In one way, all recessions are alike

What is the one common feature of all recessions? The answer is easy. During every single recession, the media is full of reports that this recession is utterly unlike anything in the past. I discussed this point in my book The Money Illusion, but I might as well have been spitting into the wind.

Here’s Bloomberg:

These are strange times, which means the last 30 years of data — maybe even the last 50 years — don’t offer much insight. The normal indicators may not tell us much of anything at all. Even the reliable inverted yield curve that’s supposed to predict recession may be less reliable after years of quantitative easing followed by quantitative tightening.

Perhaps there will be no inflection point when a recession hits. Maybe inflation falls and then we just recover. That’s not unprecedented, but we are entering this period from a different place than we’ve ever been before.

To me, the economic situation seems utterly normal. There was too much demand stimulus, NGDP rose too fast, inflation increased, and policymakers are finally beginning to contemplate steps that would bring inflation down. So what’s new?

In my book, I cited a Time magazine article from 1991 explaining how the recession at that time (which was utterly normal) was supposedly nothing like anything we’d seen before. Today, the article seems almost comical.

Much of the confusion comes from the fact that most journalists and economists are working with the wrong model. The business cycle is actually quite simple. Monetary policy drives NGDP and NGDP drives fluctuations in RGDP. And interest rates do not tell us anything useful about the stance of monetary policy. For that you need to look at NGDP and NGDP expectations.

If you think the Fed has been tightening monetary policy for a year, you might wonder why the economy keeps chugging along with rapid NGDP growth. But what makes you think the Fed’s been tightening monetary policy for the past year? Interest rates?

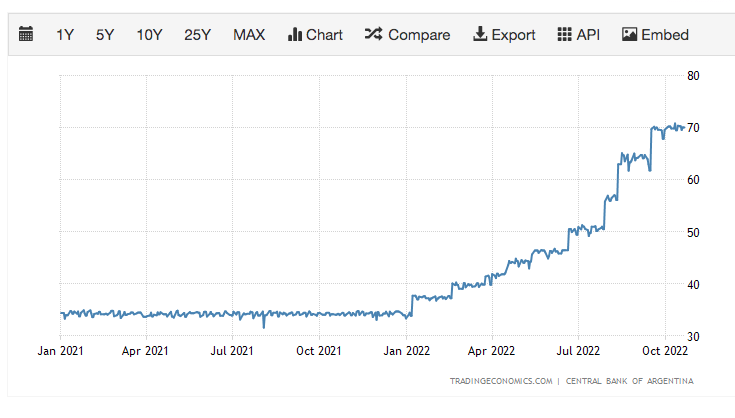

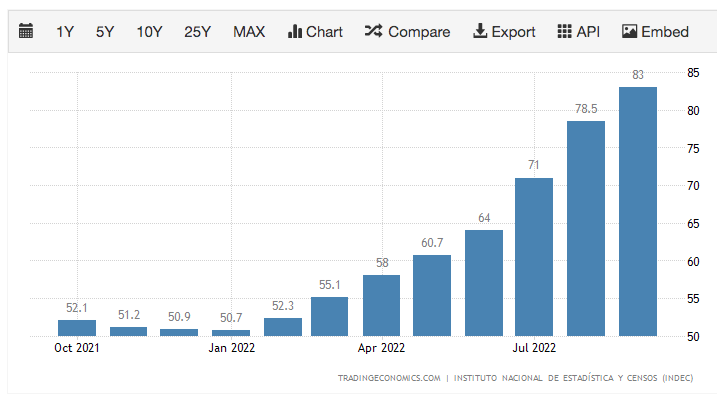

Here are interest rates in Argentina:

Wow, those sharply rising interest rates must be driving inflation much lower!

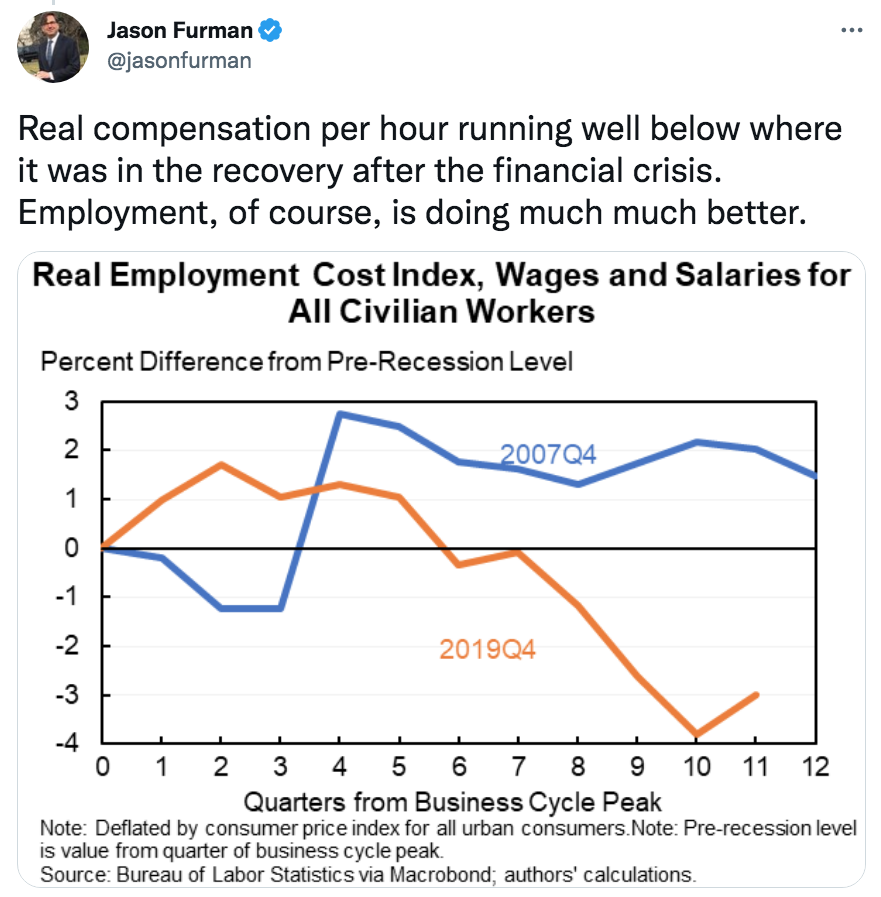

PS. Slightly off topic, but commenters used to be surprised when I told them that easy money wouldn’t improve real wages. The whole point of stimulus is to lower real wages so that firms hire more workers:

Tags:

28. October 2022 at 12:53

good to know that the supply crash had nothing to do with inflation ad that economics can fix thus

28. October 2022 at 13:03

This is one of Sumner’s best posts.

Short-term rates-of-change in money flows always contract during a recession. That is not presently the case. In fact, short-term flows are increasing while long-term flows are decreasing.

The July 1990–Mar 1991 recession was unique. It was the first time that bank debits roc became negative since the GD.

28. October 2022 at 13:57

If someone concluded that more fake news ‘moves’ the economy that is itself being ‘conditioned’ to align with the fake news logic (Social Credit Score CCP -> ESG/SEL America), that we speak like less fake news feels bad and more fake news feels good, and we begin to focus ‘here’ not ‘there’, where like drug addicts we demand a healthy steady not too much not too little keep it ‘here’ not ‘there’…

Does that really tell us anything true outside its own invocation of ‘trial/struggle’ as a particularly patterned narrative that everyone is supposed to trust or else the information pattern dialectic flow goes from ‘denial’ -> ‘smear’?

“Election denier” is being invoked from the same sources whose bodies and statements are “denying elections”.

Since when did anyone have to trust not just the inconsistent information as a description of a whole, but trust the people invoking the inconsistencies?

Accusers of treason engaging in treason?

Soviet style smearing of ballot box ‘watching’ from d’s narrative in information and physical form right now. Watchers watching the watchers and the watchers being watched are the same people accusing watchers of what the watchers are doing.

28. October 2022 at 14:42

wdw, Read this, you might learn something:

https://www.econlib.org/persistent-inflation-is-always-and-everywhere-a-monetary-phenomenon/

28. October 2022 at 15:50

its astonishing to me that the fed with 1400 phds on staff and a budget in excess of 500m is so wrong and sumner and his ilk are sure of as much? maybe both are wrong.

28. October 2022 at 16:05

If hours worked are up, and real gdp is up, doesn’t that mean that workers aren’t getting poorer, just working more hours, even if average hourly compensation is down?

28. October 2022 at 18:16

German fascism is finally and for the first real time being destroyed.

https://i.imgur.com/EOuQBBI.jpg

28. October 2022 at 18:29

Konnech’s lawyers in court ridiculed and mocked Catherine Englebrecht for describing her election integrity teams (who exposed Konnech as a front for the CCP) as ‘patriots’.

The corrupt judge wants Engelbrecht to reveal EVERY SINGLE PERSON who has seen the information. Not just the original 2 guys who called Gregg Phillips to look at it.

That is doxxing hundreds of people in open court. Some Anons would be on that list. They showed this info at the Pit back in August. What the judge calls a “CURE” could and would KILL people.

They asked about people’s families.

They asked about people’s friends.

They entered unverified pictures into the record of people they thought were guilty.

Patriots are exposing a crime syndicate and getting threatened for it in the court system.

We are truly up against evil.

28. October 2022 at 18:36

I know I’m in the right because I do not feel proud or gloaty when someone else gets censored.

Some people do feel proud, they are in the wrong.

28. October 2022 at 19:35

Lizard, Exactly.

George, You said:

“German fascism is finally and for the first real time being destroyed.”

Always suspected you had a soft spot for the Nazis

28. October 2022 at 23:06

“The whole point of stimulus is to lower real wages so that firms hire more workers”

This is probably how we should describe stimulus to counter perma-stimulus bias. Stimulus sounds too positive and contractionary policy too negative. Who could oppose stimulating the economy or support slowing the economy down other than old curmudgeons? “Running the economy hot” would sound a lot less appealing if people understood it to mean intentionally generating enough inflation to outpace wages. Similarly, limiting inflation to give wages a chance to catch up sounds a lot better than “contractionary policy” or, worse, “slowing the economy down”.

29. October 2022 at 04:12

Scott not sure if you saw but perhaps the most influential strategist on Wall St (Michael Hartnett) is now saying the Fed is highly likely to raise its inflation target to 3%. This is exactly how inflation expectations start to become unanchored and exactly why the Fed’s slow approach to tackling inflation is self-fulfilling. I fear our central bank needs a refresher course in economics.

Hartnett is not some random commentator. The biggest investors in the world pay close attention to his work.

29. October 2022 at 04:46

Site owner wrote:

“Always suspected you had a soft spot for the Nazis”

Says the supporter of Ukrainian neo-nazis, and the supporter of Hitler’s dream of an ‘EU’ ‘country’ with Germany as effective HQ. If Hitler were told there was an EU with Germany in control, he would have jumped for joy along with you, Herr Site Owner.

https://www.nbcnews.com/storyline/ukraine-crisis/german-tv-shows-nazi-symbols-helmets-ukraine-soldiers-n198961

https://www.newsweek.com/nato-says-it-didnt-notice-ukraine-soldiers-apparent-nazi-symbol-tweet-1686523

This ‘suspicion’ you insinuate is being observed from me, is in fact an invocation of your own internal dialectic, projected out, to cover your own ‘soft spot’ for communists (and fascists it seems), as nothing in my words or in my heart or mind has a soft spot for either fascists or communists. I can condemn both, you can only condemn one.

My post was to point out that the fascistic censorship forces emanating out of Germany have FAILED to stop speech on Twitter, at least in this instance of a Jewish tiktok account user who is exposing crazy liberals and being attacked for it by fascistic censorship forces.

Wait, did you…did you have in your warped head that libs of tiktok is who the fake news smeared them to be, a ‘nazi’? Oh no, the brainwashing goes much deeper than I had assumed.

https://forward.com/news/500135/libs-of-tiktok-twitter-chaya-raichik-orthodox-jewish-woman/

I nominate your comment as the worst in this blog’s history.

Fascism, and Communism, both are dependent on controlling the flow of information, controlling free speech. When information flow cannot be controlled, there cannot be fascism or communism. Fascist logic never did not end WW2. It came to America as Operation Paperclip and spread elsewhere in the world, to e.g. Ukraine.

In 1943 the following directive was issued from communist headquarters to all communists in the United States:

‘When certain obstructionists become too irritating, label them, after suitable build up, as fascist, or nazi, or anti-semitic, and use the prestige of tolerance organizations to discredit them. In the public mind constantly associate those who oppose us with those names which already have a bad smell. The association will after enough repetition become fact in the public mind.’

I see your only recourse is to invoke the same playbook. The fact you took that post as an excuse to label me as ‘soft on Nazis’, based on a completely ignorant smear of an Orthodox Jewish woman, is proof your logic is the same as the communist logic. Disconnected from reality.

You’re not ‘seeing’ anything in me, you’re invoking your own dialectic and projecting it.

Wow, how embarrassing.

29. October 2022 at 05:35

The Paul Pelosi story is getting weird.

Paul Pelosi and the communist nudist were both half naked when the police showed up. They were in their underwear.

How did someone randomly get into the mansion of the person 3rd in line to the Presidency?

Where was Nancy Pelosi?

Make it make sense.

29. October 2022 at 05:51

https://i.imgur.com/oGHEsSz.png

Why is the Clinton crime family’s chief lawyer so fixated on preventing eyes on ballot boxes in Arizona?

They’re SCARED.

29. October 2022 at 06:07

@crispus attucks:

Sumner’s prescription is workable. It’s common sense. If you gather enough data, you’ll find out for yourself.

29. October 2022 at 08:02

Spencer,

“workable” … “common sense”

That’s exactly what was said about all previous ‘instrument’ choices and ‘transmission mechanism’ choices and ‘target’ choices of central banking, the 5th plank of the Communist Manifesto:

“Centralization of Credit in the Hands of the State, by Means of a National Bank with State Capital and an Exclusive Monopoly.”

It’s time to admit that centralized planning of the economy doesn’t work no matter what the ‘target’. N-GDP or N-Wage ‘targets’, while being superior to price targeting only in the sense that it is less but still positively destructive, would only cause their own problems.

By that time however the dialectic would already have shifted, there would already be a new wave of ‘no no THIS is the better equation’ intellectuals promising an improvement over the one being implemented causing problems.

The world isn’t helped by assisting communists with ‘a better’ set of equations to better control people who are all born free and innocent. It’s not helped by insisting and thus logically / practically condoning painting what is ultimately man made to somehow be a physical law of nature.

One of the greatest tricks EVERY socialist attempt has relied on, is the false narrative that socialism is ‘inevitable’. Marx pushed the narrative that socialism will arrive ‘with the inexorability of a law of nature’.

THAT same semantic trick is echoed by ‘monetarists’ of all stripes against all critics of ‘fiat central banking’. Critics are smeared, by design, as ‘against history’ in one form or another. Be it ‘you’re naive’ (too what? The ‘necessity’ narrative), or ‘immature’ (compared to what? The ‘modern’ view of socialized man), etc etc etc.

It’s like there is a prescripted series of contrived statements and counter statements and counter counter statements all in sequence to dominate conversations through repeated intimidation, smearing and slandering until the targets relent or are in some way or another overpowered.

We are here suffering from central bank destruction because academics are pushing narrative that the issue allegedly isn’t the fact money is communist, it’s allegedly that the equations need to be changed. We are all suffering from inflation that would not and could not occur with sound money chosen by civilizations worldwide voluntarily for millennia.

Monetarists OWN THE ENTIRE INTELLECTUAL support framework as being willing and cooperating ‘advisors’ to communist banksters who are running the economy into the ground.

———

crispus attucks:

“its astonishing to me that the fed with 1400 phds on staff and a budget in excess of 500m is so wrong and sumner and his ilk are sure of as much? maybe both are wrong.”

Confirmed both are wrong. The ‘economic calculation’ logic is unassailable.

29. October 2022 at 08:14

https://nationalfile.com/video-stew-peters-releases-new-trailer-for-upcoming-died-suddenly-film/

Coming soon…

29. October 2022 at 08:19

It’s not communism, it’s our predatory society.

The “Go-for-Broke Banker” Ron Chernow:

“The brightest and most combative fore of these fuddy-duddies was Walter Wriston, the protagonist of Phillip L. Zweig’s “Wriston” (Crown, 952 pages), a jumbo book that aspires to be a biography of the former Citicorp chairman, a modern history of the bank and a comprehensive survey of postwar American finance.

Mr. Wriston must have seemed an ideal focus for such an endeavor. A born iconoclast with no reverence for his benighted superiors, he scoffed at the cumbersome procedures, excessive prudence and ingrained snobbery of the bank under Stillman Rockefeller.

By 1967, having rise to chief executive, he began to mastermind the bank’s explosive change from a stagnant deposit-and–loan institutions to a global purveyor of financial resources.

A sworn fore of bureaucrats, Mr. Wriston often joked: “Regulators sit by while snails go by like rockets.” He devoted much of his career to diving through loopholes in bank holding-company legislation or wriggling free of interest-rate restrictions.

As Mr. Zweig shows, Mr. Wriston presided over an encyclopedic range of innovations-among them negotiable CDs, term loans, syndicated loans, floating-rate notes and currency swaps-that ended forever the moribund bonking of the 1950s and ushered in our razzle-dazzle age of finance. The old prudential banker’s ethic was eclipsed by the hedonistic freedom of the consumer culture.”

29. October 2022 at 08:30

“Incomes are generated by production and the economic system is said to be in equilibrium when all the incomes earned are returned to the income flow through spending.”

Economists don’t know a debit from a credit. All bank-held savings are lost to both consumption and investment.

29. October 2022 at 09:04

Great post!

When you say ‘NGDP drives fluctuations in RGDP’ – I assume you mean it can sometimes drive fluctuations in RGDP, not that it alone drives such fluctuations. Is that a correct understanding ?

29. October 2022 at 09:26

https://www.dailywire.com/news/federal-judge-rules-arizona-activist-group-can-monitor-maricopa-county-ballot-drop-boxes

Why do dark money funded Democrat orgs not want transparency and eyes on ballot boxes?

Hint: Everyone knows the answer, fake news is just spinning a false ‘victim’ narrative in a desperate attempt to remove the eyes to permit cheating.

29. October 2022 at 09:33

“All bank-held savings are lost to both consumption and investment.”

That isn’t true for two reasons, one, because bank loans expand ex nihilo when their cash balances expand (fractional reserve), and two, cash balances today are what funds future consumption and investment. Either way they’re not ‘lost’.

Unfortunately the crucial concept of TIME is too often abstracted away in monetarist models.

29. October 2022 at 09:35

Spencer:

“It’s not communism. It’s our predatory society.”

Redundant, they are synonymous.

29. October 2022 at 09:36

“But what makes you think the Fed’s been tightening monetary policy for the past year?”

Isn’t the strong USD evidence of monetary tightening?

29. October 2022 at 09:59

Effem, You said:

“Scott not sure if you saw but perhaps the most influential strategist on Wall St (Michael Hartnett)”

It’s hard for me to evaluate something like that. We will see.

Right now, 10 year TIPS are at 2.5%, which is about 2.2% PCE inflation. Given that inflation will certainly remain high for another year, that’s about 2% for the subsequent 9 years. Of course TIPS spreads have been wrong before, but I think your claim is about investor expectations, not subsequent reality.

George, Paul Pelosi was half naked at home? I’m very disappointed.

Market Fiscalist, Yes.

kjz, Yes it is, but I regard NGDP as more reliable. As I’ve said before, I’m not suggesting precisely zero tightening, just that policy remains highly expansionary relative to the target. If people think 9% NGDP growth over the past year is “painful” wait until they see 3.5% NGDP growth.

29. October 2022 at 10:24

re: “That isn’t true for two reasons”

No. Loans and deposits come into being simultaneously. All TDs originate within the payment’s system. Income not spent is typically converted / shifted from DDs to TDs

As Dr. Philip George rediscovered, in his E-Book “The Riddle of Money Finally Solved”, diagnoses these recessions as a cash-imbalance phenomenon (which corroborates Dr. Pritchard’s (Ph.D. economics, Chicago 1933, M.S. statistics, Syracuse) thesis:

“When interest rates go up, flows into savings and time deposits increase” ( the ratio of M1 to the sum of 12 months savings ).

Demand for money:

https://fred.stlouisfed.org/graph/?g=eTtE

29. October 2022 at 10:30

As Einstein said, “a harmonious reality underlying the laws of the universe”, based on “the vagaries of observations”.

Economic theories are astonishing, mysterious, and counterintuitive.

“What science teaches us, very significantly, is the correlation between factual evidence and general theories.”

see: “Commercial Banks and Financial Intermediaries: Fallacies and Policy Implications–A Comment Leland J. Pritchard Journal of Political Economy

Vol. 68, No. 5 (Oct., 1960), pp. 518-522

“The case against commercial bank saving accounts”

Leland James Pritchard 1964 Banker’s magazine

“The economics of the commercial bank : savings-investment process in the United States” Leland James Pritchard 1969

“Should Commercial Banks Accept Savings Deposits?” Conference on Savings and Residential Financing 1961 Proceedings, United States Savings and loan league, Chicago, 1961, 42, 43.

“Profit or Loss from Time Deposit Banking”, Banking and Monetary Studies, Comptroller of the Currency, United States Treasury Department, Irwin, 1963, pp. 369-386

29. October 2022 at 10:37

“We are worried about a loss of adequate liquidity in the market,”

Yellen warned in typical economist-speak, noting that the overall supply of Treasury bonds has skyrocketed, without a commensurate increase in the ability of broker-dealers to make a market in those securities.

The FED should drive the banks out of the savings business, and simultaneously drain the money stock.

29. October 2022 at 17:57

twitter’s recently fired chief censor is sorely needed here on this blog, but don’t quote me on it.

29. October 2022 at 21:59

“Loans and deposits come into being simultaneously.”

Wrong, loans need some quantity of existing deposit as % so it can fund the business infrastructure extending the referenced loans.

Money holdings are logically and empirically prior to any loan algorithm.

That fractional reserve % of loans unbacked by existing money deposit can be numerically labelled as ‘equal’ sized additions of loan amount and deposit amount does not change this fundamental ordering of dependency.

Without any deposit whatsoever, loans cannot be instantiated. The introduction of a deposit need not necessarily be itself funded from a loan.

29. October 2022 at 22:00

Agrippa is so weak and unsure of themselves that other human beings voices are targeted for censorship. What a coward.

29. October 2022 at 22:03

Site owner

“George, Paul Pelosi was half naked at home? I’m very disappointed”

What a tone deaf narrative attempt.

They were BOTH in their underwear. Pelosi on the police dispatch call was quoted as saying “David is my friend.”

This is a lover incident gone wrong.

Fake news trying to gaslight the public to associate the communist prostitute as a Maga republican lol.

30. October 2022 at 05:41

No, it is a given that the banking system already holds enough deposits that can be multiplied.

From the standpoint of the commercial banks, the monetary savings practices of the public are reflected in the velocity of their deposits and not in their volume.

Whether the public saves or dissaves, chooses to hold their savings in the commercial banks or to transfer them to intermediary institutions will not, per se, alter the total assets or liabilities of the commercial bank banks nor alter the forms of these assets and liabilities.

30. October 2022 at 06:16

It’s like goldsmith banking. Since savers in the commercial banking system never transfer their monetary savings outside the banks, the goldsmiths in turn, could surreptitiously loan out some of the specie and bullion placed with them for safekeeping, resulting in many more certificates being in circulation than could be matched by the gold and silver in the goldsmith’s vaults.

30. October 2022 at 06:28

“No, it is a given that the banking system already holds enough deposits that can be multiplied.”

Glad you agree, so I’m not sure why you prefaced with a ‘No.’

What you are labelling ‘a given’ is also human created. Deposits before loans. Deposits ‘a given’ means they are there logically prior to loans.

30. October 2022 at 10:40

It’s logic, stock vs. flow. You have to have a unified theory, where exceptions can be explained. If you tally the inputs and outputs of the system, you will find that they are offsetting, indeed peripheral.

The only conclusion to accept is that the banks created the new money.

As Luca Pacioli, a Renaissance man, “The Father of Accounting and Bookkeeping” famously quipped: “debits on the left and credits on the right, don’t go to sleep with an imbalance”.

30. October 2022 at 12:12

“You have to have a unified theory”

Impossible to advance an alleged complete theory without inconsistency. There is no ‘must’ or ‘necessity’ to have a complete system here.

See Godel.

31. October 2022 at 06:55

There’s no inconsistency. Everything that’s happened was accurately predicted in 1961.

31. October 2022 at 06:58

Princeton Professor Dr. Lester V. Chandler, Ph.D., Economics Yale, theoretical explanation was:

1961 – “that monetary policy has as an objective a certain level of spending for gDp (sounds like N-gDp level targeting today), and that a growth in time (savings) deposits involves a decrease in the demand for money balances, and that this shift will be reflected in an offsetting increase in the velocity of demand deposits, DDs.”

Chandler’s conjecture was correct from 1961 up until 1981 (during the “monetization” of time deposits, the transition from clerical processing to electronic process, and the end of gated deposits).

Thus, the saturation of DD Vt (end game) according to Corwin D. Edwards, professor of economics. [Edwards attended Oxford University in England on a Rhodes scholarship and earned a doctorate in economics at Cornell University. He spent a year teaching at Cambridge University in England in 1932. He taught at New York University in 1954, the Chicago School from 1955-1963, the University of Virginia, and the University of Oregon from 1963-1971.]

Edwards: “It seems to be quite obvious that over time the “demand for money” cannot continue to shift to the left as people buildup their savings deposits; if it did, the time would come when there would be no demand for money at all”

That is, as stagnant (or frozen) time deposits became unhinged (the deregulation of Reg. Q ceilings), the velocity in the residual deposits were to be an offset in AD. The increased “demand for money” would thus be compensated in the turnover of the ungated transactions’ deposits.

Leland Pritchard, Ph.D., Economics, Chicago, 1933, M.S. Statistics, Syracuse: “It seems highly improbable (and in contradiction to Professor Chandler’s theoretical analysis, that the stoppage in the flow of these funds is entirely compensated for aby an increased velocity of the remaining demand deposits.

It is quite probable that the growth of time deposits shrinks aggregate demand and therefore produces adverse effects on gDp.”

The rest is history.

This is corroborated by Dr. Philip George’s The Riddle of Money Finally Solved.

31. October 2022 at 07:01

Professor emeritus Leland James Pritchard (Ph.D., Chicago Economics 1933, M.S. Statistics) never minced his words, and in May 1980 pontificated that:

“The Depository Institutions Monetary Control Act will have a pronounced effect in reducing money velocity”.