Fiscal austerity and growth in national income

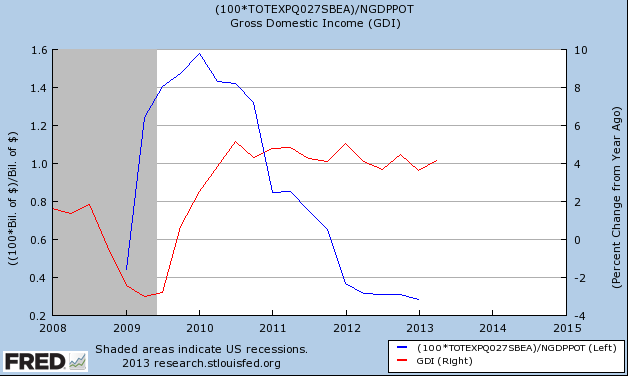

This post will rely entirely on some interesting graphs that Michael Darda sent me. The first shows spending on the original stimulus program (as a share of GDP), which Michael got from a recent Paul Krugman post. Then Michael added the growth rate in nominal gross domestic income (which is one of the two ways that the government uses to estimate NGDP):

Michael noted that despite the most “intense fiscal consolidation since the Korean War demobilization”, NGDI kept pugging along at a stable 4% per year.

I can think of two ways in which this is not quite as bad for the Keynesians as it seems, but also two arguments that cut the other direction. Here is Paul Krugman:

So next time someone goes on about how we had this huge stimulus that failed, you can tell him that the “huge” stimulus “” in response to the worst financial crisis in three generations “” peaked at a whopping 1.6 percent of GDP, and was effectively gone in a bit over two years.

This sounds plausible, but raises another uncomfortable truth. The actual stimulus was somewhere around $780 billion and the devout Keynesians said something like $1.3 trillion was needed. But if a stimulus of $780 billion did almost nothing, it’s hard to see how stimulus that was less than 1.7 times larger would have made a big difference. In other words, the argument Krugman used for fiscal stimulus, that monetary stimulus was politically impossible, also seems to apply to the sort of fiscal stimulus that would have been required to make a decisive difference.

On the other hand I’d argue that while the needed monetary stimulus seems to be politically infeasible at the moment, that’s only because QE is the only option on the table. In the long run it might be easier to convince the consensus of economists that a truly powerful fiscal monetary stimulus (say level targeting rather than QE) is the way to go. I think it would be far harder to convince policymakers that a (say) $3 trillion stimulus was the way to go. But that’s obviously a judgment call.

The other argument that Keynesians could use is that NGDP growth has tailed off a bit more than NGDI, to around 3.2%. I’ve seen papers that suggest NGDI is more accurate in the short run, and the NGDI data far more closely matches other data we have such as monthly employment numbers, but it’s at least possible that the NGDP numbers are more accurate. Even so, that’s a very modest slowdown. Especially when you consider the next factor.

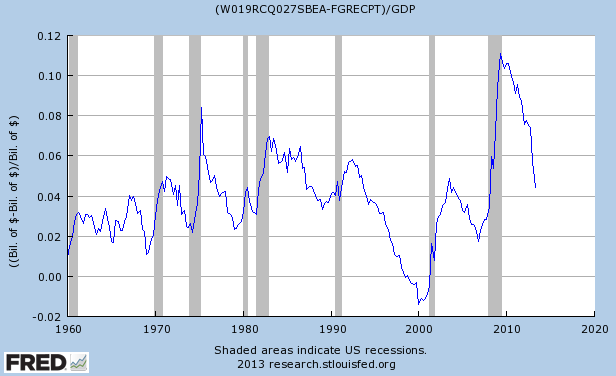

Cutting against the Keynesian argument is that the Krugman graph used by Darda actually understates the amount of recent austerity. I noticed this when I saw the blue line level off since early 2012, despite a strong shift toward austerity in 2013. The problem is that (AFAIK) the income tax increases, payroll tax increases, and sequester, were not part of the ARRA. So let’s look at the budget deficit (again as a share of GDP and again provided by Darda):

Note the sharp plunge toward austerity in 2013, which doesn’t show up in the ARRA graph. The deficit fell almost immediately from over 7% to less than 4.5% of GDP.

Yes, you’d really like the cyclically adjusted deficit, but seriously, GDP growth has been fairly slow in recent quarters, surely the adjusted deficit would also be falling sharply in 2013. So the austerity shown in Krugman’s graph, already the steepest since the 1950s, was much steeper by this measure. I’m sure some of my commenters can come up with better estimates here, and I’ll add updates as they do so.

Happy Labor Day! The 5th straight Labor Day with plus 7% unemployment.

PS. David Beckworth has a good post on this as well.

PPS. Another argument used by Keynesians is that S&L spending is rising. But the revised Q2 GDP data shows S&L spending down again.

Tags:

2. September 2013 at 07:08

Re: “a truly powerful fiscal stimulus (say level targeting rather than QE)”

Should “fiscal” have been “monetary”?

2. September 2013 at 07:48

The CBO anticipated this a year ago and forecast GDP declining at a 2.9% annual rate in the first half of 2013, leading unemployment to rise above 9 percent near the end of the year. The CBO referred to the 1990/1991 recession for comparison. The projected deficit of $641 billion is almost the same as the current $642 billion projection by the CBO (at least I still think it is current, maybe there is a more recent update).

So in my mind, Keynesians already approached this topic and anticipated a run of the mill recession. That failed prediction and the fact we didn’t get even so much as a blip in the jobless claim or payroll job numbers puts a stake through the heart of the vampire of Keynesian multipliers.

I’ve brought this up to Keynesians and the best they have to offer me is that real GDP was on the verge of rising 6% in the first half of 2013 and that surge was killed by austerity. Others (incredibly, and without facts to back it up) say the deficit fell so much because the economy is so strong, not because of austerity.

–“CBO’s economic projections for next year are heavily influenced by the fiscal policy specified by current law. As discussed in detail in Chapter 1, significant fiscal tighten- ing resulting from a combination of tax increases and spending cuts is set to begin to take effect in January. If that tightening occurs, output will decline in the first half estimates, the deficit in fiscal year 2013 will come to $641 billion, $487 billion less than the shortfall in 2012.7 A major factor in that difference is the recent or impend- ing expiration of many of the temporary changes in tax and spending policies that have been enacted or extended during the past few years. Some new policies that would reduce the budget deficit also are scheduled to take effect in January (see Box 2-1). Altogether, under current law, the reduction in the deficit between 2012 and 2013 will be the largest (measured as a share of GDP) since 1969.

Reflecting that sudden and sizable fiscal tightening, CBO projects that real GDP will contract by 0.5 percent in 2013 after growing by 2.1 percent in 2012 (as measured by the change from the fourth quarter of the previous year; see Table 2-1). Real GDP is projected to fall at an annual rate of 2.9 percent in the first half of next year and then to rise at an annual rate of 1.9 percent in the second half. In light of the way it has identified past recessions, the National Bureau of Economic Research would probably view such a contraction in output in the first half of 2013 as a recession (similar in magnitude to the recession in the early 1990s).

The contraction of the economy will cause employment to fall and the unemployment rate to rise to 9.1 percent in the fourth quarter of 2013, CBO projects (see Figure 2-7 on page 36).”–

CBO August 2012 Deficit Projection

http://www.cbo.gov/sites/default/files/cbofiles/attachments/08-22-2012-Update_to_Outlook.pdf

Current Deficit Outlook

http://www.cbo.gov/publication/44172

2. September 2013 at 08:16

Justin Dailey,

The idea that US RGDP would grow by 6% in 2013 beggars all belief.

2. September 2013 at 09:26

It does beggar belief doesn’t it? Yet it’s really the only option which is consistent both with the data and large Keynesian multipliers.

2. September 2013 at 09:56

Thanks Daniel.

Justin, And of course if the counterfactual is 6% RGDP growth, then that completely discredits their claim that eurozone austerity caused the double dip recession. After all, what’s the eurozone counterfactual, give the ECB was tightening monetary policy in 2011?

2. September 2013 at 11:22

In the ongoing Keynesian/Monetarist conversation I note that Keynesians think that stimulus was too small (and given that cut back in spending at the state level that does seem credible to me). The monetarists think that the FED hasn’t done enough, even though they are doing things they never have done before. I note that Krugman thinks that more FED actions can’t hurt and might help, but most monetarists appear to think stimulus is wasted. I don’t see this argument being settled any time soon, but given the harm caused by the great recession I wish both the stimulus had been larger in infrastructure spending (since that puts people to work and we could use better infrastructure anyway) and that the FED had used 2% inflation as a real target and not an upper bound.

I took a macroeconomics course 30 years ago after getting an engineering degree. Much of the course was devoted to studying graphs where there were no numerical units on either axis, the independent variable was not clearly implied, the shape of the curve was normally assumed to be linear (without any apparent justification), the slope of the curves were resolvable only into one of four states (positive, negative, vertical, or horizontal), and great import was given to shifting curves even though the actual shape of the curve was simply assumed. The data that these curves purported to plot were never actually available in real time and were subjected to large revisions months and even years after the fact. I came away from the course thinking that macroeconomics was pretty useless for making adjustments in the short term (anything less than six months) and might not be very useful in the longer term also. Scott Summer and Matthew Yglesias might think that the central banks can maneuver like a humming bird, but they only know where they are flying with a large degree of uncertainty. Nominal interest rates/bond prices are known in real time but how well do we know the current path of NGDP?

The other tenet of economics that I always found questionable was the assumption of rationality of individuals and groups. Daniel Kahneman and his compatriots have chipped away at individual rationality, but I think the irrationality of groups is still under appreciated. Some in the Chicago school of economists seem to be unable to admit that some human behavior is irrational, i.e. there is no such thing as bubbles. They look at behavior that was akin to lemmings rushing over a cliff and conclude that the underlying rationality was just not apparent.

A futures market in NGDP might make better predictions than a committee of bankers, but still might occasionally run away to irrational exuberance or pessimism.

2. September 2013 at 12:42

Percent change from a year ago performs an annual smoothing on GDI that is suspect over a perturbation that only lasts 2 years.

If you look at the derivative of a log fit (continuously compounded rate of change), you see the drop in GDI was localized to 2008-2009 so that it looks like the plunge was halted by stimulus. Of course monetary stimulus was happening at the same time. Again the empirical data is inconclusive and argument devolves to getting the null hypothesis to be ones position.

2. September 2013 at 12:43

“A futures market in NGDP might make better predictions than a committee of bankers, but still might occasionally run away to irrational exuberance or pessimism.”

True,(the EMH isn’t the PMH, the Perfect Markets Hypothesis) but markets adapt to new information much faster than governments or quasi governmental institutions, and thus self-correct much quicker. Governments are truly awful in this regard

2. September 2013 at 14:35

JAS, Sounds like you had a bad professor. As far as the EMH, not one person in 1,000,000 understands what the world would look like if the EMH were true. So don’t jump to conclusions.

Yes, NGDP targeting is not perfect, just better than the alternatives.

Jason, The big mistake the Keynesians made was making predictions about austerity. Remember when they assured us that the eurozone austerity caused the double dip recession? And that anyone who believed otherwise was a fool who believed in zombie economics? Those assurances don’t look so good today.

2. September 2013 at 15:06

Hey Scott,

If government employment hadn’t been cut by 1 million in the past three years, unemployment would be below 7% now, wouldn’t it?

I’ll take the world we live in, thanks.

2. September 2013 at 15:39

“I think it would be far harder to convince policymakers that a (say) $3 trillion stimulus was the way to go.”

Well, if the $3 tril is for boondoggle gov’t cash to Dem Party Donors for silly projects like Solyndra, ya, tough sell.

But if it was for tax cuts, which Reps say they want, I’m sure any Dem pres. could come up with as much fiscal tax cut stimulus as needed.

“Fiscal stimulus” can be either terrible gov’t spending or very helpful tax cuts (like Bush did! Good job Bush).

Scott, you often talk about tight/loose monetary policy, noting that interest rates don’t show it the policy.

What about bank lending? where are the graphs on how much banks are lending to consumers, to businesses? I claim tight money means less lending, loose money means lots of lending. But macroecon bloggers don’t follow lending. Why not?

3. September 2013 at 05:26

Brian, No, I doubt unemployment would be below 7%.

Tom, Lending has nothing to do with monetary policy. Don’t confuse tight credit with tight money.

3. September 2013 at 05:56

Scott, what’s behind the doubting? Looking at y/y or seasonally-adjusted numbers, the cut in government jobs is more like 750K since July 2008 (which also removes the census blip.)

If governments hired these 750K people tomorrow, isn’t the impact on unemployment pretty straightforward? I get something like 6.8%.

Careful what you wish for, or lament.

3. September 2013 at 08:20

The problem is stimulus became the new budget benchmark. Stimulus never ended, austerity never began.

2013 United States federal budget – $3.8 trillion

2012 United States federal budget – $3.7 trillion

2011 United States federal budget – $3.8 trillion

2010 United States federal budget – $3.6 trillion

2009 United States federal budget – $3.1 trillion

Also, proportion of GDP is probably the wrong measure, governments spend specific absolute dollars for specific reasons, most of which have relatively little to do with overall GDP. Absolute total government expenditures per capita are generally considerably higher in U.S. states than European countries, and much higher than here even as recently as the 1990s. Not very “austere.”

3. September 2013 at 12:53

Brian, Monetary offset.

3. September 2013 at 13:53

Scott, thanks for sticking with me on this one. I thought it’d come down to your trademark laconic snark. Well played sir.

For my own edification, you are saying that more government workers would have meant more fiscal stimulus, which would have meant less monetary accommodation, which would have meant slower private-sector growth, which would have meant a similar total jobs number today. Is that it?

Perhaps.

Where would government employment be today if we had strong NGDP growth in 2008-2009? My gut says 500,000-750,000 higher than it is – this number only goes down during serious crises.

4. September 2013 at 14:30

Brian, Yes, we’d have more private sector jobs and more public sector jobs.