In economics, price changes don’t have any effect, they are effects

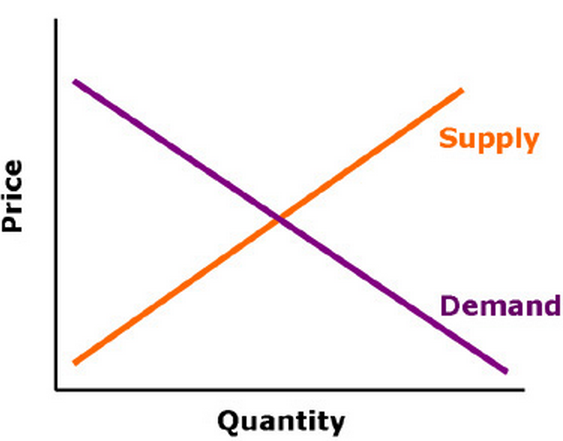

I don’t know how many times I have to keep saying this before the rest of the profession figures it out. Never reason from a price change. [Update: I mean an equilibrium price change.] It makes no sense to argue whether a higher price will increase or decrease quantity. Here is a S&D diagram. I dare you to show me how price changes affect quantity.

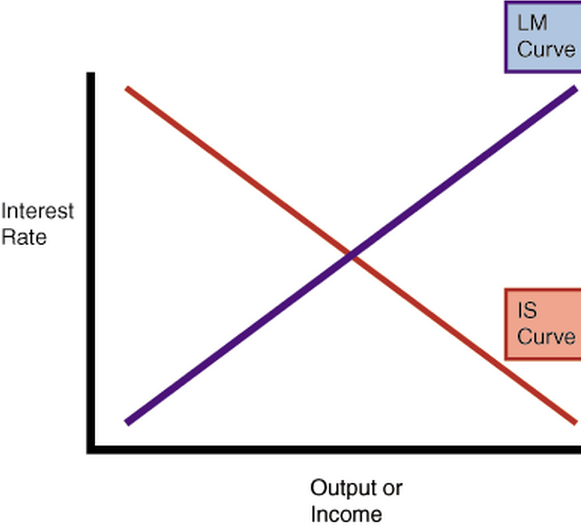

And here is an IS-LM diagram. Interest rates are the price of credit. Changes in interest rates do not have any effect on quantity of output, price of output, or any other variable. It’s not even an “other things equal” deal; price changes have no effect.

At this point some economists will say; “I meant an interest rate change caused by a change in monetary policy.” The problem is that higher interest rates can be produced by both easier and tighter monetary policy. And easier and tighter monetary policy have opposite effects on prices and output. So I’m sorry, but it’s still a meaningless debate. It’s not that there is a right or wrong answer; there is no coherent question. Monetary policy can shift the LM curve, the IS curve, or both.

Consider this analogy: A debate over whether high oil prices increase or decrease global oil consumption. The debate is meaningless. Price has no effect. Here’s how the issue should be discussed:

A. An Arab oil embargo caused higher prices and lower consumption in 1974.

B. Booming Chinese auto sales caused higher oil prices and higher consumption in 2007.

Prices are not a cause of anything; they are an effect. And interest rates are a price. So please stop these silly posts discussing the impact of a change in interest rates. Talk about the effect of expansionary and contractionary monetary policies—that’s an interesting question.

This criticism applies to both sides of the debate. John Cochrane and Noah Smith should not be discussing the possibility that higher rates lead to higher inflation, and Paul Krugman should not be claiming that the standard model suggests that higher rates lead to lower inflation. Actually, both claims are true in specific situations. But without specifying the specific situations in which each claim is true (especially the path of the money supply and IOR) the claims becomes utterly meaningless.

Truly a debate about NOTHING.

PS. If you are still having trouble with this, consider the following. A 1/4% rise in the fed funds rate today can be accompanied by a near infinite number of simultaneous expected changes in the future expected path of variables like the fed funds target, the monetary base, the interest rate on reserves, the reserve requirement, and all sorts of other policy levers. Those variables in turn have a near infinite number of effects on all sorts on market variables other than short term interest rates, including TIPS spreads, commodity prices, forex prices, future expected real estate prices, stock prices, corporate bond risk spreads, etc., etc. And all that happens immediately.

Here’s another example. Assume Japan has run zero percent inflation for 20 years while the US has a credible 2% inflation target. Zero inflation is expected to continue in Japan. Suddenly they depreciate the yen 17% and set up a rigid currency board with the US. PPP tends to hold in the very long run; so long term Japanese inflation expectations immediately rise from 0% to 2%. Interest parity holds even in the short run, so Japanese interest rates immediately rise to US levels. That’s a case where Cochrane is right, and it’s 100% consistent with IS-LM. In contrast, in January 2001 the Fed cuts rates more than expected, and TIPS spreads rise sharply on the news. That’s a case where Krugman was correct, and it’s 100% consistent with IS-LM.

The correct answer is “it depends.”

PPS. Question for Nick Rowe. Does my yen/dollar peg solve the coordination problem you discuss in this post?

HT: TravisV.

Tags:

11. November 2014 at 09:04

Hi. I’m not an economist, so forgive me my heresies, but I will speak from an area I have great experience in, the oil business. I think that some people (me included) use prices as a shorthand for shifts in either demand, supply or both. It seems to me that the picture you show is a snapshot in time, and doesn’t represent what’s going to happen in a real, dynamic situation. Oil prices have gone down – observable fact. Why? Definitively increased supply from US shale at lower prices that OPEC was trying to maintain (downward shift in supply curve), and possibly downward shift in demand (maybe not – alot tougher to suss out.) _ But we are no longer on the graph you show_ – so one can often, and usually conclude something about quantity from price changes. At least in my biz.

It’s even more drastic in the domestic nat gas biz. Increased seasonal prices lead directly to shift demand in the power sector from gas to coal (and the converse). Shale has resulted in an ever-downward moving supply curve. The classic curves exist for microseconds.

I guess my point is that the classic supply demand curve says NOTHING about a truly dynamic market. Price changes indicate that the curve(s) have changed, and will customarily indicate the direction quantity is moving.

If you’re talking about the actions of a single firm FACING that S/D at a point in time, OK, it holds. I also agree that something causes prices to move, but at least my markets respond to those moves by very rapidly (and also long-term slowly) changing the curves, not moving along them.

Do I make any sense?

11. November 2014 at 09:14

I don’t follow. While not disagreeing with you on interest rates, I don’t think that your general claim is true, as far as I understand it.

For example, say I sell tomatoes at the local market. One day, I double the price I usually charge. This price change is an effect (it’s the result of the reasoning that led me to change my price for tomatoes) but it’s also a cause of the likely fall in the quantity demanded.

Similarly, when you say “Big increases in the minimum wage cause unemployment”, you mean that “The change in the price of marginally valuable labour further away its equilibrium level causes a change in the quantity of that labour that is demanded”.

11. November 2014 at 09:25

Good post. Helpful to me.

11. November 2014 at 09:38

It’s too bad that macro is hard for even brilliant people to understand.

I do like that we’re advocating more NGDP, though, because advocating higher inflation is a tough sell.

It’s not actually the inflation that we want. We just think that if we have faster NGDP growth, then there will be A LOT of RGDP growth and employment growth with a teeny-tiny increase in inflation.

While that story is persuasive and appealing, too many people are stuck in the mud of the “Inflation Fallacy”……

http://worthwhile.typepad.com/worthwhile_canadian_initi/2014/09/its-the-inflation-fallacy-duh.html

11. November 2014 at 09:48

@W. Peden

If you double the price and nobody else does, you will sell zero tomatoes. If you double the price and everybody else triples their prices, you will sell all your tomatoes (stipulating for the moment that your tomatoes are roughly the same as everyone elses).

While your pricing decisions will affect your particular sales, they will have a miniscule effect on the total quantity of tomatoes demanded. Assuming you want to make money selling tomatoes, your pricing decisions will mostly reflect what everyone else is doing. Unless you’re a monopolist, but you’ll still be constrained by your cost curve and the market demand curve.

11. November 2014 at 09:54

Excellent observation.

Prices of fuel change because customers are either able to borrow or are broke (insolvent). Prices are the outcome … but they have downstream effects.

When there are insolvent customers then drillers must borrow in their place until they are also insolvent.

What is underway in fuel markets today is dueling insolvencies! Right now customers are failing first and fuel prices are falling.

Interest rates are irrelevant as they are cost of purchasing power claims against capital (resources) rather than capital itself. As capital is wasted/destroyed, claims against it are rendered worthless … it doesn’t matter how much- or how little these claims cost.

11. November 2014 at 10:01

If NGDP is basically a sum total of prices, isn’t NGDPLT a form of reasoning from a price change?

11. November 2014 at 10:14

Marc, I’m afraid that in economics you need to use very precise language or your meaning won’t be understood. I have no idea why “dynamic” considerations invalidate this post. I think you might have something else in mind.

I would never deny that in some industries a price change is usually correlated with a particular change in Q, as in some industries supply is much more or less stable than demand.

W. Peden, Good point, check my update.

Carl, Think of NGDP as like a hyperbola, the AD curve. Then a change in NGDP is a shift in aggregate demand, and hence not reasoning from a price change.

11. November 2014 at 10:16

@W. Peden, in your tomato example, quantity falls because the supply curve shifted up and left. If price doubles because the demand curve shifts out, then quantity does not fall. So, price doubling is not what causes quantity to fall or rise; shifts in supply or demand are the cause.

Increases in the minimum wage cause unemployment because the wage floor prevents markets from clearing. We can’t say that a wage increase itself causes unemployment because wage increases that result from increased labor demand actually increase employment. Once again, its the shift in supply or demand that matters, not the price change per se. I think that is Scott’s point.

11. November 2014 at 10:33

I disagree with you on short-term interest rates. Moden monetary policy sets the price and then the quantity adjust to it (supply is infinitely elastic). If the central bank follows a kind of optimal Taylor rule, then you’re right. But otherwise no.

Btw. how could monetary policy induce a shift of the IS curve (not along the curve)? Expectations?

11. November 2014 at 10:38

Double post, sorry.

IS-LM has nothing to do with modern monetary policy. In the IS-LM framework the central bank control the quantity of money, whereas now central banks control its price.

“Suddenly they depreciate the yen 17% and set up a rigid currency board with the US. PPP tends to hold in the very long run; so long term Japanese inflation expectations immediately rise from 0% to 2%. Interest parity holds even in the short run, so Japanese interest rates immediately rise to US levels.”

How do they depreciate the yen? You’re confusing the cause (increase in the interest rate) and the effect (depreciation of the yen). If you’ve in mind the micro-foundations behind or simply something like Dornbush’s overshooting model it is pretty clear.

11. November 2014 at 10:48

MB. Yes, obviously expectations shift the IS curve. Happens all the time.

Not sure your point about modern monetary policy and interest rate targeting–how does that apply to anything I said here?

On your second comment, it’s easy to peg an nominal exchange rate with a fiat money system; the central bank simply buys and sells unlimited foreign assets at the target rate. The Swiss recently did exactly what I suggested here–sharply depreciated their currency against the euro, then pegged it at 1.2. You should check out the Swiss move, that’s truly “modern” monetary policy.

The overshooting model is a nice one for exogenous changes in the money supply, but I wasn’t relying on it.

11. November 2014 at 10:49

George Selgin posted this a week ago: http://www.freebanking.org/2014/11/04/keynes-to-fdr-forget-quantitative-easing

[Sigh]…..

11. November 2014 at 10:53

Also, someone should write a post highlighting what’s happened with 5-Year Inflation breakevens since October 15th and 16th…..

11. November 2014 at 11:07

@Travis, short-term breakevens have edged up about 0.2% since the middle of October. BTW- the stock market bottomed out on October 15th and has bounced 8% since.

So…I can’t put my hands on anything specific, but the markets seem to be guessing that the Fed will be more dovish than they thought in the middle of October and/or they are more optimistic about the economy (GDP and jobs report). I can never tell how to separate these two.

11. November 2014 at 11:09

Scott: “Question for Nick Rowe. Does my yen/dollar peg solve the coordination problem you discuss in this post?”

Yes. (Though there might be speculative attacks on the peg.)

11. November 2014 at 11:24

Okay, a change in price for a good cannot change the quantity of that good. We can talk about shifts in supply or demand that shift the price and quantity of that good.

However, we can say that the change in the price of a good impacts the supply and demand of other commodities.

Look at oil. A change in the price of oil, lowers production and transportation costs for other products (supply shock) Furthermore, falling oil prices raises the real income of consumers. (demand shock)

The interest rate is the price of credit, a change in this price should impact other sectors.

11. November 2014 at 11:55

Is it fair to put things this way:

A. An Arab oil embargo, via higher oil prices, caused lower oil consumption (quantity demanded) in 1974.

B. Booming Chinese auto sales, via higher oil consumption (demand), caused higher oil prices in 2007.

Then prices are some times the reason for changes in quantity demanded, and sometimes changes in demand are the reason for changes in prices. The key difference here not being that demand causes price changes, and price changes cause changes in quantity demanded.

11. November 2014 at 11:57

A question: in microeconomics, does your rule that “prices are never a cause of anything” still hold? Take the following reasoning (that I heard from Milton Friedman, by the way): “how do producers decide how many units of a good to produce? They increase production until the marginal unit adds as much to costs as to income. Then they stop producing. Now, if the price for the good increases, they realize it is now profitable to produce one more unit. So they increase production. In other words, the higher price shifts the point where MR = MC.”

Now it seems to me that the above _is_ economics reasoning; and it does treat a price change as a cause of something else. And it was Milton Friedman who said the above (you can find it in Free to Choose for example).

11. November 2014 at 12:02

Yeah, those Noah/Cochrane pieces had me scratching my head. Investors don’t really care what the Fed does with interest rates, they care about what inflation will do to their nominal returns.

The whole idea you can talk about interest rates that way seems obviously wrong. Interest rates were much higher at the beginning of the Volcker regime, but so was inflation. Why? Simple, investors did not yet believe the Fed would stop inflating.

11. November 2014 at 12:17

Scott is right. You can’t reason from a price change.

And this is why price elasticity of demand (dQ/Q / dP/P) calculations for, say, oil are so useless.

You actually need a four phase model:

1. Supply is increasing:

1a. faster than demand is increasing

1b. slower than demand is increasing

2. Supply falling:

2a. faster than demand is falling

2b. slower than demand is falling

For 1a., prices will be falling even as demand is increasing, elasticity is negative

For 1b., prices will be increasing, elasticity is positive

In both cases, demand is increasing

For 2a., prices are increasing, demand is falling and elasticity is a positive number

For 2b., prices are falling, demand is falling, elasticity is a positive number

And this is why we have to be very careful with statistical analysis, which virtually no one doing oil markets analysis is.

11. November 2014 at 12:37

Sorry, the price elasticity of demand signs should read:

1a. –

1b. +

2a. –

2b. +

11. November 2014 at 13:18

#1: Norway

#2: Switzerland

#3: New Zealand

#4: Denmark…..

http://www.businessinsider.com/the-30-most-prosperous-countries-in-the-world-2014-11

http://www.businessinsider.com/heres-a-snapshot-of-global-prosperity-right-now-2014-11

11. November 2014 at 14:20

Thanks Travis, I did a post at Econlog.

Nick, Thanks, and BTW, Switzerland did almost exactly what I described, and survived speculative attacks (admittedly easier to do if you are trying to raise inflation.)

Rick, For example A, I’d rather say a reduction in supply reduced consumption, or a rise in price reduced “quantity demanded.” The word ‘consumption’ is not synonymous with demand, so B is wrong. A and B are symmetrical, so your explanations should be symmetrical. Right now they are not.

Maurizio, If the price of coffee falls because of more supply of coffee, there will be less demand for tea. If the price of coffee falls because of less demand for coffee (say a health scare) then there will be more demand for tea. However in the coffee case it is fair to talk in “other things equal” terms about the effect of a change in the price of coffee on the demand for tea.

Steven, Sorry, I don’t follow that at all. What “elasticity” are you describing?

Travis, That’s a really odd ranking for NZ.

11. November 2014 at 15:00

Scott,

“Never reason from a price change. [Update: I mean an equilibrium price change.]”

given that we are never in a perfect equilibrium, is your point still valid?

11. November 2014 at 16:07

Prices are both means to ends and also ends of means.

It is false to claim prices are ONLY effects. People utilize and respond to past prices as part of the totality of means to achieve their ends.

11. November 2014 at 16:25

Kevin Dick,

“[Unless you’re not a monopolist etc]” – my scenario was not supposed to be an equilibrium case; just an everyday case of cause-and-effect. My local outdoor market doesn’t have multiple sellers of tomatoes. Or any sellers, for that matter! IF I double my price and that’s not driven by e.g. a rise in costs, then there is an opportunity for someone else to enter the market and get in on the extra profits, but we’re just thinking about the causal relations on a particular day.

BC,

Just because A is caused by B, it does not follow that A does not cause C. That prices are caused by shifts in quantities does not entail that prices do not cause changes in quantities, just like the fact that a thunderstorm is caused by atmospheric conditions doesn’t entail. that the thunderstorm doesn’t cause the animals in storm area to be frightened. Put more abstractly, that causes are themselves effects does not mean that they’re not causes.

Scott Sumner,

So let’s see if I follow you now: equilibrium prices cause no changes, because in equilibrium all the relevant supply/demand curves and prices have done all their adjustments? Or put another way, once prices have co-ordinated supply and demand, there’s nothing further for them to do, but you can still then have a shift in quantity demanded or quantity supplied that causes a change in price?

11. November 2014 at 16:43

never reason from a price change in an unrealistic model. Never ever.

11. November 2014 at 16:59

Philippe,

No, that’s not at all a good methodological principle.

11. November 2014 at 17:25

it wasn’t really meant as a methodological principle.

11. November 2014 at 17:33

Shame, because it’s not clear what else it could be, except maybe a joke.

11. November 2014 at 17:57

satire is a type of joke, right?

11. November 2014 at 19:54

“It makes no sense to argue whether a higher price will increase or decrease quantity.”

Taxes e.g -excise duties- in oil products have effect (direct or indirect) in prices and in quantity taking into consideration income elasticity of demand?

12. November 2014 at 00:36

Hhmmmmmm. If Cochrane is arguing for an interest rate peg…he is really arguing for price controls. So even if the supply or demand for credit booms or shrinks….

12. November 2014 at 01:33

Philippe,

The thing is, it’s close to a legitimate methodological principle: idealizations can be good if you’re looking to simplify matters conceptually/computationally or focus upon one single causal relation (or a counterfactually small set of causal relations) but not if the idealization is what drives the general conclusion you’re drawing.

12. November 2014 at 01:51

W. Peden: I understand Scott this way: “Never reason from hypothetical price change if it is the only data point you have. Because your results while coherent may very well be useless.”

I do not read him that “Price changes, in fact, do not cause anything” as you suggest.

The best way I understand this topics is that many times in Economics the variables are co-determined. Nick Rowe had a very good post here: http://worthwhile.typepad.com/worthwhile_canadian_initi/2012/06/linearity-and-the-concrete-steppes.html

So prices and quantities on a market are co-determined simultaneously based on how supply and demand looks like at the moment. However looking only at price does not help us.

PS: Scott, I have one quibble with this part – “It’s not even an “other things equal” deal; price changes have no effect.”

If price changes in standard S&D model and other things are equal that means that supply/demand does not shift which means we are only moving along the curve which has a pretty specific result in that given model. That is what I think confuses people here. It may have been to strong a wording.

12. November 2014 at 02:59

If interest rate rises stifle investment and production falls and from that less finished products are brought to market and causes a higher market price , then higher interest rates can cause price inflation. Likewise lowereing interest rates can cause deflation in market prices if they increase productivity and the number of products brought to market.

12. November 2014 at 04:08

J. V. Dubois,

I certainly agree with Scott, as you read him.

Anyway, on the Western European front, the Bank of England today announced that it expects to fail at inflation-targeting over the next few years. *SIGH*.

12. November 2014 at 05:00

[…] Source […]

12. November 2014 at 05:41

Scott –

See, for example, estimates of price elasticity of demand in Table 3 (p 34) of this document:

http://econweb.ucsd.edu/~jhamilto/understand_oil.pdf

These all show that short run price elasticity of demand for oil is a negative number. Now, if you actually go period by period in the historical data (which I have), you’ll note that these elasticity numbers are all but useless for understanding quantity / price dynamics.

First, price elasticity is a function of whether demand or supply is in the driver. If supply is falling, then prices will tend to increase, leading consumption to fall. (Well, it has to as an accounting matter unless you run down inventories.) The elasticity coefficient will be negative (+dP / -dQ).

On the other hand, during an expansion, we can see increasing prices in the face of increasing supplies. Such was the case from 2003 to 2008 (albeit, there was little supply growth from 2005 to 2010). The coefficient is positive (+dP / +dQ).

In both cases, prices are increasing, but it’s not possible to reason to the underlying supply-demand conditions from that alone. An increase in price does not necessarily imply a decrease in demand.

Second, elasticity depends greatly on where you are wrt carrying capacity. For example, if the US is spending 2% of GDP on oil, then you’ll probably see an increase in price accompanying an increase in demand. If an economy is above carrying capacity price, as Europe has been since 2011, you’ll see falling consumption in the face of falling oil prices. Again, the elasticity coefficient is positive (-P / -Q), but it tells us virtually nothing by itself. Put another way, price elasticity of demand is also a function of where on the supply / demand curve we are. Conceptually, it’s closer to the second derivate and than the first derivative. It doesn’t apply uniformly across the supply demand curve.

And by the way, if a country is above the carrying capacity price for oil, it has always been in either recession (more typically) or stagnation. Always. We don’t need hysteresis, interest rates, NGDP, low TFP growth, fiscal policy, demographics or the rest. If oil consumption as a percent of GDP is greater than carrying capacity, the best you can hope for is stagnation. That’s a very consistent lesson from the historical record.

12. November 2014 at 06:02

I think this is correct. Reminds me of the identification problem in econometrics. Probably can’t reason from just a change I equilibrium Q either.

12. November 2014 at 06:04

“change in equilibrium Q”

12. November 2014 at 09:50

[…] him to read this (among others) Scott Sumner […]

12. November 2014 at 11:45

Philippe, Yes.

W. Peden, You mean a shift in supply or demand can still cause a price change. Yes.

Alex, Yes.

JV, See my next post.

Dinero, See my next post.

Steven, I can’t make any sense out of your post. You seem to be defining elasticity in a way that has nothing to do with how economists define it. Elasticity is not the percentage change in quantity divided by the percentage change in price. That number could be positive or negative, and doesn’t measure anything.

gofx, Yes, it’s essentially the identification problem.

12. November 2014 at 14:58

Well, go ahead. Please define price elasticity of demand for me.

13. November 2014 at 07:04

Steven, It’s percent change in Q demanded over percent change in price, along a given demand curve.

The last five words are crucial.

13. November 2014 at 07:48

That’s great.

So how do you get the data to analyze that?

14. November 2014 at 05:44

Steven, That’s the whole “identification problem,” which requires very sophisticated economic analysis. But sometimes there are natural experiments, such as a big tax change. Even there, however, it only gives you the short run elasticity, a figure that is much lower (in absolute value) than the long run elasticity.

14. November 2014 at 05:52

Let me answer my own question for you.

1. You can take data over a longer period, and assume that supply effects balance out over time. This is questionable, but if I read it correctly, essentially what most economists do. The downside of this approach is that you’re left reasoning from a price change at any given time.

2. You can move to a two or four phase model, as the one I outline above, and then work the numbers by phase. In this case, you’re looking for breaks in the data, and having seen a presentation on this at the IEEA conference, I think the analytics work pretty well. (I know the break in the US oil data back to 1970 almost month by month, so I know where the breaks are and these line up pretty well with statistical analysis.)

That’s how you do it, best I can tell.

15. November 2014 at 06:21

Steven, No one can say you lack self confidence. In one day you go from not knowing the elasticity of demand concept, to solving the age old identification problem (worth a Nobel Prize in Economics if true.) Seriously, it’s really hard to estimate elasticities, and nothing in your post suggests to me that you’ve solved that problem. You’d have to be much more specific than “line up pretty well”

20. May 2015 at 20:42

[…] price (P) of a stock, bond or commodity tells us nothing about the effect on the quantity (Q). “Never reason from a price change,” is how economist Scott Sumner, director of the program on monetary policy at George Mason […]

25. February 2016 at 11:51

[…] Sumner’s rants against reasoning from interest rates explain why the Fed ought to be embarrassed to use interest […]