1946

Over at Econlog I did a post discussing the austerity of 1946. The Federal deficit swung from over 20% of GDP during fiscal 1945 (mid-1944 to mid-1945) to an outright surplus in fiscal 1947. Policy doesn’t get much more austere than that! Even worse, the austerity was a reduction in government output, which Keynesians view as the most potent part of the fiscal mix. I pointed out that employment did fine, with the unemployment rate fluctuating between 3% and 5% during 1946, 1947 and 1948, even as Keynesian economists had predicted a rise in unemployment to 25% or even 35%—i.e. worse than the low point of the Great Depression. That’s a pretty big miss in your forecast, and made me wonder about the validity of the model they used.

One commenter pointed out that RGDP fell by over 12% between 1945 and 1946, and that lots of women left the labor force after WWII. So does a shrinking labor force explain the disconnect between unemployment and GDP? As far as I can tell it does not, which surprised even me. But the data is patchy, so please offer suggestions as to how I could do better.

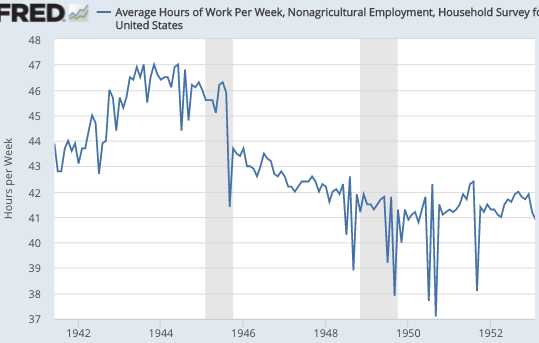

Let’s start with hours worked per week, the data that is most supportive of the Keynesian view:

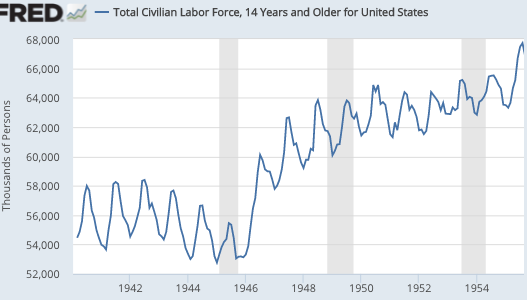

Weekly hours worked dropped about 5% between 1945 and 1946. Does that help explain the huge drop in GDP? Not as much as you’d think. Here’s the civilian labor force:

So the labor force grew by close to 9%, indicating that the labor force in terms of numbers of worker hours probably grew. Indeed if you add in the 3% jump in the unemployment rate, it appears as if the total number of hours worked was little changed between 1945 and 1946 (9% – 5% – 3%). Which is really weird given that RGDP fell by 22% from the 1945Q1 peak to the 1947Q1 trough–a decline closer to the 36% decline during the Great Contraction, than the 3% fall during the Great Recession.

That’s all accounting, which is interesting, but it doesn’t really tell us what caused the employment miracle. I’d like to point to NGDP, which did grow very rapidly between 1946 and 1948, but even that doesn’t quite help, as it fell by about 10% between early 1945 and early 1946.

Here’s why I think that the NGDP (musical chairs) model did not work this time. Let’s go back to the hours worked, and think about why they were roughly unchanged. You had two big factors pushing hard, but in opposite directions. Hours worked were pushed up by 10 million soldiers suddenly entering the workforce. In the offsetting direction were three factors. A smaller number of (mostly women) workers leaving the workforce, unemployment rising from 1% to 4%, and average weekly hours falling by about 5%. All that netted out to roughly zero change in hours worked.

So why did RGDP fall so sharply? Keep in mind that while those soldiers were fighting WWII, their pay was a part of GDP. They helped make the “G” part of GDP rise to extraordinary levels in the early 1940s. But when the war ended, that military pay stopped. Many then got jobs in the civilian economy. Now they were counted as part of hours worked. (Soldiers aren’t counted as workers.) That artificially depressed productivity.

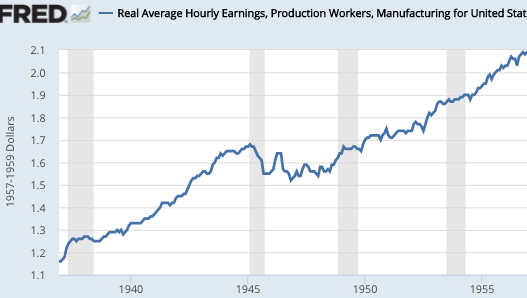

It’s also worth noting that real hourly wages fell by nearly 10% between February 1945 and November 1946:

This data only applies to manufacturing workers. But keep in mind that the 1940s was the peak period of unionism, so I’d guess service workers did even worse. So my theory is that the sudden drop in NGDP in 1946 was an artifact of the end of massive military spending, and the strong growth in NGDP during 1946-48, which reflected high inflation, helped to stabilize the labor market. When the inflation ended in 1949, real wages rose and we had a brief recession. By 1950, the economy was recovering, even before the Korean War broke out in late June.

Obviously 1946 was an unusual year, and it’s hard to draw any policy lessons. At Econlog, I pointed out that the high inflation occurred without any “concrete steppes” by the Fed; T-bill yields stayed at 0.38% during 1945-47 and the monetary base was pretty flat. Some of the inflation represented the removal of price controls, but I suspect some of it was purely (demand-side) monetary—a rise in velocity as fears of a post-war recession faded.

This era shows that you can have a lot of “reallocation” and a lot of austerity, without necessarily seeing a big rise in unemployment. And if you are going to make excuses for the Keynesian model, you also have to recognize that most Keynesians got it spectacularly wrong at the time. Keynesians often make of big deal of Milton Friedman’s false prediction that inflation would rise sharply after 1982, but tend to ignore another monetarist (William Barnett, pp. 22-23) who correctly forecast that it would not rise. OK, then the same standards should apply to the flawed Keynesian predictions of 1946.

Tyler Cowen used to argue that 2009 showed that we weren’t as rich as we thought we were. I think 1946 and 2013 (another failed Keynesian prediction) show that we aren’t as smart as we thought we were.

Update: David Henderson has some more observations on this period.

Tags:

24. September 2016 at 09:43

Scott,

See my piece on the postwar miracle at EconLog:

http://econlog.econlib.org/archives/2016/09/the_us_postwar_1.html

24. September 2016 at 10:14

Sumner: “Obviously 1946 was an unusual year, and it’s hard to draw any policy lessons” –so…Sumner attempts to draw policy lessons?

Nazi Germany also had a sort of boom when, during the mid-1930s, Hitler built the Autobahn and rearmed Germany. So?

Anomalous years don’t mean much.

PS–a good book on post-WWII Japan is Ian Buruma’s “Year Zero”. So? Well this post is full of non-sequiturs so why not?

24. September 2016 at 11:22

1946 must have been like 1921, loss of GDP without a credit crisis. I don’t know if there was a credit pause, but it was not a crisis.

That is what makes those years different from the Great Depression and Great Recession. If you can’t get a loan because banks are being procyclical, that is quite different than the short slumps of 1921 and 1946.

24. September 2016 at 12:16

Thanks David

Ray, Remind me, what are the three reasons the SRAS curve slopes upwards? And which of the three imply that money is not neutral?

24. September 2016 at 13:36

After WWII, the Fed did not cut rates at all to offset the fiscal austerity. Indeed after holding them at 0.38% for about 2 years, they began gradually raising them in mid-1947. Nor did they do any QE. And despite all that, the economy remained fine, with the unemployment rate fluctuating between 3% and 5% throughout 1946, 1947, and 1948, despite millions of men suddenly being discharged from the military. The Keynesian predictions did not come true.

So we can raise rates now, too!?

I like the last 3-4 blog posts a lot but don’t the years 1944-47 kind of disprove monetarism a bit as well? What would have been the recommendation (or prediction) of market monetarism during those years? Don’t do any monetary offset and the economy will boom like never before?

24. September 2016 at 14:42

Here’s an eyewitness to the 1946 economy;

“[A]t the end of 1946, less than a year and a half after V-J day, more than 10 million demobilized veterans and other millions of wartime workers have found employment in the swiftest and most gigantic change-over that any nation has ever made from war to peace.” —Harry S. Truman, Economic Report, January 8, 1947, p. 1

24. September 2016 at 15:34

The Summer of ’46 (Aug 9, in the NY times);

http://hisstoryisbunk.blogspot.com/2014/04/bad-news-boom-denialists.html

Economic Council to Curb ‘Boom’ First

Reading in part;

President Truman’s new Economic Advisory Council began work today with the declaration that the country must not “get into a runaway boom.”

On January 24, 1947, Times readers saw this; Economists See No Major Slump [ahead of the current boom].

Financial and public economists agreed today at the annual forecasting session of the American Economic Association that the United States was in the midst of a very large and important inflation boom.

By December of 1947 the Times headline was Economist Warns of Post-War Boom.

Business economist’ H.B. Arthur is quoted saying “we are in a stage of the boom where vulnerability is great and where some of the sustaining forces are becoming increasingly precarious.

Fear the boom!

24. September 2016 at 15:37

Then there are the pictures;

http://hisstoryisbunk.blogspot.com/2014/04/ya-gotta-ac-cent-uate-positive-e-lim-in.html

24. September 2016 at 15:56

The Fed fears the boom right now, Patrick. Jamie Dimon does to. From my article and his letter to his investors Dimon said:

“I am a little more concerned about the opposite: seeing interest rates rise faster than people expect. We hope rates will rise for a good reason; i.e., strong growth in the United States. Deflationary forces are receding – the deflationary effects of a stronger U.S. dollar plus low commodity and oil prices will disappear. Wages appear to be going up, and China seems to be stabilizing. Finally, on a technical basis, the largest buyers of U.S. Treasuries since the Great Recession have been the U.S. Federal Reserve, countries adding to their foreign exchange reserve (such as China) and U.S. commercial banks (in order to meet liquidity requirements). These three buyers of U.S. Treasuries will not be there in the future. If we ever get a little more consumer and business confidence, that would increase the demand for credit, as well as reduce the incentive and desire of certain investors to buy U.S. Treasuries because Treasuries are the “safe haven.” If this scenario were to happen with interest rates on 10-year Treasuries on the rise, the result is unlikely to be as smooth as we all might hope for.” [Emphasis mine]

http://www.talkmarkets.com/content/us-markets/jamie-dimon-is-janet-yellen-proving-will-rogers-right?post=106802&uid=4798

So, here is the deal, Dimon wants growth, but is afraid of growth, because he knows the counterparties will be screwed if there is a boom. He is admitting that a boom and a fast rise in 10 year yield would be disruptive.

Got that people? He is as conflicted about growth as Janet Yellen is. Sumner has no chance with a sustained boom. Let’s just settle for helicopter money and a little economic activity that would come from that.

24. September 2016 at 17:41

I am surprised you missed the most important point of all: the personal saving rate fell by half.

For the mechanism read Chapter 5 of “Macroeconomics Redefined” http://www.amazon.com/dp/B00ZX9O5XQ

The rate was 23.6% in 1942, 25% in 1943, 25.5% in 1944, 19.7% in 1945, 9.5% in 1946, 4.3% in 1947

See Depression, War and Cold War: Studies in Political Economy by Robert Higgs

25. September 2016 at 00:00

That 10% drop in real manufacturing wages explains a lot about why 1946 was an absolutely massive year for labor strikes. Yeselson says that about 10% of the US work-force went on strike at some point in 1946, and at its peak nearly 2 million workers were on strike at the same time.

Would that have been large enough to influence some of the statistics you provided above?

25. September 2016 at 00:39

@ssumner – I already conceded your point, cyber-bully. Now please educate us on the steepness of the SRAS curve; is it not true that the more shallow it is, the greater the effect of any money non-neutrality, but if there’s high steepness, as with high inflation or large AD fluctuations (see below), monetarism is impotent (money becomes neutral)? That according to monetarist based theory (see Mankiw below). Read the below from Mankiw, a right-wing monetary-ish economist (though his best papers were apparently on Neo-Keynesianism from what I can tell) not unlike you (though you are politically left). Concede these points: (1) high inflation and/or fluctuating unstable AD is actually counterproductive to monetary policy (by the terms of the AS/AD model), (2) low inflation and stable AD actually result in monetarism being more effective, (3) your NGDPLT could create a sort of radical fluctuation and/or high inflation that will make SRAS steep (see Lucas below) hence monetarism becomes impotent. BTW, Mankiw thinks a lot of Lucas’ ‘imperfect information’ and not so much of sticky prices / wages. A good man, Mankiw, I’ve traded email with the Great Man, as with Tyler Cowen. Don’t recall any emails from you however…

Deserves a post, or, simply ignore me like MF says, as you do when defeated? Run away professor! – RL

Mankiw, “Macroeconomics” (2003) – Chap. 8, SRAS –

“Although all countries experience economic fluctuations, these fluctuations are not exactly the same everywhere.International differences are intriguing puzzles in themselves,and they often provide a way to test alternative economic theories. Examining international differences has been especially fruitful in research on aggregate supply. When economist Robert Lucas proposed the imperfect-information model,he derived a surprising interaction between aggregate demand and aggregate supply: according to his model,the slope of the aggregate supply curve should depend on the volatility of aggregate demand.In countries where aggregate demand fluctuates widely,the aggregate price level fluctuates widely as well.Because most movements in prices in these countries do not represent movements in relative prices,suppliers should have learned not to respond much to unexpected changes in the price level. Therefore, the aggregate supply curve should be relatively steep (that is, a[alpha] will be small). Conversely,in countries where aggregate demand is relatively stable,suppliers should have learned that most price changes are relative price changes.Accordingly, in these countries, suppliers should be more responsive to unexpected price changes,making the aggregate supply curve relatively flat (that is, a[alpha] will be large). Lucas tested this prediction by examining international data on output and prices. He found that changes in aggregate demand have the biggest effect on output in those countries where aggregate demand and prices are most stable. Lucas concluded that the evidence supports the imperfect-information model. 6 The sticky-price model also makes predictions about the slope of the short- run aggregate supply curve.In particular,it predicts that the average rate of inflation should influence the slope of the short-run aggregate supply curve.When the average rate of inflation is high,it is very costly for firms to keep prices fixed for long intervals.Thus,firms adjust prices more frequently.More frequent price adjustment in turn allows the overall price level to respond more quickly to shocks to aggregate demand. Hence, a high rate of inflation should make the short-run aggregate supply curve steeper. International data support this prediction of the sticky-price model.In countries with low average inflation,the short-run aggregate supply curve is relatively flat:fluctuations in aggregate demand have large effects on output and are slowly reflected in prices.High-inflation countries have steep short-run aggregate sup- ply curves.In other words,high inflation appears to erode the frictions that cause prices to be sticky. 7 Note that the sticky-price model can also explain Lucas’s finding that countries with variable aggregate demand have steep aggregate supply curves. If the price level is highly variable, few firms will commit to prices in advance (s will be small). Hence,the aggregate supply curve will be steep ( a [alpha] will be small). “

25. September 2016 at 04:17

Hi Scott, just pointing this out, Citi write this week:

“Other ‘options’

Derivatives on inflation to regain credibility: One idea by Francesco Papadia, a former Director General of Market Operations at the ECB, is for the Governing Council to reinforce the credibility of its inflation target by entering the market in inflation derivatives. The basic idea is that ECB could offer an option that pays out to counterparties if the inflation rate was over a certain period is lower than a threshold (strike price) level. Alternatively, or perhaps as a complement, the ECB could intervene in the inflation swaps market, offering a fixed rate of inflation against floating inflation.”

25. September 2016 at 12:28

Christian, You said:

“I like the last 3-4 blog posts a lot but don’t the years 1944-47 kind of disprove monetarism a bit as well? What would have been the recommendation (or prediction) of market monetarism during those years? Don’t do any monetary offset and the economy will boom like never before?”

The interest rate and the monetary base do not describe the stance of monetary policy—you need to look at NGDP growth. I must have said this 100 times.

Patrick, Thanks for those links.

Philip, Given what happened to public saving, I’d hope that private saving fell!

Brett, I suppose that might have had some impact on RGDP growth, but probably nothing decisive.

Ray, So you now agree with Bernanke’s claim that the Fed’s tight money policy caused the Great Depression? Or are you still trying to hold on to money neutrality? If you don’t agree with Bernanke, why do you think that he is confused?

So do you now agree with Mankiw’s claim that money is not neutral? If not, why not?

Geoff, Very interesting—link?

26. September 2016 at 07:12

The interest rate and the monetary base do not describe the stance of monetary policy—you need to look at NGDP growth. I must have said this 100 times.

That was exactly the point I was trying to make. You wrote NGDP fell extremely in the beginning of the discussed period and the government “reacted” with extreme austerity that wasn’t really offset by QE or something similar.

I thought in the case of falling NGDP the recommendation of market monetarism would have been austerity as well but combined with more monetary offset.

I assume market monetarists would have gotten somewhat cold feet – at least in 1944. Of course they would not have been as wrong as the Keynesians (not at all) but I assume they would have demanded more monetary offset in 1944. Or not?

27. September 2016 at 06:49

Christian, You said:

“That was exactly the point I was trying to make.”

Then you are pretty bad at making points, as you said exactly the opposite. But if you agree with me, then great.

30. September 2016 at 17:44

Sigh, Christian’s point was clear, that NGDP did not grow, and actually fell slightly over a period of a year or two, and yet unemployment as you noted did not skyrocket.

That is an empirical falsification of the market monetarist theory. It is already refuted in theory, but 1946-7 shows it is refuted empirically as well.