Can an industrial recession coincide with steadily growing real GDP?

Can an $18 trillion dollar economy keep growing at a fairly steady rate, despite a sudden slump in the industrial sector (manufacturing, mining and utilities)?

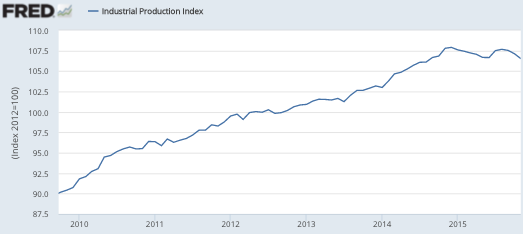

Here is some recent data for industrial production:

Industrial production grew fairly consistently up to December 2014, but then suddenly began falling slowly. Now let’s see what happened to real GDP:

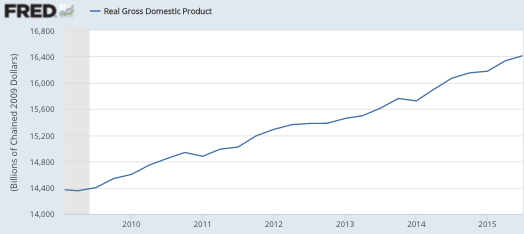

Somehow RGDP has maintained a roughly 2% growth rate since 2010, despite a sudden slump in the industrial sector. Is that even possible? Yes, services picked up the slack.

Somehow RGDP has maintained a roughly 2% growth rate since 2010, despite a sudden slump in the industrial sector. Is that even possible? Yes, services picked up the slack.

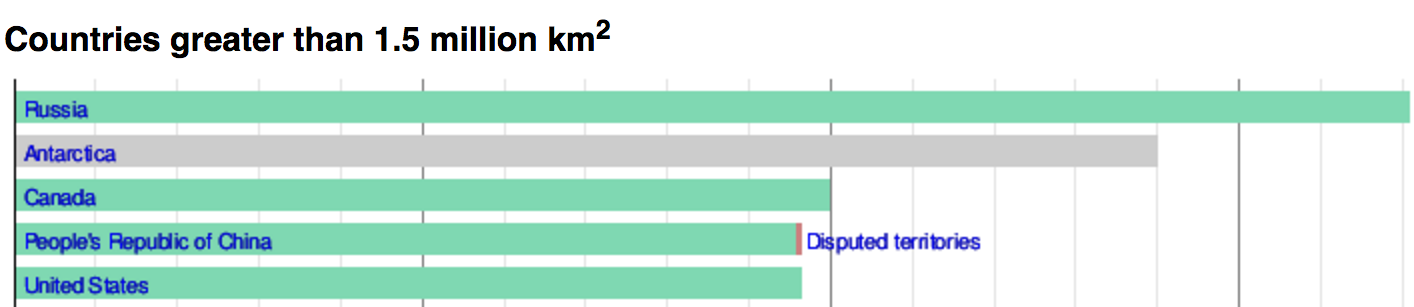

Next question: Can two $18 trillion dollar economies, each of which have the third largest land mass on Earth, continue growing despite a slump in the industrial sector?

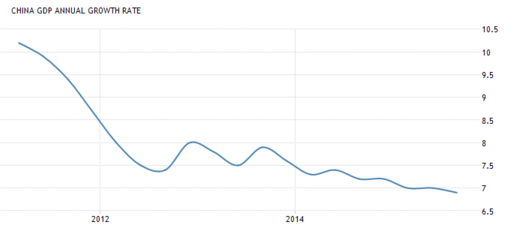

Of course the second $18 trillion economy (PPP) is China. And in China, industrial growth has fallen from the 9% to 10% range in 2013 to about 6% in 2015:

And yet China’s RGDP growth has only slowed slightly, from roughly 7.5% to 8.0% in 2013, to about 7% today:

However there is one very important difference between the two cases. Lots of people believe the Chinese GDP data can’t possibly be correct, given the big reduction in the growth rate of industrial production. But I don’t recall anyone questioning the US figures, despite an even larger slowdown in the growth rate of industrial production.

However there is one very important difference between the two cases. Lots of people believe the Chinese GDP data can’t possibly be correct, given the big reduction in the growth rate of industrial production. But I don’t recall anyone questioning the US figures, despite an even larger slowdown in the growth rate of industrial production.

PS. After I wrote this post I noticed that Tyler Cowen is predicting Chinese growth will soon fall to zero. I think growth will be closer to 6%, and don’t see how his reasons (excessive debt, etc.) would not have applied equally well in other years. Indeed he doesn’t mention what I think is the best argument for a Chinese recession, an overvalued exchange rate which is reducing NGDP growth. In any case, I think the safest prediction is the same one I’ve been making for over 35 years. Boom! And look at the bright side, if I’m wrong this time then my record will still be better than the Golden State Warriors. Tyler also mentions slowing Australian growth, and indeed troubles in the mining sector are affecting Australia. However it’s worth noting that Australia’s unemployment rate actually declined during 2015.

PS. How can the US and China, both the world’s largest economy (due to a dispute over PPP), also both be the world’s third largest country? Disputed territories.

Tags:

6. January 2016 at 08:10

Sure Scott, people will simply have to sell each other more insurance in the service sector and we will be fine. Or maybe not.

By the way, I gave you a favorable review last night, as you are right about the Fed tightening. But solutions must be in the real economy and not be so speculative. Things are set up now just for speculation by the Fed. JMO. http://www.talkmarkets.com/content/us-markets/sumner-and-his-market-monetarists-compared-to-mish-libertarians-and-keynesians?post=81981

6. January 2016 at 08:12

Tyler Cowen’s last post on China seemed incomplete. BTW, the Shanghai composite is up about 20% YOY and the Singapore down about 15%. The S&P 500 is about flat.

Who should be worried?

6. January 2016 at 09:24

The U.S. should be more worried about negative growth than CN. We live in an age of diminished expectations.

And U.S. manufacturing has still been improving. It’s oil-related sectors that are dragging U.S. IP down.

6. January 2016 at 10:34

Scott – how are the categories (manufacturing, mining, utilities) of the industrial production index contributing to overall change in the index? My guess is that commodities are overwhelmingly responsible for the slump in IP, which could make it a more temporary slump.

6. January 2016 at 10:38

I think I promised something on China’s outlook.

Here’s a piece I wrote for CNBC on China’s growth prospects. I argue that policy has taken a nationalist turn, and that’s bad for growth.

http://www.cnbc.com/2016/01/05/why-chinas-growth-could-be-over-commentary.html

6. January 2016 at 10:55

Isn’t the big elephant in the room here oil prices in both the US and China? Cheaper oil increases real wages without companies paying more. So most other sectors can expand and consumers can spend money on other things. As FT has joked with clips of Dallas and other bad soaps that this happened in the 1980s.

And yes, I do think the doomsayers are ahead of the curve and the drop in comodities and oil probably has a bigger impact on Chinese consumers. So I believe the Chinese economy is more similar to the 1960 US manufacturing economy with a strong dollar keeping input prices low and allowing real wages to significantly increase.

6. January 2016 at 13:17

Well, at least the Chinese have this to occupy themselves with:

http://colonelcassad.livejournal.com/2556326.html

Productive fiscal stimulus?

6. January 2016 at 14:38

The highlight on industrial production is curious given the usual focus here upon nominal growth.

I wonder if Scott’s conclusions about China’s nominal GDP growth would change were he to adjust its industrial production to a nominal basis?

China’s reported PPI is deeply deflationary, to the tune of -5.9% as last reported, for four consecutive months…

This suggests that nominal growth in the value of China’s industrial production is materially lower than the reported real rate of 6% and perhaps somewhere around zilch, possibly even negative if PPI deflation is actually worse than reported.

And yet Scott still believes national level N/R GDP figures. Curious.

6. January 2016 at 15:00

Related points to Randy’s question above

1) As best I can tell, it looks like utilities comprise ~10% of the index (http://www.federalreserve.gov/releases/G17/SandDesc/table1.28.htm), of which electric power represents the vast bulk. Is that the correct reading?

2) Electric power demand is highly seasonal (http://www.eia.gov/electricity/data/browser/ to visually get the flavor). More properly speaking though, the seasonality is not in the same sense as say, consumer retail goods but in the sense of being highly weather-sensitive. The difference between summer peaks and spring/fall troughs is a) on the order of 30-35% b) almost entirely due to weather, i.e. that the increase in summer demand is overwhelmingly for air conditioning, and smaller winter peaks are due to demand for home heating.

3) As a consequence of 2), the standard econometric methods to seasonally adjust will implicitly assume average weather over the time period used for estimating the seasonality. When comparing longer periods of time (e.g. a full calendar year to another) this is not much of an issue because weather differences usually wash out by then, but on a month-to-month basis the difference between actual weather and normal weather can cause a lot of noise. For any economist trying to look at monthly-granularity IP for economic trends, I would recommend excluding the electric utility component entirely for reasons analogous to excluding food & energy from month-to-month CPI (noise is much larger than the signal) unless you have a method for making a weather adjustment that is more precise than standard seasonality adjustments (note: speaking as a professional energy analyst I am happy to make suggestions on that matter).

4) On the scale of macro-monthly data, there is no way to store electricity, so production must meet demand in real-time (very literally- on the grid, a supply/demand mismatch of 1% would force a regional blackout in 30 seconds as the voltage change would otherwise irreparably damage electronics). As a consequence, unlike most other industries, electric production must match the seasonality of demand 1-for-1 (actually more than 1-for-1 due to transmission losses). An additional reason to exclude month-to-month variation from macroeconomic analysis.

5) There is a perma-1 month lag between the most recent IP index and the DOE data used for utility generation. The most recent IP data is through November, but the underlying DOE data that is used as the basis for utility IP component is only through October. Whatever the Fed is using for November must be a very rough guesstimate either on the Fed’s part or the DOE’s. Without knowing how that guesstimate is made (and I can’t find any documentation on it), I would really, really, really recommend excluding utility output from any macro analysis based on the Nov data.

6) While it’s not really relevant to Scott’s post, utility IP ought to probably be excluded from any capacity utilization figures used in most macroeconomic analysis. Because of the aforementioned storage problem and the cataclysmic effects of a sustained blackout, electric power infrastructure is on the whole designed to have 12-15% overcapacity in relation to the instantaneous peak of demand. “Underutilization” of electric generation capacity does not indicate slack demand but rather indicates a) seasonality of demand b) a conscious policy choice to “overbuild” capacity. (As a side note, the cost-recovery mechanism for that “overcapacity” is the primary policy/market-design problem in the electricity market)

6. January 2016 at 15:19

Matt,

That was very nice. You can add in number of weekends in a month throws things off too. Adds a lot of off-peak hours into the average.

6. January 2016 at 18:09

Scott,

Why do you focus on the Chinese RGDP growth? The Chinese NGDP growth has collapsed from 19.4% in 3Q2011 to 6.2% in 3Q2015. That is a pretty severe slowdown. It averaged more than 15% from 1Q2004 to 3Q2011.

What does this say about the monetary policy in China? Surely this is a cause for concern especially as nominal debt continues to grow in double digits?

6. January 2016 at 19:18

Randy, I believe that mining has been the weakest.

Steven, But you don’t present any evidence that policy is taking a nationalist turn. Most news reports say the recent moves are towards liberalization.

Collin, A year ago I predicted that the plunge in oil prices would not affect the US, and I was right.

Lots of economists talked like it was a “tax cut” that would raise growth. Today’s WSJ pointed out that those predictions were wrong.

Fyodar, Rather than saying I “believe” the GDP data, I’d rather say I’m waiting for a good reason to disbelieve the data. So far the naysayers have between wrong, and wrong again, and wrong again. Maybe some day they’ll be right, but I’m not persuaded by their arguments.

I don’t believe any GDP data is exactly right, even the US data. I’ve said actual Chinese RGDP growth might be in the 5% to 6% range. But it’s not zero.

Matt, Very good point. I’d actually like to see an index that dropped utilities and added construction. I think of construction as a more “industrial” type activity that electricity. It would then be picking up the more cyclical parts of the economy.

Apoorv, Monetary policy in China is clearly too tight. I’ve said that in other posts. In this post, I said that if they do have a recession it will be due to tight money.

6. January 2016 at 21:14

“Apoorv, Monetary policy in China is clearly too tight. I’ve said that in other posts. In this post, I said that if they do have a recession it will be due to tight money.”

So, I thought the Chinese learned from our mistakes rather than ending up repeating them. So why are they tightening?

Did some globalist banker tell them to do it? What caused this behavior?

6. January 2016 at 22:16

“Indeed he doesn’t mention what I think is the best argument for a Chinese recession, an overvalued exchange rate which is reducing NGDP growth.”

Ah ah aaah, no that contradicts your own theory, Sumner.

The only cause for rising or falling NGDP according to MM principles would be the PBOC’s actions.

You just tacitly admitted that the fall in NGDP in the US during 2008-2009 was not necessarily caused by the Fed. That there are other factors that cause NGDP changes besides central bank inflation/deflation of the money supply.

Oops.

6. January 2016 at 22:49

Thanks for your response, Scott. Let me put it another way: how do you reconcile a modest decline in China’s NGDP growth rate when nominal industrial production appears to have crashed from mid/high teens growth yoy to zero growth or outright decline? Can it really be that services growth has exploded by enough to compensate for such a massive fall in such a large component in GDP? I suggest not.

A follow-up to your response to Apoorv: how can money be “too tight” in China when both credit and M2 are both growing at a faster pace than reported NGDP? Are you really asserting that credit and money growth should be EVEN HIGHER, when it’s abundantly clear that China is in the grip of a gargantuan credit bubble?

7. January 2016 at 01:12

I’m surprised you haven’t weighed in on Stanley Fischer’s statements:

LIESMAN: WHEN I LOOKED AT WHERE THE MARKET IS PRICED, THE MARKET IS PRICED BELOW WHERE THE FED MEDIAN FORECAST IS. QUITE A BIT. TWO RATE HIKES REALLY, IF YOU COUNT THEM IN QUARTER POINTS. DOES THAT CONCERN YOU THAT THE MARKET NEEDS TO CATCH UP WITH WHERE THE FED IS OR IS IT A MATTER OF YOU THINK THE FED NEEDS TO RECALIBRATE TO WHERE THE MARKET IS?

FISCHER: WELL, WE WATCH WHAT THE MARKET THINKS, BUT WE CAN’T BE LED BY WHAT THE MARKET THINKS. WE’VE GOT TO MAKE OUR OWN ANALYSIS. WE MAKE OUR OWN ANALYSIS AND OUR ANALYSIS SAYS THAT THE MARKET IS UNDERESTIMATING WHERE WE ARE GOING TO BE. YOU KNOW, YOU CAN’T RULE OUT THAT THERE IS SOME PROBABILITY THEY ARE RIGHT BECAUSE THERE’S UNCERTAINTY. BUT WE THINK THAT THEY ARE TOO LOW.

http://www.cnbc.com/2016/01/06/cnbc-exclusive-cnbc-transcript-federal-reserve-vice-chairman-stanley-fischer-speaks-with-cnbcs-steve-liesman-on-squawk-box-today.html

7. January 2016 at 05:03

Also there is this Fischer speech from Sunday:

given that financial variables are a critical part of the transmission mechanism of monetary policy, when policymakers say the economy is overheating, they may well be considering the behavior of asset prices as a critical part of that phenomenon and part of the reason to tighten monetary policy. Thus, I believe that the real issue of whether adjustments in interest rates should be used to deal with problems of potential financial instability is macroeconomic, and that if asset prices across the economy–that is, taking all financial markets into account–are thought to be excessively high, raising the interest rate may be the appropriate step

http://www.federalreserve.gov/newsevents/speech/fischer20160103a.htm

7. January 2016 at 05:37

[…] Indeed he doesn't mention what I think is the best argument for a Chinese recession, an overvalued exchange rate which is reducing NGDP growth. In any case, I think the safest prediction is the same one I've been making for … Article by recession – Google Blog Search. Read entire story here. […]

7. January 2016 at 08:03

Steve, interesting as are all these comments. If asset prices are too high, it means every house built is too expensive from the start. Every car built is too expensive from the start. Also, every small business has less access to credit when interest rates are low and they create the jobs. Big business benefited from low rates. They have massive cash for protection. But they don’t create the jobs. Also, they issue their own credit, bonds, and don’t need loans from banks so banks should be able to make more by lending to the real economy, and to mid sized and small companies. But then, Fischer still wants IOR? That is the part I don’t get. Go easy on me, Scott.

7. January 2016 at 11:26

I don’t think Scott will be too happy with that Fischer speech. For one thing, he lists four possible steps to deal with the zero lower bound (ZLB) problem, and none of them are NGDP targeting. For another, one of the steps he does consider is a higher inflation target, but he argues against it because it might lead to more variability in inflation: “The welfare costs of high and variable inflation could be substantial. For example, more variable inflation would make long-run planning more difficult for households and businesses.” If this is a problem for a higher inflation target, it must be even more of a problem for NGDP targeting. I think Scott would argue that variable inflation shouldn’t matter for planning, and instead what should matter is smooth and steady NGDP growth, but it looks like Fischer would disagree.

7. January 2016 at 12:11

Fyodar, You said:

“A follow-up to your response to Apoorv: how can money be “too tight” in China when both credit and M2 are both growing at a faster pace than reported NGDP? Are you really asserting that credit and money growth should be EVEN HIGHER, when it’s abundantly clear that China is in the grip of a gargantuan credit bubble?”

No, you are confusing money and credit. I’m not arguing for easier credit, I’m arguing for easier money. They are completely unrelated. They need faster NGDP growth. They may also need slower credit growth, I’m not qualified to offer an opinion on that question.

On the other question, growth in services is running at about 11%, so that could offset slower growth in IP. I’m certainly not claiming the figures are exactly right, but it’s not clear to me which figures are clearly inaccurate. People make a lot of claims to that effect, but I don’t see the evidence. China’s consumer sector is clearly booming, I think everyone agrees on that point. The exact RGDP growth rate is debatable, but the fact that IP has slowed sharply does not preclude a fairly strong RGDP growth rate. On the other hand, I concede it may well be less than the official 6.9%. Time will tell. Looking back, it’s clear that the high reported growth rates over the past 35 years are broadly correct.

Steve, I did a post on Fischer just yesterday. Maybe I should do another.

O. nate. I already did a post on that.

7. January 2016 at 13:37

“No, you are confusing money and credit. I’m not arguing for easier credit, I’m arguing for easier money. They are completely unrelated.”

I’m sorry, but…what?! In which universe are money and credit NOT related? That is a truly astounding thing for anyone to say of a modern economy, let alone a professor of economics.

Could you please elaborate or explain what you mean by this?

7. January 2016 at 13:56

Fyodor, here is Scott’s definitive post on the subject. Easy money is expansion of the money supply. http://www.themoneyillusion.com/?p=11310

I personally think credit is connected, so that banks are more willing to lend where they can make a secure profit. If they can only lend at very low interest, they are afraid to lend.

Easy credit, low interest rates actually discourage lending to people buying a house, people doing small or medium businesses because those people have no access to the credit markets. Big companies can issue their own bonds.

So, IMO, the job creators, the small and medium businesses must gain access to credit and can only do so if interest rates go up. It doesn’t always work because sometimes you have to save big business by lowering rates, especially if they borrowed up to their gills. But the big businesses don’t create most of the jobs, historically.

Scott is also arguing, I think, that real rates exploded in late 2008 and banks didn’t loan to take advantage of the chance to make a big profit.

7. January 2016 at 17:09

Thanks, Gary, but if that’s the definitive post it’s disappointingly obtuse. You state that, “Easy money is expansion of the money supply.”

However, what Scott actually states in that post is the following:

“Since the 1980s I’ve advocated a policy aimed at steady growth in NGDP expectations. Brad DeLong has recently made similar recommendations. That’s great. And if that’s the goal, then easy money is a policy expected to exceed the NGDP growth target, and tight money is a policy expected to fall short.”

This is a self-referential circular definition, i.e. easy money is whatever circumstances enable NGDP to exceed a given target rate of growth.

Maybe Scott could answer my question put a different way: how can China growing M2 at around 13-14% yoy relative to NGDP growth of 7-8% yoy be suffering from monetary policy that is “too tight”?

7. January 2016 at 18:48

Fyodor, What’s astounding is that something everyone was taught when I was in grad school, has now been forgotten by so many.

Money is the medium of account—the monetary base in the US. Credit is loans. Changes in the value of money have no necessary relationship between the real volume of credit. Yes, it impacts the nominal quantity, but it impacts the nominal quantity of everything.

NGDP growth is a good indicator of monetary policy in China, whereas M2 growth is a better indicator of credit growth (albeit far from perfect). If you are right (I’m not saying you are, but let’s assume that) then China should raise the NGDP growth rate and lower the M2 growth rate. Ignore everything Gary says about my views, he’s clueless on these issues.

Gary, You said:

“Easy money is expansion of the money supply. ”

Just go away, you have no idea what you are talking about. This is not a field for amateurs

7. January 2016 at 19:49

Fine Scott, I understand, however if you can’t communicate with amateurs you become like the guys with the complex financial vehicles, who understood them while everyone else didn’t. That didn’t work out to well for the democracy did it Scott? But apparently you said exactly this to Vox which you just denied now:

The Federal Reserve chooses between two basic options. It can expand the money supply by creating new dollars and introducing them into circulation. This is known as an “easy,” “loose,” or “expansionary” policy. http://www.vox.com/2014/7/8/5866695/why-printing-more-money-could-have-stopped-the-great-recession

Perhaps you are more like Rasputin than people think. Or maybe the Pied Piper. Just lure the Fed away, ok? They are rats. 🙂

7. January 2016 at 20:35

@Fyodor @Gary Anderson – now you see why I called Sumner the Pied Piper. He says: “No, you are confusing money and credit. I’m not arguing for easier credit, I’m arguing for easier money”- when in fact the EU, USA have less than 10% of the GDP in ‘money’ (Finland is at 3%) and Bernanke’s 2002 FAVAR paper says monetary shocks are, at best only responsible for 3.2% to 13.2% of output (out of 100%). So Sumner thinks something that is less than 10%, in both total and in rates of change, is so important to the economy? That it makes a difference between recession and non-recession? Keep in mind that even with a paperless, currency-less economy, you can still have ‘units of account’. You just specify something as the ‘unit’, it can even be those ultra-heavy round stones they used in Polynesia. Or Bitcoin. Or (my favorite) gold.

7. January 2016 at 20:58

“@Fyodor @Gary Anderson – now you see why I called Sumner the Pied Piper.”

Lol, I didn’t know that.Lol. Can you imagine when words mean one thing one time and another thing another time? The human race would be crazy. I commend Scott on appearing to be sane while doing that. I just wish he could restore my confidence, in him!

But Ray, you must be an Austrian. At least you are a professional, so I won’t attempt to answer you. I hope you understand this blog is for professionals, unlike myself.

7. January 2016 at 21:30

“Money is the medium of account—the monetary base in the US. Credit is loans. Changes in the value of money have no necessary relationship between the real volume of credit. Yes, it impacts the nominal quantity, but it impacts the nominal quantity of everything.”

Ah, thanks. I’m up to speed on the backstory and your position is a lot clearer now.

A question, however: why do you think the monetary base has any relation to the direction and magnitude of NGDP growth given the bulk of NGDP and an even greater proportion of financial transactions is transacted with what you don’t consider to be money?

“NGDP growth is a good indicator of monetary policy in China, whereas M2 growth is a better indicator of credit growth (albeit far from perfect). If you are right (I’m not saying you are, but let’s assume that) then China should raise the NGDP growth rate and lower the M2 growth rate. Ignore everything Gary says about my views, he’s clueless on these issues.”

Could you explain why NGDP is a good indicator of monetary policy?

Also, when you say that, “China should raise the NGDP growth rate and lower the M2 growth rate”, do you mean the target level of NGDP growth, or actual outcome, and how should China lift NGDPg and lower M2g?

Thanks again for your responses.

7. January 2016 at 21:48

http://evonomics.com/how-learning-economics-makes-you-antisocial/ After reading this, what Scott has done makes sense:

Scott said:

Gary, You said:

“Easy money is expansion of the money supply. ”

Just go away, you have no idea what you are talking about. This is not a field for amateurs.

———————

Scott previously said as edited by Vox:

The Federal Reserve chooses between two basic options. It can expand the money supply by creating new dollars and introducing them into circulation. This is known as an “easy,” “loose,” or “expansionary” policy.

http://www.vox.com/2014/7/8/5866695/why-printing-more-money-could-have-stopped-the-great-recession

Economics students get progressively dishonest according to the former head of Harvard Business School, and the link is above. Since Scott has a PhD, one can only contemplate his level of veracity. 🙂

8. January 2016 at 15:34

How much of the apparent decline in industrial production is an artifact of the decline in oil prices?

Producing 9 million barrels of oil at $100/barrel produces more “output” than 10 million barrels of oil at $40/barrel. No?

8. January 2016 at 17:42

Fyodor, The monetary base is important because it is the medium of account. By analogy, the gold market was really important under the gold standard regime. Since things are priced in terms of base money, changes in the supply and demand for base money have a powerful impact on all nominal aggregates. The Fed has the power to control the value of money, and needs to do so.

Central banks have various tools for controlling the supply and demand for base money. Those tools are very effective, but should not be confused with tools for controlling debt. For instance, in China there is too much debt because of government created moral hazard; the central government backstops bad loans made by the state-owned banks. To reduce that problem, you need tighter controls over banking lending (even better would be bank privatization.)

Gary, I just love commenters who quote other people and claim they are quoting me. Very classy, as I’d expect from you.

Cooper, Industrial production is real output, not nominal.

10. January 2016 at 12:54

“Since things are priced in terms of base money, changes in the supply and demand for base money have a powerful impact on all nominal aggregates.”

Except it seems that they don’t. The US monetary base has exploded in recent years, for the obvious reason, with little apparent effect on NGDP.

Going back to the earlier questions:

1) Could you explain why NGDP is a good indicator of monetary policy?

And

2. When you say that, “China should raise the NGDP growth rate and lower the M2 growth rate”, do you mean the target level of NGDP growth, or actual outcome, and how should China lift NGDPg and lower M2g?

11. January 2016 at 08:08

Fyodor, I said supply and demand. What happens to the demand for base money at zero rates? What happens when the Fed pays IOR at a rate higher than T-bill yields?

Regarding NGDP, recall that monetary policy impacts AD, not P or Y directly. The split is controlled by supply side factors. And NGDP measures AD better than P does, as P is impacted by supply shocks.

11. January 2016 at 08:10

China can lift NGDP by devaluing the yuan, and reduce credit growth by tightening regulations on the state-owned banks. Ideally privatize them–but that will take a long time.

11. January 2016 at 15:33

“What happens to the demand for base money at zero rates? What happens when the Fed pays IOR at a rate higher than T-bill yields?”

Ceteris paribus, demand for money increases, deposits at the Fed increase. This explains the accumulation of deposits at the Fed. It doesn’t reconcile the unresponsiveness of NGDP to base money explosion with your theory.

“Regarding NGDP, recall that monetary policy impacts AD, not P or Y directly.”

Monetary policy doesn’t affect AD directly either. This doesn’t demonstrate why NGDP is a “good indicator of monetary policy”.

“China can lift NGDP by devaluing the yuan, and reduce credit growth by tightening regulations on the state-owned banks. Ideally privatize them–but that will take a long time.”

You don’t think those are contradictory policies? The evidence suggests that falling credit growth in China is correlated with falling NGDP growth. Furthermore, the means of “devaluing” the yuan itself could be profoundly deflationary/depressive to NGDP, e.g. if driven by unrestricted and unsterilised capital outflow.

17. January 2016 at 13:49

Ahem?

17. January 2016 at 14:15

Fyodor, Check out my “short course on money”. Temporary monetary injections have little effect, as I pointed out in a 1993 paper, and Krugman confirmed in a 1998 paper.

I believe that monetary policy does directly impact AD.

And no, the two policies I describe are not contradictory. When I was in school we were all taught not to confuse money and credit–now I see people do it all the time. Monetary policy determines the size of NGDP, whereas credit policy determines the ratio of credit to NGDP. They are fundamentally different policies. The Zimbabwe hyperinflation could have occurred in an economy with virtually no credit.

18. January 2016 at 13:21

Thank you, Scott.

“Temporary monetary injections have little effect…”

How do you define “temporary”? The US monetary base surged more than 50% in one year seven years ago and then continued to grow at a rapid pace over following years. It’s now massive relative to its starting point eight years ago, with no material effect on NGDP. Eight years is a long time, enough time to include at least one full economic or business cycle. It’s a stretch of Keynesian proportions to call this “temporary” and it does not reconcile with your theory.

“I believe that monetary policy does directly impact AD.”

I know you believe it; I’d like to know why, based on what evidence?

“And no, the two policies I describe are not contradictory. When I was in school we were all taught not to confuse money and credit–now I see people do it all the time. Monetary policy determines the size of NGDP, whereas credit policy determines the ratio of credit to NGDP. They are fundamentally different policies. The Zimbabwe hyperinflation could have occurred in an economy with virtually no credit.”

When you were in school were you also taught about open capital accounts and money supply in a managed exchange-rate regime? What happens to money supply in China if net capital outflows exceed the current account surplus?

On the central question, eyeball the data: there is a strong apparent relationship between China’s credit growth and NGDP growth. The available evidence suggests that slower credit growth in China results in slower NGDP growth. If you disagree, I’d be grateful if you would explain why.

Thanks again for your responses.

24. January 2016 at 13:53

*bump*

24. January 2016 at 14:32

Fyodor, The first question is easy to answer, the Fed switched to IOR, which causes a large, one time increase in the demand for base money. Without IOR, the temporary effects last as long as you are at the zero bound. Once you exit the zero bound you tend to get the standard quantity theory results.

You asked:

“I’d like to know why, based on what evidence?”

Theory predicts it would, and I’ve spent a lifetime examining 100s of cases where it seems to have these effects.

Suppose money did not impact AD. Then when interest rates are positive, the Fed could double the money supply, with no rise in nominal spending. But that would mean the average cash balances held by the public would double in real terms. But why would the Fed’s action cause people to want to hold larger real cash balances? It wouldn’t cause me to want to hold larger real cash balances–how about you?

You said:

“What happens to money supply in China if net capital outflows exceed the current account surplus?”

Those are unrelated issues. The PBOC may operate in such a way that they are correlated, but they are conceptually unrelated. Look, the money supply in the US is correlated with almost all nominal variables, over long periods of time, including nominal spending on haircuts. That doesn’t mean haircuts are money. Credit and money are very different things.

I’d like to see data on the Chinese monetary base, and credit data. Without that I can’t comment.

27. January 2016 at 15:10

“Fyodor, The first question is easy to answer, the Fed switched to IOR, which causes a large, one time increase in the demand for base money. Without IOR, the temporary effects last as long as you are at the zero bound. Once you exit the zero bound you tend to get the standard quantity theory results.”

It was more than a one-time increase in base money – base money continued to climb through the QE era. Regardless, the known facts are that base money exploded and yet NGDP did not. Why not?

“Theory predicts it would, and I’ve spent a lifetime examining 100s of cases where it seems to have these effects.”

Strangely enough, theories tend to work better in theory than in practice, so I would be more interested in your empirical work describing the direct effect of base money supply on AD.

“Suppose money did not impact AD. Then when interest rates are positive, the Fed could double the money supply, with no rise in nominal spending. But that would mean the average cash balances held by the public would double in real terms. But why would the Fed’s action cause people to want to hold larger real cash balances? It wouldn’t cause me to want to hold larger real cash balances–how about you?”

This also doesn’t address the purported direct – again, I stress “direct”, because that’s how you put it – link between money supply and AD.

“Those are unrelated issues. The PBOC may operate in such a way that they are correlated, but they are conceptually unrelated.”

In a controlled/managed FX regime, of course the PBOC operates them as related. The run up, and recent run-down, in the PBOC’s FX reserves is the by-product of the CNY (de)monetisation of China’s balance of payments position in a fixed/managed exchange rate system. Net inflows (i.e. current a/c + capital a/c > 0) result in FX accumulation (i.e. PBOC issues CNY to buy USD), as we’ve seen for most of the past 20 years. Since 2014, however, net outflows, driven by the capital a/c, have resulted in run-down of FX reserves. The FX reserves are umbilically connected to CNY money supply through the operation of PBOC’s balance sheet. The bulk of its assets are FX assets (mostly USD-denominated assets, it can be assumed), accumulated through this process and funded by the bulk of its liabilities: CNY deposits of Chinese banks. Now, the PBOC has mitigated the expansionary/contractionary effect on domestic CNY creation of FX reserve management through the aggressive use of required reserve ratios, but that’s the mechanism. Ceteris paribus, net outflows of capital are contractionary to money supply.

“I’d like to see data on the Chinese monetary base, and credit data. Without that I can’t comment.”

Fair enough. The PBOC’s annual reports are a good start and the usual suspects (Bloomberg, Datastream, CEIC etc.) can provide the data time series.

30. January 2016 at 07:59

Fyodor, You asked:

“It was more than a one-time increase in base money – base money continued to climb through the QE era. Regardless, the known facts are that base money exploded and yet NGDP did not. Why not?”

I think you missed my point. The injections were either expected to be temporary or expected to later be sterilized with higher IOR.

You asked:

“Strangely enough, theories tend to work better in theory than in practice, so I would be more interested in your empirical work describing the direct effect of base money supply on AD.”

Check out this post, and the rest of the series (I.e the next few posts.)

http://www.themoneyillusion.com/?p=30081

You asked:

“This also doesn’t address the purported direct – again, I stress “direct”, because that’s how you put it – link between money supply and AD.”

Of course it does. The attempt to get rid of excess cash balances drives up AD. That’s monetary economics 101, isn’t it?

It’s up to the Chinese government as to whether they wish to tie together credit and money. In the early 1980s the US accompanied a tight money policy with an expansionary credit policy.

2. February 2016 at 14:23

Thanks, Scott. I do appreciate your time on this discussion.

“I think you missed my point. The injections were either expected to be temporary or expected to later be sterilized with higher IOR.”

I think you missed my point. Base money expanded massively; NGDP did not: thesis falsified, no?

“Check out this post, and the rest of the series (I.e the next few posts.)

http://www.themoneyillusion.com/?p=30081”

Thanks, that’s interesting, but doesn’t really address the point, i.e. whether monetary policy directly affects AD.

Now, establishing a correlation between dM and dNGDP may support your thesis of causation, but doesn’t demonstrate that the causative effect is direct as opposed to indirect.

Contrast the post-Keynesian IS-LM model’s fixation on the real interest rate as the “price” driver of investment, thereby INDIRECTLY affecting AD. I’m not endorsing that model, just representing the traditional alternative just-so story.

I’m interested in your transmission mechanism, i.e. what is the chain of logic that changes economic actors’ propensity to transact (i.e. dAD) as a DIRECT result of dM.

“Of course it does. The attempt to get rid of excess cash balances drives up AD. That’s monetary economics 101, isn’t it?”

No, I don’t think it’s that simple, and I don’t think you do either. HOW is AD driven up? Consumers spend more? Businesses invest more? How and why do you see this happening as a DIRECT result of the change in the stock of “money” (however your choose to define it), by what mechanism?

“It’s up to the Chinese government as to whether they wish to tie together credit and money. In the early 1980s the US accompanied a tight money policy with an expansionary credit policy.”

I think you’re retreating to dogma. Either you address China’s particular economic quandary on its own terms (i.e. it has a managed exchange rate) or you don’t. Assuming away the established political economy isn’t an answer for China.

8. February 2016 at 14:08

*nudge*

21. February 2016 at 19:31

*tweak*

28. February 2016 at 21:59

Third time lucky?

29. February 2016 at 19:59

Fyodor, You said:

“I think you missed my point. Base money expanded massively; NGDP did not: thesis falsified, no?”

No, read what I wrote, in the passage that you were responding to.

You said in reply:

““Of course it does. The attempt to get rid of excess cash balances drives up AD. That’s monetary economics 101, isn’t it?”

No,”

What do you mean “no”? It is. If you don’t think so read some books on monetary economics. I don’t have time to teach an entire course here. Monetary economics is basically supply and demand theory. Do you also disagree with supply and demand theory? More supply of something lowers its value.

You said:

“by what mechanism?”

Hot potato effect, AKA excess cash balances are spent, driving up AD.

If China has constraints then things get far more complicated, I agree with that. I don’t see why they can’t devalue, who’s stopping them?

1. March 2016 at 19:55

“No, read what I wrote, in the passage that you were responding to.”

OK, let’s go to the tape:

S: Since things are priced in terms of base money, changes in the supply and demand for base money have a powerful impact on all nominal aggregates.

F: Except it seems that they don’t. The US monetary base has exploded in recent years, for the obvious reason, with little apparent effect on NGDP.

S: Fyodor, I said supply and demand. What happens to the demand for base money at zero rates? What happens when the Fed pays IOR at a rate higher than T-bill yields?

F: Ceteris paribus, demand for money increases, deposits at the Fed increase. This explains the accumulation of deposits at the Fed. It doesn’t reconcile the unresponsiveness of NGDP to base money explosion with your theory.

S: Fyodor, Check out my “short course on money”. Temporary monetary injections have little effect, as I pointed out in a 1993 paper, and Krugman confirmed in a 1998 paper.

F: How do you define “temporary”? The US monetary base surged more than 50% in one year seven years ago and then continued to grow at a rapid pace over following years. It’s now massive relative to its starting point eight years ago, with no material effect on NGDP. Eight years is a long time, enough time to include at least one full economic or business cycle. It’s a stretch of Keynesian proportions to call this “temporary” and it does not reconcile with your theory.

S: Fyodor, The first question is easy to answer, the Fed switched to IOR, which causes a large, one time increase in the demand for base money. Without IOR, the temporary effects last as long as you are at the zero bound. Once you exit the zero bound you tend to get the standard quantity theory results.

F: It was more than a one-time increase in base money – base money continued to climb through the QE era. Regardless, the known facts are that base money exploded and yet NGDP did not. Why not?

S: I think you missed my point. The injections were either expected to be temporary or expected to later be sterilized with higher IOR.

F: I think you missed my point. Base money expanded massively; NGDP did not: thesis falsified, no?

S: No, read what I wrote, in the passage that you were responding to.

I’ve reread what you wrote, again, and it’s clear that you have no explanation for the unresponsiveness of NGDP to the explosive growth in base money. Your rationale, if you have one, is that demand for base money leapt symmetrically to offset the supply thereof, thereby presumably nullifying the effect on NGDP that you would otherwise have expected. This is a circular evasion, which you followed with your assertion that the unresponsiveness of NGDP was a temporary effect driven by the zero bound and expectations of later sterilisation. We’re eight years into this monetary experiment and you still can’t admit that NGDP and base money are plainly not connected as your theory argues.

“What do you mean “no”? It is. If you don’t think so read some books on monetary economics. I don’t have time to teach an entire course here. Monetary economics is basically supply and demand theory. Do you also disagree with supply and demand theory? More supply of something lowers its value.”

More supply of money lowers its price relative to other goods. Whether that induces me to buy other goods, to save or to otherwise convert my money to other assets is not a direct relationship with aggregate demand, i.e. a direct impact upon demand for goods and services, as per the original point. So, no, it’s not that simple. If it were, you could explain to me why USD base money has exploded and US consumers have NOT reacted by spending their newly created “hot potatoes”.

“If China has constraints then things get far more complicated, I agree with that. I don’t see why they can’t devalue, who’s stopping them?”

Read what I wrote, in the passage where I explained it to you.