Another bubble? When was the first one?

This caught my eye :

There is plenty of temptation to crack open the champagne and celebrate the U.K.’s return to economic health, with even cautious Chancellor of the Exchequer George Osborne declaring victory was his.

Yet there are still several important reasons to be cautious about a series of better-than-expected economic indicators.

(Read more: U.K.’s economic recovery )

One of the most concerning is the prospect of another house price bubble forming. Interest rates have remained at a historic low for four and a half years, and the government has introduced measures like the Help to Buy scheme, where it guarantees mortgages for first-time buyers with relatively small deposits.

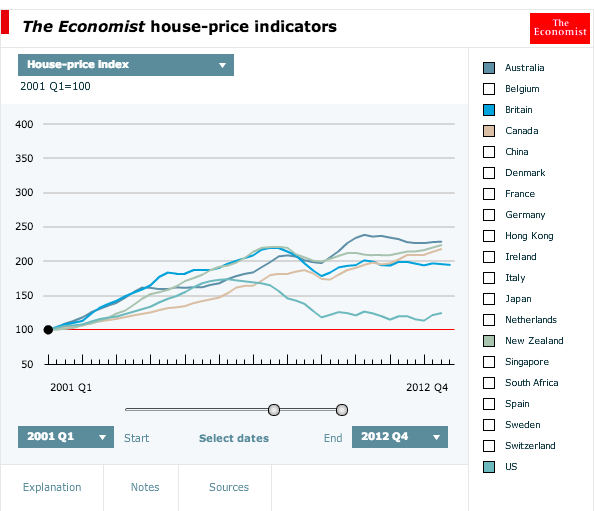

I wonder what they mean by “another house price bubble?” If it had been a US newspaper, I would have understood the comment. Many think the US had a housing bubble in 2006, although I don’t agree. But Britain? Here are house prices in 5 English speaking economies:

As you can see, the US pattern does look like a bubble, but the other four countries all show steep increases (in Britain’s case even steeper than the US), but then a leveling off, as if markets correctly saw that there were good fundamental reasons for house prices to soar in the early 2000s.

When the US index peaked at around 175 in 2006, the UK index was at around 195. It still is, even as the US index dropped back to 120. Yes, there was a small decline in UK prices during the steep 2009 recession, but what would you expect a rational, non-bubblicious market to do in the face of such an economic disaster?

So back in 2006 pundits in 5 English speaking countries cried “Bubble!!!” In 4 out of 5 of the countries they were wrong. But in 5 out of 5 cases they insist they were right, as we see from self-congratulatory advertisements in The Economist.

Unless one wants to argue that any small decline in a highly volatile asset market that had previously risen sharply is a “bubble,” there is obviously no evidence of bubbles in the four non-US cases shown above. And if you do insist that any decline in a highly volatile asset market that had previously risen is prima facie evidence of bubbles, . . . well, then I hardly know what to say.

PS. Here’s an article describing how the Chinese are snapping up a lot of properties in Sydney. Aussie labor is employed building houses. The houses are traded for Chinese goods. The only special feature is that the houses don’t physically leave Australia. Chalk up one more reason why current account deficits are an utterly meaningless number.

Tags:

14. September 2013 at 05:46

Mr. Sumner, I’ve heard you discuss the U.S. housing bubble before. Could you explain your reasoning as to why you now feel it wasn’t a bubble?

Also, do you deny that there were capital inflow bubbles in developed countries in the mid-2000s? The U.S. current account deficit peaked at, what was it, 7% of GDP?

I must admit, I’ve always bought the conventional view of the crisis: current account imbalances led to a combination of low long-term interest rates and an overvaluation of the real exchange rate, which distorted the price system and led to over-investment in real estate.

14. September 2013 at 06:57

Totally off topic. However, two things you’ve said Scott that always seemed really wrong to me-your defintion of stagflation as low GDP and high inflation-rather than high inlfaiton and high unemployment-and that the price level is 100 times higher in Japan I’ve now seen may be less simple than I thought.

So-on stagflation at least-I owe you something of a nea culpa.

“So on stagflation Sumner wasn’t wrong but I wasn’t either, exactly. We were both kind of right but incomplete. However, I had implied that he said something ludicrous and clearly this is not true. On the price level issue it seems that it may turn on the distinction between MOA-MOE. Still ,Sadowski does admit that Sumner could have been clearer here. On a MOE basis the statement that the price level is 100 times as high in Japan as in the U.S. would be ludicrous. ”

http://diaryofarepublicanhater.blogspot.com/2013/09/mark-sadowski-responds-sumner-on.html

14. September 2013 at 07:02

Joe, I don’t believe bubbles exist because I believe in the EMH.

Australia has had perhaps the world’s largest CA deficits since 1992, and hasn’t had a single recession, so I don’t believe CA deficits are the problem. The main problem in developed countries is unstable monetary policy (unstable NGDP) and to a lesser extent moral hazard created by government backstops.

Interest rates throughout the world have been low in recent years, even in countries with huge CA surpluses (such as Northern Europe.) That’s the reality of the 21st century (Great Stagnation) economy.

14. September 2013 at 07:04

Mike, Very simple question: When I said the Japanese price level is 100 times higher than the US price level, what did people think I meant?

Answer that, and perhaps we can get somewhere.

14. September 2013 at 07:19

Dr. Sumner, I think I see just steady growth of home prices in Canada. It doesn’t look like bubbles. I rather say that steady growth of income has led to steady growth of home prices.

14. September 2013 at 07:27

Any claim of a “bubble” in US home prices has to explain why cities like Dallas, Denver, and Charlotte experienced nothing that looks like a bubble in prices, all cities that experienced a lot of growth and housing being built. Perhaps people would claim that it’s random, but I suspect that local land use policies and other supply-side policies made a difference. My tentative theory is that for creating wild price swings the worst of all possible worlds is a regulatory environment that allows all housing to be eventually built but delays it for a long time. That creates lags in the market responding to changes in the need for housing supply, and wilder price swings. (Areas that very strictly regulate new housing have other problems that I think are worse, but they generally avoid large price declines by simply restricting supply so much.)

14. September 2013 at 07:49

As a long term renter in the SE of England I’m amazed at the conclusion you draw.

If you lived in the UK and knew about all the props that have been put in place to preserve the collapse of this bubble you would, I hope, not reach this conclusion.

The UK housing market lacks any fundamentals. There are many reasons for it, including changes to pension tax, government subsidies, bank forbearance, long term cultural issues and demographics.

The big problem for analysis of the UK situation is the lack of open data. US data is analysed by many excellent sites and robust conclusions are drawn, however there is little coverage of little England. When outsiders do take a quick glance they tend to perform superficial analysis like looking at a few data points on a single graph. Which is typical of economics 🙁

14. September 2013 at 07:57

Sorry – didn’t say this explicitly – the UK housing bubble hasn’t been pricked thanks to the props. It’s a bubble that is dividing generations and building up enormous social problems that will become apparent once we remove the assumption that a demographic bulge can all simultaneously cash in. Volume is way down, the value of these assets is not achievable yet it needs to be realised for the 60+ generation to survive as many have no pensions and often remortgaged to live it up.

14. September 2013 at 08:06

It might help to start with a valid framework from which to determine whether a bubble in a housing market exists – the one we developed is very similar to the methods we developed for identifying bubbles in the U.S. stock market. The Economist’s index is a fairly clumsy measure (as it doesn’t cut through to the fundamental trends underlying the data).

The First Anniversary of the Second U.S. Housing Bubble

You’ll find links to our posts describing the contributing factors to the U.S. housing bubbles at the bottom of this post, and this link will take you to our archived posts looking at whether housing bubbles exist in Canada (no), China (no, until its stimulus, then yes), England (yes) and Australia (yes, however it was a comparatively minor event).

As for whether bubbles can even exist per the EMH, they most certainly can. If you understand that markets are really signal systems, that are subject to the influence of noise, which can vary in duration and magnitude, bubbles and other disruptive events can most certainly occur.

I’m afraid that the EMH can only really account for the basic signal portion of how markets work, which is fortunate for its continued existence since all noise-driven events end – it’s only ever a matter of when.

14. September 2013 at 08:09

Ben,

“The big problem for analysis of the UK situation is the lack of open data.”

The principle problem with UK economic data is that the Office of National Statistics runs as though it were headed by Sir Humphrey Appleby:

http://en.wikipedia.org/wiki/Humphrey_Appleby

For statistics on the UK I usually go to Eurostat, AMECO, the ECB Statistical Warehouse, the OECD, or almost anywhere rather than struggle with the ONS.

I can’t understand how UK economists can do any meaningful analysis at all with such an organization.

14. September 2013 at 08:21

Well I think what at least some thought you meant-certainly me among them- was that the price of bread in Japan was 100 times more expensive than in the U.S. Again, I may well be confused on this. Is there a difference in your mind between the price level and the exchange rate. My assumption was that there is.

14. September 2013 at 08:34

Chun and John, That’s right.

Ben, How will we know when it’s “pricked.” (And please don’t say when prices fall.)

Ironman, I don’t find the definition of EMH-consistent bubbles to be useful. The standard view is that bubbles violate the EMH, and I think that’s a more useful definition. Obviously you are entitled to use any definition you want, but I’m just explaining my use of the term ‘bubble.’

Mike, Obviously I meant that bread costing $3 in the US cost about 300 yen in Japan. What else would I have meant?

14. September 2013 at 08:53

But is that the price level or the exchange rate?

14. September 2013 at 09:15

People always say there was a housing bubble in the USA and then launch their political agendas. But the institutional commercial property market popped the same way and by equal dumps.

Ergo, forget your agendas. The Fed asphyxiated the economy in 2008, that is what happened. There were fighting…inflation, you guessed it.

14. September 2013 at 10:20

Benjamin: The Fed did asphyxiate the economy in 2008; but the housing bubble popped in 2006. The Fed faced all the financial consequences of declining home prices and kind of just puttered around for a while before ineffectively under-intervening to save an exploding financial time-bomb. It has continued to do so ever since.

Is it that surprising to see bubbles in multiple, closely related asset classes?

14. September 2013 at 12:29

Mike, Both.

Ben and Michael, The first half of the housing collapse was exogenous, but the second half, and the concurrent commercial RE collapse, was due to falling NGDP.

14. September 2013 at 12:44

Ok. That’s all I wanted-a straight answer. So the exchange rate and the price level are one in the same?

14. September 2013 at 14:06

ssumner – ‘how will we know when it’s “pricked” ‘

when social mobility comes back, which fell steadily under Labour. Housing costs are detached from wages. People can’t “work” themselves out of their class. Many in their 20s are stuck in their parents’ home, unable to become financially independent due to insane rent costs. Not that this is on the graph from The Economist.

Still the shape doesn’t look like there is a problem so maybe my living in the UK and following (and living) this problem isn’t as good as a qualified economist armed with a graph and experience on making statements about the “pattern”.

“as if markets correctly saw that there were good fundamental reasons for house prices to soar in the early 2000s.”

Come on! There are many reasons as I enumerated in my last post. None of them were because the UK was on some kind of new plateau. Also your graph starts in 2001. Nobody in their right mind in the UK would use this graph starting in 2001. Labour came in and pumped from 1997. Start from 2001 and you get ~200 increase on this index, from 1997 it’s over 250.

I can’t even see how you got that graph. This page shows the UK *way* out of whack for every indicator:

http://www.economist.com/blogs/dailychart/2011/11/global-house-prices

Also the UK did peak and fall back a bit as things deflated slightly. Plus there is no discussion of volume nor regional variations, which are massive in the UK thanks to the insane city state that is London.

Mark A. Sadowski – UK stats are so bad by design. As you note Appleby was no fool. He was a mendacious toad. Just another example of a lack of openness in the UK.

14. September 2013 at 15:01

Sumner the price level vs. the exchange rate http://diaryofarepublicanhater.blogspot.com/2013/09/sumner-and-difference-between-price.html

14. September 2013 at 15:08

Scott, does the EMH apply to to mixed economies, though? Unless you’re proposing that political economies are always efficient?

Some of the (admittedly amateurish) research I’ve done on domestic poverty issues in the U.S. are cases of government-driven fiscal failure; for example, the government messes up the real exchange and interest rate of a given geographic region, which causes the price system to fail. I don’t think this validates (or invalidates) the EMH.

I’ve always thought of the mid-2000s capital surge to developed economies as a similar phenomenon: was it truly a natural, market-driven event, or was caused by sovereign distortions of global financial markets?

After all, foreigners didn’t invest heavily in the U.S. in the 19th century (when we were also running sustained CA deficits) simply to improve their own country’s external asset position; they did it because America’s potential growth rate warranted it.

Would private markets have invested as heavily in the U.S. in the 2000s in the absence of sovereign distortions?

14. September 2013 at 15:59

The US did not have “a” housing bubble. Specific places in the US had surges than collapses in housing prices. Indeed, that the US has such variable housing markets is part of the reason why there were price collapses–houses cannot move but people can, so there was, in effect, a person-arbitrage effect which blocked how big the differences in housing prices could get. Andy Harless’s point about whether saving was “pushing on” investment or vice versa has explanatory power, but a lot more when asset-supply is rationed. (In China that extends to lack of reliable saving options–see

http://brontecapital.blogspot.com.au/2012/06/macroeconomics-of-chinese-kleptocracy.html–which affects the Chinese appetite for, amongst other things, US securities and Australian houses.)

As for the UK situation, the problem is not a “bubble”, the problem is rationed land-use. This leads to both blockages in social mobility and greater instability in housing prices.

14. September 2013 at 16:17

Bugger, my link grew unhelpfully. It was to

http://brontecapital.blogspot.com.au/2012/06/macroeconomics-of-chinese-kleptocracy.html

BTW The attraction to Chinese of US treasuries replicates a former pattern when the scale of the Chinese economy and deficiencies in Chinese political economy led to an apparently endless demand for liquid assets produced by the dominant Western Hemisphere Power.

http://skepticlawyer.com.au/2013/06/10/things-fall-apart-the-centre-cannot-hold-a-post-somewhat-about-china/

14. September 2013 at 16:42

“As you can see, the US pattern does look like a bubble, but the other four countries all show steep increases (in Britain’s case even steeper than the US), but then a leveling off, as if markets correctly saw that there were good fundamental reasons for house prices to soar in the early 2000s.”

NEVER REASON FROM A PRICE CHANGE.

That isn’t what bubbles are. Bubbles are not rapid increases and then decreases in prices.

Bubbles are something “real.” They are times during which scarce resources are allocated into physically unsustainable projects in the division of labor.

Once the errors are revealed, real capital is liquidated and re-allocated (as well as labor).

Most of the time these events are associated with rapidly rising prices and then falling prices, but this is not the core of the nature of bubbles. They are a possible consequence.

A central bank can always “make it look like there are good fundamental reasons for prices to soar” by simply printing so much money that present and future prices are greater than past prices.

Dr. Sumner is, like most positivists, erroneously trying to identify bubbles by looking at past prices.

That there was a housing bubble in the US isn’t proven or validated by observing housing prices over time. For if Bernanke printed 10 times more money 2008-2010 than he did, then housing prices likely would not have fallen. But this doesn’t mean there wasn’t a housing bubble! The existence of a housing bubble is predicated on the nature of the housing market (and the rest of the market) in the present, not what Bernanke may or may not do in the future.

If there is a housing bubble, it isn’t contingent upon future choices by central bankers. Bernanke of the future cannot change the economy of the past.

NEVER REASON FROM A PRICE CHANGE.

14. September 2013 at 18:34

Mike Sax, No, they are not the same thing.

14. September 2013 at 21:01

OT but relevant question for Sumner:

Michael Woodford talks some about whether the increase in the monetary base (done through QE or helicopter drops) is permanent. He hints it does not really matter as the Fed could make it permanent simply by continuously buying bonds as old ones mature, I guess.

I suspect it matters, and that it should be clear that increases in the monetary base are permanent. I do not like the idea that the Fed eventually has to either sell the QE hoard and extinguish the cash it receives (rather then transfer to Treasury), or let the bonds mature and then extinguish the cash.

I think there should be a mechanism for printing money and making it stick, in short. What’s the point in printing more money if the Fed also promises to take it away someday?

14. September 2013 at 21:14

MichaelM:

No, I expect commercial real estate to pop just the same as residential, as it is leveraged just the same. You have heavily leveraged purchases in a declining economy…you get a gathering collapse.

Why “gathering”?

Banks will lend on real estate; they consider it collateral. They are happiest lending when values of rising, and that helps create the top. Oddly enough, banks lend heaviest just when it is most dangerous to do so–near the top.

Again, strangely enough, after a real estate collapse, banks remain chary of lending, even though after the plummet is the safest time to lend—so they exacerbate the trends on the downside too. Stupid-o-nomics at work.

This is why I contend real estate is “sui generis” within the world of macroeconomics, and does not fit into anyone’s dogmas or theories or ideologies.

Real estate is just there, the home for huge amounts of capital, and ready to crush the banking system at any time. A simple solution might be a reg that real estate down payments, commercial or residential, be 20 percent or more.

Along with MM to keep values slowly rising

Here is a truism: Steady mild inflation in real estate will prevent banking collapses.

Actually that’s almost all you need to know.

Think about that. The dot.com bomb of the late 1990s did nothing to our banking sector.

That said, wipe out Fannie and Freddie for all I care—but then also wipe out the home mortgage interest tax deception. Oh, where did everybody go? Why is wiping out the home mortgage interest tax deduction never a topic of conversation? Hello? Yoo-hoo?

14. September 2013 at 22:52

Scott,

You know I’m basically with you on the housing boom…but I wonder, is a market like housing that lacks clear shorting and arbitrage opportunities theoretically kept out of bubbles because of EMH? Or, do you consider the rent-v-buy decision a sort of arbitrage?

15. September 2013 at 00:14

Ok. So they are not the same thing. Good, I didn’t think so either. Now as to your claim that the price level is 100 times higher in Japan-what I notice is that the exchange rate between the dollar and yen are basically $1 dollar for 100 yen.

So this is why I wondered if you considered them the same thing.

15. September 2013 at 05:40

1. The fact that human pattern recognition software is prone to seeing bubbles where there aren’t is lamentable, but not an argument against the existence of bubbles.

2. Your EMH = no bubbles view- is it really standard? Sounds tautological to me, and dependent on a simplistic view of the EMH. In financial markets particularly, the role of intermediaries, who ‘make markets efficient’ itself depends on some kind of inefficiency in the first place that they can exploit.

3. I’m inclined to think that bubbles are ‘unknown unknowns’ so there isn’t much point in bubble-ology, contra Jeremy Grantham, who, in his dotage, has decided that bubble-ology is the sine qua non of investing. Again, though, this is not an argument against their existence.

4. Contrast Warren Buffett, who is perfectly willing to accept that bubbles happen- in the short run, markets are a voting machine, in the long-run a weighing machine, but generally doesn’t worry too much about macroeconomics.

5. Looping back to #1, we’re constantly gaining insights into human behavior- a host of cognitive biases color the emotions and behaviors of even serious investors- becoming an investor is largely an exercise in self-understanding. More generally, though, you can’t be an expert in every security, and piggybacking off of the ‘wisdom of crowds’ is often an efficient strategy, except that sometimes it leads to bubbles.

15. September 2013 at 06:20

“Be greedy when others are fearful and fearful when others are greedy.”

True, false, nonsensical, other?

15. September 2013 at 06:49

Ben, The key is to set an explicit price level or NGDP targeting. That insures that enough of the new money will have to be permanent in order to hit the target.

kebko, I suppose housing is less efficient than equities, but I still think housing is a reasonably efficient market.

Brian, You said;

“Your EMH = no bubbles view- is it really standard? Sounds tautological to me,”

Not at all. It predicts that index funds will outperform mutual funds set up to take advantage of bubbles.

I don’t argue the EMH is true, I argue it is useful.

Your greed/fear maxim is probably true if the EMH is false.

15. September 2013 at 07:37

“I don’t argue the EMH is true, I argue it is useful.”

Suppose A finds utilizing EMH to be useful…to A.

Suppose B finds utilizing anti-EMH to be useful…to B.

If A and B find mutually incompatible theories to each be “useful” to their activity, then are they obligated to recognize that the opposite theory is “useful”, just not for themselves?

Does this not imply relativism?

15. September 2013 at 07:59

The EMH and mistaking beauty for truth http://diaryofarepublicanhater.blogspot.com/2013/09/sumner-emh-and-mistaking-beauty-for.html

15. September 2013 at 13:33

Scott – not sure how that last reply carries on the thread 🙂

Anyways, when looking at the UK market don’t start from 2001. You are missing the boat. Start at 1997.

Have a look into the UK in a meaningful way – I can assure you it’s a god damn mess. Our press are ignorant and our government are habitual liars so you have to dig deeper than soundbites in the mainstream.

Interesting blog, until next time you touch on UK housing, which is few and far between, have a good one…

16. September 2013 at 06:58

Ben, You need to be more specific. It does no good to say things are a mess in Britain. Things are a mess everywhere.

18. February 2017 at 10:03

[…] in the US cost about 300 yen in Japan. What else would I have meant?” http://www.themoneyillusion.com/?p=23505 I asked for clarification-is this the rate of exchange or the price level […]

15. April 2017 at 03:49

[…] I argue it is useful. Your greed/fear maxim is probably true if the EMH is false. http://www.themoneyillusion.com/?p=23505 Incidentally, I was mistaken yesterday about Greg being AWOL after my Sadowksi […]