China’s retail boom

In my view many pundits are excessively pessimistic about the Chinese economy, focusing too much on the weakness in heavy industry and exports. Offsetting that weakness is booming growth in retail sales, as Chinese incomes rise very rapidly. BTW, if China really is doing so poorly, then precisely WHY are Chinese incomes growing so rapidly? There are possible answers — fast rising unemployment or fast rising inflation — but I see no evidence of either. Here’s a recent report from Forbes:

Beijing’s National Bureau of Statistics reported that retail sales in China jumped 10.8% in August compared to the same month last year. That was substantially better than every consensus estimate. Analysts had predicted sales would come in at 10.5%, the same increase as July’s.

Most observers are bullish about consumption as the next driver of the Chinese economy. The dominant narrative tells us China is in a transition from investment-led growth to growth propelled by consumer spending. The oft-cited Andy Rothman, now at Matthews Asia, calls the country “the world’s best consumption story.”

The evidence supporting that proposition looks compelling. Apple, from the first indications of a few hours ago, immediately sold out its iPhone 6S and iPhone 6S Plus in China. Express parcel deliveries were up 47% in July compared to the same month in 2014. Box office revenues? For the first eight months of this year, theyskyrocketed 48.5% from the corresponding period last year.

Consumption contributed 50.2% of growth of gross domestic product in 2014. In the first half of this year, it accounted for 60.0% of GDP.

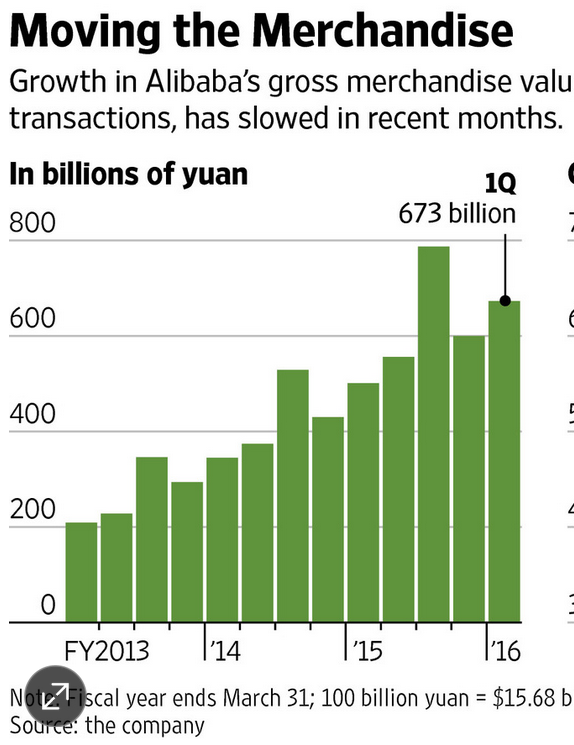

In recent years it has become trendy in China to buy goods online. Alibaba is by far the largest online retailer, so I thought I’d take a look at its numbers:

That graph is a bit misleading for two reasons. First, the latest figures are actually 2015:2, not 2016:1 (their fiscal year ends in March.) And second, growth is expected to slow modestly in Q3 due to the stock market plunge. But clearly the trend is very strong, and other online retailers show the same pattern:

That graph is a bit misleading for two reasons. First, the latest figures are actually 2015:2, not 2016:1 (their fiscal year ends in March.) And second, growth is expected to slow modestly in Q3 due to the stock market plunge. But clearly the trend is very strong, and other online retailers show the same pattern:

Three Chinese Internet companies””Alibaba, Tencent Holdings Ltd. and Baidu Inc.””are now among the world’s largest in market capitalization. The industry’s rise has come even as China’s economic growth has slowed from its double-digit pace of a decade ago.

Some other competitors are expressing caution, though many are signaling still-strong growth. Executives at Alibaba rival JD.com Inc. said last month that they expect third-quarter revenue growth of between 49% and 54%””compared with a year-earlier 61%””reflecting a “conservative outlook in light of the recent Chinese stock-market correction and the slowing macroeconomic conditions.”

Of course just as in America, some of this growth is coming at the expense of brick and mortar firms, and there are indications that sales are flat for many ordinary retailers. But don’t underestimate the importance of online; Alibaba alone now sells more than $100 billion dollars per quarter. If we assume the entire online sector is around $150 billion per quarter, then growth in that sector (year-over-year) is probably on the order of $50 billion per quarter, or $200 billion per year. Thus online growth alone can explain about half of the growth in China’s $4 trillion retail sector.

This relatively sunny view of Chinese retailing is one argument in favor of the Fed raising rates in September, although on balance I still think that would be a mistake. (Of course if China were actually sliding into recession, a rate increase now would be a mistake of epic proportions.) I strongly agree with Ray Dalio’s recent take:

Ray Dalio, the founder of the world’s largest hedge fund Bridgewater Associates, said the firm believes the next big move by the Federal Reserve will be to loosen U.S. monetary policy, not tighten it.

In a client note sent out on Monday, Dalio said the Fed is paying too much attention to the short-term ups and downs of the business cycle rather than the longer-term ramifications of central banks driving interest rates to zero, which now leaves them no room to act if worldwide deflation takes hold.

“The ability of central banks to ease is limited, at a time when the risks are more on the downside than the upside and most people have a dangerous long bias,” said Dalio, who helps manage $162 billion at Bridgewater. “Said differently, the risks of the world being at or near the end of its long-term debt cycle are significant.”

. . .

Dalio said the Fed has overemphasized the importance of the cyclical short-term business cycle in its desire to raise rates, but has been less attentive to the longer-term trend toward deflation.

He said the Fed will react “to what happens,” suggesting it should undertake more quantitative easing, or QE, but he isn’t positive of that, given Fed officials’ desire to raise rates.

Dalio warns of global disinflation, slow global economic growth, and the lingering risk aversion that is behind the proclivity to hold cash despite its significant negative real returns.

“Our risk is that they could be so committed to their highly advertised tightening path that it will be difficult for them to change to a significantly easier path if that should be required,” Dalio said.

That final comment is especially important. This was precisely the mistake the Fed made in mid-2008, when many at the Fed assumed their next move would be higher. It was really hard for them to re-orient their thinking to the need for a rate cut, and hence they did not cut rates during the May through September period, when interest rate cuts were desperately needed. This effective tightening made the recession (which had already begun) much worse.

This time the probable consequences would be more benign, a slowdown in growth and undershooting the inflation target, not recession. But it would leave the Fed with fewer options when the next recession occurs.

HT: Ben

Tags:

15. September 2015 at 06:33

Yes, the retail sales figures from China do not suggest a nation about to collapse. (Tyler Cowen looks out to lunch lately, btw),

And the central bank, the People’s Bank of China, seems to be moving to stimulus. I wish more was understood about the PBoC.

QE in the USA?

Should be conventional policy until we see inflation north of 4%. If that ever happens. Has not happened in Japan. They are on on course to radical reduction of their national debt without hitting their inflation target.

So we can pay off the national debt. Oh, that? Just a little side benefit.

Horrors, what would do if we paid down the national debt, had tight labor markets, and inflation still below target? Horrors! Horrors! Impossible! Bad talk!

But it is happening in Japan…..

15. September 2015 at 06:48

HT: Ben? But this post is exactly what Tyler Cowen has today on Marginal Revolution, except he feels China retail sales may be 0.9% y-o-y, which mimics he says GDP growth (!)

Why am I reading this inferior good when the superior good is offered? I guess I’m not the representative agent for blog readers…

15. September 2015 at 06:48

LITTLE PLUG FROM THE TRADE FOR NGDPG

One key reason, according to Gundlach, is lack of growth in nominal GDP, which is growing at only 4.1% annually. That’s less than the rate of 3.7% in September 2012 when the Fed began its third quantitative easing program (QE3). Gundlach said his team at DoubleLine has shifted its focus to nominal (instead of real) GDP because “we don’t live in an inflation-adjusted world.”

15. September 2015 at 07:39

A deeper look at the data suggests Chinese retail sales have not actually grown in 2014-15.

As Balding points out, flat retail sales make a lot more sense given that output and imports of consumer goods are flat to falling.

15. September 2015 at 07:51

Sorry, link here.

15. September 2015 at 07:58

Hmmm, I see you already linked to that piece indirectly, through Tyler. I would have assumed Alibaba was one of China’s 100 largest retailers in Comprehensive Retail, unless they don’t consider Internet to be retail.

15. September 2015 at 08:04

BTW Balding also had an explanation of why reported inflation is low.

http://www.baldingsworld.com/2015/07/15/considering-the-veracity-of-chinese-gdp/

15. September 2015 at 08:18

Tall Dave–

As stated, perhaps internet sales are booming in China. Or perhaps upstart retailers are grabbing the action.

15. September 2015 at 08:29

[…] 6. Raise rates by an eighth of a percentage point? Ha-ha. And Scott Sumner is optimistic about Chinese retail. […]

15. September 2015 at 08:45

[…] 6. Raise rates by an eighth of a percentage point? Ha-ha. And Scott Sumner is optimistic about Chinese retail. […]

15. September 2015 at 10:32

benjamin cole — So we’re saying the 100 largest retailers were flat to declining, but overall retail sales grew by 10% driven entirely by online sales and growth by smaller retailers?

Also, that doesn’t seem to be what China is reporting. These numbers are a little older but looks like they claim growth of around 7% for non-line retail sales of large retailers.

http://inventariandochina.com/2015/06/12/china-total-retail-sales-of-consumer-goods-in-may-2015/

BTW looks like Alibaba is about 80% of China’s online retail sales.

http://projects.wsj.com/alibaba/

15. September 2015 at 10:35

But I can’t figure out where Balding’s numbers come from, there’s just a spreadsheet. Oh well.

15. September 2015 at 11:39

Reaser, Thanks, but since when is 4.1% less than 3.7%?

Talldave, Balding was the one that said half of all apartments in Beijing are unoccupied. I’ll go with the online data, which doesn’t look like a recession to me. Yes, all the growth in retail could be due to a combination of online and new firms. The number of retailers in China must be growing fast, and most are small. When you are a new firm, 100% of your sales are “growth.” I think 10.8% is far closer to the truth than 0.9%.

Also, aren’t retail sales figures nominal? (Actually, I’m not certain). If so then your inflation conspiracy theory would not impact the results. So again, what are the Chinese doing with all their fast growing income?

Also, if inflation really were high then the yuan would have fallen sharply, instead it’s appreciated sharply over recent years.

Also, he looked at 50 retailers, not 100. And we have no idea what share of retail they comprise.

15. September 2015 at 12:01

Scott — Again, China says large retailers are growing at 7%. But the 100 largest aren’t? Zuh?

Your RGDP conspiracy theory requires that growth to happen without increasing freight or electric usage, while export and imports are shrinking, and housing to experience less than 10% inflation since 2001. Still haven’t heard any reasonable explanation of how that’s possible.

If real growth is so strong, why did China have to spend $100B to support the yuan?

Check again, Balding looked at both 100 and 50 largest retailers. Although I still don’t know where that comes from.

15. September 2015 at 12:22

I was curious so I looked up the “half of apartments are unoccupied” thing. China’s official number is over 20%, and close to 30% in 2nd and 3rd tier cities, and Balding is able to cite half a dozen sources that agree with him, though it looks like those sources have vanished into the ether since 2012.

Also, Ordos seems to have gone from ghost city to ghostier city.

http://gizmodo.com/4-instant-cities-that-are-still-completely-empty-1693270774

15. September 2015 at 12:53

Dear Commenters,

Did any particular news drive interest rates and stock prices higher today?

15. September 2015 at 13:04

Interesting, see below:

“Futures show that this meltup started soon after the weak retail sales data (after a ramp post-China) and was helped by a series of weak data from IP to Biz Inventories”

http://www.zerohedge.com/news/2015-09-15/bonds-baumgartnerd-bad-data-sparks-unhedged-panic-buying-stocks

15. September 2015 at 13:35

“Kevin Erdmann Writes One of the Most Important Blog Posts of The Year”

https://thefaintofheart.wordpress.com/2015/09/15/kevin-erdmann-writes-one-of-the-most-important-blog-posts-of-the-year

http://idiosyncraticwhisk.blogspot.com/2015/09/real-wage-growth-and-tight-labor-markets.html

15. September 2015 at 14:47

Talldave. Sorry, the claim that half the apartments in Beijing are empty doesn’t even pass the laugh test. No “China expert” should say stuff like that.

The fact that people have to keep pointing to Ordos, because the other ghost city stories are collapsing in the light of day, speaks volumes.

I responded to your other comment at the next post.

16. September 2015 at 01:07

“Growth propelled by consumer spending” does not exist. You produce, then consume. If you don’t produce, you don’t consume.

16. September 2015 at 12:19

Matt Yglesias on the rise of a new left

http://www.vox.com/2015/9/16/9322625/sanders-corbyn-mulcair

Your thoughts, Scott?

17. September 2015 at 04:47

Edward, Thanks, I’ll do a post.

22. September 2015 at 08:31

David Andolfatto relates some thoughts on China from his St. Louis Fed colleague. Supports your theory on China’s actual prospects, or at least revealed preference is China is optimistic on global growth.

http://andolfatto.blogspot.com/2015/09/on-chinese-fiscal-stimulus-memory-hole.html