Japan prediction from 2011, revisited

Back in 2011 most experts claimed there was nothing the Japanese could do to boost NGDP. It was believed they were stuck in a liquidity trap. Then in 2012 candidate Abe announced that he would implement a more expansionary monetary policy, including a 2% inflation target. I suggested the policy would help, although they’d fall short of 2% inflation. Mark Sadowski has a post showing the path of inflation. (When Abenomics was announced in November 2012 the Nikkei was around 8700 and the yen at less than 80 to the dollar.)

Mark also generously quoted from a 2011 post of mine that I’d forgotten about.

Just to be clear, it is quite possible (likely in my view) that Japan could get another 2% of RGDP by switching to a 3% NGDP target. But it would be a one-time gain, as their labor market got less rigid. Unemployment might fall to 2% or 3%, but trend growth shouldn’t change.

In fact, RGDP growth was 2.4% in the first year of Abenomics, and has been roughly zero since. Recall that zero is the new trend growth for Japan, due to their rapidly falling working age population. Yes, I was a bit lucky, but as Napoleon once said “give me lucky generals.” (or something vaguely like that, probably in French, not English.)

Marcus Nunes has a new post that quotes from the recent FOMC meeting:

There was push back against hesitating. A number of officials argued that a rate increase could convey confidence to the world about the economic outlook and that the Fed needed to move in acknowledgment of the progress the economy had already made toward normalcy.

Yes, tighter money from the Fed is just what global markets are looking for right now, to regain confidence.

You can’t make this stuff up. While traveling I saw a story that the new President of the Dallas Fed is going to be a management professor.

PS. I have a new post at Econlog.

Tags:

20. August 2015 at 09:03

That Mark Sadowski post is really good. Also, I’d say Japan’s trend rate of growth is just under half a percent per year, Germany’s is almost the same, and Italy’s is truly 0%:

http://research.stlouisfed.org/fred2/graph/?g=1E2Y

20. August 2015 at 09:25

Good posts by you and Mark. Good call. Impressive. Most impressive.

20. August 2015 at 10:44

@scott

A few questions for you to clarify your views.

1. In your quote above you’re suggesting that a higher NGDP target would cause a reduction in the rigidity of the labor market? If so how?

2. I assume that you believe higher M resulted in increased NGDP. From a producer’s perspective (who can buy inputs at today’s prices) why would higher expected nominal spending not result in higher real production?

I have a slightly different take on these which I’ll share, after you have responded.

20. August 2015 at 11:30

dtoh,

1. Perhaps some wages were stuck above equilibrium–the rise in NGDP reduced them to equilibrium.

2. No, I do expect some impact on RGDP from higher NGDP, I said about 2% in that quote.

20. August 2015 at 11:31

E. Harding, I believe the trend rate in Italy and Germany is higher than in Japan. That graph shows actual RGDP, not trend.

20. August 2015 at 11:31

Hi Scott,

The graph doesn’t account for the VAT increase in April 2014 … I recall you saying:

“Japan will be hit by an adverse supply shock next year (higher sales tax rates) which will boost inflation-making it look like they will hit their 2% target. Don’t be fooled.”

It’s much less dramatic if you remove the (clearly visible) VAT jumps:

http://informationtransfereconomics.blogspot.com/2015/08/dont-forget-vat.html

20. August 2015 at 11:36

Jason, Yes, but even without the tax increase, there was a rise in inflation. The fall in the yen from 76 to 125 obviously boosted prices.

Fiscal policy has of course been contractionary, so the Keynesian model would predict higher unemployment.

20. August 2015 at 11:41

@ssumner

No, it shows actual RGDP, adjusted for unemployment, which is a good approximation of trend RGDP. Look closely. Actual RGDP in Italy has done much, much worse. My previous statement stands.

20. August 2015 at 12:14

Hi Scott, you said:

“Fiscal policy has of course been contractionary … ”

Has it?

https://research.stlouisfed.org/fred2/graph/?g=1Fd7

Government spending as a fraction of GDP has been growing since 2008. And net borrowing has increased since then as well …

https://research.stlouisfed.org/fred2/series/GGNLBAJPA188N

Is there some measure showing Japan’s fiscal policy contractionary? Raising the VAT would be contractionary, but that isn’t the only thing that’s happened.

20. August 2015 at 13:56

Jason

What do you think a rise in VAT is? Expansionary?

20. August 2015 at 14:26

Jason,

Your two claims totally contradict each other.

You can’t claim that the consumption tax increase was big enough to be the predominant cause the increase in inflation and yet at the same time claim that it was too small to have a contractionary effect.

To put this into perspective, according to the Japan Statistical Yearbook:

http://www.stat.go.jp/english/data/nenkan/index.htm

Consumption tax revenue in FY 2013 (which ran from April 1, 2013 to March 31, 2014) was 10.65 trillion yen. NGDP was 482.7 trillion yen in FY 2013 according to the Japan Cabinet Office. Thus consumption tax revenue was 2.2% of GDP in FY 2013 when the consumption tax was 5%. Thus the increase in the consumption tax to 8% very likely raised consumption tax revenue to 3.5% of GDP or an increase of about 1.4% of GDP.

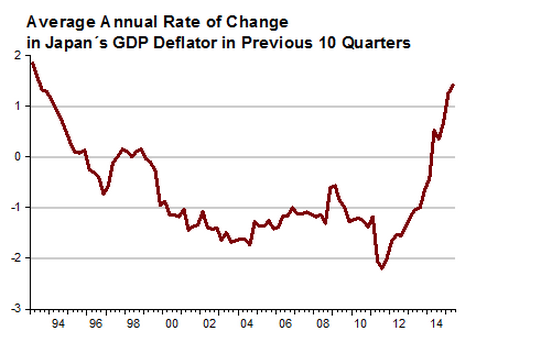

Let’s assume that *100%* of the increase in revenue passed through to an increase in the price level. The average rate of change in the GDP deflator in the 10 quarters through 2012Q4 is (-1.4%). The average rate of change in the GDP deflator in the 10 quarters through 2015Q1 is +1.4%. The change in average inflation is thus 2.8 points of which the most that the consumption tax increase could have contributed over that 10 quarter period is about 0.56 points.

In short, the consumption tax increase’s contribution to the increase in average GDP deflator inflation over the past 10 quarters represents no more than one fifth of the total.

(continued)

20. August 2015 at 14:53

(continued)

A hike in consumption tax revenue equal to 1.4% of GDP very likely was contractionary, unless spending was also increased, which it so happens it was. But how large was the spending increase, and since the output gap very likely has grown smaller with declining unemployment, shouldn’t we take into account the business cycle?

The simplest way to check this is to consult Krugman’s favorite reference on these matters, which is the CAPB found in the IMF Fiscal Monitor.

http://www.imf.org/external/pubs/ft/fm/2015/01/pdf/fm1501.pdf

According to Table A4 on page 79 Japan’s general government Cylically Adjusted Primary Balance CAPB decreased from (-6.9%) of potential GDP in calender year 2012 to (-7.5%) of GDP in 2013. This decrease in the CAPB of 0.6% of GDP refelcts the fiscal stimulus and was before the increase in the consumption tax in April 2014.

But the CAPB rose to (-6.6%) of GDP in 2014 and is projected to rise to (-5.4%) of GDP in 2015. The CAPB is projected to increase by 1.5% of GDP between 2012 and 2015. So evidently the discretionary increase in taxes has exceeded the discretionary increase in spending.

In short, Abenomics has on average been fiscally contractionary.

20. August 2015 at 14:56

@scott,

I would offer a slight different take on things. I’m speculating a little here so I’d be interested in your view.

1. In general at low rates of NGDP, I think it’s hard to get much of a sustained delta between NGDP and RGDP. Producers can just arbitrage by buying input at today’s prices and selling output at tomorrow’s inflated price. Until you start having supply constraints you won’t get much delta between RGDP and NGDP. (And yes, I’m ignoring hysteresis.)

2. It may be a little premature to make judgements about Japanese inflation. There were a few things going on including: a) increase in the consumption tax, b) pretty effective jawboning to get large corporations to raise wages, and c) higher import prices.

3) Japan is probably picking up a few tenths of a percent of growth on the tourism boom.

4) IMHO the efficacy of Japanese monetary policy gets dulled/delayed a bit because a lot of the new money goes into foreign assets. This pushes the yen down and I’m not sure the pickup in exports generates the same or as an immediate effect that the economy would get from direct domestic spending/investment.

20. August 2015 at 15:01

Correction: the increase in consumption tax revenue is likely closer to 1.3% of GDP.

20. August 2015 at 17:38

Note that “dtoh”, who is friendly to Sumner, senses something amiss but just can’t quite put their finger on it. I will be more explicit: Sumner said in his 2011 piece that Japan would get a “one-time” pop by “switching to a 3% NGDP target”, NOT by ‘more expansionary monetary policy, including a 2% inflation target’ as Sumner now claims. Targeting inflation is NOT the same as targeting NGDP. Central banks all over the world target inflation, but, agrees Sumner, they don’t yet target NGDP. So why does Sumner not make this distinction? Possibly he is trying to characterize the initial modest success of Abenomics to ‘targeting NGDP’ rather than inflation, but Sumner lacks the data to say whether JP targeted NGDP or inflation, so he rightly errs on the side of caution by now calling it merely ‘expansionary’ and ‘targeting inflation’. Typical Sumner misdirection and doublespeak.

BTW, a supposed star, along with Australia, in ‘targeting NGDP’ was Israel in the last Great Recession. But today it’s announced that ‘Israel’s economic growth slowing dramatically in 2015’, which suggests: (1) the long run is here, and (2) targeting NGDP–if that’s what Israel’s central bank does–only works ‘one-time’, as in 2008, and doesn’t work now. On this last point at least the Keynesians claim their policies work all the time, not just ‘one-time’.

Shorter Ray: NGDPLT = Sumner = fraud.

20. August 2015 at 18:53

Well, I suppose I’m a hopeless trend growth optimist, but I suspect they could eke out more growth at 4% NGDPLT. People often don’t realize Japan is only about as productive as Italy on a per-capita basis despite some really compelling institutional advantages. As it stands, looks like South Korea will overtake them soon.

20. August 2015 at 20:00

I don’t think Japan can eke any more growth out, judging from the Sadowski post.

As for Korea:

http://research.stlouisfed.org/fred2/graph/?g=1EVC

I’m not saying convergence is over; I am saying it’s almost over.

20. August 2015 at 20:01

Again, peak RGDP/person relative to the U.S. is defined as 1.0000.

20. August 2015 at 20:05

RGDP per worker, not per person.

20. August 2015 at 22:10

Ray,

I think Scott is correct in principle, but what he predicted (and I’m extrapolating) was both obvious and trivial, i.e that: a) an expansionary monetary policy (be it with and NGDP target or an inflation target) will get you a temporary bump up in real growth as you move back to trend, b) once you get to full employment (i.e to trend), real growth is going to drop back down, c) at trend, you’re not going to get much more increase in real growth (without structural reforms), and d) any further increase in the NGDP growth rate will be mostly price not volume.

Where I disagree is that a) I don’t think Japan is anywhere near full employment (even without structural reforms) and b) I think that the inflation being seen in Japan may not be a result of Japan getting back to trend (i.e. full employment) but rather that there is some other funky stuff going on.

21. August 2015 at 03:03

What is so interesting about the Fed is that they are actually exceeding their SEP estimates at the moment. In Q2, real GDP will be revised up to almost 3.5% from an initial estimate of 2.3%. What we know about Q3 is positive, helped by consumer spending and residential investment. The unemployment rate is at their Q4 estimate two quarters ahead of schedule. Core inflation has been surprising to the upside this year. The data is pushing them closer to a rate hike while the financial markets are pushing them further away. There may be a misreading of the Fed’s intentions here.

21. August 2015 at 04:03

The only way Japan can see a consistently positive RGDP is to be a leader of industries like in the 70s, 80s and 90s.

Today, Japan’s economy is functioning because of its ultra-low interest rate, which needs to be lower every year, as its debt grows.

Secondly, if Japanese industries lose its competitiveness, profits will fall, causing exports to drop and imports to rise as the Japanese value ‘superior’ goods. Both these events will cause the Japanese Yen to weaken further to gain competitive advantage through devaluation.

21. August 2015 at 06:22

How should countries determine what is the optimal Ngdp/inflation growth for them?

21. August 2015 at 06:57

E Harding– Well, Mark’s post is aptly titled in that respect: a monetary policy that isn’t implemented can’t do much — Japan did not implement 3% NGDPLT, did not hit 3% NGDP growth for even a single year, and no one currently expects BOJ to hit 3-4% over the medium or long term. Japan only implemented a policy that ephemerally resembles NGDPLT, so I’m not surprised the gains are thus far ephemeral.

I suspect most people (even MM) are underestimating the cumulative effects of recursive changes in expectations that will occur once markets fully absorb a credible policy of NGDPLT, similar to the way few probably foresaw in 1979 that Volcker’s regime would eventually lead to the Fed missing a 2% inflation target every year.

Also, I think the graph you want is something like this:

https://research.stlouisfed.org/fred2/graph/?g=1EVC

This trend must be a bit shocking to older Japanese — it’s as though Mexico approached parity with the United States over just 20 years.

Obviously a lot of other factors come into play but just for fun I wanted to plot nominal GDP per capita for S Korea and Japan starting with 1985 set equal, but it wasn’t readily available at FRED or WB. Oh well 🙂

21. August 2015 at 07:04

Boo, FRED dropped off the second series.

21. August 2015 at 08:06

“I think Scott is correct in principle, but what he predicted (and I’m extrapolating) was both obvious and trivial”

I agree. It’s what basic macroeconomics would tell you would happen. The problem is that basic macroeconomics isn’t used enough in analyses of macroeconomic phenomena, because housing bubble macroprudential Lehmans CPI doesn’t include food or energy.

21. August 2015 at 08:38

Jason, It’s considered contractionary by Keynesians. Obviously those terms are subjective.

And I was talking about the last couple years, not the period around 2008.

dtoh, You said:

“In general at low rates of NGDP, I think it’s hard to get much of a sustained delta between NGDP and RGDP.”

I’m not sure what you mean. Are you talking about short run non-neutrality? Long run non-neutrality?

Ray, It’s amusing to see you struggle to understand the concept of money neutrality.

Talldave, Monetary policy only affects growth in the short run, and I believe Japan is closer to France than Italy.

E. Harding, I’m not talking about RGDP per worker.

Pras, It’s a very complex question, but 3% to 4% growth in per capita NGDP would work in most cases.

21. August 2015 at 08:47

Not sure I can believe NGDPLT and 5% deflation would produce the same growth in the long run. Suspect superneutrality applies most reliably over 2% and below hyperinflation.

Depends whose numbers we look at, but on average Japan seems to be about halfway between France and Italy. Interestingly, CIA has South Korea ahead of Italy already.

https://en.wikipedia.org/wiki/List_of_countries_by_GDP_(PPP)_per_capita

21. August 2015 at 08:59

Sumner: “Ray, It’s amusing to see you struggle to understand the concept of money neutrality.” – what? I’m not even talking about money neutrality in this post, I’m talking about your statements about NGDPLT vis-a-vis Japan.

@dtoh – thanks. When you say ‘trend’ you must mean some simple line plotting along the lines of ‘output gap’ and “potential GDP”. I think this construct however is fiction. And as you may know, the Solow model for growth has but one one component long term, steady state: technology growth, exogenous to the model. If Tyler Cowen, Gordon, and others are right about a “Great Stagnation”, it means that the ‘natural rate’ an economy expands at present is in fact very low, according to the Solow model.

21. August 2015 at 10:18

@ssumner

It’s not RGDP per worker, it’s RGDP adjusted for unemployment (with Q1 2009 set as 1.026 for the three countries). I only mentioned RGDP per worker in relation to Korea, not Italy, Germany, and Japan.

21. August 2015 at 11:42

E. Harding,

What period are you using to establish the trend?

From 2007, there seems to be a 0% trend for both Germany and Japan, and a slight negative trend for Italy.

21. August 2015 at 13:23

Scott:

I am struggling to reconcile this statement “monetary policy only affects growth in the short run” with this statement “the NGDP problem is both easy to fix and a big part of what’s hurting the world economy…Monetary policy is our only hope” (http://www.themoneyillusion.com/?p=14448).

Should I read the latter statement as “Monetary policy is our only hope for short run growth, but long run growth depends on structural factors.”

And, if you do screw up short term growth due to bad monetary policy, don’t you run the risk of creating structural problems as institutions adapt (and mal-adapt) to handle the short run growth crisis?

21. August 2015 at 17:19

The increased inflation from Abenomics only harmed economic coordination and contributed to reduced productivity.

21. August 2015 at 17:31

@Justin D

I’m using the period 2010-today.

22. August 2015 at 06:59

Regarding that FOMC quote:

The Fed “conveying confidence” will always engender the opposite response from the market, as the market understands that Fed Confidence = tighter money.

As long as the Fed is accurately assessing the economic climate, this counterbalance is a good thing. The situation will quickly get unstable if the Fed sees the economy slipping back into recession and thinks, “Quick! Signal more confidence!”

The market only wants the Fed to recognize the current economic reality. It’s not waiting around for the Fed to “inform” it what the economic reality is.

23. August 2015 at 04:54

Talldave, The Economist has France at 40k, Japan at 39k, and italy at 35k. That seems more plausible to me.

Ray, Ah, but you only think you are not talking about money neutrality.

E. Harding, Yes, but there are lots of issues you need to address when estimating trend rates. For instance, Japan trend growth has slowed sharply over the past decade, so if you simply use a decade average, you miss that slowdown.

Carl, You said:

“Should I read the latter statement as “Monetary policy is our only hope for short run growth, but long run growth depends on structural factors.”

And, if you do screw up short term growth due to bad monetary policy, don’t you run the risk of creating structural problems as institutions adapt (and mal-adapt) to handle the short run growth crisis?”

Yes to both statements.

jj, That’s right.

24. August 2015 at 18:47

Thanks, I didn’t realize The Economist published their own GDP PPP data. Perhaps the most interesting aspect of the numbers is how much they vary!