How does fiscal austerity affect exports?

I had thought the standard Keynesian model predicted that fiscal austerity would weaken a currency. Thus austerity should boost net exports, but reduce domestic expenditures by even more. Ed Dolan suggests that the opposite has been occurring:

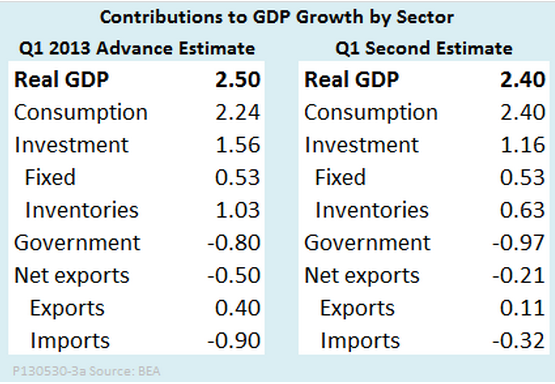

The second revision of GDP data released today by the Bureau of Economic Analysis confirmed that the U.S. economy expanded at a moderate 2.4 percent annual rate in the first quarter of 2013. The figure for overall growth was almost unchanged from the 2.5 percent of last month’s advance estimate. However, there were significant changes in several of the components of GDP growth, as the following table shows.

Tags:

6. June 2013 at 17:44

I may be mistaken, but I recall that fiscal austerity depreciates the exchange rate because it lowers real interest rates (by reducing demand or forcing monetary offset through lower interest rates). But, according to Keynesians, the opposite should now be true. Nominal rates are held at zero and the real rate is affected by inflation. Fiscal contraction (if not offset) reduces inflation and hence raises the real rate, leading to an appreciation, which hurts net exports.

6. June 2013 at 17:59

I don’t understand this post. J’s articulation of the Keynesian logic here is absolutely correct: normally, when interest rate is not constrained by the zero lower bound, the monetary authority will lower rates in response to fiscal contraction and weaken the currency. (It’s worth noting that here, the monetary authority is just mimicking what would happen in frictionless, real equilibrium, where a decline in government spending should generally cause a real depreciation.)

But when the zero lower bound is binding, the interest rate cannot perform its usual role, and government austerity will either have no effect on the real exchange rate or possibly (by decreasing expected inflation) actually strengthen it. This is the extreme Keynesian position, one that I don’t entirely endorse (I am more of a believer in “monetary offset”, even at the zero lower bound), but it is nonetheless consistent with the evidence you’re citing here.

So I just don’t understand what you’re aiming at here. Your tone suggests that you’re not citing this as evidence contrary to your own position; instead, presumably you envision a world where “fiscal austerity -> strengthening real exchange rate and lower net exports” is consistent with your views on the primary of monetary policy. But I have no idea what the world could be. If a central bank explicitly targeted NGDP and was no constrained by the zero lower bound, fiscal austerity should produce a boom in net exports.

7. June 2013 at 05:41

J and a reader, Fiscal austerity should increase government saving (reduce dissaving), which should depreciate the exchange rate and boost net exports. In my view US net exports have fallen due to “headwinds” such as the European recession. This makes the 2013 Q1 number even more impressive. In other words, fiscal austerity should have hit domestic spending especially hard, but that sort of spending actually grew faster than the overall RGDP. Without the headwinds from overseas, growth would have been even faster. That makes it even less likely that fiscal austerity is slowing the economy.

8. June 2013 at 09:08

You copied an entire post at seeking alpha:

http://seekingalpha.com/article/1487272-how-does-fiscal-austerity-affect-imports

Irregardless of content, this is plagiarism.

9. June 2013 at 06:01

Adm, ?????????????