What Caused the Great Moderation? And was it sudden or gradual?

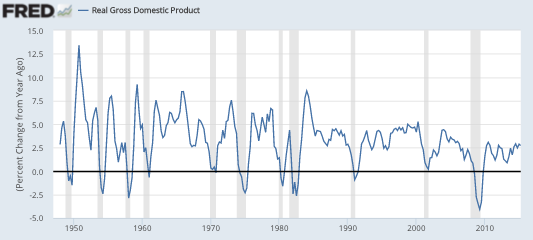

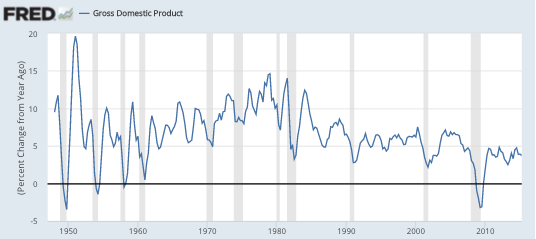

There’s a new Vox article by Lola Gadea, Ana Gomez-Loscos, and Gabriel Pérez-Quirós showing that the Great Moderation that began around 1984 is still intact, despite the Great Recession. This got me thinking about the cause or causes of the Great Moderation. In the end I’ll argue there were two causes, and that the moderation actually occurred in two steps, first in 1961 and then in 1984. Here’s a RGDP growth rate graph that clearly shows a decline in volatility after 1984:

The first idea that popped into my head was that industrial production is unusually volatile, and has been becoming a smaller share of our economy. When did this start? I don’t have data on IP as a share of the economy, but this graph shows that manufacturing has been shrinking as a share of GDP, and manufacturing is the vast bulk of IP.

The first idea that popped into my head was that industrial production is unusually volatile, and has been becoming a smaller share of our economy. When did this start? I don’t have data on IP as a share of the economy, but this graph shows that manufacturing has been shrinking as a share of GDP, and manufacturing is the vast bulk of IP.

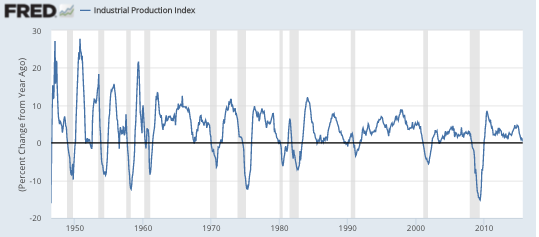

So maybe the Great Moderation simply reflects the shrinking share of this highly cyclical industry. Unfortunately, further research disproved that theory, as even IP has been getting much less volatile over time:

So maybe the Great Moderation simply reflects the shrinking share of this highly cyclical industry. Unfortunately, further research disproved that theory, as even IP has been getting much less volatile over time:

Now you can begin to see why I hypothesized two stages in the Great Moderation. The five business cycles during the Truman/Eisenhower years saw especially volatile IP. Most strikingly, the smallest peak of those 5 cycles (my birth year) is higher than the highest peak since 1960. On the IP graph it looks like the Great Moderation began in 1961, and then got even more moderate after 1984. So that made me wonder why other researchers don’t point to 1961 as the turning point.

Now you can begin to see why I hypothesized two stages in the Great Moderation. The five business cycles during the Truman/Eisenhower years saw especially volatile IP. Most strikingly, the smallest peak of those 5 cycles (my birth year) is higher than the highest peak since 1960. On the IP graph it looks like the Great Moderation began in 1961, and then got even more moderate after 1984. So that made me wonder why other researchers don’t point to 1961 as the turning point.

Go back to the real GDP graph, and you’ll see why. The moderation in real GDP during the Kennedy through early Reagan years (say 1961-84) is much less pronounced than for IP. Not really statistically significant.

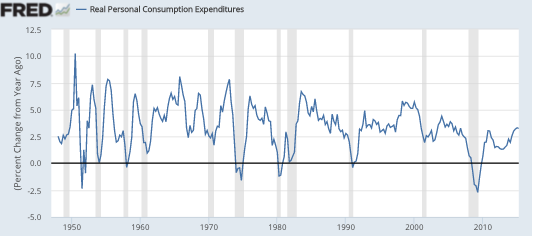

We’ve looked at IP, so what’s left? Most of what’s left is consumption—was that becoming more volatile during 1961-84, offsetting the improvement in IP stability?

Not as far as I can tell. Indeed if it weren’t for the two severe oil shocks (1974 and 1980) consumption might well have become less volatile after 1961. If those two oil shocks had occurred in the Truman/Eisenhower years, and not during 1961-84, then perhaps the Great Moderation would have been dated from 1961.

Not as far as I can tell. Indeed if it weren’t for the two severe oil shocks (1974 and 1980) consumption might well have become less volatile after 1961. If those two oil shocks had occurred in the Truman/Eisenhower years, and not during 1961-84, then perhaps the Great Moderation would have been dated from 1961.

But we still have a mystery to explain. The reduced volatility in IP after 1961 is quite clear, whereas consumption is about the same, or perhaps slightly less volatile. So why doesn’t the real GDP graph show more improvement? After all, consumption and IP are most of the economy (and yes I know I’m double counting a bit here, but my question remains.)

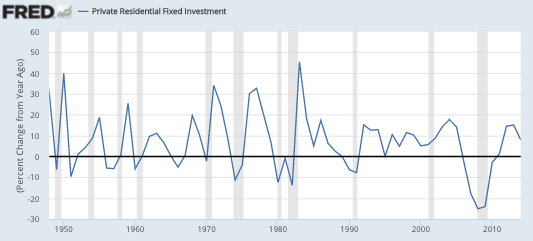

One thing that’s left is construction. I could not find a real construction series going back that far, but did find residential investment:

Now we are getting somewhere! Notice that residential investment is actually more volatile during 1966 to 1984 that during the preceding 14 years. Yes, home building is a modest share of GDP, but look at the swings in those growth rates. (I could only find nominal growth, but the swings are so large that they’d also show up in real growth.)

Now we are getting somewhere! Notice that residential investment is actually more volatile during 1966 to 1984 that during the preceding 14 years. Yes, home building is a modest share of GDP, but look at the swings in those growth rates. (I could only find nominal growth, but the swings are so large that they’d also show up in real growth.)

So now we seem to have a partial answer. There was some tendency for the economy to moderate after 1961, but mostly if you exclude homebuilding. If you include homebuilding, then 1984 looks like the year that the Great Moderation began. The question is why?

Here’s the graph you have all been waiting for, monetary policy (er, I mean NGDP growth.)

NGDP growth volatility clearly fell after 1961, and then moderated further after 1984 (except for 2008-09, obviously.)

NGDP growth volatility clearly fell after 1961, and then moderated further after 1984 (except for 2008-09, obviously.)

So why didn’t RGDP growth moderate as much as NGDP growth, during the 1961-84 period? The easy answer is the two oil shocks. (And I’d add the imposition and removal of price controls in 1971-75.) Yes, that may be part of the story; the oil shocks hit consumption hard. But let’s think about residential investment, which became more volatile during the middle period. Why did that occur when NGDP growth was becoming more stable?

The answer seems clear, NGDP growth from one year to the next was becoming more stable, but the longer-term NGDP growth rate was becoming unanchored, as inflation soared from 1% to 13%. With trend NGDP growth changing significantly, and unexpectedly, long-term nominal interest rates (on T-bonds and fixed rate mortgages) became highly unstable. Yields on 30-year T-bills soared to roughly 15% in 1981.

Because of our peculiar residential mortgage system, these big swings in interest rates whipsawed residential investment, making it highly volatile during the Great Inflation. That’s why the Great Inflation had to end before the Great Moderation could begin. It also implies that if the Great Inflation had been steady inflation/NGDP growth, which was predictable, then the Great Moderation would have begun in 1961, not 1984. (And if my grandmother had wings . . . )

In this story there are two key milestones:

1. In 1961 the Fed figured out how to avoid the stop-go policies of the previous 15 years. But their technique left longer-term inflation/NGDP growth completely unanchored. After 1984 the Fed figured out how to walk and chew gum at the same time, how to keep inflation both low and stable. Ditto for NGDP growth (except 2008-09)

If you look closely at the residential investment graph, you’ll see that homebuilding was more volatile in the 1990-91 recession than in the 2001 recession. That may be because in the first of the two we were still working off the last bit of the Great Inflation. Inflation went into that recession at a 4.5% rate, and came out closer to 2%. In the 2001 recession we entered and left the recession with about the same (2%) inflation rate. Of course there were other factors too, the 2001 recession was focused on business investment, and the resulting fall in interest rates helped homebuilding. In 1990, homebuilding had been overextended by reckless S&L lending. But even with all the craziness in homebuilding in the past few decades, the 1970s were even more unstable.

Obviously the Great Recession is sui generis (first time I’ve used that term), but in the recovery period we are back to eerily steady RGDP growth. The 5 recessions in 15 years that we saw after WWII now seems like ancient history. I can’t even imagine the US having 5 recessions in the next 15 years—although the one thing I’ve learned in macro is that just when you expect something will never return (like zero interest rates) it comes back. So all forecasts are provisional.

PS. IP involves domestic capital goods, domestic consumer goods and exports. The domestic consumer goods portion is double-counted in my analysis. It might have been better to use services rather than consumption—but I doubt my conclusions would have changed.

Tags:

26. October 2015 at 09:56

Excellent post.

I will just add that if we asked someone to point out where reckless monetary policy led to a demand-side housing bubble, nobody looking at those last two graphs would pick the 2000s. Nobody. The entire public discussion of finance over the past 15 years has been a massive exercise in reasoning from a price change. It’s not even like there is a point to it but some people take it too far. There is simply nothing there besides reasoning from a price change.

NGDP growth at the peak in the 2000s barely even reached the average growth rate of post WW II, yet the description that is considered above a burden of proof is the one that sees this period as some sort of crazed bubble where debt and money were flowing out of control.

26. October 2015 at 10:14

Scott, I think there are several things wrong in this post!

You should reread your early Feb 09 post: GDP=Y+C+I+NX=Gross Deceptive Partitioning!

Just one comment: NGDP growth was NOT more stable after 1961 and before 1984. As you mention further down, its variance was infinite (it was not stationary).

26. October 2015 at 10:30

[…] 5. Is the Great Moderation still going on? And commentary from Scott Sumner. […]

26. October 2015 at 10:32

My immediate reaction after the first paragraph was that the pre-1980 era is the aberration, and bad monetary policy would have been the cause.

Specifically the Phillips curve mentality that lower un-employment could be “bought” at the costs of slightly higher inflation. What we received was a short-term reduction in unemployment at the cost of instability.

26. October 2015 at 10:34

Scott, the author´s conclusion:

“The Great Moderation is not over in spite of the Great Recession even if we use a historical dataset beginning in the 19th century. The Great Moderation was originally associated with a decrease in output volatility and was considered a great achievement in terms of reducing risk and of decreasing the frequency and depth of recessions. However, after carefully analysing the characteristics of the Great Moderation, they seem to be more clearly associated with the shape of expansions. Perhaps the benefits associated with an apparent increase in stability are paid for at a very high price. Feeble expansions may be the price to pay for low volatility.”

is, in my view, a “Great Cop-out”! I remember that even in late 92 people were complaining about a “feeble recovery”, and even talking about “triple dips”. That was the first recession after the start of the “GM”, so people thought that the usual strong bounce back would be the normal pattern, forgetting the also “feeble recession”.

If the economy is more stable, both the “downs” and “ups” are more constrained.

Just because NGDP (and RGDP) growth and inflation are stable at present, should not be confused with what a GM is about. That also requires the LEVEL of NGDP to be adequate.

26. October 2015 at 10:38

That last point I discuss here:

https://thefaintofheart.wordpress.com/2014/05/22/a-great-moderation-is-possible-at-many-activity-levels-the-question-is-to-find-the-right-one/

26. October 2015 at 10:40

On the Origins of the Great Inflation

https://thefaintofheart.wordpress.com/2012/08/25/the-origins-of-the-great-inflation/

26. October 2015 at 11:11

Off topic but Ygledias has a new article

http://www.vox.com/2015/10/20/9570175/labor-share-housing

I’m becoming more and more convinced that zoning laws are an economic atrocity. My wish fulfillment fantasy is conservative or libertarian lawyers teaming up with liberals and taking all the zoning laws in the United States all the way to SCOTUS and arguing that they violate the 14th amendment and discriminate against the poor.

How much of a boost to RGDP would eliminating all zoning laws be, in your opinion Scott?

26. October 2015 at 12:26

Kevin, Great comment.

Marcus, Great comment, and I was thinking about that after I wrote the post. Note that in the end I pointed to two types of NGDP instability being the problem:

1. Year to year instability, which got smaller during the Great Inflation.

2. Instability over longer term, say 5 or 10 years, which got greater during the Great Inflation. (As you noted)

In my view these two changes tended to offset during the Great Inflation, and the real breakthrough came after 1984, when both types of instability got smaller.

On your second comment, I am addressing the Great Moderation, as it is commonly described. That looks at growth rates, not levels. I agree that if you look at levels then the past 10 years seems far less impressive.

Yes, it would boost growth a lot. That and immigration are the two areas where the government could quickly and dramatically boost aggregate supply.

26. October 2015 at 12:47

If you go to BEA table 1.2.6 you will find real GDP broken down by major sector. It is goods, services and structures,

not manufacturing.

But the data shows that since the early 1950’s goods share of GDP has increased from some 22% to 33%.

Services has remained roughly in the low to mid 60s%, with not clear trend of it’s share growing or contracting.

However, structures has fallen significantly from about 20% to around 7%.

I know that is not what you would expect, but the world is full of misperceptions.

26. October 2015 at 12:48

Nice article.

This seems like a better result for the word, but do you think maybe we lose something here that boom and bust gave us? Now we get Twitter instead of Apollo.

Partly facetious but it does seem like stability has made negative NPV projects really obvious, and there are some really great negative NPV projects out there! High speed rail, Grand Central Terminal, Apollo, etc.

26. October 2015 at 13:05

I always assumed the Great Moderation started 1983 when Paul Volcker finally slayed the Great Inflation Dragon of the 1970s and oil prices dropped tremendously. So what changed:

1) The United State AS is getting steeper. This is because (higher or lower) commodity prices don’t have the effect on the economy as it once did. (Notice housing prices are set by location, location, location versus building materials.)

2) The workforce growth is shrinking and getting flatter.

3) As Paul Krugman has noted as global economy expanded, the US economy is ‘flatter’.

26. October 2015 at 13:25

As finance increased as a share of the economy–nearly doubled today from the 1950s–economic instability decreased. There goes Bernie Sanders’ favorite soundbite.

26. October 2015 at 13:42

Scott,

The blue line represents industrial production as a percentage of national income (without capital adjustment). The top red line is industrial production as a percentage of employment (nonfarm payroll). The bottom red line excludes utilities and consequently begins at an earlier date.

https://research.stlouisfed.org/fred2/graph/?graph_id=136614&updated=8776

As a png link.

https://research.stlouisfed.org/fred2/graph/fredgraph.png?g=2jtc

26. October 2015 at 14:57

Given the 1950s NGDP volatility, why’s it still remembered as a good time for the economy?

26. October 2015 at 15:05

Also, is there an of analysis of the international Great Moderation out there?

26. October 2015 at 16:02

Well, you also get less volatility when you suffocate something.

The central banks of the Western world began inflation-fighting in the early 1980s after inflation reached into double digits. We gave up a lot of growth to accomplish single-digit inflation. Perhaps it was worth it.

This culture of inflation-fighting has become deeply embedded in central banks, where today some central banks, the ECB for example, have mission statements to hold prices steady, without regard for economic growth.

Central banks, like many public agencies, can stagnate around sanctified mission statements.

It is incredible today to recall that in 1992 Milton Friedman chidef the US Federal Reserve for being too tight, when inflation was at 3%.

Janet Yellen has rhapsodized about a 1% IT, which once enacted would likely become a ceiling.

If you read BIS literature you will believe inflation-obsessed cultists run central banking.

26. October 2015 at 16:18

“We gave up a lot of growth to accomplish single-digit inflation.”

-Nope. No evidence of that.

26. October 2015 at 20:17

Meanwhile, Downunder, the Great Moderation continues …

27. October 2015 at 11:49

Spencer, You said:

“I know that is not what you would expect, but the world is full of misperceptions.”

I assure you that that table is not accurate—the misperceptions were with the statisticians who put it together.

Mark, Thanks for that info. What do you think is wrong with the BEA table 1.2.6 that Spencer points to? Obviously it’s wrong, but why?

E. Harding, It was preceded by war and depression, and living standards rose a lot from the 1930s to the 1950s. It’s all relative—if you are doing much better, you feel good.

30. October 2015 at 10:31

The “Great Moderation” was caused by two things.

– Increasing productivity

– “Moderate Wage Increase” from 1980/1981 onwards. With Moderate Wage Growth I mean the following:

In the 1960s & 1970s employees got wage increases at or above inlfation. From the early 1980s onwards employees got wage increases below inlfation.