trash the non-aggression principle (oh the horror!) and free market money (oh no, letting the market process, not guns, decide what the money will be?!).

Obama was re-elected not because the establishment GOP strayed away from neoconservatism, and into libertarianism and free market money – which it didn’t by the way – but because of many factors totally different from the hilarious one you proposed, among which include a still lingering discontent with how the economy ended up once the GOP’s two term control ended.

The reason you believe it’s because of libertarianism and free market money is because of how intellectually influential the ideas of ONE Congressman in the GOP has been. It’s because those ideas resonate with you, and you don’t like it.

The establishment GOP is still very much pro-imperialism, pro-police state, and pro-theocracy. Same with the Democrats, by the way.

The population believed Obama was going to be an alternative, not a continuation.

17. August 2013 at 03:11

Benjamin:

If there is a secular decline in the Labor Force Participation Rate, then the substantial secular decline for 5 years is showing up. It is possible that the discouraged workers from 2009 caused the sharp drop. But as labor market conditions have improved, many of those folks returned to the labor market and are now employed. Other people, however, retired as they would have anyway.

Of course, it could have been people that would have retired or claimed disability that did so “early” due to the bad labor market in 2008-2009.

There are actually numbers for discouraged workers. It is 988 thousand. If you add those to the unemployed, it adds less than 1 percent, bringing it up to 8%.

17. August 2013 at 03:11

Forgot to mention: The establishment GOP is also pro-Fed. That’s one reason why they try to ostracize Republicans who want people to be able to choose to opt out of the central banking system while upholding their property rights.

Oh, and if you believe libertarianism is “nonsense”, then that means you initiate violence against other individuals and/or their property, and you cannot comprehend or understand what it means to deal with others peacefully. I guess that means if someone were to come over to your house, and initiate coercion against you, and/or take your belongings against your will, that you would just let them do it, since, you know, that would not be “nonsense.”

17. August 2013 at 04:15

Amity Shlaes, are you KIDDING ME???

“Diana West masterfully reminds us of what history is for: to suggest action for the present. She paints for us the broad picture of our own long record of failing to recognize bullies and villains. She shows how American denial today reflects a pattern that held strongly in the period of the Soviet Union. She is the Michelangelo of Denial.”

http://delong.typepad.com/sdj/2013/08/the-american-right-has-long-thought-in-its-secret-heart-that-roosevelt-was-a-communist-eisenhower-too.html

17. August 2013 at 05:27

Let’s say there is no minimum wage law and no UI, would there still be structural unemployment? And if yes, what are the main causes?

I never understood why -apart from demand side problems- people ready to work at market prices shouldn’t find a job? Isn’t most of so called structural unemployment voluntary? More like frictional unemployment?

17. August 2013 at 05:44

Ben, I think he addressed that point. The trend has fallen gradually but the actual rate falls in a sort of staircase of sharp breaks, due to the business cycle.

And 7.4% is still recession level unemployment–far worse than the worst month of the previous recession. So I wouldn’t expect lots of worker shortages.

17. August 2013 at 05:45

libertaer, I agree that those are the main causes of structural unemployment.

17. August 2013 at 07:07

Could someone please help me in the comments section here?

http://unlearningeconomics.wordpress.com/2013/08/17/market-monetarism-jumps-the-shark

The author is asking for examples where, after interest rates fell to 0%, aggressive monetary policy successfully cured the situation.

17. August 2013 at 08:30

TravisV,

Sounds like you’ve got into a bad position: if there are no examples of interest rates falling to 0% (and there aren’t) then logically there can be no examples of interest rates falling to 0% and aggressive monetary policy curing the situation.

17. August 2013 at 08:33

W. Peden,

Seems to me that Japan has been a good example of 0% interest rates……

17. August 2013 at 08:38

TravisV,

Perhaps (it depends on how you define it) but then one would be inferring from a sample of one. Japan is as good an argument against the efficacy of fiscal stimulus as it is an example of the efficacy of monetary stimulus; the difference is that recent experience suggests that monetary stimulus is effective in ZLB situation when the target is set right.

17. August 2013 at 08:47

W. Peden,

Right, the central bank needs to have the understanding that a different target is needed and the willpower to print enough to hit that target.

I suppose the specific interest rate we should be talking about is the Fed Funds rate and the equivalent in other countries. Isn’t the Fed Funds rate practically zero right now?

Also, was there a Fed Funds rate during the 1930’s? If not, what is the basis for Sumner & Co.’s claim that the U.S. fell into the ZLB during the 1930’s?

17. August 2013 at 09:06

TravisV,

For inter-country comparisons, you’d be better off looking at short-term treasury bills.

“Practically zero” and “zero” are different numbers.

T-bill secondary rates in 1933-1934 were about as low as they are now, i.e. “practically zero”.

17. August 2013 at 09:12

The target interest rate in Japan used to be exactly zero. I forget what it is now, but still very close to zero.

BTW, Sweden never had a negative target rate, only a meaningless corridor rate was negative.

17. August 2013 at 09:22

You already gave ‘Unlearning econ’–who happens to be an old foil of mine–the best example; FDR’s taking the country off the gold standard in 1933.

Rob (we’re on a first name basis) responded entirely in character; that that didn’t count because long term bonds weren’t at zero. But look at short term rates in figure #5 here;

http://research.stlouisfed.org/publications/review/92/03/Depression_Mar_Apr1992.pdf

They are near zero.

And don’t ever expect Unlearning Econ (who has never learned much, in the first place) to play honestly.

17. August 2013 at 09:36

‘Amity Shlaes, are you KIDDING ME???’

I’d say it’s DeLong who is kidding you (and he knows better, because I’ve pointed out to him, more than once, that there is plenty of evidence to show just how badly American Communists withing the FDR Admin. influence our conduct of WWII and the early Cold War).

I haven’t read Diana West’s book, but it’s quite amazing that David Horowitz thought he could get away with bending to Ronald Radosh’s fit of pique–replacing a favorable review with Radosh’s entirely obfuscatory one)–since Radosh got clobbered by Stan Evans back in 2008 for exactly the same thing;

http://www.anncoulter.com/columns/2008-01-01.html

17. August 2013 at 10:10

Travis (et al.),

By insisting that 10 year bond rates be near zero Unlearningecon is effectively redefining the liquidity trap.

Keynes’ original description of a liquidity trap refers to the existence of a horizontal demand curve for money at some *positive* level of interest rates. Given that there is no evidence of the existence of a liquidity trap for an interest rate greater than zero, in modern macroeconomics liquidity trap refers to a situation in which the nominal *short term* interest rate is near zero.

His completely novel definition of a liquidity trap, in which 10 year bonds must have a yield near zero does not even exist. The lowest annual average yield for government issued 10 year bonds on historical record was for Japan in 2012, and it was equal to 0.84%, and is in fact the only time it has ever been less than 1%. In fact no other country on earth has ever had a government issued 10 year bond close below 1.17%.

Thus Unlearningecon is asking you to go on a snipe hunt which was apparently his whole intention.

P.S. I left a reply there essentially saying this.

17. August 2013 at 10:25

Ditto, Mark Sadowski. Exactly right about the ‘snipe hunt’; that’s Unlearned’s M.O.

Now, back to the Ronald Radosh-Diana West dispute (Scott long ago told me not to bother apologizing for going off topic, so I won’t here either); West has begun to counterattack (ala Stanton Evans) and it’s pretty amusing;

http://gatesofvienna.net/2013/08/diana-west-on-the-question-of-scholarship/

———quote——-

For example, Radosh writes: “Instead of weighing these fears, West turns to another anecdote telling how George Elsey found confidential files in the Map Room that showed FDR naively thinking he could trust Stalin, and instructed Hopkins to tell Soviet Foreign Minister Molotov that FDR was in favor of a Second Front in 1942.”

There’s one problem with Radosh’s scholarship here. This anecdote about George Elsey, confidential files and the Map Room isn’t in my book. Anywhere. ….Radosh wrote a retort headlined: “Diana West’s Attempt to Respond.” ….

In his retort, Radosh writes: “Maybe she couldn’t find the anecdote. But it is there in three different places where she writes how FDR told Hopkins to go into Molotov’s bedroom while he was staying in the White House so that he could meet with the President, and at that meeting, Hopkins told Molotov that FDR was in favor of a Second Front.”

Now we have another problem. The brand new anecdote isn’t in my book, either.

It gets worse.

———–endquote————

Oh yes, it does. As Radosh’s story is bunk; it wasn’t FDR telling Harry Hopkins to tell Molotov…. It was Hopkins, on his own volition, coaching Molotov on how to approach FDR, the next day, on how to get his sympathy for more aid to Stalin. Radosh is amazing.

17. August 2013 at 10:29

Mark Sadowski,

Good point. Even Paul Krugman’s redefinition of the liquidity trap only referred to short-term rates of interest hitting the ZLB.

17. August 2013 at 11:20

Mark Sadowski,

Thanks for your help! Greatly appreciated.

17. August 2013 at 12:58

Travis, The real question is whether monetary stimulus has ever failed at the zero bound. And of course the answer is no.

In 1933 monetary stimulus succeeded in boosting NGDP sharply.

17. August 2013 at 17:28

Bill Woolsy: Hello and I enjoyed your comment.

My point is cultures are mutable.

Someone predicting LFPR in 1970 would have projected way low—-women entered the force.

18. August 2013 at 05:26

Very interesting analysis. It does sound pretty convincing…but you need more data. You need to break down the 25-55 age group into smaller age groups and also on immigrant and racial lines to really look at the demographic trends. Just more evidence in my mind on how you can use the selective use of statistics to prove just about anything. But what would most economists do with themselves if this was not the case? Krugman graphs showing the correlation between marginal tax rates and growth rates are the ultimate in this regard…as if nothing else happened between the 50’s and now…

23. August 2013 at 07:38

While I’m sympathetic to the general idea here, I have trouble believing the actual curve I’m looking at. That curve suggests that the underlying demographics of the baby boom were responsible for 80% of the participation bump centered in the 1990s, and that the rising level of women in the workforce only represented about 20%?

Also the curve suggests that the level of participation just after the crash is *normal* rather than significantly below trend. If participation is usually well above trend in a boom, then we could presume that after the worst crash in 70+ years, it would be quite a bit below trend.

Are the demographics really so extreme that with almost no horizontal movement in the curve, we be considered back to trend already in LFP?

I doubt it.

27. August 2013 at 23:17

Michael, I think I can answer your doubts.

On the women vs. baby boomers question, your intuition is correct. But, you have to remember that separate from the boomer issue, LFP for all the prime working ages is declining by about a percent a decade. For men, this has been a trend for decades, and women’s participation peaked in the 90’s and is now following a similar trend. That kind of tilts the entire graph downward. Without that trend across age groups, LFP would be a little higher now, and would settle in at 64 or 65 in the future, and then the evident proportion of the effects of women vs. boomers would reflect more obviously what your intuition is telling you.

On the trend line, I set the trend line at the bottom of the cycle, so we are near the trend you would expect at the bottom. If you set the trend at some average level, we would probably be below it, but less than 1% below it, and the long term trend is steep enough downward that, at best, we will go horizontal for a while, like in the 2000s. To figure out where the trend line would be at that precision, you would really have to get down to intra-age group details, which I didn’t do.

But, that’s the point I’m making. Reasonable arguments about how far off LFP is from a normalized trend would amount to disagreements of some tenths of a percent. We are not suddenly 3% off of a normal LFP level because of the business cycle.