What smart people think, and where to start

Suppose you are a bright young student who wants to get up to speed with the best of the blogosphere. I could encourage you to read Marginal Revolution, Slate Star Codex, Robin Hanson, Eliezer Yudkowsky, Scott Aaronson, Paul Krugman, Brad DeLong, Econlog, Crooked Timber, Razib Khan, Nick Rowe, David Beckworth and many other bloggers.

But you might prefer to start with this mega blog post by David Siegel, in which he offers opinions on a wide range of topics. You will be quickly brought up to speed on what smart people think about all sorts of issues. Here’s a brief excerpt, which leads into section 2:

BELOW ARE 150 QUESTIONS AND SHORT DISCUSSIONS WITH LINKS TO RESEARCH. They are not meant as short-cuts or my “opinion,” but rather as launching points for your own research. The links are more important than the text. Feel free to skip to the section that interests you, the questions are in no particular order. Here are the categories again:

NOTE: I am a rationalist. I feel most at home in the rationalist tribe. Rationalists generally see things in a similar way, and we are happy to change our minds when we see new evidence that points in a new direction. When we disagree about something, we never “agree to disagree.”* Instead, we define a suitable test and make a friendly bet on the outcome. Whoever loses is happy to give up the money in exchange for a more accurate view of the world.

DISCLAIMER! This is not investing, health, legal, or policy advice. I give a lot of recommendations here. Some may be wrong (or wrong for you). You are responsible for your own actions and outcomes.

If you are like me, you might have had the following reaction to reading his post. I have opinions on about 50% of the topics covered by Siegel. On those topics I agree with him at least 90% of the time. I can infer that his opinions on the other 50% (about which I know little) are also mostly sound. Thus I can quickly learn a lot about what the evidence suggests to a rational person by reading this long blog post. He also has lots of good methodological advice, regarding how to best approach difficult issues.

I see two areas where Siegel offers views on big issues that do not align with what smart people think. I’m not going to mention one of those areas, as I believe it would give readers a misleading impression of his overall approach and would cause some people to avoid reading his post. And you really should read it!

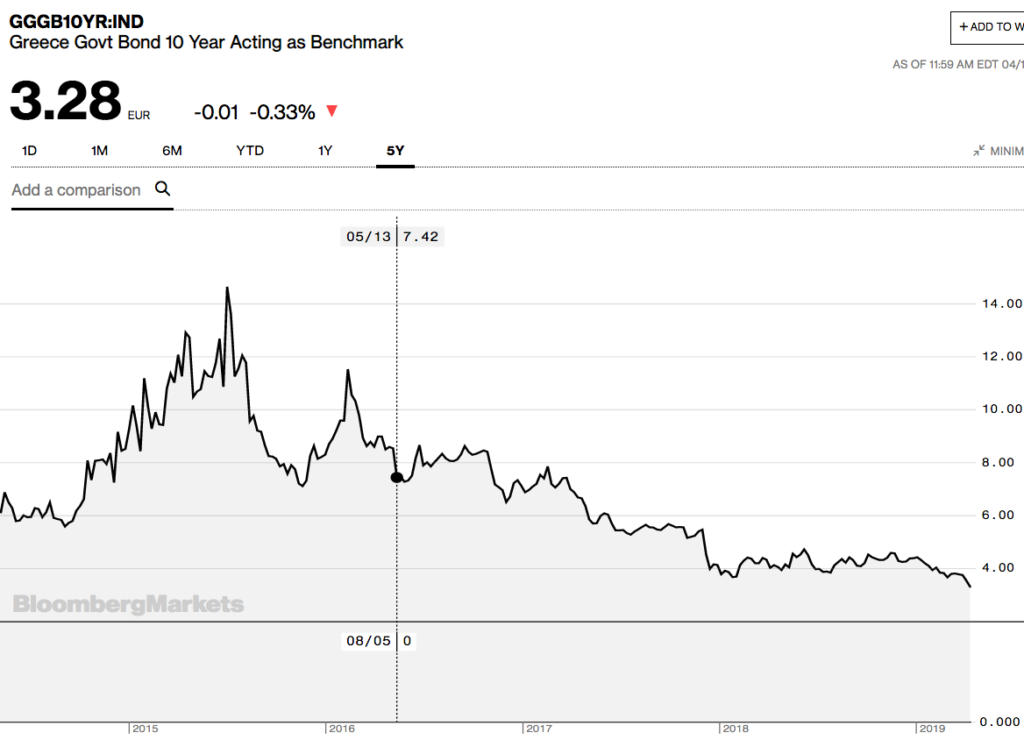

The second area where he offers a very heterodox take on a major issue is the housing bubble and the Great Recession. He pushes back against what most smart people think, and cites my views as well as those of Kevin Erdmann. He’s a market monetarist.

Now here’s an interesting question. Should this particular heterodox view cause me to have a higher opinion of David Siegel or a lower opinion? My inside view (gut instinct) tells me that I should have a higher opinion, while my outside view (dispassionate perspective) tells me that I should downgrade Siegel; it should push me a bit in the direction of viewing him as a crackpot. After all, only a crackpot would believe a Bentley professor over the best and the brightest of economics. But in the broad scheme of things these two areas don’t matter very much. His overall post is very high quality, and a good introduction into the smarter thinking in the blogosphere.

After you read and absorb this information, you’ll be ready to meet the other bloggers you read on a more level playing field.

PS. You might object “there’s nothing new here.” That’s not quite right, as he really is an expert in a few particular areas (such as cybercurrencies.) But that’s not the point. The point is that you can absorb this information in one quick reading, whereas elsewhere on the internet you’d have to read through hundreds of scattered blog posts to get all of this information.