NOW you want easier money?

I happened to catch Rick Santelli on CNBC this morning, the first time I had seen him in years. I recall he always used to complain about the zero interest rate/QE policies of the Bernanke/Yellen years, and indeed mocked the idea that easier money could somehow create growth when bad supply-side policies were holding the economy back. And yet, now that unemployment is down to 3.7% and inflation is back up to 2%, he suddenly opposes a rate increase. I nearly spit out my coffee.

A number of people have recently asked me about what’s going on with all the conservative commenters suddenly opposing higher interest rates. Didn’t they warn us a few years back that low rates were causing artificially high asset prices? If so, wouldn’t we want to unwind these asset bubbles with slightly higher (albeit still extremely low) rates?

Steve Chapman pointed me to a Wall Street Journal piece by Stanley F. Druckenmiller and Kevin Warsh:

The time to be dovish was when the crisis struck and the economy needed extraordinary monetary accommodation. The time to be more hawkish was earlier in this decade, when the economic cycle had a long runway, the global economy ample momentum, and the future considerably more promise than peril.

I do recall lots of conservatives favoring a more hawkish policy in the early 2010s. During most of this period, unemployment was in the 8% to 10% range and both inflation and inflation expectations were unusually low. I would have thought that was the time to be more dovish, not more hawkish. But let’s say I’m wrong and that Bernanke’s monetary stimulus was excessive, perhaps because it triggered high asset prices. In that case, why would someone who had a hawkish view in the early 2010s now oppose interest rate increases, at a time when asset prices are even higher?

In the forlorn hope that I won’t be misunderstood, let me acknowledge two points:

1. There’s a very respectable argument that the Fed should not raise rates tomorrow. That’s not what puzzles me.

2. People have a right to shift their views on the Fed policy stance, indeed that’s appropriate when conditions change. Thus in the early 2010s I thought Fed policy was clearly too tight, whereas now I think it’s about right, because we are close to their inflation and unemployment rate targets.

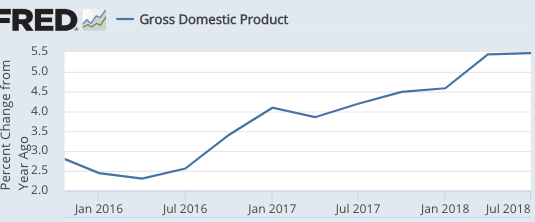

Many of my commenters are conservatives who oppose a rate increase tomorrow, but also thought money was too tight in the early 2010s. That’s fine. What puzzles me is those who thought it was too loose when inflation was 1.5% and unemployment was 8%, but now think that the Fed is likely to make it too tight by pushing rates up to . . . 2.5%—at a time of 2% inflation and 3.7% unemployment. What’s your model?

The elephant in the room is the head of political party with an elephant mascot—Trump. He thought rates were too low before he became president, and now complains they are too high. He thinks his trade war is a reason not to raise rates, even though he also claims that trade wars boost American GDP growth by bringing jobs home, which would actually be a reason to raise interest rates. Of course, no thinking person takes Trump tweets at face value; it’s all politics. But that raises an interesting question. The bizarre flip flop of many conservative commenters regarding monetary policy occurred at roughly the same time as the Trump flip flop, which we all know reflected political considerations.

I don’t wish to impute bad motives to those I disagree with; indeed I’m probably missing something. I eagerly await a coherent explanation of why a tighter policy was needed when the economy was severely depressed and asset prices were far lower than today, and 2.5% interest rates are excessive at a time when the economy is booming, inflation is back at 2%, and asset prices are far higher than in the early 2010s.

Again, I am not saying these conservatives are wrong today. There are respectable arguments for not raising rates tomorrow. I simply don’t understand the conservative model of monetary policy. You may disagree with me, but when it comes to monetary policy I’m no moron. I can generally teach even theories with which I disagree, and indeed I often taught the Keynesian model to my students. But I wouldn’t even know how to explain modern conservative views on monetary policy to my students. What is the model?

When I go to conservative monetary policy conferences, I hear one speaker after another rail against “discretion”. But when I read modern conservative commentary on monetary policy, I’m confronted with policy judgments that seem far, far, far more discretionary than anything that came out of new Keynesian economics. At least the new Keynesians favored targeting inflation at 2% and unemployment at the natural rate. That’s not ideal, but it’s a sort of guidepost.

In contrast, consider this uber-discretionary set of claims:

In a first-best world, the Fed would have stopped QE in 2010. It might then have mitigated asset-price inflation, a government-debt explosion, a boom in covenant-free corporate debt, and unearned-wealth inequality. It might also have avoided sowing the seeds of future financial distress. Booms and busts take the Fed furthest from its policy objectives of stable prices and maximum sustainable employment.

So a tighter money policy in 2010 would have moved us closer to the “policy objectives of stable prices and maximum sustainable employment” because it would somehow prevent “booms and busts”? Exactly how does that work? I haven’t seen such fancy footwork since James Harden went up against the Utah Jazz.

And what happened to conservative support for the Taylor Rule?