Communication breakdown

The Fed announced a new policy of Flexible Average Inflation Targeting back in August 2020. Over the next few months, the Fed failed to provide a clear and consistent interpretation of what the policy actually entails. More recently, it has become clear that FAIT is intended to be asymmetric. But some features of the policy remain unclear, such as when it began.

Jerome Powell gave a speech explaining the new policy in August 2020, and this is naturally the place to look for an official explanation. But Powell’s explanation is vague and unclear:

We have also made important changes with regard to the price-stability side of our mandate. Our longer-run goal continues to be an inflation rate of 2 percent. Our statement emphasizes that our actions to achieve both sides of our dual mandate will be most effective if longer-term inflation expectations remain well anchored at 2 percent. However, if inflation runs below 2 percent following economic downturns but never moves above 2 percent even when the economy is strong, then, over time, inflation will average less than 2 percent. Households and businesses will come to expect this result, meaning that inflation expectations would tend to move below our inflation goal and pull realized inflation down. To prevent this outcome and the adverse dynamics that could ensue, our new statement indicates that we will seek to achieve inflation that averages 2 percent over time. Therefore, following periods when inflation has been running below 2 percent, appropriate monetary policy will likely aim to achieve inflation moderately above 2 percent for some time.

Let’s break that down into 4 smaller chunks:

We have also made important changes with regard to the price-stability side of our mandate. Our longer-run goal continues to be an inflation rate of 2 percent. Our statement emphasizes that our actions to achieve both sides of our dual mandate will be most effective if longer-term inflation expectations remain well anchored at 2 percent.

This suggests that the policy was intended to be symmetric. (That was also my view.) Under an asymmetric policy where the Fed only offsets inflation undershoots, inflation (and inflation expectations) would average more than 2%.

However, if inflation runs below 2 percent following economic downturns but never moves above 2 percent even when the economy is strong, then, over time, inflation will average less than 2 percent. Households and businesses will come to expect this result, meaning that inflation expectations would tend to move below our inflation goal and pull realized inflation down.

In these two sentences Powell seems to accuse the previous Fed of an asymmetric policy that allowed below 2% inflation but not above 2% inflation. He correctly points out that if policy is asymmetric, then inflation will not average 2% over time. And that’s bad! So why would anyone think Powell was now advocating an asymmetric policy?

To prevent this outcome and the adverse dynamics that could ensue, our new statement indicates that we will seek to achieve inflation that averages 2 percent over time.

This sentence pretty clearly implies that the policy is intended to be symmetric. He’s already explained why an asymmetric policy is bad, and then follows that up by stating that the new policy seeks an average inflation rate of 2%, with no mention of asymmetry. And the term “average” has a pretty clear meaning, more consistent with the symmetric interpretation. Case closed?

Not quite. The final sentence gives an example of how FAIT might work in practice:

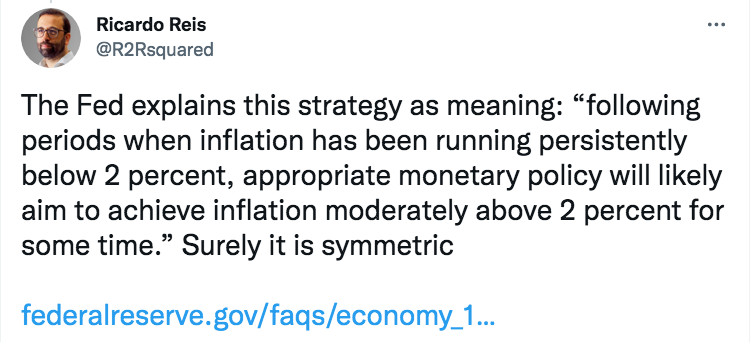

Therefore, following periods when inflation has been running below 2 percent, appropriate monetary policy will likely aim to achieve inflation moderately above 2 percent for some time.

This could be interpreted in two ways. He might be merely using this case as an example, as during August 2020 inflation was running below target and the Fed intended to offset that low inflation with higher than 2% inflation in the future. That would be consistent with the symmetric interpretation. Or he might be signaling that the policy is asymmetric, but that would directly contradict his earlier statements that inflation will continue to average 2% over time.

It is now clear that the Fed intends for inflation to average above 2% over time, but I defy anyone to get that interpretation from Powell’s August 2020 statement.

A few months later, Richard Clarida gave his own interpretation to FAIT:

The new framework is asymmetric. That is, as in Bernanke, Kiley, and Roberts (2019), the goal of monetary policy after lifting off from the ELB is to return inflation to its 2 percent longer-run goal, but not to push inflation below 2 percent. . . .

I believe that a useful way to summarize the framework defined by these five features is temporary price-level targeting (TPLT, at the ELB) that reverts to flexible inflation targeting (once the conditions for liftoff have been reached).

This interpretation is clearly different from Powell’s earlier explanation. Recall that Powell said:

Therefore, following periods when inflation has been running below 2 percent, appropriate monetary policy will likely aim to achieve inflation moderately above 2 percent for some time.

In contrast to Powell, Clarida is saying that the Fed will only offset below 2% inflation that occurs at the zero lower bound. When not at the zero bound, the Fed will revert to ordinary inflation targeting, the exact same policy regime that was in place prior to 2020. Clarida’s interpretation is actually more consistent with maintaining an average inflation rate of 2%, because inflation usually runs below target when the economy is at the zero lower bound. (But not always, as we saw in 2021.)

Even TPLT would have been a slight improvement over previous Fed policy, as long as the new policy is pre-emptive. That is, as long as the Fed tightens as appropriate during the catch-up period to keep the expected future price level on target. But Powell didn’t just adopt FAIT in 2020; he also abandoned the policy of pre-emptive moves to prevent inflation overshoots. Now the Fed would wait until excessive inflation was actually occurring before tightening. When combined with FAIT, that’s a recipe for disaster (as Frederic Mishkin recently noted.)

John Williams also described an asymmetric FAIT, but emphasized that he was not describing the actual Fed policy, just his preference:

I should be clear from the start that the goal of my presentation is to engage in the broad academic and central bank discussion on monetary policy strategies, and that this is not, and should not be interpreted as, a description of the Federal Reserve’s new policy framework or the practical application of AIT to real-world situations.

Clarida offered a similar disclaimer. So what is the actual policy?

You might be saying to yourself that the problem is with me. “Sumner is a dummy; the public understood that the policy would be asymmetric.”

Well, apparently “the public” does not include prominent economists such as Ricardo Reis.

Nor does it include Fed economists writing articles in Fed publications explaining the policy to the general public. This is from a 2021 Dallas Fed paper by Enrique Martínez-García, Jarod Coulter and Valerie Grossman:

By comparison, average inflation targeting means that policymakers would consider those deviations and can allow inflation to modestly and temporarily run above the target to make up for past shortfalls, or vice versa. [Emphasis in original]

So now it’s symmetric again. But by early 2022, it was asymmetric again. What a mess!

Even today, it’s not clear if the new Fed policy applies at all times, or only at the zero lower bound.

PS. You might recall that Communication Breakdown appeared on the first Led Zeppelin album. But that album contains another song that better describes my feelings about Fed communication.

And why stop there? After all, Powell used to play guitar in a rock band. Maybe he was inspired by “How Many More Times”, or “Good Times, Bad Times.” What would Powell think of these lyrics?

Your love is not credible.

It’s a time inconsistent thing.

I need a commitment mechanism.

Baby, I need a ring.

PPS. Larry Summer’s view of FAIT:

Tags:

19. June 2022 at 11:42

Here’s a basic calculation I did.

I think TIPS spreads might imply that the market still sees inflation that is basically in line with FAIT.

https://mobile.twitter.com/KAErdmann/status/1537995772746035201

19. June 2022 at 11:48

I am not sure I care what the stated policy objectives are. Look at what they do and not what they say. The Fed has allowed inflation to run hot and has mostly sat on their respective hands.

19. June 2022 at 13:05

The internally consistent (and potentially overly-charitable) interpretation is something like the following: FAIT applies when the Fed cannot maintain its target, not merely when it messes up and doesn’t maintain it. So at the zero bound (so the story goes), the Fed can’t get the 2% that it wants, so it commits to hit it on average over time. Since, in their mind, there is no way that the Fed has trouble hitting its target outside of the “inflation too low at the lower bound” problem, it’s an asymmetric policy without saying so.

19. June 2022 at 13:40

Kevin, But why do you think that outcome would be consistent with FAIT? The average inflation rate would be well above 2%.

19. June 2022 at 15:13

Stupid question – *why* has the Fed allowed AIT to fail like this? Is it political pressure, of which I had thought the Fed was pretty insulated from, especially since Powell is just starting his second term?

19. June 2022 at 17:25

It’s tips spreads, so the breakeven rate is a bit higher than the Fed pcepi target. From 2004 to 2015 had a pretty tight stable mean of around 2.5, so that seems like a reasonable estimate of what the neutral 2% target breakeven spread would be.

19. June 2022 at 17:55

Seems like recession is FAIT ACCOMPLI at this point.

19. June 2022 at 19:26

Mira, They made a mistake.

Kevin, But if all we do is get back to 2% in 5 years, then FAIT will have failed, as inflation will average far above 2% for the 2020s.

Steve, Yes, recessions are inevitable. But no one can predict when they will occur. It could be one year or ten. Who knows?

19. June 2022 at 23:55

I don’t understand macro, but I know it is “Dazed and Confused” without looking.

20. June 2022 at 05:14

I think it comes down to an earlier point you have made: whether you view the Fed as a fire-fighter or arsonist.

Imagine it’s 2019. Corona is a beer and Wuhan is a malapropism of Wu-Tang Clan. If you think that there are structural factors creating a low-inflation/deflation environment and what the Fed does is fight against these persistent structural influences, then any overshoot about 2% is going to tend to come down by itself if the Fed does nothing. It will be temporary – “transitory” if you will. Even in those circumstances, the challenge will soon be getting inflation back up to 2% again, and while the Fed is doing that (“long and variable lags” seems to be all that the Fed remembers of Friedman) the average will tend towards 2%.

Robert Hetzel is very good at describing the influence of this sort of understanding of inflation in Fed history.

So, even though it sounds ridiculous, I genuinely think that they didn’t give serious consideration to persistent inflation above 2%. That’s one reason why they responded so slowly in the early days of this inflation.

20. June 2022 at 08:11

Gordon, Great song.

William, Yes, Hetzel is very good on this issue.

20. June 2022 at 09:04

I still don’t understand why more people aren’t focusing on real rates shooting up over the last few months. Inflation estimates have actually come down a bit, it’s entirely real rates that are driving overall rates. Wouldn’t understanding why that is going on be one of the most important things?

20. June 2022 at 09:27

Here’s the relevant Fred chart:

https://fred.stlouisfed.org/graph/?g=PfTR#0

Here’s an old (1984) Fed paper explaining what causes changes in real rates:

https://files.stlouisfed.org/files/htdocs/publications/review/84/12/Rates_Dec1984.pdf

Expected Inflation: higher expected inflation drives lower real rates – assuming the inverse is also true, that doesn’t explain current situation, since inflation expectations have been ~flat since March while real rates have been going up.

Monetary Policy: Fed paper writes this is “controversial”, and in the long-run there is no effect

State of Economy: Certainly a link here, but that’s not what’s going on today, given equities and other asset prices have been plunging

Business Taxes: Not relevant

Federal Budget Deficits: I think this is the most probable cause – expectation of future budget deficits leads investors to demand higher return (due to increased risk). Note Scott, this is what I was referring to a few weeks ago – this by definition must mean that investors are increasing probability of default (otherwise where else could the “risk” be coming from??)

Declining Price of Energy: not relevant, since energy prices have been *increasing*

20. June 2022 at 12:10

Before I clicked the link, I thought the song would be “How Many More Times “.

20. June 2022 at 12:42

Powell just improvises. There is no policy, there are no models. Powell doesn’t understand money and central banking.

With the American Rescue Plan added to the 1st qtr. 2021 N-gDp of 10.9% there was sufficient justification to tighten policy, to reduce AD.

Every reform, however necessary, will by weak minds be carried to an excess. — S.T Coleridge, Biographia Literaria

20. June 2022 at 13:20

sd0000, You said:

“Note Scott, this is what I was referring to a few weeks ago – this by definition must mean that investors are increasing probability of default (otherwise where else could the “risk” be coming from??)”

I don’t think it’s just default risk—more federal borrowing could drive up real rates by reducing national saving.

21. June 2022 at 06:54

There’s a huge myth about interest rates.

Economics could easily be described as the search for the Philosopher’s Stone of the Ultimate Control Theory of the Private Quantity of Credit. Economists are obsessed by it.

It’s a complete farce. It’s like centrally planning pig iron output.

21. June 2022 at 10:19

Just like how Powell said (paraphrasing): “we will not target a forecast but wait for actual inflation” and then said the opposite a few months later once inflation materialized.

There was no clear intent on FAIT when it was rolled out. They simply improvised as they went along to avoid any inconvenient paths.

The Fed is not an economic institution. It’s a political institution combined with a make-work program for Economics PhDs as a form of window-dressing.

21. June 2022 at 21:18

Slightly OT, do you think you are too US/Fed centred? A glance at a selection of worldwide inflation rates shows surging inflation across many different monetary areas, Australia to Brazil, EU to UK, Singapore to S Korea, even (for them) Japan and Switzerland. Have all the world’s central banks made the same mistakes at the same time? Or does US monetary policy rule the world?

21. June 2022 at 21:51

James, You asked:

“Slightly OT, do you think you are too US/Fed centred? A glance at a selection of worldwide inflation rates shows surging inflation across many different monetary areas,”

I don’t pay much attention to headline inflation. I did a post recently where I argued that ECB policy has been very good. Ditto for Japan. It’s the Fed I criticize.

Focus on NGDP

22. June 2022 at 06:02

Here’s another amazing example of terrible communications. Scott, do you have a theory as to why the Fed’s economic theory is so off-base?

@ewarren

asks if higher rates will bring down gas prices

Powell: “I would not think so, no.”

Warren: will higher rates bring down food costs for families?

Powell: “I wouldn’t say so, no.”

22. June 2022 at 07:29

Bernanke was the one that censored all communication between economists and the outside.

22. June 2022 at 08:06

Effem, Powell is a mediocre economist.

22. June 2022 at 11:47

So, Powell finally confirmed at today’s hearing that FAIT is not symmetric. Maybe he read the post (or maybe the Senator that asked the question did?)

22. June 2022 at 12:57

Have now read your Euro blog post over at the other place. Euro-NGDP was updated the day after your post. Looks outta control NGDP now, just like Euro-inflation.

https://fred.stlouisfed.org/series/EUNNGDP#0

Same mistakes being repeated by central banks around the globe? Groupthink and/or the unique challenges of covid and Russia/Ukraine? My original question is still valid.

22. June 2022 at 20:44

Rafael, He said something similar in January. Did they ask him why Fed publications said it was symmetric? (That’s probably too much to ask of Congress.)

James, Not sure what you are asking—that graph shows Eurozone NGDP right on target.

Japan’s NGDP is actually down over the past few years.

23. June 2022 at 01:32

The ECB doesn’t target NGDP.

ECB targets inflation, average of 2%, starting at some unspecified point and over an unspecified period, just like the Fed. And … just like the US, Euro-area inflation now at 8%.

As the chart (if you switch to YoY % change) shows, for what it is worth, the Euro-area just experienced a second quarter (1Q22) of 9% YoY NGDP growth, not a target but not good or competent either. Just like the Fed.

Most central banks understandably struggling to tame (an initially good) post-covid NGDP recovery surge in growth. Fed is hardly unique in all of this, contrary to your opinion.

23. June 2022 at 04:28

If FAIT is asymmetric then the inflation target is literally unknowable. If we target 2% but allow overshoots of unspecified magnitude; the resulting inflation can be anything. We now have a central bank with no target.

23. June 2022 at 07:43

If you’d want to overthrow this country, then you’d do exactly what the fed has been doing for the last 60 years.

Dr. Franz Pick:

(1)”government bonds are certificates of guaranteed confiscation.”

(2)“The fact is that the destiny of every currency is devaluation and expropriation.”

(3)“The difficulty with a debt that doubles every ten years is that the interest compounds to the point that it can no longer be paid out of the current revenues. Once the interest itself is debt financed, the compounding accelerates.

That’s why folks subscribed to Dr. Franz Picks’ “Pick’s Currency Report”, a monthly newsletter, and “Pick’s Currency Yearbook” (90 currencies each year).

23. June 2022 at 08:05

James, You said:

“The ECB doesn’t target NGDP.”

That’s right, but it also doesn’t slavishly target headline inflation in the short run. When there is an adverse supply shock, the ECB allows inflation to rise above 2% as long as long run inflation remains anchored at 2% (and vice versa). The best way to do that is with relatively stable NGDP growth. So the ECB is right on target as far as future inflation is concerned.

23. June 2022 at 09:06

Putin was right: “US inflation result of ‘unprecedented’ money-printing”.

We were being lied to. This communist containment policy, like North Korea, Viet Nam, which severed the gold’s tie to the $, will dethrone the U.S. $. As soon as inflation subsides, and interest rates fall, the U.S. $ will plummet and gold will rise.

23. June 2022 at 12:25

So, what’s R *? Or what’s U *?

What’s the N-gDp path? Whether FAIT is or was symmetrical or asymmetrical is immaterial.

It doesn’t even matter. The FED doesn’t have the tools, let alone a model, to hit a target.

The money stock can never be properly managed by any attempt to control the cost of credit. And the only tool, credit control device, at the disposal of the monetary authority in a free capitalistic system through which the volume of money can be properly controlled is legal reserves. Powell eliminated legal reserves in March 2020.

As I said: The FED will obviously, sometime in the future, lose control of the money stock.

May 8, 2020. 10:38 AMLink

Jerome Powell is the worst FED chairman ever.

23. June 2022 at 13:18

Dr. Sumner,

Reading through the headlines today about the fed pushing us into a recession rather than a soft landing, a question for you: could rigid NGDP targeting push us into a negative RGDP growth rate? With inflation trending at 8%, I’m imagining a -3% adjustment to RGDP with a +8% inflation number would net about 5% NGDP growth. Would be curious to hear your thoughts on how or should negative RGDP growth could be avoided in that situation.

24. June 2022 at 04:53

Yes, I agree with your view of his hodgepodge explanation. Assuming you read what I write, I have been saying the same thing. On the one hand it was impossible to not see his view as symmetrical, (how can one “anchor” at 2% without symmetry?). Yet he made comments that implied (not literal—-implied) he would not be symmetrical.

My guess he is s good at monetary policy as he was at guitar playing.

Still, it does not mean this leads to Larry Summers Hindenburg analogy—-although maybe it does.—Precision is likely not as important as we might think. I hope so. Because we do not have it.

25. June 2022 at 07:41

Randomize, There is some risk that 4% NGDP growth could cause a recession, but it would be quite mild. The alternative is an even worse recession in the future.