Japan hasn’t yet run out of ink and paper

Here’s Noah Smith at Bloomberg:

Japan’s great monetary policy experiment is drawing to a close, and the results may change the way the world thinks about central banking. The Bank of Japan’s recent quarterly report says, in effect, that the central bank has done all it can do to raise growth and inflation, and that fiscal policy needs to step in and help. The BOJ admitted that monetary policy alone won’t be enough to hit its 2 percent inflation target, now or ever.

This is very troubling for monetarists (as those who think that monetary policy is the key to macroeconomic stabilization are sometimes called). If central banks can’t control the rate of inflation, what hope do they have of affecting the economy?

I was surprised to read that the BOJ’s quarterly report had said that the BOJ had done all it could, particularly since the head of the BOJ frequently says exactly the opposite. So I followed the link to the “quarterly report” and found . . . another Bloomberg article:

Many economists interpreted a BOJ policy shift in September as preparation for a sustained fight to generate inflation. Shirai said the central bank would maintain the status quo on policy unless the yen surges or economic data deteriorate.

And what will it do to policy if the yen “surges”? Let me guess, it will ease policy. So why not ease policy today?

In fact, the BOJ denies that it is out of ammo.

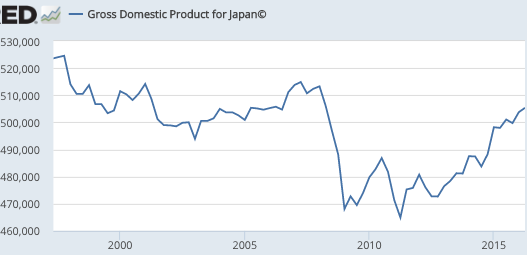

Market monetarists have been more accurate in their Japan forecasts than any other group. I believe that I was the first western blogger to comment on Abenomics, and I consistently predicted that the policy would raise inflation, but not all the way up to 2%. That’s been my view all along, and that’s exactly what’s happened. The actual inflation rate has averaged closer to 1.0%, but even that is a dramatic improvement over the deflation that preceded Abenomics (and this occurred during a period of rapidly falling oil prices, when even US inflation underperformed). I also pointed out early in 2016 that the BOJ was moving to a more contractionary policy, and we now see the effects of that policy switch on Japanese inflation, which has fallen. Even so, the impact of Abenomics on NGDP is clearly positive. It began rising almost immediately after Abenomics was announced in late 2012:

The rest of the article makes the usual mistakes, confusing low interest rates and QE with easy money, whereas they are usually reflective of the fact that the central bank policy is too contractionary. The market monetarist solution now is the same as it always was—NGDPLT—combined with a “whatever it takes approach” to monetary stimulus. If you want a smaller central bank balance sheet, then aim for a higher NGDP growth target. This is not rocket science; we know how to do it, we just need to get real world central banks to try.

The rest of the article makes the usual mistakes, confusing low interest rates and QE with easy money, whereas they are usually reflective of the fact that the central bank policy is too contractionary. The market monetarist solution now is the same as it always was—NGDPLT—combined with a “whatever it takes approach” to monetary stimulus. If you want a smaller central bank balance sheet, then aim for a higher NGDP growth target. This is not rocket science; we know how to do it, we just need to get real world central banks to try.

But don’t let the perfect be the enemy of the good. Abenomics really was much better than what came before, and we can do still better. Instead of abandoning monetary policy, why not improve it?

There’s another thing I don’t understand about all these “monetarism has failed” articles—where are all the “Keynesianism has failed” articles? Didn’t Japan do massive fiscal stimulus, causing it’s debt to balloon to 250% of GDP? Why isn’t fiscal stimulus viewed as a failure? I suppose a Keynesian would say, “well they should have done even more”? OK, but why doesn’t that also apply to monetary stimulus? After all, fiscal stimulus is far more costly. In contrast, there’s no limit to how much money can be printed. And why do we get this:

If Japan is out of the monetary easing game, other countries will doubtless follow. The era of bold monetary policy experimentation that began with the global financial crisis is now drawing to a close. More and more, economic policy makers will look to fiscal initiatives and to deeper structural reforms to boost growth and stop deflation.

Why not say the failure of fiscal stimulus in Japan means that governments are “out of the fiscal game”? In fact, governments can never be out of the monetary policy game, unless they revert to barter. As Nick Rowe likes to point out, there is no such thing as not doing monetary policy. The only question is where are you going with that policy. If you have a policy that delivers low NGDP growth rates and near zero interest rates, then you will end up with a big central bank balance sheet. There’s no way to avoid that except by aiming for a higher NGDP target. Fiscal policy doesn’t create any short cut to success, as the Japanese case already showed. In January 2015, the Swiss tried to “get out of the monetary policy game” so they could shrink their balance sheet, and the balance sheet is now bigger than ever. If you are going in the wrong direction, then switch policy.

If any central bank was going to fulfill the dreams of monetarists, it was Kuroda’s BOJ.

Actually, Australia’s much closer to what monetarists have in mind, unless you consider letting the yen appreciate from 125 to 100/dollar to be a monetarist “dream”.

Here’s another article on the BOJ, from last month:

“We are buying government bonds to achieve the 2% price target,” Kuroda said.

Kuroda said that he doesn’t expect the BOJ to run out of JGBs to purchase.

He said that the BOJ’s easy policy would not lead to hyper-inflation.

PS. Stephen Kirchner sent me to this. Great idea, do massive fiscal stimulus when unemployment is 4.9% and the Fed is raising rates to prevent an overshoot of 2% inflation. Why didn’t I think of that? I often say that talking about politics takes 30 points off a person’s IQ (including me). I have a new one. The zero bound takes 30 years of progress away from macroeconomics. It took macro 30 years to recover from the Great Depression, and it’ll probably take 30 years to recover from the Great Recession. I won’t live that long.

🙁

Tags:

11. November 2016 at 10:36

Looking forward… We could well see a Giant stimulus package coming out of the unified republican governmt….all aimed at elite interests…in the form of crony capitalism… financed by soaring nation debt…

And then in a few years the elite will demand we pay down the debt by slashing SS and any other part of the social safety net… And warn us that asking them to pay for it will DOOM us all.

It’s gonna be so Orwellian… Again… as The People, Politicians, and certain paid for academics (not Scott )… who proclaimed DOOM at Obama’s attempts at stimulus… no longer care about debt…

11. November 2016 at 10:47

Bill,

If Trump goes the deficit spending route I imagine Paul Krugman opining that this time the debt matters.

11. November 2016 at 11:04

Thanks for this Scott. I read that Noah Smith piece and was like WTF? When did the BoJ say they were giving up? Bloomberg opinion is hack central. They are extremely hubristic, puffed up by millions in revenues generated by the financial data service. Can’t WAIT til a good competitor comes along and I can stop giving Mike Bloomberg two grand a month to give to doofuzians like Noah Smith.

11. November 2016 at 11:12

Dan W.

we will see. But I’m expecting that he’ll be more like me and complain about its form.

And Keynesians don’t call for increased deficit spending at all times…it’s supposed to be countercyclical…

So if the economy strengthens (to what point ?) he can be philosophically consistent and call for spending restraints… Seeing as how up till now he was still calling for stimulus…. if he turns on a dime it will be telling…

11. November 2016 at 11:22

My sympathy, professor. Your science shows all the marks of theology, after the fervor has left it, and there are sinecures to award. Does not preclude technically challenging work, but orthodoxy is determined in other ways

On the positive side, monetarism is now worth slandering (from the point of view of orthodoxy — if which Noah is but a small, largely just aspiring supplicant). That’s actually a sign of what you’ve achieved. Chapeau

(First they ignore you, then they laugh at you, then they fight you, then you win.

–> stage2!)

11. November 2016 at 13:15

Great post.

‘Why not say the failure of fiscal stimulus in Japan means that governments are “out of the fiscal game”?’

Dare I say it’s because most Americans don’t pay any attention to what is happening elsewhere?

The Smith post is illustrative of the reason I stopped reading him. Is this how economists are trained these days – savants who play with data but have no intuitive grasp of counterfactuals? Maybe that’s why 80% of economists don’t seem to understand the meaning of opportunity cost? Then again, within the mainstream media, Smith probably best represents the type of economist you need to persuade to get the Fed to accept MM.

11. November 2016 at 13:54

Bill, Yes, interesting how in 24 hours the GOP does a complete about face over stimulus spending. I wonder what happened to change their minds?

11. November 2016 at 14:50

“It took macro 30 years to recover from the Great Depression, and it’ll probably take 30 years to recover from the Great Recession.”

Scott, as I’m an IT guy, I’m curious about something. With so many economists blogging, isn’t the interchange and debate of ideas taking place faster than when such interchange was done through conferences, papers, and books?

11. November 2016 at 15:53

“combined with a “whatever it takes approach” to monetary stimulus”

Well, the BOJ has done monetary stimulus up to stock market purchases. This year, there is still deflation and negative NGDP growth.

Having QE go up to buying possibly trillions of dollars of assets other than government bonds brings up many real-world questions. When the Central Bank owns stock, how does it vote on proxy forms? What happens when the stocks go down in price and the central bank is technically “insolvent?” For less liquid assets, would a central bank’s trading desk pay literally anything for the asset? If not, how does the trading desk negotiate purchases to be sure of a fair price?

I don’t see a generally higher inflation rate being sure to avoid the zero-lower bound either. Lehman would have likely gone bankrupt as LTCM’s counter-party in the 90’s without LTCM being bailed out by other banks. The only workable solution I see is a Kimball-like proposal which really changes how people view paper currency.

Outside of Kimball-like proposals, functionally central banks can be limited based on what’s within political possibility. If Japan buying broad stock market ETF’s is not enough to set expectations, what asset purchases would set expectations?

11. November 2016 at 15:59

Alright, I would need to correct a big part of my piece. I quickly brought up NGDP for Japan and it looked like it was declining. Only GDP in dollars is declining. NGDP in Yen is growing. Japanese inflation is also at -0.5%, which looked like negative NGDP growth as well.

I still would disagree with unorthodox monetary purchases. Stock market purchases may be more politically palatable, but Kimball-like policies are more workable and distort markets less in my opinion. This is especially the case if there isn’t a government backstop to large bank deposits such as commercial paper and Repo agreements in 2008.

11. November 2016 at 16:28

Sumner: “I was surprised to read that the BOJ’s quarterly report had said that the BOJ had done all it could,…” – Sumner reads Japanese?

Sumner: ” I believe that I was the first western blogger to comment on Abenomics, …” – what an ego! I find it hard to believe Sumner was first at anything, except self-promotion.

Sumner: “I won’t live that long.” – another sympathy ploy. Sumner might outlive all of us.

11. November 2016 at 18:25

Excellent blogging.

Haruhiko Kuroda, Bank of Japan Governor, has shown resolve in his battle to bring Japan to prosperity, more than any other central banker.

Yet he has seen the yen appreciate by 20-25% in the last year. He needs to do more, if he can get fellow board members to agree.

Kuroda should imitate the greatest central banker of all time, Takahashi Korekiyo, the Japanese finance minister who quickly beat back the Great Depression in Japan, even as other developed nations floundered and withered. Korekiyo used money-financed fiscal programs to great effect, sparing millions of Japanese the ravages of depression. That story is well-buried, never in econ textbooks, btw.

The People’s Bank of China this week moved the yuan down to the lowest level in six years, and I do not blame them. The PBoC should do even more, as China is below their inflation target And yes, they would be better off with a NGDPLT and more privatization.

There remains in ossified orthodox macroeconomics the view that stimulative actions by central banks are sinister, but activist actions to asphyxiate economies are okay. Some still view central banks as statist-inflationary organizations, even as Western central bankers rhapsodize about deflation.

Side note to Scott Sumner:

I checked the numbers on whether, in real dollars, U.S. national security spending is double today what it was under Ronald Reagan, as David Stockman contended in the recent past.

Perhaps that was the case when Stockman said so a few years ago, and Stockman may have included war-spending in Afghanistan and Iraq, which has subsided, and which is NOT included in these figures:

In constant dollars:

DoD and VA spending 1988: $505.9 billion

DoD, VA and Homeland Security spending 2016: $719.8 billion.

Missing: black budget outlays; prorated interest on the national debt; outlays in Afghanistan and Iraq, and perhaps other Mideast nations.

Okay, so the US today, in real dollars, spends 42% more on national security than it did in 1988, the height of the Reagan military build-up.

I stand corrected.

However, I would advise Sumner and taxpayers to refute the notion that defense spending should be “X% of GDP.” Like any federal outlay, defense spending should the least possible.

If the US economy should double in the next 20 years, but threats evaporate, we should spend zero on war-making ability. But, say, if China should become bellicose, imperialist and heavily armed, and our economy flounders, we should probably spend 10% or more of GDP on war-making ability.

Our economy is much larger today than when Reagan governed in the Oval Office. The threats today are much, much smaller.

We should expect shrinking, rather than rising national security outlays. Good luck with that.

My guess is that Trump, like Reagan (and Bush jr.) will use federal agency national-security outlays to bolster GOP-affiliated groups and voters. It is something of a version of the old machine-politics seen a few generations ago in Kansas City or Boston.

11. November 2016 at 20:13

Feel like I’ve been reading the same obvious mistakes for so many years now.

Japan is probably on a new NGDP trendline, but it will take some time to convince everyone of that.

11. November 2016 at 20:16

Commenter Jeff at Noah Smith’s post sez;

https://www.bloomberg.com/view/articles/2016-11-10/japan-shuts-down-its-monetary-lab#comment-2997235421

————-quote———–

This is utter nonsense. Look at the Dollar/Yen exchange rate. The Bank of Japan depreciated the yen when Abe first took office, but then stopped doing so at the end of 2013. The rate was flat from then until they resumed depreciating in the second half of 2014. The yen depreciated to about 120 per dollar in early 2015, and stayed near there until the end of that year, but then the central bank actually let it appreciate all the way back up to just over 100 per dollar now. That’s at least a 15 percent appreciation against a dollar that was also appreciating. This is tight, not easy money.

It is trivially easy for a central bank to target an exchange rate. If the Bank of Japan were to announce that they were going to depreciate back up to 120 per dollar immediately, and then continue to depreciate at an annual rate of 4 or 5 percent, you can bet your pension that Japanese nominal and real GDP growth would take off, as would the inflation rate.

This BS that monetary policy can’t create inflation is just crazy. Japan has zero inflation or deflation because that’s what the Japanese central bank wants. If they say otherwise, they are either lying or laughably incompetent. I know the Japanese don’t like immigration, but perhaps they should import a few central bankers from Venezuela.

—————-endquote—————

12. November 2016 at 04:01

@Ben Cole – of course real spending on war is greater in the USA now than in 1988–real GDP has grown about double since then. That’s always true in a growing economy. Perhaps you should adjust by military expenses / GDP (ratio). Anybody paying for your posts at your new site? I’d not quit my day job as a Thai turkey farmer if I wuz u.

@Patrick R. Sullivan – quoting: “it is trivially easy for a central bank to target an exchange rate” – no it’s not. First, recall Soros and Black Monday, BOE. Next, from what I’ve read the BOJ is very ‘weak’ when it comes to $/Yen targeting. Sure they do it, but they ‘lean into the wind’ rather than arbitrarily change the exchange rate to whatever they want. Since money is neutral it’s hard to see any real effects from currency devaluations. Even in the famous Plaza Accord the dollar was already falling (this accord is usually cited as a success in central bank targeting of exchange rates, but, like the Volcker myth of ‘breaking the back of inflation’ –wrong, inflation was already coming down when Volcker was in charge–it’s just a myth).

Repeat after me: money is neutral, and even nominal changes in a money supply are hard for central banks to achieve. It’s not as easy as Sumner claims of ‘print more money’. The US Fed tripled its balance sheet from $1T to 4T after 2008 to no effect, proof of that. And short of hyperinflation (where even I concede money is not neutral at that point), printing money won’t do anything, neither real, nor, due to the zero bound, nominally. Nuff said. Like talking to a brick wall with you diehards.

12. November 2016 at 04:32

Ray Woepez:

When you speak of “neutral,” are you speaking of neutral as in the NFL “neutral zone” between offensive and defensive lines, or the “Romulan Neutral Zone” of the original Star Trek series?

12. November 2016 at 06:19

Paul Krugman has at times said that any Keynesian spending would be good, even if it’s just digging holes and refilling them. Regardless, he’ll find ways to (a) say why “this” spending (whatever it happens to be) is the wrong type, (b) say why tax cuts don’t count, and (c) re-defend his statement on election night that the stock market will never recover from this election.

12. November 2016 at 06:20

Benjamin Cole,

42 percent growth over 28 years amounts to 1.27 percent annual growth. Considering that at least half of defense spending goes to pay personnel this is just another example of Baumol’s Cost Disease.

12. November 2016 at 06:22

@Patrick Sullivan,

Yup, that was me. Glad you like it. I thought I had beaten Scott to it, but little did I know he was preparing this post.

12. November 2016 at 08:51

Jeff: You are correct.

VA bills are exploding.

I think a better goal is a 1.27% decrease in National Security-foreign policy outlays per year.

Even a return to a draft citizen-soldier military is beginning to make sense.

Could the leadership class draft soldiers to conduct perma-wars?

12. November 2016 at 09:18

I know I shouldn’t feed the troll, but here goes:

Ray, that was me Patrick was quoting saying it was trivially easy to target an exchange rate. Perhaps I should have said it is trivially easy to depreciate your own currency. The British failed because they were trying to do something close to the opposite, i.e., they were trying to keep the currency from depreciating but weren’t willing to tolerate the high domestic interest rates that were resulting from their efforts.

But depreciating your currency is easy. The Bank of Japan can create billions of yen with a simple mouse click. It costs them nothing to do so. If they want to sell yen for less than the current market price, there is no one in the world that can stop them. If the market price for yen is 1/100th of a dollar, and they want to sell yen for 1/120th of a dollar, they can do so. If they stand ready to sell an unlimited quantity of yen for that price, they can drive the market price down to the price they are willing to sell for.

This is not rocket science. It’s trivially easy, as I said. Noah Smith has to know that, so I don’t get where he’s coming from.

12. November 2016 at 10:46

John Taylor: “Take off the muzzle and the economy will roar”

https://economicsone.com/2016/10/16/take-off-the-muzzle-and-the-economy-will-roar

12. November 2016 at 20:02

Re Japan:

Considering that banks lend on real estate primarily, and the creation of money may be endogenous, maybe the Bank of Japan needs to declare it is implementing money-financined fiscal programs, or “helicopter drops.”

Lowering rates and QE helps, some singles here or there, but why not bring out the serious lumber?

Question: Why are the lessons of the Weimar Republic taught endlessly (and usually incorrectly; it was depression and deflation that help usher in Hitler), but never the lesson of Takahashi Korekiyo, the Japanese Finance Minister, and the greatest central banker of all time, who turned back the Great Depression in Japan through helicopter drops?

Millions of Japanese enjoyed prosperity rather than depression thanks to Takahashi. Oh, that.

Sadly, Takahashi was assassinated by militarists and had the misfortune of being right in one of the worst chapters in history.

But he was right.

12. November 2016 at 20:10

“Paul Krugman has at times said that any Keynesian spending would be good, even if it’s just digging holes and refilling them. Regardless, he’ll find ways to (a) say why “this” spending (whatever it happens to be) is the wrong type, (b) say why tax cuts don’t count, and (c) re-defend his statement on election night that the stock market will never recover from this election.”

You’re wrong. Krugman specifically retracted his call on election night that Trump would be bad for the economy:

“But it’s important not to expect this to happen right away. There’s a temptation to predict immediate economic or foreign-policy collapse; I gave in to that temptation Tuesday night, but quickly realized that I was making the same mistake as the opponents of Brexit (which I got right). So I am retracting that call, right now. It’s at least possible that bigger budget deficits will, if anything, strengthen the economy briefly. More detail in Monday’s column, I suspect.”

http://krugman.blogs.nytimes.com/2016/11/11/the-long-haul/?module=BlogPost-Title&version=Blog%20Main&contentCollection=Opinion&action=Click&pgtype=Blogs®ion=Body

Even though the US is technically outside the zero-bound, I believe the Fed raised interest rates far before any honest inflationary pressure. Even though unemployment is at 4.9%, the employment/prime-age ratio suggests slack still in the economy.

http://data.bls.gov/timeseries/LNS12300060

To put it another way, the Fed raised rates from 0% to 0.25% much sooner than they would raise rates from 2% to 2.25%. A large program of deficit spending could increase employment even though the Fed theoretically could offset the spending. If rates are higher, then the Fed is less likely to offset the spending.

It’s also reasonable to say tax cuts “don’t count” for Keynesian spending, especially tax cuts for the rich. That’s nothing against the rich in particular. The rich are just *very* likely to save their tax cut rather than spend it.

To be clear, in an ideal world I would be against *either* deficit spending on infrastructure or deficit-financed tax cuts. Ideally, the Fed would have a clear solution for breaking through the zero-bound and would adhere to a clear inflation level target.

12. November 2016 at 23:15

Looks like the yield peg/cap promise was a pretty good move (no one can really tell if it was meant as a peg or a cap). It does seem that they were close to surrender, but all that upward pressure in global yields from Trump’s policy threats could turn what was meant as a cosmetic innovation to a genuine game changer for Japan. After all, they are not really giving up on 2% target. JGB outperformance vs. other bonds, and spiking USDJPY speak for themselves. Of course, Trump can change the game by channeling auto executives’ ill-informed complaints about Japanese manufacturers taking advantage of renewed weakness in the yen…

13. November 2016 at 01:52

Greetings Sir,

I am a student in India with a request to blog about ongoing demonetisation of higher denomination of Rs 500/1000 notes in order to search for unaccounted incomes to increase tax revenue by increasing people under tax net.

The problem is that this sudden shock has negatively affected 85% of Indian rural based economy that runs on cash.There is rampant rumour mongering where poor uneducated are selling their savings in 500/1000 notes in discount to middlemen with bank accounts.Tyler Cowen has done a piece saying that it is good for India as lower productivity sectors will come under the tax bracket.

What is your opinion or experience when other countries have done a similar exercise.Thanks in advance

13. November 2016 at 02:44

@Jeff – “Ray, that was me Patrick was quoting saying it was trivially easy to target an exchange rate. Perhaps I should have said it is trivially easy to depreciate your own currency” – yes, thanks for that clarification. But it doesn’t change my analysis much. The Baxter & Stockman 1989 paper “found that the transition to a freely floating exchange rate regime only led to a substantial upward shift in both nominal and real exchange rate variability but virtually no change in the distributions of conventional macroeconomic fundamentals.” – translation: despite big jumps in exchange rates, both nominal and real, they did not affect the real economy. This is consistent with the fact money is neutral. So even your ‘mouse clicks’ will fail to do anything. Nor, for that matter, will the converse, raising interest rates, do much to the real economy (people and businesses adjust). Money is largely neutral Jeff. Changing the money supply does nothing to the real economy. Did not even Ben Cole learn this painful lesson the hard way when he debated me here, and lost? Ben found, much to his chagrin, that Spanish per capita wages actually were falling after a bump upwards after the Black Death (mid-1300s). Even falling after the New World silver and gold finds, until the early 1800s? As was most of Europe. In other words, the Spanish New World silver, though wasted on expensive wars and did not favor the Spanish people, did not have much of an effect on Europe. There was no ‘beneficial inflation’ (wages were falling for 400 years throughout Europe). Cole will learn eventually that Japan in the mid-1930s did relatively well due to their imperialist expansion in Manchuria, not because of mere paper printing. But he’s a slow learner.

13. November 2016 at 03:31

I lost a debate to Ray Woepez? Was that verbal tussle held in the Romulan neutral zone?

13. November 2016 at 06:11

I’m visiting Japan right now. Ordinary middle class people tell me for the first time in a gazillion years (subjectively speaking) that their incomes have gone up significantly this year, thanks to (twice-yearly) bonuses.

High-end shopping and entertainment feel very active.

I think the BOJ may be correct in suspecting that the official survey-based GDP data underestimate the actual level of economic activity.

13. November 2016 at 06:36

Gordon, I wish it were happening. People on the left basically ignore my blog. Krugman says he doesn’t even read any conservative blogs. If there is no interaction, how can there be a debate?

Matthew, I’m not asking the BOJ to do more QE, I’m asking them to set a different target.

You said:

“I don’t see a generally higher inflation rate being sure to avoid the zero-lower bound either. Lehman would have likely gone bankrupt as LTCM’s counter-party in the 90’s without LTCM being bailed out by other banks.”

Don’t follow this at all. What does LTCM have to do with the zero bound?

Ray, You said:

“Sumner: “I was surprised to read that the BOJ’s quarterly report had said that the BOJ had done all it could,…” – Sumner reads Japanese?”

And so we find out that Ray doesn’t know the meaning of “that”

Patrick and Jeff, That was a good comment.

HL, I might turn out well, but if so there’s an element of luck involved.

Garvit, It sounds like a very bad idea to me, but I’d need to find out more about the policy to comment.

Thanks Mikio, although an economy can do well with low NGDP growth, once the public adjusts to it.

13. November 2016 at 10:14

“Our economy is much larger today than when Reagan governed in the Oval Office. The threats today are much, much smaller.”

The military budget is based on concept of being able to come to the defense of our allies anywhere in the world on two fronts. In reality, the level of spending is not sufficient for that aim. If people are willing to change this to America first, allies are on your own, then yes the size of the force can be shrunk considerably and the costs reduced.

Technology is a huge force multiplier. Air superiority is paramount to any scenario, hence the large price tag for the F-35. Without air superiority, our entire surface ship navy will lay in waste during the first week of the battle. Our entire surface ship navy is very vulnerable to advances in stealth and electronic warfare, which makes them basically defenseless. Russian jets are basically invisible to the Aegis radar right now.

With air superiority, you are down to a gorilla war, IEDs/Manpads etc, which can, as shown in Iraq, still be a pretty potent opposition.

So, in Trumps world, their really is only one military opponent, radical Islam, and we have natural allies in Russia in fighting it. Local strong men who can control it and we can control should be in charge, democracy in the middle east is a crazy dangerous idea. This potentially a much cheaper route for the US. While weapons research/development can not be cut regardless of policy, the size of the military could certainly be cut under Trump’s America first world view. I have my doubts whether much will change, these views are of course the opposite of main stream republican views.

13. November 2016 at 16:02

“Didn’t Japan do massive fiscal stimulus, causing it’s debt to balloon to 250% of GDP? Why isn’t fiscal stimulus viewed as a failure?”

It is by this economist.

“(9) The finding suggests that Japanese fiscal policy has been ineffective during the 1990s (but also the prior and subsequent decades, as tests show), . . . ”

http://eprints.soton.ac.uk/339271/1/Werner_IRFA_QTC_2012.pdf

14. November 2016 at 02:28

I liked this post a lot. This Noah Smith guy is sickening…

14. November 2016 at 08:54

From the BOJ:

I believe this is the report the article Noah Smith linked to, was referencing:

“Japan’s economy is likely to continue growing at a pace above its potential through the projection period — that is, through fiscal 2018 — on the back of highly accommodative financial conditions and the effects of the government’s large-scale stimulus measures,

as well as the recovery in overseas economies.”

I couldn’t find anything in the report saying the BOJ was giving up and asking Abe to expand fiscal policy.

From a September 16th, 2016 report (about a month and a half before the aforementioned report was released):

“The Bank will continue expanding the monetary base until the year-on-year rate of increase in the observed CPI (all items less fresh food) exceeds the price stability target of 2 percent and stays above the target in a stable manner.”

14. November 2016 at 08:55

Forgot to put in the link to the September 16th report:

14. November 2016 at 08:56

Hmmm…doesn’t seem like its working…

.

.

14. November 2016 at 08:58

Thanks Alex.

14. November 2016 at 10:47

Phil Mason makes a similar point here: that everyone is sure they’re 100% correct in their political opinions:

https://www.youtube.com/watch?v=SVBd0sKJQz8

Maybe that’s the reason for the IQ hit?