By all means support Trump. By all means vote for Trump if you wish (I’d prefer you didn’t). But stop the insanity! Stop making excuses for Trump.

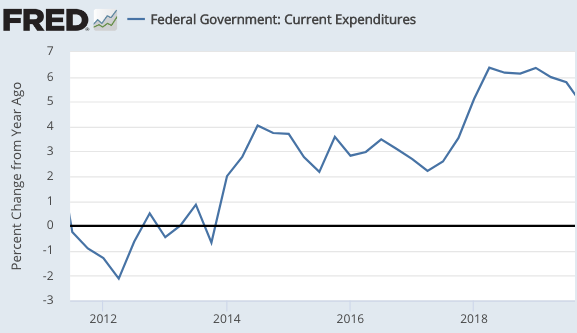

A few months ago, multiple commenters told me that Trump wasn’t to blame for the excessively large CARES Act. To get needed aid, he had to acquiesce to the demands of the big spending Dems in Congress.

Sorry, but that’s not true:

“Here’s the problem: she doesn’t want to do anything until after the election, because she thinks that helps her,” Trump said on Fox News Tuesday. “I want to do it even bigger than the Democrats. Not every Republican agrees with me, but they will,” he also said, reiterating that he’s willing to go beyond the $2.2 trillion top-line number Democrats favor.

Trump is more of a socialist than Pelosi. Deal with it. He also favored big spending increases during 2018-19, even though spending growth would normally slow during a boom, as programs like unemployment compensation decline.

So by all means support Trump (I hope you don’t.)

But stop pretending that the GOP is forced into these big spending packages.

In the entire history of the world, only one man has ever been forced to get drunk (Cary Grant in North By Northwest.) Donald Trump is no Cary Grant. If someone’s drunk with spending, we can safely assume they chose to end up in that condition.

PS. At $2.2 trillion, this is the most expensive election in global history. American elections cost more than the GDP of all but a handful of countries. And I haven’t even included the absurdly large farm welfare spending that’s already been paid out to all those lazy single moms, er, I mean to all those rugged individualist farmers in the heartland.

How about letting the market work? Why not let the price of monoclonal antibodies rise until supply equals demand?

If we did so, a thousands medical ethicists would scream about how rationing by price favors the rich.

Suppose instead that we ration by political power—give it first to people with lots of clout:

The most immediate opportunity comes from antibody drugs that can be used both as treatment and prophylaxis. President Trump and former New Jersey Gov. Chris Christie both recovered after they received antibody combinations when their symptoms were worsening. These medications are likely to be most effective when used before or soon after symptoms begin. . . .

The federal government is working on a system to control distribution, essentially sending limited supplies to states in proportion to their expected eligible patients. Governors would allocate the drugs to hospitals, as happened with the antiviral drug remdesivir.

In pre-modern times there was almost no hyperinflation, at least for extended periods of time. That’s because kingdoms mostly relied on some sort of commodity money. Thus you did not observe the sort of inflation we see under fiat money regimes.

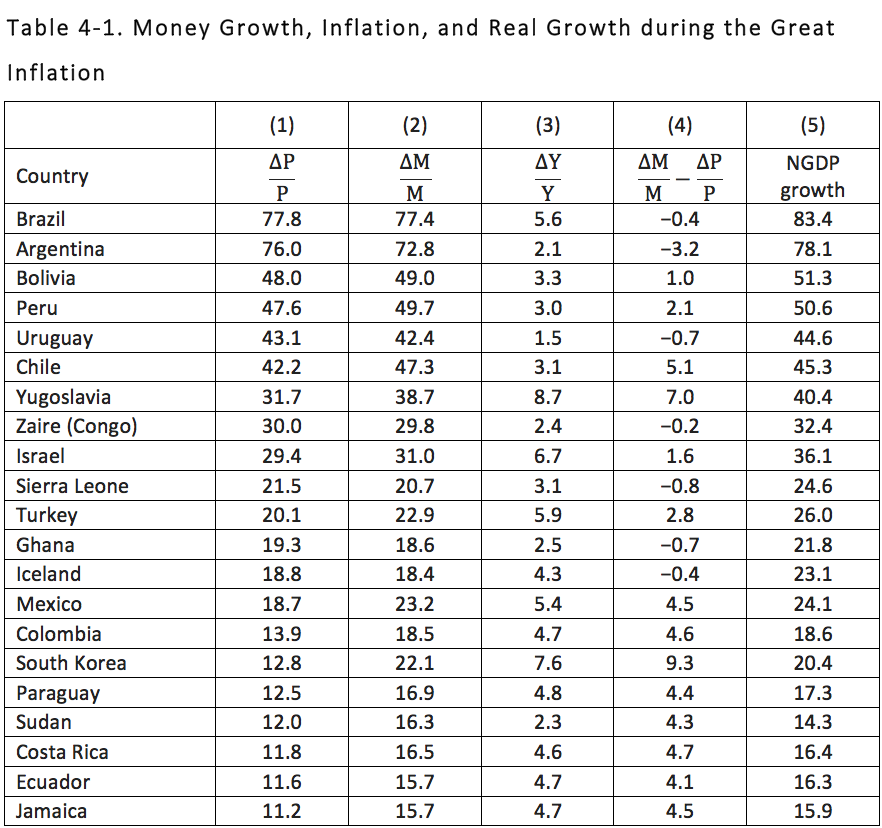

The following table shows long run money growth rates and inflation during various periods, but mostly 1950-90:

In Brazil and Argentina, prices were doubling approximately every 15 months, for decades on end.

In pre-modern times, the value of various goods tended to bounce around, rising one year and then falling the next. That’s actually still true for most goods, if you define “value” in relative terms. Thus even in countries with high inflation persisting for decades, the relative price of commodities like copper or oranges doesn’t show any dramatic (long run) upward or downward trend.

But whereas this pattern was true for essentially all goods in pre-modern times, in modern times we see two examples of goods that experienced a very rapid decline in value, which persisted over many decades. These two goods are computer chips and fiat money.

For many decades, the price of computer chips has been falling in half every 18 months, on average. This tendency is called “Moore’s Law.” In some developing countries during the 20th century, the price of their currency has been falling in half every 18 months, on average, for many decades. By 1990, one unit of Brazilian or Argentine currency could be purchased at a far lower price than in 1950, almost regardless of what you used to buy the currency. The price of their currency fell in terms of apples, oranges, coal, iron, US dollars and Japanese yen.

Over time, computer chip makers found it possible to produce a billion chips at the same cost that they had previously produced a million chips. Fiat money countries found that they could produce a trillion or even a quadrillion pesos at the same cost as they formerly produced a million or billion pesos. That cost reduction was a necessary but not sufficient cause of hyperinflation. You also needed to actually produce the money. Unlike computer firms, not all central banks are profit maximizers. (Thank God!)

It’s possible to measure NGDP using any numeraire. Thus you sometime see people claim that China has the world’s second largest GDP. In yuan terms, China’s GDP is much larger than the US GDP in dollar terms. So when people say China has the second largest GDP, they are implicitly describing what China’s GDP would look like if priced in terms of US dollars (without a PPP adjustment). Similarly, you could describe China’s GDP if priced in terms of ounces of gold or silver or one pound bags of rice. Or computer chips.

If you described the US or China’s GDP in terms of computer chips, it would be rising astronomically, it would look like a country experiencing hyperinflation. But the US and China don’t have hyperinflation. Venezuela has hyperinflation. And that’s because hyperinflation occurs when a country’s price level is rising very rapidly in terms of the thing in which prices are actually denominated.

Imagine I drew 100 graphs; each showing the US GDP measured using a different numeraire. One graph showed GDP in dollar terms. Another in terms of gold. Another in terms of apples. Another in terms of toasters. And one graph showed US GDP in terms of computer chips.

Now suppose I asked you to explain why America’s GDP in terms of computer chips rocketed much higher, year after year, for decades. Would you make reference to the Phillips Curve? To an “overheating economy”? Obviously not. Indeed I’m attacking a straw man here.

When we look at actual inflation and NGDP growth in money terms, almost nobody uses the Phillips Curve to explain inflation in a country experiencing hyperinflation. During the famous German hyperinflation of 1920-23, the world’s most famous non-monetarist economists, people like Keynes and Wicksell, suddenly switched to describing inflation in entirely monetarist terms. And then when the hyperinflation ended, Keynes quickly went back to non-monetarist explanations of inflation.

It’s always been known assumed that hyperinflation is a special case, which can only be explain by looking at what’s going on with a country’s currency. Similarly, hyperinflation of prices when measured using computer chips as a numeraire can only be explained by referring to things like Moore’s law, not Phillips curves. Hyperinflation is nothing more than a currency losing value at a very high rate. The debate is over how to explain “normal” inflation, normal NGDP growth rates.

The following equation is always and everywhere precisely true, to the very last decimal point:

M*V = C + I + G + (X-M)

Understanding what this equation means and more importantly what it doesn’t mean is the key to understanding money/macro.

The equation reminds me of two large hoofed male animals with curved horns, bashing their heads into each other, over and over again. NGDP is determined by M*V!! No it’s determined by C + I + G!!

Tyler Cowen Alex Tabarrok recently linked to an interview of Eugene Fama. His discussion of the EMH is brilliant, as you’d expect. He’s right about “bubbles”. But Alex chooses to quote from his discussion of monetary policy, which is almost completely inaccurate:

It’s not just the Fed, around the globe central banks are flooding the system with liquidity like never before. Is this a reason for concern?

Frankly, I think this is just posturing. Actually, the central banks don’t do anything real. They are issuing one form of debt to buy another form of debt. If you are an old Modigliani–Miller person the way I am, you think that’s a neutral activity: You’re issuing short-term debt to buy long-term debt or vice-versa. That’s not something that should have any real effects.

Then again, the financial markets sure seem to love it. At least it looks like that the S&P 500 is moving upwards in tandem with the expansion of the Fed’s balance sheet.

Every day we hear a story about the movement of stock prices. But the story is different each day. So basically, these stories are made up after the fact. But when we look at it systematically, we don’t see a big effect of Fed actions on real activity or on stock prices or on anything else. That’s why I use to say that the business of central banks is like pornography: In essence, it’s just entertainment and it doesn’t have any real effects.

Let’s consider the applicability of Modigliani–Miller to monetary policy. Is it true that the Fed was just swapping one liability for another similar government liability, which should not have much impact on relative prices?

Conventional economists might try to disprove Fama by pointing to the fact that the Fed can use OMOs to control interest rates. But here I’d agree with Fama; their control of rates is greatly exaggerated. Unfortunately, he’s still wrong about OMOs not having much effect.

Fama’s been making this argument for a long time, well before the zero bound situation arose. So let’s go back to 2007, when the monetary base was 98% composed of currency. At the time, one-month T-bills yielded 5% and currency yielded 0%. How can yields have been so different on two assets that are supposedly close substitutes?

[Update: In the comment section, John Cochrane says Fama is speaking to the post-2008 period, so the preceding paragraph may be in error. The sentence beginning “Actually” kind of sounded like he was making a general proposition about central banks in various times and places. The central banks of India? Turkey?]

And how many times in your life have you stood in a checkout line at a store behind someone trying to pay for purchases with T-bills? Zero? Same here.

So both common sense experience and market prices confirm that currency and T-bills are not at all close substitutes. Don’t like 2007? In 1981, T-bills yielded 15% while cash yielded 0%. In Switzerland, cash yields more that government bonds. How does M-M explain that fact?

Currency is more like “paper gold”, an asset with idiosyncratic uses that are almost unrelated to our financial system. Most currency is used for small transactions and tax evasion, areas in which T-bills are useless.

So Fama’s basic approach is wrong. Now it’s true that modern interest bearing bank reserves are much closer substitutes for T-bills than is currency. And it’s useful to think about how to model this. But you need a general model that applies to both bank reserves and currency. The M-M theorem is not a useful starting point, even in the world of 2020.

Fama’s also wrong about market responses to Fed announcements. Fed announcements often have a powerful effect on financial markets within seconds of the announcement. The odds of this being random are far less than 1 divided by the number of atoms in the universe. Perhaps Fama hasn’t studied this area.

To be sure, there are plenty of problems with empirical work on the impact of monetary policy, especially its longer run impact on the macroeconomy. Economists have done a poor job of addressing the identification problem, and this may partly explain Fama’s skepticism. But there’s no doubt that the Fed has a huge impact on asset prices; anyone that follows the markets closely knows this.

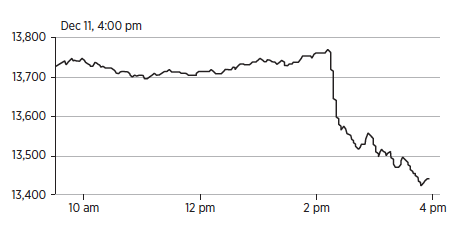

In one respect it is like pornography; I know it when I see it. Here’s the impact on the Dow of the unexpectedly contractionary Fed announcement of December 11, 2007, which occurred at 2:15pm:

That’s more disgusting than any picture of a naked lady.

There are dozens of similar examples. Modigliani–Miller has no implications for monetary economics.

Here’s why my dispute with Fama is so ironic. Who convinced me to look at monetary policy this way? Fama did! Once I understood the EMH, I realized that other macroeconomists were doing things all wrong. The way to do macro is to look at the immediate impact of policy surprises on asset prices. I quickly saw that economists were grossly underestimating the impact of policy shocks like December 11, 2007, which triggered the Great Recession.

So I’ve used Fama’s EMH model for monetary economics, and ended up as far away from Fama as it is possible to be.

Welcome to a new blog on the endlessly perplexing problem of monetary policy. You’ll quickly notice that I am not a natural blogger, yet I feel compelled by recent events to give it a shot. Read more...

My name is Scott Sumner and I have taught economics at Bentley University for the past 27 years. I earned a BA in economics at Wisconsin and a PhD at Chicago. My research has been in the field of monetary economics, particularly the role of the gold standard in the Great Depression. I had just begun research on the relationship between cultural values and neoliberal reforms, when I got pulled back into monetary economics by the current crisis.

"Couldn't find the substack and if it's moderated just as well... Voted for Trump and he won. Sorry liberal Scott Sumner who believes in money non-neutrality, which is akin to..."

"Scott, Quick note of thanks. I've hugely enjoyed your blog and the intellectual stimulation I gotten from it. Also it was pleasure getting to know you and your wife. Hope..."