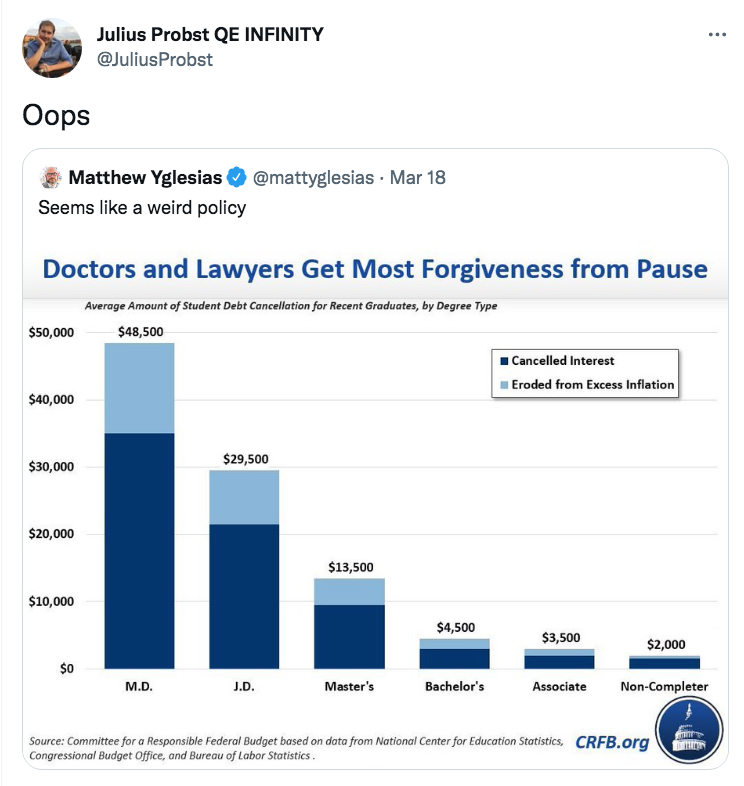

The typical Dem used to be a blue-color worker in someplace like Youngstown, Ohio. Now the party gets more votes from well-educated coastal cities. From that perspective, the following graph doesn’t seem all that “weird”, at least no more weird than the Dem’s current obsession with repealing the SALT cap.

Matt Yglesias has an excellent post on how to think about the current overheating in the US economy. Here are a few excerpts:

So NGDP, even though it’s a bit of an unfamiliar indicator, is also a very simple one. Counting up the total amount of dollars spent across the economy isn’t a totally trivial task, and the official numbers are subject to error and revision. But it is absolutely the simplest part of the whole process. Calculating the rate of inflation is a much more conceptually difficult (how do you adjust for the changing quality of restaurant meals or haircuts?) and fraught enterprise. So even though the official names tend to call inflation-adjusted quantities “real,” NGDP has always struck me as considerably more real than RGDP. The former is an actual count of defined quantities (dollars spent) while the inflation-adjusted figures are necessarily an abstraction.

Yglesias cites David Beckworth’s chart showing NGDP rising above trend, and then suggests:

I spent more than 10 years consistently thinking that the Fed was erring too much on the side of inflation aversion, and I now think the reverse. Not because I’ve changed, but because this very simple indicator — NGDP — is now giving us a different message.

Unfortunately, the Fed has set policy at a level where they are expected to fail:

What I do feel strongly about is that if I had Jay Powell’s job, I would be saying to the staff, “I’m not an economist and I don’t know how to build a macroeconomic model, but we should be choosing the policy that, when plugged into our model, gives us the policy outcome we want to see.” This concept is called targeting the forecast.

There’s only one part with which I slightly disagree:

By the book, then, they should be trying to average out the inflation of 2021 and 2022 with future years in which inflation is really low. It seems like they’re not actually going to try to do that because you’d probably have to deliberately engineer a recession in order to make it happen. So the Fed is making the correct policy choice, but that just shows that FAIT is a bad framework.

I wouldn’t call that policy framework “bad”, although I agree that FAIT is not optimal in the sense that other frameworks like NGDPLT are better. But even if the Fed had adopted a 4% NGDP level target from the beginning of 2020, the recent high inflation would end up being partly (not entirely) offset by lower than 2% future inflation, even if there were no recession. And I also agree with Jim Bullard that FAIT is pretty similar to NGDPLT, as the “flexible” part of FAIT suggests they’d allow small deviations for supply shocks.

For instance, let’s suppose that Covid permanently depressed RGDP by 1%. Then under NGDPLT you’d have 1% extra inflation over the long run. That’s not very much. Something similar could have occurred under a well managed FAIT.

The fact that suddenly dropping inflation to below 2% would trigger a recession is not an indication that FAIT is a bad policy, it reflects the fact that the Fed has not been doing FAIT, and has allowed the economy to overheat in a way that never would have happened under FAIT. If the Fed had told the markets a year ago that they were serious about FAIT, and acted like they were serious, then the markets would have done the tightening even before the Fed took any “concrete steps”. Instead we had all this happy talk about “running the economy hot”, and that’s what we got.

I mistakenly assumed the happy talk was empty rhetoric, and that FAIT was the actual policy. I was wrong.

PS. Among reporters who are not professional economists, Matt Yglesias and Ramesh Ponnuru are the two best people to read on monetary policy.

PPS. Powell has a new speech on monetary policy, which contains absolutely no discussion of average inflation, nor any sort of reference to the Fed’s new FAIT policy. The new policy is as dead as John Cleese’s parrot. Powell attributes the recent surge in inflation to supply problems, with little discussion of excessive nominal spending. He also suggests that the Fed has been tightening policy, which is incorrect.

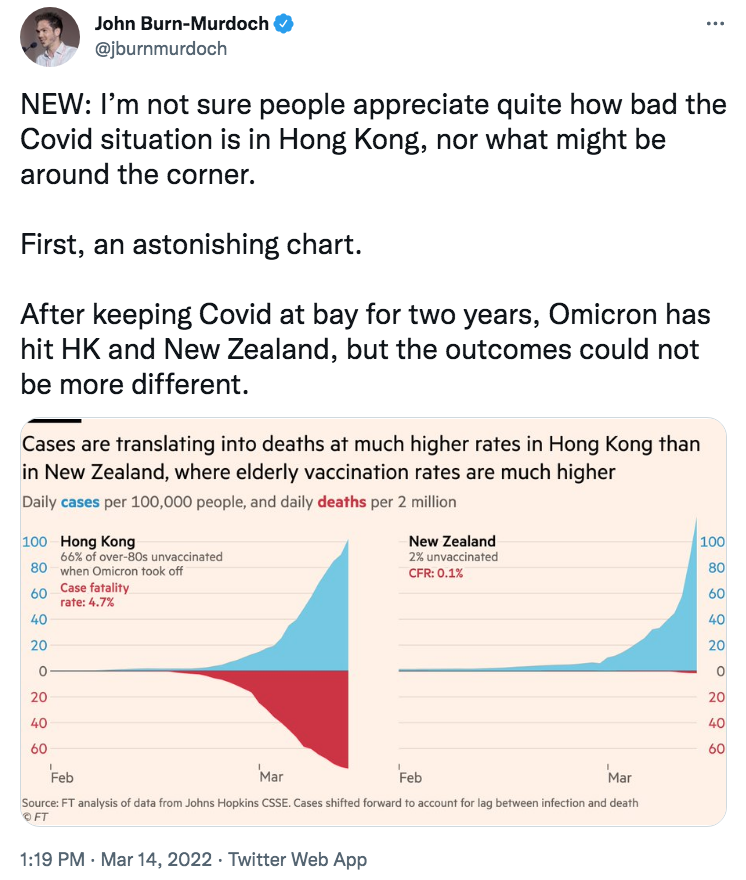

In most countries the old are more likely to get vaccinated. In Hong Kong the old are far less likely to get vaccinated. As a result:

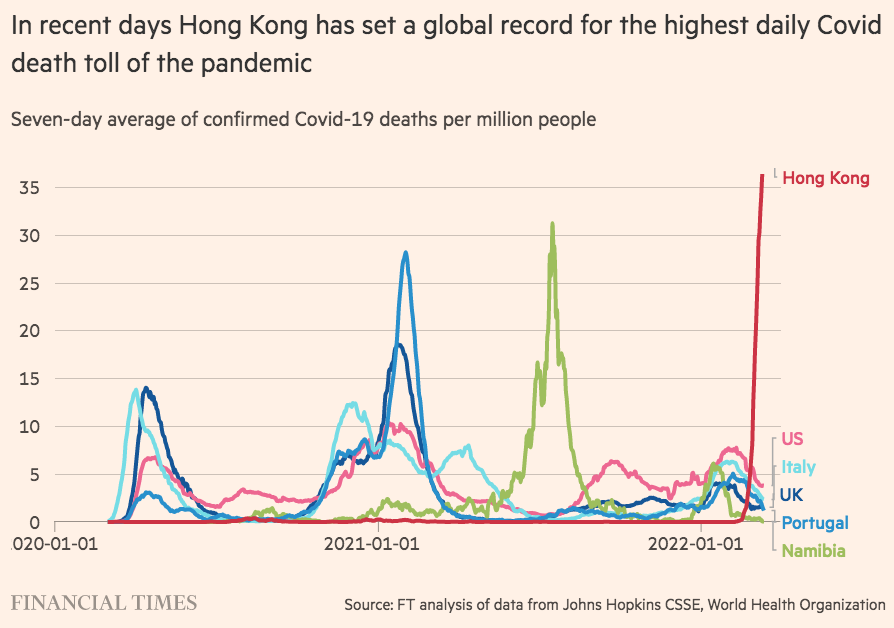

This FT article has the full story. China might be next, as they also have a huge number of unvaccinated old people. Not as many as HK in relative terms, but a vast number in absolute terms.

A couple of other points. In the past, I had commenters telling me that the Covid fatality rate in East Asia was lower than in the West for some sort of mysterious reason unrelated to behavior. We now know that’s false. Right now, the rate of Covid deaths in Hong Kong is really bad.

I also had commenters denying the effectiveness of vaccines, LOL.

I’m really worried about China, which just had its first two deaths in 14 months. Many more may soon follow.

The FT has a good article discussing the views of James Bullard and Christopher Waller on Fed policy:

In a statement released on Friday, Bullard, a voting member of the policy-setting Federal Open Market Committee, said a half-point rate rise — a tool that has not been used since 2000 — would have been “more appropriate” than the Fed’s quarter-point increase, given the strength of the labour market and broader economy, as well as the “excessive” level of inflation. . . .

Bullard noted on Friday that US monetary policy had been “unwittingly easing”, as rising price pressures have pushed short-term “real” or inflation-adjusted rates lower and kept them well into negative territory. At these levels, rates remain highly stimulative, spurring borrowing and the very demand the Fed is seeking to dampen.

Biden should have picked Bullard to chair the Fed.

Waller also has some interesting observations:

Christopher Waller, a Fed governor, said in an interview with CNBC on Friday that though data were “screaming” for a half-point move this week, geopolitical tensions justified proceeding with “caution”.

However, he backed a “front-loading” of interest rate increases this year, which he said implied half-point rate rises “at one or multiple meetings in the near future”.

How high does the Fed need to raise rates to control inflation? It depends on what sort of monetary policy they adopt.

The Fed would not have to raise interest rates as high with a tighter monetary policy as it would with a looser monetary policy. When it abandoned FAIT, the Fed made monetary policy much looser, hence they’ll have to raise rates higher than if they had stuck with FAIT. As a result, there is more likelihood that the yield curve will invert.

The Money Illusion got off to a good start in early 2009. All I had to do is to point to the obvious fact that monetary policy was far off course.

By the mid-2010s, things got boring. I was beating a dead horse.

By the late 2010s, TMI hit rock bottom. Monetary policy became quite reasonable and I pivoted to moronic Trump bashing.

Now I’m back. Even better, I get to play a different role, a scarier bird.

It wasn’t until September 2008 that it dawned on me that monetary policy was clearly too contractionary, even though in retrospect policy had been too contractionary for several months. I assumed the Fed had an effective regime in place. It didn’t.

It wasn’t until late 2021 that it became clear to me that monetary policy was too expansionary, even though in retrospect policy had been too expansionary since mid-2021. I assumed the Fed had an effective regime in place. It didn’t.

[Memo to myself: Don’t assume the Fed has an effective regime in place.]

After FAIT was announced in August 2020, I made a forecast. Here’s the entire post:

Powell says there’s no strict mathematical formula; but it’s pretty obvious to me that the markets and pundits are going to hold the Fed accountable. People think in terms of decades, and this policy was announced in 2020. Thus markets will naturally see this a commitment for inflation to average 2% over the 2020s. Since the PCE price level was 110.917 in January of this year, it needs to be close to 135 in January 2030. A slight miss would not be a problem, but a big miss (say average inflation outside the 1.8% to 2.2% range) would be seen as a policy failure. The Fed would lose credibility.

At the time, inflation had been running well below 2% since January. The 10-year TIPS spread was 1.72%, implying about 1.47%/year PCE inflation. Put the two together and the market was expecting the price level to be almost 6% too low at the end of the decade.

At that point I wasn’t too concerned, as I figured that Covid might be distorting markets. But many commenters complained that the Fed’s policy clearly had no credibility, and that they would obviously fail to raise average inflation up to 2%. Little did they know.

In April 2021, the PCE first moved above the 2% trend line from January 2020. The 10-year TIPS spread was 2.33%, implying 2.08% PCE inflation. Everything looked fine. Powell’s policy had worked.

But as I’ve pointed out in previous posts, all macroeconomic policies eventually fail. All of them. Nonetheless, this one failed sooner and more spectacularly than I anticipated.

We are two years down the road and can no longer use 10-year TIPS spreads. The 5-year TIPS spread is 3.48%, implying 3.23% PCE inflation. The 5-year, 5-year forward spread is 2.24%, implying 1.99% PCE inflation for those last three years of the 2020s. So the TIPS markets are expecting an extra 6.1% inflation (all in the next 5 years). But it’s even worse. The actual PCE is already 3.5% above the trend line from January 2020. Thus markets are expecting an extra 9.6% inflation over the 2020s, almost 1%/year. That would represent a major failure of FAIT.

[This is why we need level targeting. Think how much the point estimate of the PCE on January 2030 has changed over the past 18 months—from almost 6% below target to 9.6% above. That’s crazy. And it’s in 2030, so presumably it has nothing to do with Covid or supply bottlenecks]

In retrospect, I paid too much attention to Fed promises to target the average inflation rate. This January, Powell basically admitted that he had abandoned the FAIT policy, when he denied that a period of above 2% inflation needed to be offset by below 2% inflation in future years. Smarter observers like Bob Hetzel focused on how the language used by Fed officials echoed statements made in the 1960s and 1970s, when they also tried to “run the economy hot” to create jobs. (Kudos to Larry Summers and Tim Congdon as well.) I thought that happy talk was empty rhetoric to please the administration. I thought FAIT would be maintained. I was wrong.

The abandonment of FAIT will make the Fed’s job much harder, dramatically increasing the risk of recession. Because this policy was abandoned, inflation expectations have driven NGDP growth much higher in recent months than if markets had anticipated that the Fed would tighten enough to keep long run inflation at 2%. (Think of a loss of credibility as boosting velocity, if you wish.) Because the economy got so hot, it will take a much more contractionary policy than otherwise to bring it back down. It’s not about interest rates, it’s about the policy regime.

Here’s what I said last July, before I understood that the Fed had abandoned FAIT:

I don’t expect a recession to occur in the next few years, but recessions are almost impossible to predict. It’s more interesting to think about the sort of policy mistakes (were they to occur) that might lead to a recession within a few years.

One mistake would be an excessively tight money policy, which could trigger a recession in 2022 or 2023. That’s possible, but seems quite unlikely at the moment.

A slightly more likely scenario would involve excessively expansionary monetary policy, which drove wage growth to levels inconsistent with 2% inflation over the long run. To get the inflation rate back on target the Fed would then need a tight money policy, which might trigger a recession. . . .

Almost no one wants a recession in 2024. If we get one, it will be due to the misguided policies of people trying to help workers. They would overstimulate, and by 2023 the Fed would be forced to tighten to restore inflation credibility. I don’t think that’s the most likely case; rather it’s the most likely cause of a near-term recession should a recession occur.

Powell will need the skill of that airline pilot who landed the plane in the Hudson River to engineer a soft landing.

Welcome to a new blog on the endlessly perplexing problem of monetary policy. You’ll quickly notice that I am not a natural blogger, yet I feel compelled by recent events to give it a shot. Read more...

My name is Scott Sumner and I have taught economics at Bentley University for the past 27 years. I earned a BA in economics at Wisconsin and a PhD at Chicago. My research has been in the field of monetary economics, particularly the role of the gold standard in the Great Depression. I had just begun research on the relationship between cultural values and neoliberal reforms, when I got pulled back into monetary economics by the current crisis.

"Scott, not sure your Phoenix real house price graph proves your point. Not earining anything in real terms for twenty years on your biggest asset (seen as low risk, and..."

"Scott, "Actually, Fisher’s claim was probably reasonable. Stock valuations were not out of line in 1929, and the crash occurred because of a severe economic depression that almost no one..."

"Scott, "...Perhaps Africans cannot handle democracy?.." Don't get whether you are being sarcastic here, but isn't "us vs. them" a defining feature of democracy? How on earth do you rally..."