Are recessions about employment?

I’d say yes, but Nick Rowe disagrees. He recently tweeted an old post from 2015, which ends as follows:

Recessions are not about output and employment and saving and investment and borrowing and lending and interest rates and time and uncertainty. The only essential things are a decline in monetary exchange caused by an excess demand for the medium of exchange. Everything else is just embroidery.

First I’m going to tell you why I disagree, and then I’ll explain why my disagreement is not very important, at least for the US economy.

I don’t believe that terms like “monetary exchange” and “excess demand” are clearly defined. In my view, the most useful definition of a recession is a slowdown in employment growth that is sudden, significant and in some sense “anomalous”. By that I mean a slowdown in employment growth that seems unrelated to fundamental factors such as demographics or preferences.

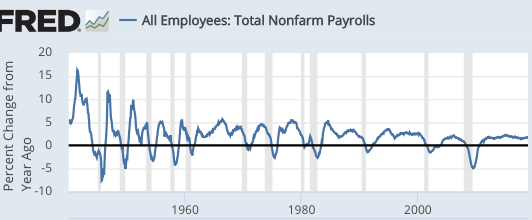

As this graph shows, slowdowns in employment growth are extremely strongly correlated with “recessions”, as defined by the NBER. (The end of WWII was a bit weird. But that was an unusual period, with women entering the labor force during the war, then leaving, and soldiers returning home.)

Thus in an accounting sense, recessions are mostly about employment, not factors such as productivity. And most economists believe the reduction in employment during recessions is non-optimal, that it does not reflect preferences. So what causes this slowdown?

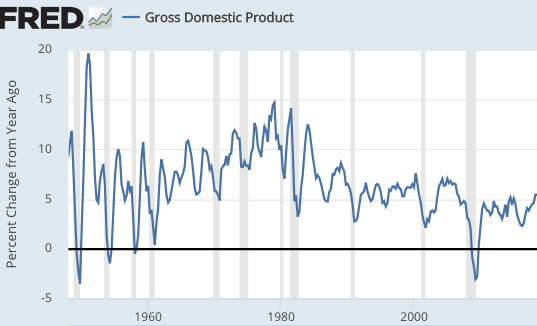

In my view (and I think Nick agrees), these recessions are caused by sharp declines in NGDP growth in an economy with sticky wages and prices. Here is some data on NGDP growth:

Once again, the correlation is quite strong. At the same time, I could easily imagine other factors causing a recession. A government might institute an extremely high minimum wage rate, and then later remove this wage floor. This would temporarily depress employment growth, without impacting NGDP. So I don’t see how recessions can always be caused by an excess demand for money, unless they are defined that way. But since we cannot directly measure excess money demand, that’s not a useful definition. All we can do is look at various macro variables and infer that there was an excess demand for money.

Once again, the correlation is quite strong. At the same time, I could easily imagine other factors causing a recession. A government might institute an extremely high minimum wage rate, and then later remove this wage floor. This would temporarily depress employment growth, without impacting NGDP. So I don’t see how recessions can always be caused by an excess demand for money, unless they are defined that way. But since we cannot directly measure excess money demand, that’s not a useful definition. All we can do is look at various macro variables and infer that there was an excess demand for money.

Nor can we solve the problem by looking at the other part of Nick’s definition, a “decline in monetary exchange”. If monetary exchange suddenly falls in half, and all wages and prices are cut in half by administrative fiat, there may not be a recession. Indeed something like this occurs during a currency reform.

[Please don’t misinterpret this observation. I am not claiming that making wages and prices flexible is a good way of avoiding recessions, it isn’t. Rather the thought experiment shows that a recession is not identical to a decline in monetary exchange. And keep in mind that NGDP is only a tiny fraction of “monetary exchange”, which is dominated by the exchange of money in the financial markets.]

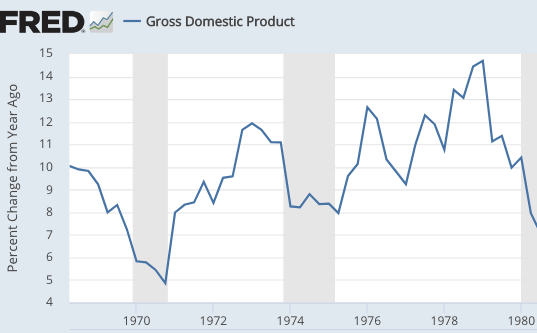

Let’s look at the recession that is generally regarded as the least monetary of all post-WWII US recessions, November 1973 to March 1975:

That graph is actually pretty good for Nick’s claim, as even the least monetary of all recessions looks quite monetary. NGDP growth slowed significantly during the 1974 recession.

That graph is actually pretty good for Nick’s claim, as even the least monetary of all recessions looks quite monetary. NGDP growth slowed significantly during the 1974 recession.

On closer inspection, we can see why this is viewed as the least monetary recession. The slowdown in NGDP growth was fairly mild compared to other recessions, whereas the fall in employment growth and RGDP was relatively severe, at least for the post-1965 period.

Many economists would attribute this to 1974 being an adverse “supply shock”, caused by soaring oil prices. I’m not so sure, as the equally severe 1979-80 oil shock produced a boringly normal recession; that double-dip recession was about as severe as one would expect from the size of the NGDP growth slowdown in early 1980, and then again in 1981-82. So even that double-dip “oil shock” recession looks quite monetary.

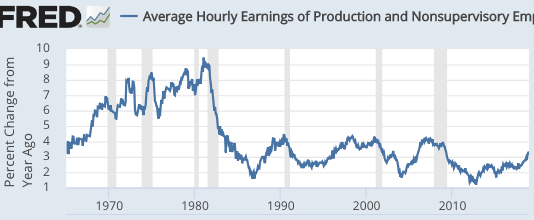

Instead, I believe the unusual severity of the 1974 recession reflects a “wage shock” caused by the removal of wage controls. These same controls had artificially boosted output during 1972 (when Nixon just happened to be running for re-election), and we paid the price in 1974 (when Nixon was fittingly removed from office.) As a result, wage growth actually rose during the 1974 recession.

Rather than define a recession as a negative monetary shock that causes less monetary exchange, I’d rather say that a recession is a sudden, sizable, and anomalous slowdown in employment growth. And then I’d say that US recessions are virtually always caused by monetary shocks that reduce NGDP growth, but in other countries (such as Venezuela and Zimbabwe) recessions are often caused by real shocks–usually bad (interventionist) government policies.

PS. I understand that the correlation between NGDP and recessions doesn’t prove causation, but we have a mountain of other evidence suggesting that causation goes from monetary variables such as NGDP to employment.

Tags:

20. January 2019 at 17:52

Scott: A thought-experiment. Monetary tightening, sticky nominal wages, lots of workers lose their jobs, and have to work even more hours than before, digging their own gardens by hand, to produce enough food to eat themselves (home production), to stay alive. Hours worked (“employment”) actually increases, even though monetary exchange falls. I would call that “a recession”.

1. Exchange makes people better off (whether we are talking about a pure endowment economy, or a more complicated economy with production and employment, doesn’t matter for that principle).

2. Exchange is very difficult without money (except in a very simple economy where direct barter is easy, but it usually isn’t).

3. A shortage of money (excess demand for money) will make exchange more difficult (it’s harder to sell stuff for money), so fewer goods will be exchanged (though some will resort to barter or home production, despite the inefficiencies of doing that).

4. So people will be worse off. (the economy is not coordinating the allocation of resources as well as it could be doing, given technology, preferences, and resources).

5. We call that “a recession”.

20. January 2019 at 22:21

Isn’t it endogenous if you say GDP is correlated with recessions if the very definition of recession is negative GDP QoQ for two consecutive quarters (Q)?

20. January 2019 at 23:50

Was that 2016 slowdown in NGDP a recession? It wasn’t for Scott but may have been for Nick and Marcus Nunes. And for the US electorate who promptly elected Trump.

21. January 2019 at 00:07

In the 1980s, French unemployment went up and stayed up since then. I have read that through the early-90s, people would say it was a recession and expect it would end and unemployment would go down to below 5% as it had been before, but eventually it just became a new normal and nobody calls the 1980-2019 period “the Big French Recession”: 8% unemployment is now considered the normal in France.

The 1972-4 example is maybe atypical in that a bad policy was quickly reversed. If wage controls had lasted into the mid 1990s, would people talk of the 1972-96 recession?

21. January 2019 at 03:31

Luis, the Germans had a similar 1980s. But interestingly enough, the unemployment came down again in the last decade for them. Still a very long time of elevated unemployment.

(But the integration of east Germany was an event sui generis, and mistakes were made.)

21. January 2019 at 08:47

Nick, I completely agree. I should emphasize that when I say “employment” I mean employment in paid jobs. So the fact that the government payroll data misses people working at home is a feature of the data, not a bug. I also agree about the welfare cost.

So in my view a recession is a sudden and temporary reduction in paid employment. My point is that this sort of “recession” could also be caused by non-monetary factors, such as minimum wage laws.

Bruno, No, you are confusing NGDP and RGDP.

James, No, and it’s not even close. In the US there are no borderline recessions. Something is either clearly a recession, or clearly is not a recession. Look at the unemployment rate series if you want to see what I mean. Indeed this is one of the most puzzling aspects of the US data—why no mini-recessions?

As far as Trump, I’ve also argued that the tight money of 2016 may have put him in office. But it was not a recession–unemployment kept falling.

Luis, Good point. France has seen a big rise in its natural rate of unemployment since the 1970s. That increase typically shows up during a “recession”, but the causes go much deeper.

21. January 2019 at 10:05

Good post. Feels like an argument about semantics.

The Great Depression and Great Recession saw massive involuntary drops in paid employment. At bottom, a Central Bank exists to avoid these things, call them what you will.

21. January 2019 at 13:30

Thanks Scott. We’re not that far apart. Just I would emphasis monetary exchange for *all* things (labour, new goods, used goods, old real assets, financial assets, etc.). Labour is just one of the things traded for money.

Brian: I think it is mostly semantics. But I think it’s a bit like defining a disease: do you define the flu by the symptoms, or by what causes those symptoms? Initially, when people disagree on the cause, you define it by the symptoms. Then later you switch to defining it by the bug that causes it. And it’s always tricky, because symptoms may vary, and you might find that one disease is really two different diseases, with similar symptoms.

22. January 2019 at 08:23

Didn’t someone once say, ‘Recession is, always and everywhere, a monetary phenomenon.’

Though politicians keep trying to disprove it;

https://www.cbsnews.com/news/nyc-restaurants-cut-staff-hours-to-cope-with-minimum-wage-hike-hitting-15/

———–quote———

Jon Bloostein operates six New York City restaurants that employ between 50 and 110 people each. The owner of Heartland Brewery and Houston Hall, Bloostein said the effect of the higher minimum wage on payroll across locations represents “an immense cost” to his business.

“We lost control of our largest controllable expense,” he told CBS MoneyWatch. “So in order to live with that and stay in business, we’re cutting hours.”

Bloostein said he has scaled back on employee hours and no longer uses hosts and hostesses during lunch on light traffic days. Customers instead are greeted with a sign that reads, “Kindly select a table.” He also staggers employees’ start times. “These fewer hours add up to a lot of money in restaurants,” he said.

Bloostein said he has increased menu prices, too. “So as a result [of the minimum wage hike], it will cost more to dine out,” he said. “It’s not great for labor, it’s not great for the people who invest in or own restaurants, and it’s not great for the public.”

———–endquote———-

22. January 2019 at 11:08

“I’d rather say that a recession is a sudden, sizable, and anomalous slowdown in employment growth.”

This is the definition that makes the most sense.

Sometimes there are big drops in NGDP/RGDP growth that don’t ‘feel’ like recessions and aren’t called such. I’m thinking of 2014Q4-2016Q2 in the USA, but this also happened in other advanced economies between 2010 and 2015. The 2015 NGDP slowdown was almost as bad as 2001, the difference seems to be expectations. In 2015, the economy was growing slowly, but there was little reason to worry it was going to get worse, markets weren’t forecasting recession at least.

I’ve also wondered if the real economy doesn’t to some extent adapt to volatile NGDP (manifested as higher cash holdings and lower risk lending & business expansion). Long term NGDP stability might leave firms/households complacent and more vulnerable to NGDP shocks. If this happens, then perhaps 2015 didn’t see layoffs because everyone was ready for the ‘double dip’.

22. January 2019 at 11:47

Nick, That raises an interesting question. From my “sticky wage” perspective, tight money might not lead to less exchange of goods that were produced earlier, such as goods sold at garage sales. On the other hand, the “income effect” from a recession could perhaps reduce the sales of existing houses and used cars—it’s an issue I haven’t given much thought to.

Justin, I’d guess that much of the slowdown in NGDP during 2016 was in capital income, not labor income.

23. January 2019 at 02:38

OT but worth pondering:

Todays news—

China singles out Tencent in new crackdown

Chinese regulators shut 733 websites and killed 9,300 mobile apps in the latest round of content crackdowns.

The content removals started on January 3.

The Cyberspace Administration of China singled out Tencent’s (OTCPK:TCEHY,OTCPK:TCTZF) Tian Tian Kuai Bao news product for spreading “vulgar and low-brow content that was harmful and damaging to the internet ecosystem.”

—30—

Does this sound like an investable climate? A place to risk capital? Oh. and million Uyghers in re-education camps?

Will the (sometimes pious) Davos crowd get turned off?

23. January 2019 at 19:44

Way off topic but can one of you good Econ bloggers review Rerum novarum? From a secular POV, is there any there there from the point of scientism?

28. January 2019 at 03:47

I am not claiming that making wages and prices flexible is a good way of avoiding recessions, it isn’t.

Interesting… Care to elaborate?

28. January 2019 at 15:06

Students, I’ll let someone else handle that.

Maurizio, It’s like trying to make airplanes safer by getting rid of gravity. If you could do so then airplanes would be safer, but how likely is it that you’ll succeed?

29. January 2019 at 02:28

Scott,

Sorry to be late with this thought, but if we get to a point technologically in which there’s almost no demand for human labor, are recessions any longer a danger?

11. October 2021 at 13:27

[…] To summarize, 1) recessions and employment fluctuations are highly correlated, 2) nominal shocks have real effects, 3) hourly wages closely follow NGDP/person, 4) when the economy is hit by a negative nominal shock W/NGDP becomes highly countercyclical because nominal wages are sticky 5) W/NGDP is very useful in explaining employment fluctuations, hence the recessions.[7]Sumner, S. (2019, January 20). Are recessions about employment?. Retrieved October 3, 2021, from https://www.themoneyillusion.com/are-recessions-about-employment. […]