Japan continues to add jobs at an astounding rate, as unemployment falls to the lowest level in decades

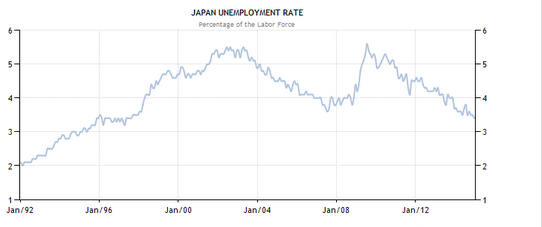

That’s right, the Japanese “recession” grinds on. A few months ago bloggers on the left and right, as well as the mainstream news media, reported that Japan had fallen into a “recession.” Only TheMoneyIllusion pointed out that this was nonsense, as analysts were confused by Japan’s falling population. Japan’s trend rate of RGDP growth is currently no higher than zero, and the post-sales tax increase RGDP slump was completely expected. The Japanese stock market was not fazed, Japanese companies continue to add workers at a rapid rate, and unemployment just fell to 3.4%, the lowest rate since the 1990s.

Japan’s seasonally adjusted unemployment declined to 3.4 percent in December compared to 3.7 percent reported in the same month of 2013 as the number of employed rose 0.6 percent and the number of unemployed decreased 6.7 percent.

The number of employed persons in December 2014 was 63.57 million, an increase of 380 thousand or 0.6% from the previous year.

The number of unemployed persons in December 2014 was 2.1 million, a decrease of 150 thousand or 6.7% from the previous year.

The jobs-to-applicants ratio increased to 1.15 from 1.12 in the previous month, the highest since March of 1992.

The number of new job offers rose 4.7 percent in December from previous month and rose 5.6 percent from the same period a year ago.

To the uninformed, the 0.6% rise in Japanese employment might seem unimpressive. But the Japanese working age population is falling by 1.5% per year, so this is equivalent to 2.1% employment growth in a stable population country, or 2.4% employment growth in a country with 0.3% growth in the working age population (such as the US.) Of course our employment only rose by about 2% last year, and yet that was the strongest performance since the late 1990s. In other words, the Japanese labor market is even hotter than the US labor market in a cyclical sense. All the claims to the contrary are written by people ignorant of Japanese demographics.

Abenomics has done the two things that it was capable of doing (reducing unemployment and slightly easing the public debt problem) and failed to do the thing many hoped for, but was never realistic given the demographics (create rapid RGDP growth.)

The people that disagreed with me, claiming Japan really was in recession, told me that unemployment is a lagging indicator (it actually is not, at least not significantly.) OK you guys, go on record and tell me when the delayed rise in Japanese unemployment will occur. I want a specific date, or at least a specific year. Will it be 2015? If not, then when? How about 2016?

Off topic, there are times that I just want to give up. From today’s news:

LONDON/SYDNEY (Reuters) – European and Chinese factories slashed prices in January as production flatlined, heightening global deflation risks that point to another wave of central bank stimulus in the coming year.

While the pulse of activity was livelier in other parts of Asia – Japan, India and South Korea – they too shared a common condition of slowing inflation.

Central banks from Switzerland to Turkey via Canada and Singapore have already loosened monetary policy in the past few weeks.

Switzerland!?!?!?

Tags:

2. February 2015 at 14:01

I actually think Japan can see significant RGDP per capita growth, even with their demographics, if they execute the proper institutional reforms. Still, no denying that employment graph is impressive.

Haha, Switzerland.

2. February 2015 at 14:12

Of course, Switzerland did ease monetary policy slightly, after greatly tightening it.

2. February 2015 at 14:34

So Scott, I’d be very curious to hear your thoughts on the new Greek Finance Minister’s proposal to restructure its debt by offering bonds “indexed to nominal economic growth” http://www.ft.com/intl/cms/s/0/7af4252c-ab03-11e4-91d2-00144feab7de.html?siteedition=intl#axzz3Qd6607ZZ

Would that not be the first government-backed market in NGDP futures?

2. February 2015 at 14:48

Excellent blogging. Yen around 120 to US dollar instead of 80. The Nikkei 225 up 20% in last year.

I disagree with Scott Sumner in one regard. I believe the expansive Bank of Japan policy has also increased Japan real GDP and not just nominal GDP.

The BoJ just needs to pour it on. Japan wages still very soft—-indeed Japan officials are publicly chastising employers to raise wages.

I am surprised the BoJ does not move to also monetize taxes.

Japan has a lot of room to grow, as seen by soft wages. Labor is being created by demand. Higher wages will create even more supply.

2. February 2015 at 15:04

Interesting that Japanese UnN continued to fall after monetary policy was tightened in 2006.

2. February 2015 at 16:34

I feel like a lot of people (including Tyler Cowen) end up confusing the issue between “Is Abenomics the best policy option (or at least significantly better than what came before)?” and “Is Japan still going to be in trouble long term because of demographic factors etc.?”

I think it’s possible to say that Abenomics is a big improvement while still thinking that Japan has insoluble problems. It’s fundamentally a pessimistic believe, but not incoherent.

2. February 2015 at 17:10

If you want to get involved… more comments on MM from the increasingly misleadingly named “Noahpinion”: http://www.bloombergview.com/articles/2015-02-02/keynesians-market-monetarists-blog-for-economic-truth

2. February 2015 at 18:06

Talldave and Ben, Just to be clear, I do think the BOJ has succeeded in increasing RGDP by a little bit, it’s just that I believe Abenomics supporters expected too much. There’s not all that much slack in the Japanese labor market.

SG, Thanks, I’ll do a post.

Rajat, Good point. My view is that the BOJ tried to tighten in 2006, but only succeeded in doing so in 2008. The initial moves to tighten were not effective. All they did is prevent policy from loosening, until 2008, when the global Wicksellian equilibrium rate fell sharply.

John, I can’t speak for Tyler (his views on AD are often more nuanced than they might appear—as are mine!) But I do think many people make that mistake.

Thanks Saturos, I’ll take a look.

2. February 2015 at 18:11

Timothy, Yes, they cut the rate to negative 0.75%. But even the SNB admitted the net effect was tightening, and both the stock and forex markets certainly saw the net effect that way. But you are right that the authors were probably thinking of that rate cut.

I saw the article as part of the media’s obsession with the idea that low rates mean easy money.

2. February 2015 at 20:28

@Sumner who says: “There’s not all that much slack in the Japanese labor market.” –

But did Sumner look at the labor participation rate of women in JP? As William Pesek says, the JP woman participation rate is very low, and the ‘third arrow’ of Abenomics is to get them to work more. So perhaps it’s not NGDPLT at all. Further, note the downward trend in the unemployment rate started well before Dec 2012 when Abenomics commenced.

2. February 2015 at 20:53

It is good to see account taken of demographics in economic statements. If the fundamentals of a country change and no account is taken of that then there cannot be a proper comparing of apples with apples nor can there be suitable policy for the demographic change.

3. February 2015 at 04:38

I do think that Tyler’s views tend to be more subtle and nuanced than they appear. But I also think that, in some ways like Krugman, Tyler has a habit of appearing more inscrutable or inviting people to conflate certain issues thanks to cryptic or vague comments. It can be interesting as a technique to draw out the assumptions of others (similar to a Socratic method), but in the end when so many people assume you think something that you don’t, I find it a failure of communication.

3. February 2015 at 05:42

Egads, do I agree with Ray Lopez? Yes on Japan!

Japan could bring women into the labor force or raise the retirement age. They are using immigrants in certain industries already.

Wages in Japan do not suggest tight labor markets.

3. February 2015 at 09:06

Benjamin might be right on this. Japan might prove that printing and monetization (of debt, of public spending, of transfer payments) is the solution to the problem of the debt overhang.

Anyway, it has gotten old reading about how sick Japan supposedly is for the past 25 years when they have low unemployment, high standard of living, social order, peace with their neighbors.

3. February 2015 at 13:59

Ray and benjamin cole

Here is the difference between male and female employment rates for Japan and for the USA.

http://research.stlouisfed.org/fred2/graph/fredgraph.png?g=Zr3

In the USA, the spread has more or less plateaued since 1995 (with some variations during the recession).

In Japan, the spread has steadily decreased and is still decreasing (the rate was slowed down in the 1990s, but has accelerated after 2000).

The USA-Japan spread has decreased from nearly 30 percentage points to about 8 percentage points.

My conclusion: more women might be able to join the workforce in Japan, but not that much. 5 more years at the current pace will completely close the USA-Japan gap.

But I agree that there is probably still some slack. I would expect that full employment is around 2% in Japan. If they can manage the 0.5%/year NGDP growth they averaged since 2010, they should make it within two years or so.

If the BoJ puts the pedal to the metal and adds an extra 0.5%, they might get there within a year.

PS: Japan has averaged 0.5% NGDP growth, but the annualized quarterly standard deviation is 4.3%! That’s pretty noisy.

4. February 2015 at 13:46

Ray, You said:

“So perhaps it’s not NGDPLT at all.”

Yes Mr. 120, it’s a pretty good guess that a policy that was never tried does not explain the rise in Japanese employment.

LK, Thanks for the info.