Focus on the target, not the instrument

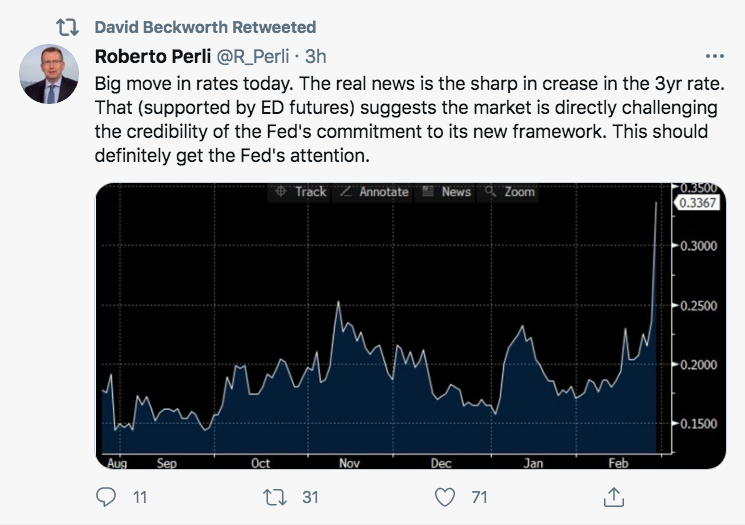

This tweet caught my eye:

While rising three-year yields might represent a lack of commitment on the Fed’s part, rising interest rates are equally consistent with bond market participants now becoming more optimistic about the economy. This might well be good news.

Interest rates are only a means to an end; the only credibility that matters is the Fed’s 2% AIT.

Tags:

25. February 2021 at 16:18

What does the info that all major assets got killed today add to this?

25. February 2021 at 16:46

Both 5 and 10 year inflation expectations are down but 10 more than 5 which are still slightly above target. This could be a believe that the Fed will stick to AIT for a while, but eventually succumb to inflation hawks and return to a policy of undershooting its supposed target.

25. February 2021 at 16:49

Hi Professor,

I have not lived through an inflationary period but have always thought rising rates are consistent with higher growth which in turn would be positive for the market. Now that we finally have some indication of rising rates and a steeper yield curve, the market is throwing a tantrum. At first it was the high multiple stocks but today it spread to most areas of the market.

How do you interpret the situation? I must be missing something.

Regards,

Rodrigo

25. February 2021 at 16:54

Real rates rose a bit more than nominal rates. TIPS spreads aren’t perfect, but if inflation were the primary worry you would expect a difference.

Wouldn’t concerns about deficits/debt better explain this movement?

25. February 2021 at 16:59

Money doesn’t matter anymore.

“As announced on December 17, 2020, the Board’s Statistical Release H.6, “Money Stock Measures,” will recognize savings deposits as a type of transaction account, starting with the publication today. This recognition reflects the Board’s action on April 24, 2020, to remove the regulatory distinction between transaction accounts and savings deposits by deleting the six-per-month transfer limit on savings deposits in Regulation D. This change means that savings deposits have had a similar regulatory definition and the same liquidity characteristics as the transaction accounts reported as “Other checkable deposits” on the H.6 statistical release since the change to Regulation D. Consequently, today’s H.6 statistical release combines release items “Savings deposits” and “Other checkable deposits” retroactively back to May 2020 and includes the resulting sum, reported as “Other liquid deposits,” in the M1 monetary aggregate. This action increases the M1 monetary aggregate significantly while leaving the M2 monetary aggregate unchanged.”

25. February 2021 at 17:00

There is no surer method of destroying America than the policies enacted since Oct. 2008.

25. February 2021 at 17:06

Trent,

For stocks it could be a higher discount rate since real rates rose

25. February 2021 at 20:37

Everyone, Taking the longer view, we’ve seen nominal rates rising for 11 months, along with rising TIPS spreads and rising equity prices.

I would not focus on a single day.

25. February 2021 at 22:31

Scott, your general point is well-taken about such a short data trend, but I have some really good indicators that were reliable in the past indicating we’re probably looking at a fall in the S&P 500 in the 13% range. This would be associated with just a .38% fall in the expected NGDP growth path. The S&P 500 index is very sensitive right now, because the discount rate is so low, a little over 2.5%.

I found a metric in December that has not failed, historically. And yes, it even predicted the Covid-19 crash with almost 3 sigmas, at the end of December. It’s very impressive. Most think the prediction wasn’t there in the markets, but it was oustentatious, if you look at the right data. I believe this data reflects market views of the Fed’s reaction function.

That said, there are some circumstances never before present when making such predictions, such as the new average inflation targeting framework and unusual support being offered to the economy. Also, it is my impression that new monetary policy regimes can tend to have rocky starts, as the Fed learns to communicate regarding forward guidance, etc. This will be interesting.

25. February 2021 at 22:38

I should add that even though we don’t have much of a trend yet, the numbers are indicating tight money, particularly today. Treasury yields fell, stock market sold off, dollar rose in forex markets, inflation expectations are falling, etc.

Prior to today, rates were rising while inflation expectations were falling, and the dollar was slowly strengthening. The dollar is up about .58% YTD, with more than half the rise coming today. Also, the VIX spiked more than 35% and VIX and S&P 500 futures are looking ugly.

25. February 2021 at 22:56

re: “Most think the prediction wasn’t there in the markets”

“Disintermediation is Made in Washington”

26. February 2021 at 01:28

“Everyone, Taking the longer view, . . . “?

‘We’ have ten years?

“ . . . our best estimate is that the net energy

33:33 per barrel available for the global

33:36 economy was about eight percent

33:38 and that in over the next few years it

33:42 will go down to zero percent

33:44 uh best estimate at the moment is that

33:46 actually the

33:47 per average barrel of sweet crude

33:51 uh we had the zero percent around 2022

33:56 but there are ways and means of

33:58 extending that so to be on the safe side

34:00 here on our diagram

34:02 we say that zero percent is definitely

34:05 around 2030 . . .

we

34:43 need net energy from oil and [if] it goes

34:46 down to zero

34:48 uh well we have collapsed not just

34:50 collapse of the oil industry

34:52 we have collapsed globally of the global

34:54 industrial civilization this is what we

34:56 are looking at at the moment . . . “

https://www.youtube.com/watch?v=BxinAu8ORxM&feature=emb_logo

26. February 2021 at 02:45

Meh, Perli has been arguing for almost a year now that the market is not actually expecting higher inflation, the breakeven is just increasing because TIPS liquidity is increasing, reducing the liquidity premium. A sound argument, but increasing inflation swaps suggest he is completely wrong. It’s hard for me to take his views on what the market is doing seriously.

26. February 2021 at 03:40

That tweet made me wince. I *think* David knows it’s probably misguided. I feel his podcast series went downhill after the first 2-3 years and Roberto Perli was a recent guest. Too much about financial plumbing and ad hoc ideas these days. Sometimes it’s better to quite while you’re (still) ahead.

26. February 2021 at 03:42

*quit

Same goes for Friday night drinks. 🙂

26. February 2021 at 09:09

Tacticus, Yes, I agree that inflation expectations are actually rising.

Rajat. David is very polite.

26. February 2021 at 20:28

It has come to the point where one would suspect conspiracy theories with an overriding destabilizing objective.

What Jerome Powell just did was criminal. There is no evidence to back his actions up. In fact, the evidence points the other way.

To say that the future is indeed bleak is an understatement.

27. February 2021 at 07:07

See: New Measures Used to Gauge Money supply WSJ 6/28/83. Neither William Barnett nor Paul Spindt, nor the St. Louis Fed’s technical staff in 2008:

“Although the evidence is mixed, the MSI (monetary services index), overall suggest that monetary policy *WAS ACCOMMODATIVE* before the financial crisis when judged in terms of liquidity;

…use accurate money flow metrics reflecting changes to AD.

All of these economists omit the most important, distributed lag effect of money flows, volume times transactions’ velocity.

See: Fed Points

https://www.newyorkfed.org/aboutthefed/fedpoint/fed49.html

“Following the introduction of NOW accounts nationally in 1981, however, the relationship between M1 growth and measures of economic activity, such as Gross Domestic Product, broke down.

Chairman Jerome Powell just errored:

“This change means that savings deposits have had a similar regulatory definition and the same liquidity characteristics as the “TRANSACTION ACCOUNTS” reported as “Other checkable deposits” on the H.6 statistical release since the change to Regulation D.”

The fact is that bank debits to “other checkable deposits” is a small fraction of the turnover in “TRANSACTION ACCOUNTS” i.e., in “total checkable deposits”.

Using this perverted rationale, Chairman Jerome Powell lumped savings deposits with transaction deposits. So, M1 now is the equivalent of M2.

No money stock figure standing alone is adequate as a guide-post for monetary policy.

WSJ 6/28/1983: “The experimental measures are designed to resolve some of the confusion by isolating money intended for spending, from the money held as savings. The distinction is important because only money that is spent-so-called “true money” – influences prices and inflation”

Now, you can’t isolate our means-of-payment money nor use the distributed lag effect to monitor money flows.

27. February 2021 at 09:47

Did the Fed ever indicate a starting point for its AIT? I am probably mistaken, but it seems like they left that vague. A vague start date will mean that the overshooting they start to achieve in 2021 or 2022 will still average 2% for awhile even if the overshooting goes on for a couple of years (using up the undershooting for the prior decade).

28. February 2021 at 06:05

G.6 Debits and Deposit Turnover at Commercial Banks (stlouisfed.org)

August 22, 1996 release

https://fraser.stlouisfed.org/files/docs/releases/g6comm/g6_19960822.pdf

Annual Rate of Deposit Turnover

15 years after the widespread introduction of “other checkable deposits”, the ratio of demand deposit turnover to “other checkable deposits” was 14.5/513.6 or 0.028232 percent

28. February 2021 at 06:52

I FED-exd my forecast for AAA corporate bonds to James Sinclair (whose father started the OTC stock market) who now publishes “MineSet” in 1981. With the introduction of NOW SuperNOW and MMDA accounts, the regulatory release of savings propelled N-gNp to 19.2% in the 1st qtr 1981, the FFR to 22%, and AAA Corporates to 15.49%.

My prediction for AAA corporate yields for 1981 was 15.48%.

I used both the “arrow of time” and the >100 year-old “distributed lag effect” of money flows.

You see, Dr. William Barnett’s “Divisia Monetary Aggregates” (The User Cost of Money), is a conterminous application without an economic projection.

Neither does: Anderson, Richard G. and Barry E. Jones, “A Comprehensive Revision of the Monetary Services (Divisia) Indexes for the United States”, Federal Reserve Bank of St. Louis Review, September/October 2011, pp. 325-359.

As [Friedman and Schwartz, (1970, pp. 151—152)] said:

“This [simple summation] procedure is a very special case of the more general approach. In brief, the general approach consists of regarding each asset as a joint product having different degrees of ‘moneyness,’ and defining the quantity of money as the weighted sum of the aggregated value of all assets, the weights for individual assets varying from zero to unity with a weight of unity assigned to that asset or assets regarded as having the largest quantity of ‘moneyness’ per dollar of aggregate value. The procedure we have followed implies that all weights are either zero or unity. The more general approach has been suggested frequently but experimented with only occasionally. We conjecture that this approach deserves and will get much more attention than it has so far received.”

28. February 2021 at 07:03

As much, and as long as it takes.

The yield curve is steepening (the interest rate differential in yields between the long-end segment of the Treasury curve and the short-end segment of the Treasury curve is widening).

But some like it hot, as nominal Treasury yields remain below inflation expectations (so what’s up with the forecasts?) — all before the next stimulus. I.e., N-gDp targeting is still in a sweet spot.

10 yr TIPs @ -.60%

10 yr breakevens @ 2.15%

10 yr Treasuries @ 1.54%

28. February 2021 at 10:27

Bill, I seem to recall that one Fed President (Evans?) indicated the beginning of 2020, which was also my assumption.

28. February 2021 at 18:00

Tacticus,

Ultimately, it may not matter that inflation expectations have been rising, because even under average inflation targeting, I suspect the Fed will kill growth more than necessary to fight above target inflation. I’ll believe that, until they prove otherwise. As Scott has pointed out previously, and as Larry Summers recently observed, the Fed has never engineered a soft landing. While average inflation targeting may help, it won’t help enough.

Also, market reactions last week seem to indicate the market is now expecting the disinflation that comes with the Fed’s heavy hand.

1. March 2021 at 06:54

re: “the Fed has never engineered a soft landing”

It is impossible to engineer a “soft landing” given the fact that the FED’s technical staff doesn’t know the difference between money and liquid assets.

1. March 2021 at 07:07

People don’t seem to be able to separate the wheat from the shaft. If inflation is nearly as quiescent as during Japan’s bubble between the period 1986 and 1991 (as is likely as demonstrated by breakevens’), then we will duplicate their experience of overinflating stocks and real estate in the next 5 years.

1. March 2021 at 07:46

The year-ahead implicit NGDP forecast is about as strong as it has been post-2008. The 5-year TIPS breakeven is 2.3%. Maybe something going on w/ TIPS liquidity premiums, but S&P500, copper, oil, and Dollar Index all point in higher-NGDP growth directions.

Does anyone really think the Fed will endure a blistering, average of 2.3% CPIU for five years? Apparently the Market does. Usually it’s smart to defer to the market.

I understand the FOMC is now conceptually open to making up for undershoots in their inflation target, but if you get even two quarters of 2%+ CPIU, the chorus of knaves howling about the one thing they know how to howl about (small changes in measured inflation) will be deafening. Do we really think, after all these years of disappointment, that the FOMC will run a balanced monetary policy for years? I’d believe 1.8% CPIU, but not 2.3% for *5 years*, it’s impossible.