How bad is the Italian debt situation?

Tyler Cowen recently linked to a John Cochrane post, discussing Larry Kotlikoff’s views on public debt sustainability. Here’s Cochrane:

(By the way, if you’re feeling superior and taking comfort that Europe will go first off the cliff, Kotlikoff disagrees. Europe’s debts are larger, but their social programs are better funded, so their fiscal gaps are much lower than ours. The winner, it turns out, is Italy with a negative fiscal gap. Answering the obvious question, Kotlikoff offers

“What explains Italy’s negative fiscal gap? The answer is tight projected control of government- paid health expenditures plus two major pension reforms that have reduced future pension benefits by close to 40 percent.”Don’t get sick or old in Italy, but perhaps buying their bonds is not such a bad idea.)

I am a bit skeptical of that claim; so I decided to check with God, er . . . I mean I decided to check with the ultimate arbiter of truth, the asset markets:

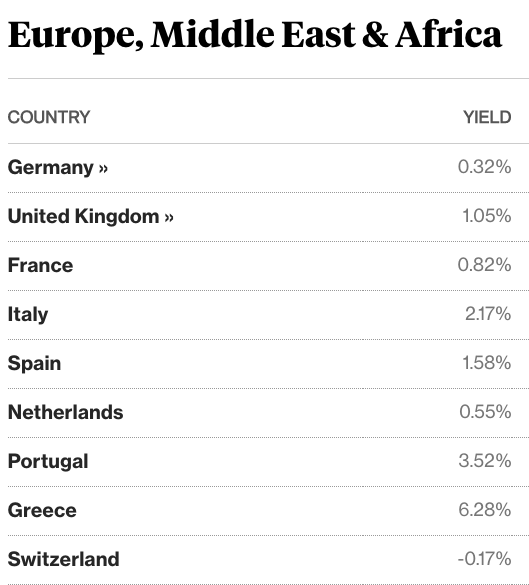

As you can see, Italian 10-year bonds offer considerably higher yields than German, French and Dutch bonds, and even higher yields than Spanish bonds. Italy has a massive public debt (third largest in the world), an economy that has shown almost no growth since 2000, and a very dysfunctional political system (which the voters recently decided not to reform.)

As you can see, Italian 10-year bonds offer considerably higher yields than German, French and Dutch bonds, and even higher yields than Spanish bonds. Italy has a massive public debt (third largest in the world), an economy that has shown almost no growth since 2000, and a very dysfunctional political system (which the voters recently decided not to reform.)

I greatly respect Kotlikoff, and even more so John Cochrane. But I respect the markets far more than any mere mortal. So unlike Kotlikoff and Cochrane, I remain relatively pessimistic about the Italian debt situation.

PS. I am back from 5 days in Turks and Caicos (is there a law in the Caribbean mandating nothing but Bob Marley music at resorts?), and I am starting to get caught up.

I have a new post on Bretton Woods as an example of the guardrails approach to policy, and another post commenting on the French elections.

My guardrails post is intended to address tiresome criticism of NGDP targeting by people who have never bothered to actually read what I have written on the topic. No, neither the current lack of interest in NGDP futures trading nor the risk of market manipulation pose any kind of problem for the system I am actually advocating. (Unless you believe, “Bretton Woods could not possibly have worked because speculators would have manipulated the market.”)

Tags:

24. April 2017 at 13:04

I think Kotlikoff is going under CBO rules: assume that the current laws will stay valid forever.

However, the market understands that France not having reformed its pension system is actually a form of policy capital: they can still reform and save money, whilst Italy has already cashed in (naturally, the earlier you cash in the more that capital is worth).

24. April 2017 at 15:43

“But I respect the markets far more than any mere mortal.”

“No, neither the current lack of interest in NGDP futures trading nor the risk of market manipulation pose any kind of problem for the system I am actually advocating.”

Pick one Mr Inconsistency

24. April 2017 at 16:08

Luis, Very good point.

24. April 2017 at 18:55

So how did Italy ‘cash in’? Is Italy invested in a portfolio of stocks, real estate and bonds that will provide the funds to meet future outflows of pension and health care benefits? Like Canada is.

25. April 2017 at 01:19

How accurate are these “market” prices anyhow when the ECB is buying so much bonds? How is this a “market” price?

25. April 2017 at 01:32

The bond market is also pricing in the political risk of Italy voluntarily leaving the EU and the euro area.

I cannot link due to a work firewall but if you browse paddypower.com you can place bets on whether Italy will still be in the EU in 2025.

This risk is less pronounced for somewhere like Spain for example.

Leaving the EU would be a net negative for non-resident Italian bondholders who would see their claims re-denominated into the lira nuova.

The same would happen to Italian state pensions. The net wealth effect is less clear here, as the vast majority of Italian pensioners’ spending would be on good and services denominated in lira nuova.

25. April 2017 at 01:40

OT from Nikkei Asian Review today.

April 25, 2017 3:00 pm JST

Soaring house prices turn ‘Australian dream’ into nightmare

Canberra mulls tax changes as young workers are squeezed out of the market

JOHN POWER, Contributing writer

A newly-constructed home is listed as sold on an advertising board in the Sydney suburb town. © Reuters

MELBOURNE — Like many of her peers, Megan Shellie doubts that she will ever be able to buy a home within a reasonable commuting distance of a job in one of the teeming coastal cities that drive Australia’s economy.

Even though she expects to be earning a salary of up to 60,000 Australian dollars ($45,000) after graduating from university in June, the 23-year-old is despondent about a market in which property prices seem increasingly out of reach of average wage-earners.”

—30—

Same thing in Great Britain reports Tyler Cowen. In the 1990s a Brit could buy a house. No more.

Given the deeply embedded system of property zoning in Australia, Great Britain and the U.S., is it not time for a frank discussion of trade deficits and booming house prices?

https://www.newyorkfed.org/medialibrary/media/research/staff_reports/sr541.pdf

The Fed says run a trade deficit and watch house prices explode.

And indeed, when Spain current account trade deficit shrank, house prices moderated.

Tokyo has very affordable housing,they are back to running trade surpluses.

Interesting topic.

25. April 2017 at 03:50

Tokyo has very affordable housing,they are back to running trade surpluses.

Tokyo as an example for affordable housing? Are you kidding?

I don’t see the connection between trade deficits and housing.

In Germany for example people complain about housing prices as well. I assume the problem is mostly zoning and regulation. On the other hand a lot of (if not most) people who are complaining so much about exploding housing prices are also complaining that there is not enough zoning and regulation.

Conclusion: Don’t listen to them, they are just ignorant and stupid.

25. April 2017 at 04:27

Christian, How is it not a market?

SD, I agree, but re-denomination is just a fancy word for “default”.

Ben, How do you propose shrinking the CA deficit? A magic wand?

25. April 2017 at 04:42

http://www.lmfinternational.com/index.php/news/602-insurance-welfare/36920-global-aging-2016-italy-s-pension-reforms-are-mitigating-the-impact-of-aging-but-government-debt-remains-a-hurdle

‘Italy’s social security reform efforts indicate significant progress toward alleviating risks to the long-term sustainability of public finances due to population aging. Yet, we expect that the country’s budgetary outlook will remain challenged, given the modest near-term economic growth outlook and the absence of a resolute reduction in the budget deficit and government debt.’

25. April 2017 at 04:51

Continuing from the same site as above;

—————quote————

According to Eurostat population projections, the old-age dependency ratio in Italy will rise to 52.9% in 2050 from 32.8% in 2015 (see table below; the old-age dependency ratio is the number of people 65 and older divided by the number of those 15 to 64). Even now, Italy has one of the highest old-age dependency ratios in our sample, second only to Japan (43.3% in 2015) and just ahead of Germany (31.8%) and Greece (31.2%). Overall, we project that the total population will grow over the coming decades, but that growth will slow down in the early 2040s, reaching 67 million in 2050. We forecast that the share of working age population in total population will fall to 56.5% by 2050 from the current 64.8%.’

…. We think that, as is currently the case, the bulk of Italy’s age-related spending will go toward pension outlays, followed by health care, representing 14.8% and 6.8% of GDP, respectively, by 2050. However, contrary to the dynamics in pension spending, which we see declining toward the end of the projection period, we expect health-care expenditures to increase at a gradual but moderate pace throughout the period.

These dynamics suggest a gradual deterioration in Italy’s budgetary position in the long term. If unmanaged, the weight of general government spending–including social security–could rise as age-related spending increases, coupled with a rising interest bill as deficits and debt mount. Our analysis suggests that, without further fiscal or structural policy reforms, Italy’s net debt could rise to 138% of GDP by 2050, slightly higher than the sample median, which stands at 134% of GDP. Nevertheless, the respective projected increases in Italy and the 58-country median, indicate that future budgetary challenges emanating from population aging in Italy appear comparatively much less pronounced than for the average sovereign included in our analysis.

———-endquote————–

25. April 2017 at 06:09

I believe that current US Social Security law actually does balance taxes and spending. It would cause a huge uproar, so I’m not saying it’s no issue. But I’m somewhat certain that once the trust fund is empty, benefits are automatically reduced by whatever percentage necessary to match inflows and outflows. Again, I’m just saying that as a technical matter and even on the technical matter I could be mistaken.

25. April 2017 at 08:13

Scott, I’m not saying it’s not a market, in a broader sense everything is a market. But what kind of market is it? The ECB seems to be a huge player in this market, maybe even quasi-government or very similar to it, with relevant interventions, that sometimes look more like open heart surgery. Not to mention they buy private bonds, too. So what do you expect in a market with interventions like this? Distortions maybe?

And what kind of market is this anyhow when it needs interventions like this? It seems to be an insufficent market, an insufficient system, a system that needs something like market monetarism very badly, so that all those interventions are not needed in the first place.

25. April 2017 at 08:45

Christian,

ECB has limits on each bond issuance and they are buying corporate AAA precisely to minimize the distortions. Moreover they are buying up the bonds more or less evenly and credit risk is given by interest rate spreads not by the absolute levels of interest.

And Scott is a bit myopic here, Italian yields are higher because of the upcoming snap-election that may create the real political and geopolitical upset(and the risk there is much bigger than Le Pen was, establishment is polling extremely weak and that’s general elections). Couple months ago you had Italian 10yr at 1.15% Does that mean their debt was more sustainable than US debt? Barely…

25. April 2017 at 12:14

George, You can’t compare Italian and US yields, they are in different currencies. And I am well aware of the Italian elections.

25. April 2017 at 12:31

“George, You can’t compare Italian and US yields, they are in different currencies.”

That’s exactly the point… Though in this case long run inflation differentials are not that big. Anyhow sustainability is about the current and projected primary budget surplus relative to (r-n)*(Total Debt/NGDP). r is the nominal rate of interest and n is NGDP growth rate. Looking solely at the interest rate is misleading, that was my point.

25. April 2017 at 13:46

Just one example from Italy according to German media: Their biggest airline Alitalia. Deep in the red since at least four years, burning one million euros every single day. Today the employees voted down a cost-cutting plan. Why? Because the employees are expecting that the Italian government will save them again, as so many times before, costing Italian (and European) taxpayers just one billion euros so far.

25. April 2017 at 16:03

I like the idea of solving the trade deficit with a magic wand, but I fear it would not work.

Ergo, I hope to open up a discussion on the interrelationship between ubiquitous property zoning, trade deficits and exploding house prices.

The orthodox macroeconomics profession needs to address property zoning as a macroeconomic issue and relate it to the global economy.

25. April 2017 at 16:05

A question that comes to mind is, are 10-year bond yields really a good measure of the expected scope of a fiscal crisis projected to arrive 20-40 years from now?

E.g., here in the USA the long-term debt course is clearly unsustainable (as CBO has been emphasizing for years) but bonds have very low yields as there is no question about the government’s ability to service them for the next 20 years or so. Why should current bond prices reflect events expected to occur only well after the bonds mature?

ISTM these prices much more reflect expected conditions over the next seven years or so than those expected to arrive 25 years from now.

25. April 2017 at 19:36

The US can always meet its obligations because it prints its own currency so 50 year rates would be low too. Italy needs to borrow from the markets, which can demand higher rates since Italy can’t print its currency to meet its obligations. So the market knows the US isn’t revenue constrained while Italy is. That’s why Italy’s rates are higher. Honestly, do we think the US will ever be able to tax and grow enough to meet its current debt? No way, it’s already too big, yet rates are still low. Because there is no risk of non payment.

26. April 2017 at 05:16

George, The countries I compared in the post all used the same currency.

Jim, Lots of people do worry about a eurozone debt crisis within the next 7 years. Remember Greece? So the yield differentials are very meaningful.

26. April 2017 at 08:15

Jim, Lots of people do worry about a eurozone debt crisis within the next 7 years. Remember Greece? So the yield differentials are very meaningful.

Yes, that’s exactly my point. The yields would seem to reflect relative near-term conditions rather more than relative preparedness for the future retirement tsunami.

26. April 2017 at 08:19

The US can always meet its obligations because it prints its own currency so 50 year rates would be low too.

Printing money to carry otherwise unsustainable debt creates inflation. In the late 1970s the government printed money, created inflation, yields on US debt rose into double-digits, and the price of long US Treasuries fell by near half.

26. April 2017 at 09:07

Scott,

like UK and Switzerland. Though they perhaps happened to be there par hasard and were not mentioned in the text, I admit. Still most of Italian premium seems to be related to redenomination risk rather than default risk.

26. April 2017 at 11:34

@George

I think Scott answered your last point already:

Re-denomination is just a fancy word for default.

I agree with Scott that the yield differentials are very meaningful. Still I assume that they are a bit distorted. They might be even bigger without the ECB interventions. I assume Scott might say that’s exactly the point of monetary policy, dummy. So I might say, yes, but maybe Italy’s problems are mostly structural, so maybe the “distortions” are really distortions; a cosmetic surgery that just glosses over the structural problems for a while until the S hits the F.

26. April 2017 at 13:00

George, Christian is right, redenomination is default. Lenders were promised repayment in euros, not worthless lira.

27. April 2017 at 06:47

George, Christian is right, redenomination is default.

In which regard one can note the USA has defaulted on its bonds twice by redenominating them in its own fiat currency substituted for promised gold. The latter instance was FDR, of course. The earlier is an interesting story, ending in the Legal Tender Cases of 1871.

During the Civil War Lincoln ordered the government to print “greenbacks” to pay war costs. His Secretary of the Treasury, Salmon P. Chase, objected that paper fiat money was unconstitutional, as it plainly was in the understanding of the day. Lincoln famously replied “I have the Constitution in my desk” and told him to do it. The war passed and afterwards the US started redeeming maturing pre-war bonds by paying them off with greenbacks. The bondholders objected that they had been promised payment in gold money and the case went to the Supreme Court.

The Chief Justice now was Salmon P. Chase and the Court ruled for the bondholders saying the Constitution required the bonds to be paid off with gold money (Hepburn v. Griswold). On the same day that the decision was announced President Grant appointed two new Justices to the Court who promptly voted to reconsider and then became the swing voters in reversing. Grant succeeded in “packing the court” as FDR only dreamt of, and fiat money became constitutional. Though to his dying day Grant insisted that his making those two appointments was pure coincidence.

The legal side of FDR’s default is important and interesting too, and is hugely neglected. After their encounter with Grant bond investors said “Fool me once…” and US bonds thereafter included explicit terms requiring them to be paid in gold whatever the USA did with its currency. When FDR refused anyhow and the case went to the Supreme Court the Justices were appalled, some writing privately that they would never buy US bonds again.

FDR made clear he was going to steamroll the Court. He wrote a speech (which still exists) telling the public it had to be ignored. With his and the Democrats’ standing in 1933 he would have rolled over it no doubt, the court as we know it would have been destroyed, no more constitutional review of New Deal programs, it would have become like the Supreme Court of Argentina.

Five Justices wrote opinions calling FDR’s act “default”, but Chief Justice Hughes (an astute politician, former Secretary of State and governor or New York) saved the Court by keeping those opinions separate and writing a deciding one that’s been described by scholars as “one of the most baffling ever issued” in which he resorted to the dodge ‘the plaintiffs have a right but no remedy’ in a great number of wordy words. As a result the Court continued to function, ruled FDR’s NRA unconstitutional, when FDR later tried to pack it he was politically weaker and it blew back on him … For the story see:

“The Gold Clause Cases and Constitutional Necessity”

http://scholarship.law.ufl.edu/cgi/viewcontent.cgi?article=1026&context=flr

Of course in 1933 the US had plenty of gold to pay off the bonds. FDR easily could have paid off the bonds by their terms while changing the gold-dollar ratio for other purposes or even going fiat. It was politics. Defaults always are, fiat money or no. (Sorry MMTers.)

This is all a digression, I guess — but there are significant lessons in it about how the Constitution really works, even unto the days of Trump.

FWIW.

28. April 2017 at 19:24

Would Nixon taking the US off the gold standard be a third redenomination? Was there enough gold at that time to continue to back the currency?

28. April 2017 at 19:34

Also, don’t budget deficits cause interest rates to go down, not up? Didn’t Milton Friedman say high interest rates are a sign that money has been too tight, not loose? Don’t budget deficits imply loose money? So wouldn’t expected future budget deficits as discussed in this post imply low interest rates?

29. April 2017 at 07:02

Jim, Thanks, I did not know about that 1871 case.

GV, I don’t think that would count as default, because bonds no longer had a gold clause. Whether it was redenomination is sort of in the eye of the beholder. Gold was much less central to the monetary regime than before 1933.

No, I think deficits are more likely to boost rates, albeit not very much. Yes, deficits tend to rise during recessions, when rates are falling. But I think rates are falling in recessions for reasons other than the deficits.

30. April 2017 at 03:36

Christian, Scott,

So is monetisation a default? BoJ? After all, investors were promised to be paid back in a stable currency, not a worthless currency. I guess that depends on your definition.

Political risk related to leaving the single currency (re-denomination) and thus the EU is not the same as plain default risk. Hence you will read in financial press about re-denomination risk and a default risk. They are not the same since they involve different scenarios and different complementary risks.

Christian has still not explained to us how evenly limited ECB purchases affect the interest rate spreads. Other than proper monetary policy preventing a total collapse of the Eurozone economy and its breakup, which is however not a first round effect. Italy would not be in trouble had ECB done its job properly. That is not to say Italy has no structural issues but the fact is that 20 years prior to the recession Italian productivity was growing almost as fast as German and it was just marginally lower than in Germany. Unemployment used to be lower in Italy than in Germany. Apparently most of the disaster in Italy is a matter of monetary policy which induced uncertainty and political risks.

I would say if Euro survives the Italian elections, it will stay here for decades to come and new members will join. EURUSD will gradually return back to 1.5+ If Italy bugs off, there will be a massive turmoil in Europe, perhaps another global recession and financial crisis.

23. June 2021 at 07:20

Italy is considered a developed country. A nation’s stage of development is determined by a number of factors, including economic prosperity, life expectancy, income equality, and quality of life. As a developed country, Italy is able to provide social services such as public education, health care and law enforcement to its citizens. Citizens of developed countries enjoy a high standard of living and a longer life expectancy than citizens of developing countries. Italy exports around $ 474 billion and imports about $ 435.8 billion each year. 11.1% of the country’s population are unemployed. The total number of unemployed in Italy is 6,581,298. In Italy, 28.7% of the population live below the poverty line. The proportion of citizens living below the poverty line in Italy is relatively high, but this is not a cause for total concern when it comes to investment. Potential financiers should look at other economic indicators, including GDP, rate of urbanization, and currency strength, before making any investment decisions. Government spending on education is 4.3% of GDP. The country’s Gini index is 31.9. Italy is experiencing good equality. The majority of Italian citizens are in a narrow income range, although in some cases there can be significant differences. Italy has a Human Development Index (HDI) of 0.872. Italy has a very high HDI value. This suggests that almost all citizens are able to lead a desirable life thanks to social and economic support; Citizens with a low standard of living receive help and support and have the opportunity to move forward in society. The Global Peace Index (GPI) for Italy is 1.669. Due to the strong presence of law enforcement agencies and the high level of social responsibility, Italy is very safe by international standards. The strength of the Legal Rights Index for Italy is 2. Overall, it is viewed as rather weak – bankruptcy and collateral laws cannot protect the rights of borrowers and lenders in the event of credit-related complications; Credit reports, if any, are rare and inaccessible.