Hypermind vs. the consensus of economic forecasters

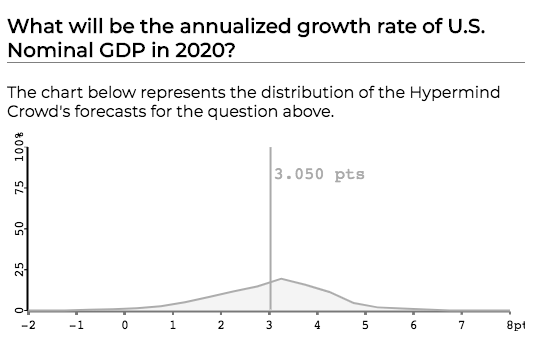

There’s a new Hypermind NGDP prediction market, which you should definitely check out. It’s still early, but right now the mean forecast for growth from 2020:Q1 to 2021:Q1 is 3.05%. That suggests that money is a bit too tight.

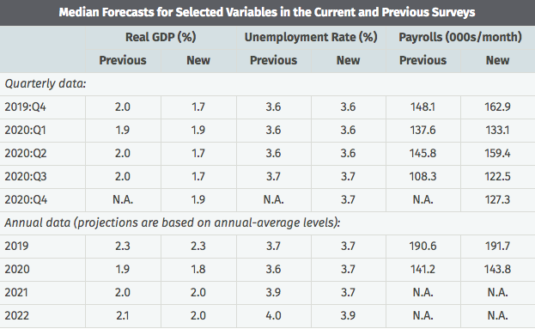

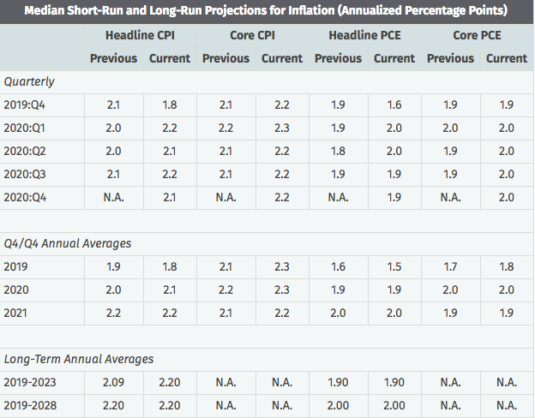

In contrast, the consensus forecast of economists, which is published by the Philadelphia Fed, shows monetary policy is right on course. They don’t provide NGDP forecasts, but they do have RGDP growth and PCE inflation:

If you combine the 1.8% RGDP growth with the 1.95% PCE inflation, it looks like the consensus forecast for NGDP growth is about 3.75% (albeit for 2019:Q4 to 2020:Q4). Thus Hypermind forecasters expect nominal growth to be significantly lower than the consensus forecast of economists.

If you combine the 1.8% RGDP growth with the 1.95% PCE inflation, it looks like the consensus forecast for NGDP growth is about 3.75% (albeit for 2019:Q4 to 2020:Q4). Thus Hypermind forecasters expect nominal growth to be significantly lower than the consensus forecast of economists.

Let’s revisit this post in about 18 months.

PS. Each forecaster at Hypermind provides a distribution in their new set-up. So those long tails are not point estimates of individual forecasters.

Hypermind is actually much easier to use than you’d think. I encourage people to participate. You will help to move the economics profession out of the Stone Age and also win free money.

PPS. The 5-year TIPS spread is 1.55%. That’s for the CPI, and implies about 1.3% for the PCE. If you add 1.3% to the Philly Fed’s 1.8% RGDP forecast you get 3.1%. Interesting. (I expect inflation to be higher than that.)

PPPS. FWIW, I predict 3.4% NGDP growth (which includes 1.6% RGDP growth). That’s midpoint between Hypermind and the Philly Fed. I believe money’s a bit too tight.

Tags:

26. November 2019 at 10:36

Yes, put a pin in this. I agree with your overall take. Put me down for 3.5% (Price is Right strategy.)

26. November 2019 at 10:49

My meta-prediction is that the 2020 Hypermind forecast will be less accurate than previous ones, as a result of the change in structure from a prediction market to a glorified survey.

26. November 2019 at 14:06

The SPF does have NGDP forecasts.

26. November 2019 at 15:20

Sam, But it still has financial incentives.

John, Do you have a link?

26. November 2019 at 15:40

There is still an inclination of central bankers and orthodox macroeconomists to be too tight on monetary policy.

For now, that is a problem. We lose a little bit of real output for no good reason. Marginal employees, whose lives might be improved, cannot find work.

If the global economy tips into recession, the timidity of central bankers will likely be a major problem. Already, central bankers are preaching they are out of ammo.

26. November 2019 at 17:52

Scott, here is the SPF NGDP forecast: https://www.philadelphiafed.org/research-and-data/real-time-center/survey-of-professional-forecasters/data-files/ngdp

27. November 2019 at 04:45

Wait a second, does Sumner really want his readers to participate? I am not sure that I trust an economic prediction that would have me as a contributor. But for what it is worth, my impression is that the Fed is divided, with some voting members (mostly regional board Presidents) thinking that the Fed’s current stance is too accommodative. So that would incline me towards thinking that whatever the Fed’s voting members are projecting as economic growth and inflation, go lower than that.

I also suspect that the election will have more of a dampening effect on the economy than most folks currently predict.

We are about to establish as a principle that the president can do almost anything they want, so long as the opposition party doesn’t hold a supermajority in the senate. Sooner or later this is going to lead to a showdown between the President and Congress versus the Supreme Court, and I don’t think that the court will win. That is, we are seeing a permanent rise in political uncertainty in the US, and I don’t think that companies have fully incorporated this uncertainty into their models yet, but they will increasingly be dong so and this is going to dampen their investment and hiring in the US. It is great for Canada, though, which already has had the good sense to give IT companies a very free hand in hiring and sponsoring employees for immigration.

27. November 2019 at 06:39

I still don’t think we have a good sense as to the impact of elections and the trade war in general, let alone one as visible as the 2020 election. I won’t go as far as to say that a prediction for 12-18 months from now is hubris, but there are, in my mind, several highly visible variables which will converge during this time:

– Presidential election

– Outcome of house/senate election

– formalized agreement with China

– Fed leadership

– energy supply disruption via Iran/Saudi conflict

Utilizing a distribution I think will defray some of the variability within predictive error terms, but on the whole I think predictive power comes much more sharply into focus Q2 2020.

27. November 2019 at 07:58

US: Annual core PCE Price Index ticked down to 1.6% in October vs. 1.7% expected

27. November 2019 at 10:56

Scott, the continuous double auction market structure provides incentives that the current format doesn’t. For example, it incentivizes “smart money” forecasters — even those who just make sure that the market price incorporates the latest FRB forecasts, say — to check back often to “pick off” the noise traders who make foolish trades. The payout structure for the previous contests didn’t have to do with how accurate your forecasts were, just how much “hypermind money” you won from trading the NGDP question. You can win this money by having better forecasts, sure, but you can also win it by just being attentive and enforcing consistency when someone moves the price too much in response to what they think is news. (This is all in the spirit of Fischer Black’s famous paper “Noise”, of course.)

In contrast, in the current setup, when the other forecasters are doing something dumb, you don’t get extra benefit from correcting their mistakes. For example, currently the Q1 2020 crowd forecast has a bizarre bimodal distribution, which is almost certainly wrong, probably because it just launched so it incorporates very few estimates so far. If this were structured as a *market*, one could make a very low risk (almost pure arbitrage) trade by buying the part of the outcome distribution that is too low (the “dip” between the two modes) while simultaneously selling the nearby parts of the distribution and the modes. This does not require you to have any actual “alpha” about the true mean of thee distribution, just a prior that it is smooth and unimodal. But unless I am misunderstanding the scoring system for the new contrast, the utility maximizing thing the do in the new format is always to express your true subjective distribution, regardless of what other forecasters have done. This lack of incentive to correct others’ mistakes via near-arbitrage trading is the source of my intuition that the new format will lead to a less accurate consensus.

To use an analogy, consider a “guess how many jelly beans are in the jar” contest, where the contestants are ranked by brier score and rewarded proportionately. Compare that to a futures market with a contract that settles to the number of jelly beans in the jar, and hedge funds are rewarded with management fees to the extent they make money trading the contract. Scott Alexander has an aphorism (I forget the catchy name) to the effect that a nontrivial number of respondents to any survey will just produce garbage answers, out a desire to screw with the experimenter or simply for fun. Those “noise traders” will not win the jelly bean guessing contest, but they will mess up the average. In contrast, their presence actually makes the futures contract on the number of jelly beans *more* efficiently priced, because they increase the potential profits of informed traders.

27. November 2019 at 11:14

I should add a note about why I believe the things I do. I’ve been in the top ~10 for many of the previous contests, winning a little less than $2K total. So obviously I have a preference for the old system 🙂 But also, my “strategy” (if it can be called that) more or less amounts to assuming that the Atlanta Fed’s GDPNow model for Q/Q RGDP growth is correct on average, and assuming next quarter’s annualized change in the GDP deflator will be about the same as last quarter’s (or the average of the last few quarters). So, certainly no “alpha” (in the sense of superior discretionary judgment or a forecasting model that uses non-public information) was involved. 90% of the time or more the markets were consistent with my very stupid model, but the rare occasions where they were not were enough to make my trading very profitable. I attribute this to my trading against uninformed market participants. Because I bet big, over time the fact that my strategy was profitable meant that the Hypermind forecast was less likely to deviate significantly from the Atlanta Fed-based model, i.e. the success of my strategy led to my forecasts having bigger weight. To the extent this outcome is “correct” (i.e. made the Hypermind price more accurate), it is not obvious to me that the a similar positive result will emerge from the dynamics of the new contest format.

28. November 2019 at 08:42

Thanks Ethan.

Sam, It’s still early on the quarterly markets, which were just set up.

10. December 2019 at 10:24

Bloomberg interviews Trichet (10th December 2019).

Trichet wants FED to tighten.

No-one has the bad manners to mention 2011.