Don’t bet against the Danes

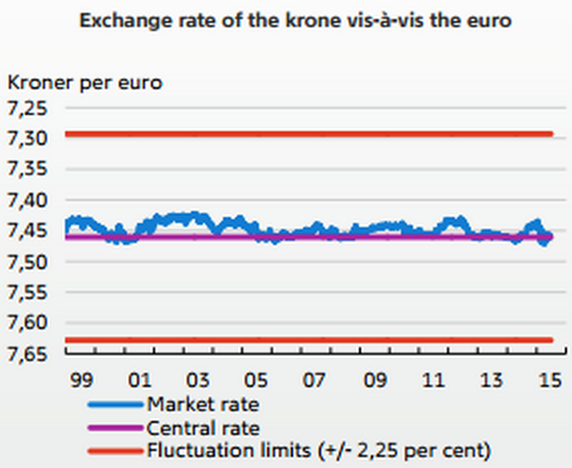

One of the important tenets of market monetarism is that countries with their own currency can can control their nominal exchange rate. This means there is no such things as a “liquidity trap”; a country can simply depreciate its currency if it wishes to create inflation. Switzerland did this in 2011 and held the exchange rate at a depressed level for more than three years. But then the Swiss National Bank let the currency float higher, for reasons that still are not entirely clear. Some argued that they didn’t want to buy up so much foreign exchange, and that this somehow discredited the claim that a central bank could always depress its currency.

I doubted that explanation; the financial markets certainly didn’t see any reason why the Swiss would need to abandon the euro peg. Fortunately, another test case occurred at about the same time, in Denmark. Speculators bought lots of Danish krone and the central back was forced to buy lots of foreign assets to defend the currency. Here’s the FT from 5 months ago.

Denmark’s central bank governor pledged to face down speculators testing its currency peg to the euro, saying he would do “whatever it takes” to defend it.

Lars Rohde told the Financial Times that Nationalbank could “go on forever” defending the peg, after lowering interest rates four times in three weeks to a global record low of minus 0.75 per cent. It has also swelled its balance sheet to a record size by printing krone in an attempt to weaken the Danish currency.

“The main message is that we are ready to do whatever it takes to defend the peg. We have unlimited access to Danish krone and we have no restrictions on our balance sheet,” he said, in his first public comments since the recent quadruple rate cuts.

Tyler Cowen claimed this would provide a test of the claim that the Swiss were not forced to devalue:

I would bet against them, in any case this will be a neat test case for our judgments of Switzerland.

It’s not 100% clear what the test actually was. No one expected the Swiss to maintain their euro peg forever; it was always viewed as a temporary expedient. More likely, the test was whether the currency peg would be abandoned because of a wave of speculation anticipating a currency appreciation. If that’s the test, the Danes seemed to have passed:

It looks like the pressure is off, for now at least.

At the start of this year, it looked a bit like Denmark could be the new Switzerland, with some observers wondering whether the tiny Nordic nation could scrap its currency peg to the slumping euro.

Pressure ramped up quickly after the Swiss central bank nixed its cap on the franc, prompting a series of Danish interest rate cuts, writes Katie Martin.

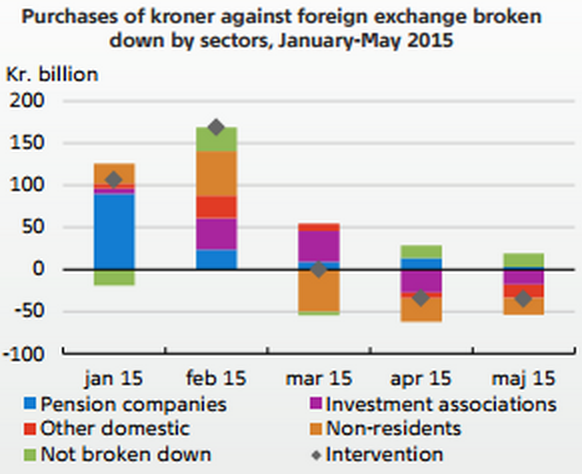

In its latest monetary review, Denmark’s central bank acknowledges that the market’s krone buying was enthusiastic in the opening months of the year.

The central bank is still intervening to lean against krone-positive flows. But it’s all on a much smaller scale.

It’s still not clear exactly why the SNB abandoned the peg (they gave mixed signals.) But if they left under “pressure” from speculators, it now looks like they made a serious mistake. It’s smooth sailing in Denmark:

And I might add that they defended their currency peg with strongly negative interest rates on reserves, an idea that was dismissed as impractical when I proposed it in early 2009. Some even claimed the policy would be contractionary. OK, so how has the krone not appreciated if negative IOR is contractionary? And why did the Swedish currency recently depreciate on news that IOR was being made even more negative?

Tags:

4. July 2015 at 07:14

Still, something strikes me as off about the actions of central banks—Denmark, Switzerland— trying to lower the value of their currencies by buying bonds or assets of other currencies.

The SNB was worried about taking losses on its portfolio, although the portfolio was acquired by running a printing press (not even, actually just digitizing money out of thin air). There was even talk that Swiss taxpayers would have to pay higher taxes to compensate for porfolio losses at the SNB!

Seems to me that both the Nationalbank and the SNB could have benefited their economies and populations a lot better by monetizing tax revenues. In other words, grant a tax holiday to businesses, and print up (digitize) the money to replace the lost revenues.

This would benefit the domestic economy and surely would depreciate the currency eventually. There would be no threat of central bank portfolio depreciation (although I still cannot agree with the idea that one can take a loss on a portfolio that has been acquired by printing money. This strikes me as an accounting concept only demented central bankers could contrive).

The Danes and the Swiss could have had a year or two in Fat City. Now what have they got?

4. July 2015 at 07:23

Sumner: “The Danes and the Swiss could have had a year or two in Fat City. ” – as MF would say, why stop at printing money for a year or two? Why not go the whole hog and print money for a couple of decades, or forever? Don’t you want prosperity to last more than a year or two? Ergo, via reductio ad absurdum, your argument is absurd.

4. July 2015 at 07:25

@myself – sorry, the quote was by the Sumner minion B. Cole. Frick and Frack.

4. July 2015 at 07:39

It’s the invasion of the Chinese property snatchers;

http://www.japantimes.co.jp/news/2015/07/03/business/salarymen-sidelined-chinese-descend-japan-property-market/#.VZf9e1Je271

———–quote————

Realty agencies in Beijing are organizing twice-monthly tours to Tokyo and Osaka, where 40 Chinese at a time come for three-day property-shopping trips, seeking safe places to invest their cash abroad. They’re being prompted by the yen’s decline to 22-year lows and excitement over the 2020 Tokyo Olympics driving up prices, as they did in Beijing in 2008. Property tours will soon start from Shanghai too.

Partly as a result of nascent Chinese buying, Tokyo apartment prices have reached their highest levels since the early 1990s, up 11 percent over two years, according to the Real Estate Economic Institute Co.

“The demand is like water exploding up from a well,” said Zhou Yinan, an Osaka-based agent at Chinese brokerage SouFun Holdings Ltd., who said his mainland buyers are about 20 percent more numerous than at this time last year. “The Chinese buyers had mainly been from Taiwan until last year, but that trend reversed since October as the yen weakened against the yuan.”

————endquote———-

4. July 2015 at 07:44

Seems it’s sort of an independence day for Puerto Rico, the Governor wants to be independent of the debt;

http://panampost.com/belen-marty/2015/07/03/treasurer-admits-puerto-rico-can-pay-debts-doesnt-want-to/

———-quote———

Carlos Colón de Armas, an economist and MBA finance professor at the University of Puerto Rico, explains that contrary to what [Governor]Padilla has said, “the public debt is easily payable.”

The best evidence of this, the economist says, is the payment the Puerto Rico Electric Power Authority made on Wednesday to its creditors: “the government made the payment that was due without any problem.”

The professor argues that the government is tight on cash, and cannot meet its debt obligations while simultaneously keeping up with the rate of spending it has always enjoyed: “what is required is that the government reduce its spending.”

“The problem is that reducing spending generates political problems,” Colón de Armas explains, “which the government does not want to incur. So they are making the mistake of seeking financial relief for the debt, when they should be looking at their expenses.”

———–endquote———-

4. July 2015 at 10:22

“It´s no use having an escape hatch if you act stupid once you´re out”

https://thefaintofheart.wordpress.com/2015/02/08/its-no-good-having-an-escape-hatch-if-you-act-stupid-once-youre-out/

4. July 2015 at 17:26

Ray Lopez: Actually, I believe in a silver-diamond standard. The Swiss National Bank should produce a large coin, made up of platinum, palladium, silver, tungsten, nickel, and aluminum. Embedded in the middle of the coin should be a diamond. To suggest regal value, the coin should be the size of a softball, though preferably flat and disc-like, and not bulging as if it were a small flying saucer. The imagery on the coin should connote massive strength and permanence, such as engravio of the Rock of Gibraltar or the USS New Jersey.

Once the Swiss converted their money supply to these new silver-diamond coins, I am sure they would obtain the benefits of zero inflation and high living standards. To those that say the Swiss have already obtained those standards, I say they would be even higher and they would drive a lot of psychic income from their new silver-diamond standard monetary system.

Imagine the petty green envy of the French, or Latvians, or the shrimpy Danes, with their pathetic little paper money, when confronted with the new Swiss coin.

5. July 2015 at 01:48

Benjamin Cole: brilliant. With a fixed monetary base of what, five or six coins, three of which are on display in museums in foreign capitals, I wonder what a loaf of bread would cost?

5. July 2015 at 03:49

Blue Eyes–Hmm. I hadn’t considered practical, temporal concerns. I was devising a regal, noninflationary monetary system. I thought by creating a powerful silver-colored coin, we could answer the atavistic auriferous genuflections of Ray Lopez.

Back to the drawing board?

5. July 2015 at 05:05

Everything has its limit. The declaration that the Danes are victors seems a little premature.

5. July 2015 at 05:16

Dax, I did not really declare them “victors” for all time, all economies fail in the long run. I said they had survived a crisis that some people thought they would not survive. Yes, the next crisis might knock them off. But that’s not the test I was considering.

Here’s another way of considering the question. Suppose Denmark had devalued. Tyler would quite rightly have claimed he was right. But they didn’t devalue. So that means he was . . . ?

Are there tests where one can be right, but never wrong? Yes, if you predict country X eventually has problems. But the value of that test would be precisely zero. The only tests that have VALUE are those that allow for one to be right or wrong.

Heres’s an analogy. Suppose you say “X is a bubble, by which I mean the price of X will eventually fall.” That test is sure to be confirmed as true, as all asset prices eventually fall. But it’s also a claim that has no value.

5. July 2015 at 06:37

@B. Cole – fixed money supply? They did that already, Google Bitcoin. The Winklevoss brothers even think it’s the Next Big Thing, though I personally think there are technical problems involving the blockchain that preclude it from being widely adopted. Back to the drawing board? Yes, with the tried and true gold coin standard.

5. July 2015 at 08:28

No way Ray: About 1000 years before gold was coined, silver was. The Chinese word for bank was and is “silver house.”

Gold is a vulgar, gaudy metal fit for bubbles and painted strumpets. The color silver is regal, and has a long lineage as a coin. A serious metal.

Diamonds are forever. A diamond-studded silver palladium platinum coin is obviously the way to go and our money supply should be based on that. The metals nickel and tungsten, when added to the large coins, add great strength, symbolic of the imposing power of a banking system based on silver-colored coinage with diamond studs.

Gold is a soft, mushy metal, sought by bought women and shallow men.

5. July 2015 at 09:59

Benjamin Cole wrote:

“Gold is a vulgar, gaudy metal fit for bubbles and painted strumpets.”

Whatever Mr. My Preferred Currency Requires Initiations and Threats of Violence In Order For It To Circulate, Whereas Gold Is Hoarded By The Very Legalized Counterfeiters Who Issue That Currency.

Fiat money has been in a bubble since its inception. It is one gigantic malinvestment that would not have become the generally accepted medium of exchange by voluntary production and exchange of private property.

Fiat money is an ancient, barbaric, immoral, socially destructive socialist system of exploitation imposed by the likes of Ghengis Khan, and other war mongers since antiquity.

Gold was not in a bubble. The dollar was in a crash.

Market forces are constantly working to expunge the supply of exchanges fiat notes and digital bytes down to zero. It is why perpetual violence against free markets is required to prevent people from doing so in accordance with what actually serves them best as a store of value and medium of exchange.

Fiat currency is virtually worthless in a free market. Tyrants, thugs, they love it because it enables them to finance what people would otherwise not let them finance even by theft.

5. July 2015 at 10:13

Benjamin and Blue Eyes are so ridiculously shallow in their critical thinking skills that they don’t even understand how a free market tends to, you know, innovate goods and services.

Apparently, if we were living in the USSR circa 1920, and someone dared suggest that maybe individuals should be free of coercion in car production and exchange, the these misguided people will guffaw and say “What, you want people to drive Model T’s for the next trillion years? No matter how far people in the future want to travel?”

You know, because a free market process never results in any changes to cars.

Ergo, the Utopian socialist logic dictates that because the socialists are too dimwitted to be able to think creatively in innovating money production and exchange, it follows ipso facto that there objectively is no way to innovate, and so the choice to be imposed on everyone by thugs with guns, is the state’s cars only, and anyone who dares question it, must be some kooky supporter of the doctrine of “Model T 4ever”.

I notice a pattern in the socialist mindset whenever they are confronted with a free market in whatever they believe has to be coercively monopolized by a state: Their creativity no only disappears, but we have to read their warped visions of what will allegedly result, permanently, with millions of other people trying and testing and competing in producing a medium of exchange.

It is an ideology of rigidity, stagnation, death.

5. July 2015 at 10:43

I don’t need to, nor would I want to, use such horrible logic as Blue Eyes is using, by saying:

“With a flexible monetary base of what, five or six percent growth, I wonder what a loaf of bread would cost in 100 years? I would have no idea how to move the decimal place over. I mean, does it make sense for people to buy a loaf of bread for anything lowee than 486,255,999 freedom bucks? What? 0.486255999 freedom bucks? I don’t get it!”

Hahaha

5. July 2015 at 10:52

Benjamin using the terms “atavistic” and “genuflect” is a case of psychological projection.

State imposed money devaluation, such as what Roman emperor Diocletian, circa 300AD, made law, is certainly atavistic.

Calling upon the rest of society to live under state imposed monopolists of currency, the overlord central banks, whom we are all to trust and obey (as long as the overlords trust and obey the true representatives of money, the MMs) is certainly a genuflection.

That is another tendency in socialist circles: A chronic inability to engage in even the most rudimentary of self-reflection and internal consistency checking. The cult is rife with performance contradictions.

5. July 2015 at 11:26

Snork.

5. July 2015 at 17:58

Good post, Scott!

6. July 2015 at 00:20

Fair enough. If Denmark is able to reduce the assets it has bought to pre-January 2015 levels, then you can declare victory. But not until. The reason why can be seen in the Swiss case. the SNB bought lots and lots of assets to defend the peg at 1.20. Then the swiss franc fell to 1.23 and 1.24 and people were doing victory celebrations, but the swiss were never able to sell any of their accumulated assets. So the next time the exchange rate went to 1.20, they had to buy even more, and the asset stock went up.

6. July 2015 at 04:18

Dax, so the Swiss and Danes were able to convert presses of a computer button into tangible assets, and you say that is a bad thing? Would you be less worried if they had bought gold or oil or London real estate?

6. July 2015 at 05:24

Dax, You have it exactly backwards. In the long run the Swiss will have to buy even more assets because they exited than if they’d stayed with the peg. Before the peg was adopted in 2011, the SNB was having to buy massive quantities of assets. After the peg their purchases the dropped off sharply.

There’s one point that I find that many economists overlook. The ratio of base money to GDP is negatively correlated with the average inflation rate. By revaluing they reduce the average inflation rate in Switzerland, making SFs more attractive, and in the long run this raises the ratio of base money to GDP. It’s monetary policy 101, but is overlooked by a lot of economists who should know better (including Paul Krugman.)

BTW, I suspect the markets also understand that in a emergency the Danes could always adopt the euro, and avoid any capital losses. That’s one reason Danish policy has more credibility than Swiss policy.

7. July 2015 at 05:23

[…] In this post Scott Sumner says it’s been “smooth sailing” for the Danes, who aren’t […]

7. July 2015 at 05:25

I’m not saying it proves Scott wrong, but FYI if my limited research skills haven’t failed me, the Danish central bank’s assets are up 50% year-over-year amidst this “smooth sailing.”

7. July 2015 at 09:17

Interesting, slightly tangential thought on negative IOR: Doesn’t the experience of the Dansmark Nationalbank during the recent recession contradict much of Cochrane (2014)?

Cochrane’s thesis is that “interest on reserves, together with the spread of interest-paying electronic money, radically changes just about everything in conventional monetary policy analysis.” The reason why this is false is because holding reserves already carries a litany of costs: the opportunity cost of investing in interest-bearing assets, balance sheet costs, inventory costs, and risk of theft or destruction. With respect to all these associated implicit costs, it wouldn’t seem that alleviating these costs by 25 basis points would radically change monetary policy.

The Danish experience is another data point that contradicts this idea, along with Japan, which faced deflation and near-zero interest rates during the 90s, but did not pay interest on reserves until 2008.

Whether Fisherian effects can explain some policy movements even in a liquidity trap, that’s another story. But I’m not sure IOR is the straw that breaks the camel’s back.

8. July 2015 at 06:24

Bob, You said:

“I’m not saying it proves Scott wrong”

That’s an understatement, it’s 100% consistent with my argument.

Daniel, As I recall his point was that QE no longer works with IOR. Is that right? If so then I agree with you. Recent events show that QE is still effective when there is IOR.