Belarus has no trouble generating inflation

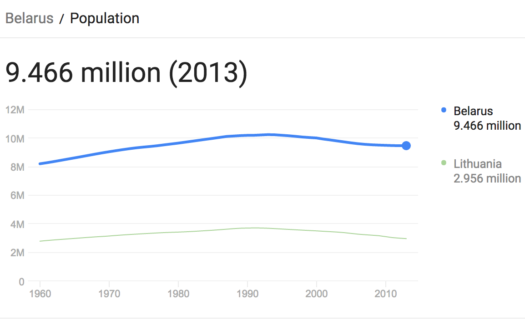

Harding directed me to the example of Belarus, which like Japan has a falling population in recent years:

And yet Belarus has lots of inflation:

And yet Belarus has lots of inflation:

Not as bad as the 100% inflation of 2012, but still running around 10% per year in recent years, despite a falling population.

Not as bad as the 100% inflation of 2012, but still running around 10% per year in recent years, despite a falling population.

So why do demographics cause deflation in Japan but not Belarus? Simple, demographics don’t cause deflation in Japan, or anywhere else.

If you have the right model of money, the world is a much less confusing place.

Tags:

19. March 2017 at 20:27

Even more importantly, the real GDP of Belarus has…are you ready for this?…nearly quadrupled since 2000. Or so says the World Bank.

So why are Western orthodox macroeconomists so obsessed with inflation?

I don’t know.

But if we get 2% inflation in the US. we are goners, dude, goners.

20. March 2017 at 00:05

It has long been a popular theory among historians that the Price Revolution of c.1470-c.1640 was caused by population growth.

Apparently, they had never heard of the C19th.

There is, of course, no real mystery. Vacuum pumps and silver-lead smelting increased the output of central European silver minds fivefold when silver was the dominant monetary metal. This was followed by the looting of the Aztec and Incan Empires and then the Potosi silver mountain. So, a series of monetary supply shocks (if you can all decade long events “shocks”).

Unless the entire massive increase in the supply of silver was hoarded, price rises were inevitable and duly occurred.

BTW the technological developments were a result of the mid C15th “bullion shortage”. The real price of silver arguably peaked around 1440.

20. March 2017 at 04:35

Demographics cause inflation is not a model I have ever used. However, I do think that demographics influences trend GDP growth. A greater % of elderly is often associated with slower GDP growth across countries. Central banks that use something like a Taylor rule might respond to these GDP growth shifts. But it’s not necessarily a direct impact.

Consider the U.S., there was a huge increase in the labor force in the 70s as the baby boomer generation came of age and more women entered the workforce. One way to look at it is that the easy money policies at the time were aimed at keeping unemployment down in view of the demographic shock. Demographics can influence monetary policy, which in turn may impact inflation.

Of course, it depends on what the approach of the central bank is, etc.

20. March 2017 at 05:14

Lorenzo, Interesting.

John, Yes, it does depend on the central bank’s reaction function.

20. March 2017 at 05:56

@Benjamin

What is going on with Belarus?!!? Their GDP per capita has increased nearly 6x in the same period (since 2000). Still half as high as Russia which is where you’d expect it to be, but double Ukraine. Is this what happens when you tax the unemployed instead of giving them subsidies?

Would be an interesting post Scott.

20. March 2017 at 05:58

Or maybe that’s unadjusted for inflation and it’s all inflation…

20. March 2017 at 06:07

But there is a “demographic school of inflation”!

https://thefaintofheart.wordpress.com/2013/09/07/eureka-the-great-inflation-was-the-result-of-demographic-trends/

20. March 2017 at 08:37

Belarus CB has a website in English;

https://www.nbrb.by/engl/

20. March 2017 at 09:10

https://www.nbrb.by/engl/Legislation/documents/2017_E.pdf

—————-quote————-

CHAPTER 1

MONETARY POLICY OBJECTIVE

1. The monetary policy in 2017 will continue to support sustainable and well-balanced development of the country’s economy through the maintenance of price stability.

The main objective of the monetary policy in 2017 will be bringing of inflation, measured by the consumer price index, down to 9% (December 2017 to December 2016).

CHAPTER 2

MONETARY POLICY IMPLEMENTATION

2. In 2017, the monetary policy will be still implemented in the monetary targeting regime, which implies control over money supply. Broad money supply will continue to be used as an intermediate monetary policy target and the ruble monetary base – as an operational one. The increment of the average broad money supply is forecasted at the level of 14% plus/minus two percentage points (December 2017 to December 2016).

3. Implementation of the exchange rate policy, which involves limited participation of the National Bank in the process of setting the national currency exchange rate, will be continued. Its dynamics will be formed under the influence of the fundamental macroeconomic factors and the measures of the 2 economic, fiscal, and monetary policies.

—————endquote————

20. March 2017 at 11:57

So where would you rather live, Belarus or Japan? Which has more potential? Money is neutral people. And “the Price Revolution of c.1470-c.1640” had inflation of merely 1.2%/yr on average (source: George Selgin)

20. March 2017 at 16:39

Great example. It gets tiresome listening to demographics as monetary destiny.

20. March 2017 at 17:08

This isn’t very interesting without some reasonable explanation. Anyone?

20. March 2017 at 19:19

Belarus’s chronically high inflation rate was caused by its chronically high monetary growth rate:

https://books.google.com/books?id=pzZBBAAAQBAJ&pg=PA531&dq=belarus+inflation+money+growth&hl=en&sa=X&ved=0ahUKEwj607OdzebSAhVj7YMKHUnIDAsQ6AEIOTAF#v=onepage&q=belarus%20inflation%20money%20growth&f=false

This started out as an attempt to massively extend credit to keep large enterprises afloat:

https://books.google.com/books?id=lmld75blKCwC&pg=PA168&lpg=PA168&dq=%22that+rates+of+credit+expansion+were%22&source=bl&ots=fmny-CyM0j&sig=shoVijyvofz80WDh1cirmAuEgPU&hl=en&sa=X&ved=0ahUKEwiTgPzQ0ObSAhUn2oMKHWd_A2IQ6AEIHDAA#v=onepage&q=%22that%20rates%20of%20credit%20expansion%20were%22&f=false

20. March 2017 at 23:11

In Japan the government exhorts private-sector companies to raise wages but they don’t have much incentive to do so. In Belarus, the government controls prices of most inputs and capital allocation so all large companies do what the government says. Japan’s parliament could pass laws requiring companies to increase wages or instituting price controls, but it wouldn’t be a simple decision by administrative fiat.

21. March 2017 at 03:05

It was interesting thoughts, that Belarus tax the unemployed instead of giving them subsidies, but it’s novelty in their politics, which interrelated to Soviet times.

But Belarus example is very interesting in terms of rapid growth with high inflation and number of economic meltdowns. And protectionism policy, sure…

21. March 2017 at 03:40

Scott,

Some insight into the BoE decision-making process. Not entirely awful, but ample room for improvement:

http://www.bbc.co.uk/news/business-39332826

21. March 2017 at 17:01

Thanks W. Peden.