Better late than never (Kudos to the ECB)

I frequently criticize the ECB’s weird inflation target. To their credit, ECB policymakers have finally seen the light:

After years of failing to lift inflation up to its objective, the ECB has ditched its target of “close to, but below, 2 per cent”, which policymakers concluded was too opaque and implied a cap on price growth.

The central bank said its new target of 2 per cent was symmetric, “meaning negative and positive deviations of inflation from the target are equally undesirable”. The new target is a medium-term objective with flexibility to fluctuate in either direction in the short term.

This will provide more clarity and transparency to ECB policymaking.

Throughout history, central bank policymakers have often debated two issues at the same time: What rate of inflation is the appropriate goal and what is the best way to achieve that goal? This caused policymakers to split up into “hawks” and “doves”, which added uncertainty about the future course of monetary policy. If all policymakers can agree to the same goal, then the only differences are technical, not ideological. Markets would face less uncertainty.

I’m not so naive to think the ECB has entirely moved past hawks and doves, but this is a step in the right direction. The next step should be some sort of level targeting (or AIT), which would further move the bank away from the hawk/dove split and toward a more enlightened approach to monetary policy.

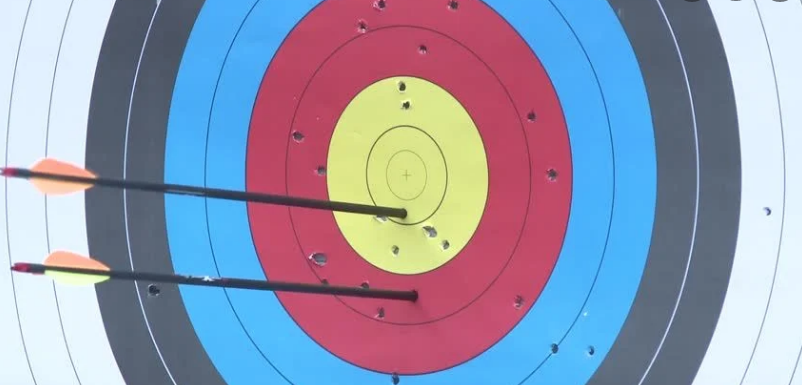

Which arrow is “close, but just below the bullseye”? The Italians would say the top arrow whereas the Germans would say the bottom arrow.

Both groups can agree that this is a bullseye:

Tags:

8. July 2021 at 14:01

This is great news.

8. July 2021 at 14:54

Eventually the Europeans can have debates about whether a few quarters of 2.3% inflation is the sign of Weimar like monetary chaos.

Although I doubt ECB would let things slip past 2.1%

8. July 2021 at 15:23

Yes, a good move, if a decade or more late. Did you see this bit though?

8. July 2021 at 15:24

Sorry – here’s the link: https://www.ecb.europa.eu/press/pr/date/2021/html/ecb.pr210708~dc78cc4b0d.en.html

8. July 2021 at 16:35

Powell dismisses the importance of the money stock.

Currency use (stimulus money) is in a downtrend:

10/1/2020 ,,,,, 0.13

11/1/2020 ,,,,, 0.14

12/1/2020 ,,,,, 0.13

01/1/2021 ,,,,, 0.11

02/1/2021 ,,,,, 0.10

03/1/2021 ,,,,, 0.09

04/1/2021 ,,,,, 0.09

05/1/2021 ,,,,, 0.08

The cash drain factor is an important signal at market turning points.

8. July 2021 at 16:47

Steve Hanke says “the money supply determines the course of nominal GDP and N-gDp includes real growth and the inflation rate”.

Chairman Jerome Powell: “there was a time when monetary policy aggregates were important determinants of inflation and that has not been the case for a long time” Powell refers to M2. So did Alan Greenspan. Neither Powell nor Greenspan knows money from mud pie. And they have Ph.Ds. in economics.

As an example, the price of oil troughed in Jan 2016 as long-term money flows fell by 80 percent from 1/2013 to 1/2016. Oil fell by 70 percent during the same period. The Trade Weighted U.S. Dollar Index: Broad, Goods and Services rose from 1/2/13 to 1/4/16 from 90.6941 to 114.1596

Why do you think stocks fell in Sept 2015 and oil bottomed in early 2016.

Parse dt; real-output; infation

01/1/2015 ,,,,, 0.05 ,,,,, 0.20

02/1/2015 ,,,,, 0.07 ,,,,, 0.19

03/1/2015 ,,,,, 0.07 ,,,,, 0.19

04/1/2015 ,,,,, 0.07 ,,,,, 0.21

05/1/2015 ,,,,, 0.07 ,,,,, 0.18

06/1/2015 ,,,,, 0.07 ,,,,, 0.19

07/1/2015 ,,,,, 0.06 ,,,,, 0.20

08/1/2015 ,,,,, 0.06 ,,,,, 0.18 China devalues Yuan

09/1/2015 ,,,,, 0.01 ,,,,, 0.15

10/1/2015 ,,,,, 0.02 ,,,,, 0.16

11/1/2015 ,,,,, 0.03 ,,,,, 0.13

12/1/2015 ,,,,, 0.04 ,,,,, 0.16

01/1/2016 ,,,,, 0.02 ,,,,, 0.14 oil bottoms

02/1/2016 ,,,,, 0.04 ,,,,, 0.12

Thus, my prediction for the bottom in oil was:

“Lags are constants but “K” is not. K is the reciprocal of Vt. The bottom isn’t Dec. but Jan. (like last year)”

8. July 2021 at 22:07

Gosh. It’s been such a long-time coming.

Funny how the FT is still so slow to get it, though. Monetary policy remains always about rates, rates, rates. Is it something about the journos (likely) very brief undergrad experience of the monetary economics bit of their general economics degree, or worse some even smaller part of a general social sciences background? Or just they never did any economics at all and such a belief is just in the ether?

9. July 2021 at 05:24

The first deceleration in short-term money flows since the March 2020 bottom, given the current trajectory, won’t occur until next month (August). On the other hand, inflation, dismissing any change in velocity (the demand for money), won’t materially subside.

Parse date; real output; inflation

02/1/2020 ,,,,, 0.05 ,,,,, 0.03

03/1/2020 ,,,,, 0.20 ,,,,, 0.21

04/1/2020 ,,,,, 0.33 ,,,,, 0.40

05/1/2020 ,,,,, 0.40 ,,,,, 0.46

06/1/2020 ,,,,, 0.44 ,,,,, 0.50

07/1/2020 ,,,,, 0.44 ,,,,, 0.53

08/1/2020 ,,,,, 0.45 ,,,,, 0.56

09/1/2020 ,,,,, 0.45 ,,,,, 0.61

10/1/2020 ,,,,, 0.53 ,,,,, 0.68

11/1/2020 ,,,,, 0.77 ,,,,, 0.79

12/1/2020 ,,,,, 0.84 ,,,,, 1.26

01/1/2021 ,,,,, 0.65 ,,,,, 1.31

02/1/2021 ,,,,, 0.66 ,,,,, 1.41

03/1/2021 ,,,,, 0.70 ,,,,, 1.51

04/1/2021 ,,,,, 0.71 ,,,,, 1.60

05/1/2021 ,,,,, 0.78 ,,,,, 1.65

06/1/2021 ,,,,, 0.79 ,,,,, 1.77

07/1/2021 ,,,,, 0.76 ,,,,, 1.81

08/1/2021 ,,,,, 0.55 ,,,,, 1.79

09/1/2021 ,,,,, 0.27 ,,,,, 1.72

The FED’s models are slow to pick up changes in the economy. And their response is even slower. Fortunately there’s not much impact to R-gDp until the 1st qtr. of 2022.

9. July 2021 at 08:42

Rajat, Yes, and that’s why they should just stop targeting prices, and switch to NGDP.

James, I’ve just given up on that issue. The mainstream will never learn.

9. July 2021 at 12:38

Is it really just the journalists? Seems like a problem with a good bit of the economics profession.

Steve

10. July 2021 at 00:29

In the ‘past’?

” . . . the ECB has

70:57 been a disaster from day one it’s

70:59 created asset bubbles banking crises

71:02 massive recessions vast unemployment . . . “

“ . . . right now it’s Germany’s

71:25 turn because the ECB is now creating and

71:27 property bubble in Germany has been

71:29 since 2009 while it’s killing the

71:33 community banks the good banks they’re

71:35 all forced now to lend for property

71:37 speculation so check me out in five

71:39 years time the property bubble will

71:42 burst and the tired German banking

71:44 system will be bust and the ECB will be

71:47 responsible . . . “

https://www.youtube.com/watch?v=8FT-zyTX2nE&lc=z23dxvchbqzixx0rh04t1aokg5flnl0yyhzfwwshwgkubk0h00410.1540380500211044

“Germany’s amazing house price boom continues unabated

LALAINE C. DELMENDO | May 18, 2021

Despite the global pandemic, Germany’s long-running house price boom continues strong, thanks to low interest rates, weak construction supply, as well as the increased demand from more than 1 million refugees. In a country where the housing market has historically been extraordinarily stable, this is a significant shift.”

https://www.globalpropertyguide.com/Europe/Germany/Price-History

10. July 2021 at 00:32

“There are other significant ‘anomalies’ that have challenged the old as well as the new mainstream approaches. While theories place great store by the role of interest rates as the pivotal variable that has significant causal force, empirically they seem far less powerful in explaining business cycles or developments in the economy than theory would have it. In empirical work, interest rate variables often lack explanatory power, significance or the ‘right’ sign. When a correlation between interest rates and economic growth is found, it is not more likely to be negative than positive. Interest rates have also not been able to explain major asset price movements (on Japanese land prices, see Asako, 1991; on Japanese stock prices, see French and Poterba, 1991; on the US real estate market see Dokko et al., 1990), nor capital flows (Ueda, 1990; Werner, 1994) – phenomena that in theory should be explicable largely through the price of money (interest rates). Furthermore, in terms of timing, interest rates appear as likely to follow economic activity as to lead it.”

Towards a New Research Programme on

‘Banking and the Economy’ –

Implications of the Quantity Theory of Credit for the

Prevention and Resolution of Banking and Debt Crises

http://eprints.soton.ac.uk/339271/1/Werner_IRFA_QTC_2012.pdf

10. July 2021 at 05:35

“Inflation is not a problem for this time as near as I can figure. Right now, M2 [money supply] does not really have important implications. It is something we have to unlearn.” Jerome Powell, Chairman of the Federal Reserve.

The Federal Reserve Bank of St. Louis’ FRED DATABASE is government controlled. Before the FED discontinued the M1 money stock figures, and removed withdrawal restrictions on savings/investment type accounts, it revised M1 with M2 data, destroying the history of the time series. I smell a rat.

10. July 2021 at 06:09

Richard Warner is crazy too. Banks aren’t intermediaries. From a systems viewpoint, commercial banks (DFIs), as contrasted to financial intermediaries (NBFIs): never loan out, & can’t loan out, existing deposits (saved or otherwise) i.e., in any deposit classification, or the owner’s equity, or any liability item.

Every time a DFI makes a loan to, or buys securities from, the non-bank public, it creates new money – demand deposits, somewhere in the system. I.e., all bank deposits are the result of lending and not the other way around.

Dr. Alton Gilbert (in “Requiem for Regulation Q, What it Was and Why it Passed Away” the Fed’s research staff’s Bible).

The implicit, and unambiguously fabricated, premise in this question is that time (savings) deposits, are a source of loan-funds to the commercial banking system. I.e., the deregulation of interest rates for just the banks (the nonbanks were deregulated prior to 1966) is a ruse.

No, all bank-held savings are an unrecognized leakage in Keynesian National Income Accounting.

10. July 2021 at 07:24

re: ” as income velocity that cannot but impress anyone who works extensively with monetary data” (Friedman, 1956, p. 21).

Or (WSJ, Sept. 1, 1983)

Friedman bastardized the equation of exchange that he had printed on his car license plate. The transactions’ velocity of money has sometimes moved in the opposite direction as income velocity.

10. July 2021 at 07:47

re: “the ‘mystery of the missing money’ (Goldfeld et al., 1976).

The transactions velocity of money was a statistical stepchild. I.e., virtually all the demand drafts that were drawn on DFIs, the CUs, S&Ls, etc., cleared through DDs – except those drawn on MSBs, interbank & the U.S. government.

If you look at 1974-1975 you’ll find Vi rose while Vt fell.

10. July 2021 at 11:08

Steve, Unfortunately, you are correct.

22. June 2022 at 11:38

Sorry for not keeping up. I have now read your ECB post. It is great they’ve abandoned the <2% inflation target. But … just like the Fed it’s resulted in equal confusion and probably too loose monetary policy as Euro-HICP just hit 8% YoY. It seems Central Banks have moved as one to something no one quite finds credible.

Focusing on Euro-Area NGDP as you suggest, that seems outta control too -after exact same initial covid success as elsewhere – eg the US.

https://fred.stlouisfed.org/series/EUNNGDP#0

So, back to my original question, have you over-focused on the Fed and not noticed the same confused monetary situation worldwide?

22. June 2022 at 13:01

Ignore this, I clearly read the wrong post! Sorry. My correct comment is your latest blog. The link still works, as does my question.