Do central banks worry more about the bond market or the labor market?

Commenter Nick directed me to this FT story:

Mr Williams spoke amid speculation about when the Fed will pull the trigger following more than six years of rates at near-zero levels. Economists including Lawrence Summers, a former US Treasury secretary, have urged the Fed to leave rates unchanged until there is clear evidence that inflation, and inflation expectations, are set to breach its 2 per cent target.

However Mr Williams dismissed such calls, warning of the risk that the Fed gets behind the curve on inflation and that it could end up being forced to hike rates “much more dramatically” to rein in inflation, provoking market turmoil. Given the trails with which monetary policy operates it was better to start raising interest rates “gradually, thoughtfully”, he said.

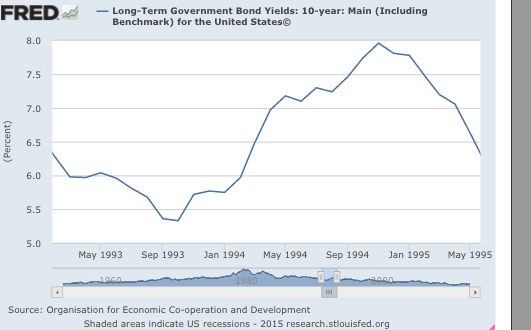

When I hear Wall Street types talk about the danger of a sudden and dramatic tightening of interest rates, they often refer to the awful 1994 “bloodbath” in the bond market, triggered by the Fed’s decision to tighten monetary policy after a period of low rates during the 1991 recession and weak recovery. Here’s a graph showing the rise in 10-year bond yields, which sharply depressed bond prices in 1994.

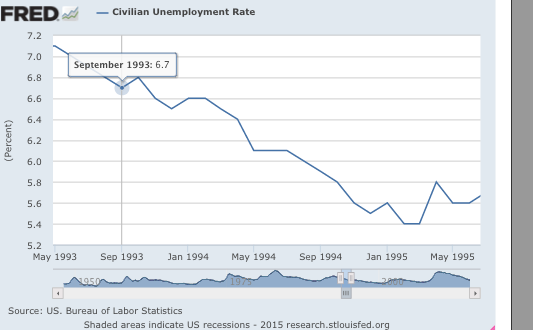

Fortunately, there was no “bloodbath” in the labor market, which is the market I care about:

Nor was there a bloodbath in the stock market. The 1994 move was an example of highly effective stabilization policy by the Fed, despite all the gnashing of teeth in the bond market. I wonder if the Fed is overly concerned about the impact of its policies on the bond market, and insufficiently concerned about the impact on the labor market.

In contrast, during April to September 2008 the labor market was deteriorating rapidly—clearly headed into a recession—while the Fed twiddled its thumbs. Unemployment rose from 5.0% in April to 6.1% in August, which was 1.7% above the low point reached at the cyclical peak (4.4%.) In the past, a recession has occurred 100% of the time when unemployment rose by more than 0.8% above the cyclical low, so the 1.7% rise was a completely unambiguous signal. How did the Fed respond? They did nothing at their September 2008 meeting, 2 days after Lehman failed.

Tags:

13. February 2015 at 09:00

I honestly don’t know what data frmo what markets bankers like Williams and Bullard look at, but I do know that Bullard was dismissive of using data from wages. He called wage inflation “a lagging indicator” of overall inflation. I can’t think of a model that can produce such a result. Maybe they think that wages are a result of a healthy economy as opposed to one driving factor in the economy I like to refer to as “The Demand Curve” [/sarcasm]. Maybe their thought process is:

1. Normalize rate policy

2. Keep inflation low

3. ?

4. Profit!

13. February 2015 at 09:15

Prof. Sumner,

1994 appears to go against your typical story. It’s an interesting case where tightening of monetary policy resulted in a significant increase in a long-term interest rate (10-year Treasury).

Presumably, in this case, the liquidity effect outweighed the income effect and liquidity effect, correct? Isn’t it pretty rare for the liquidity effect to be so relatively strong for such a long period of time (12+ months, in this case)? Any explanation for why the liquidity effect was so relatively strong?

13. February 2015 at 09:16

Excuse me, meant to type “outweighed the income effect and INFLATION effect”…..

13. February 2015 at 10:05

I was a bond trader fresh out of school in 1993. I remember this well.

While it was a bloodbath in the bond market, it was also Greenspan’s execution of the “soft landing” that earned him the nickname of Maestro.

13. February 2015 at 10:44

“They did nothing at their September 2008 meeting”

I was bored so I decided to look at their press release for that date:

http://www.federalreserve.gov/newsevents/press/monetary/20080916a.htm

First they say they’re going to leave the target federal funds rate unchanged (at 2%). Then they said ” the substantial easing of monetary policy, combined with ongoing measures to foster market liquidity, should help to promote moderate economic growth.”

What was this substantial easing? Were they referring to a previous rate cut? Clearly that wasn’t enough.

“The downside risks to growth and the upside risks to inflation are both of significant concern to the Committee. The Committee will monitor economic and financial developments carefully and will act as needed to promote sustainable economic growth and price stability.”

So were they unwilling to cut the federal funds rate due to fear of overshooting the inflation target? Sounds like a good reason to focus on NGDP rather than inflation.

13. February 2015 at 11:06

If your concern is wage levels, why not target wage levels instead of NGDP?

13. February 2015 at 12:04

Bill Woolsey replies: http://monetaryfreedom-billwoolsey.blogspot.com/2015/02/what-do-central-bankers-want.html

13. February 2015 at 12:12

Brit,

If you get really bored you can look at the transcript of the meeting now:

Here’s just a taste of a weighty exchange I enjoyed:

“MR. DUDLEY. I think the expectation going in is, for most people, that you are not prepared to ease today, but if things got really dark from here you would. So the question is, How do you convey that with the right word? You need something in between “closely” and””

MR. WARSH. I think the sentiment we are trying to suggest is watchful waiting. We are not indifferent, we are not clueless, we are paying attention, but we are not predisposed. Hence, Governor Kohn’s suggestion.

MR. KOHN. My suggestion was to substitute “carefully” for “closely.” I agree that “monitor closely” had this other connotation, but I think we should be seen as paying more attention than usual. There might be another alternative.

MR. DUDLEY. “The Committee will carefully evaluate economic and financial market developments.” That means you are on the case.

CHAIRMAN BERNANKE. Well, it is not an analytical thing we are doing. We are just watching closely.

MR. WARSH. Keenly? Carefully?

MR. LACKER. Mr. Chairman?

CHAIRMAN BERNANKE. Yes. President Lacker.

MR. LACKER. Including “closely,” what does that imply about the opposite? I mean,

are we going to be able to take that out?

MR. WARSH. Well, we have done things like “in a timely manner” and other kinds of

phraseology.

MR. LACKER. Yes, but this is an adjective.

CHAIRMAN BERNANKE. No, it’s an adverb.”

13. February 2015 at 12:12

Oh, here’s the link:

http://www.federalreserve.gov/monetarypolicy/files/FOMC20080916meeting.pdf

13. February 2015 at 13:29

I think it’s fair to say that the Fed did in fact tighten too rapidly (or anyway too much) in 1994 and early 1995. It’s clear in retrospect. With no inflation pressure to speak of, they nevertheless raised rates in January 1995 and wound up having to cut them beginning in July of the same year to stave off a recession.

I think this was an understandable mistake. Given that the 1991 recession was the first post-war recession to feature such slow recovery in the labor market, they very likely were surprised by the fragility of the economy at that point. On the other hand I don’t think it could be considered an understandable mistake if they tighten too much too quickly this time around.

13. February 2015 at 13:41

Nick,

That read like an SNL skit.

13. February 2015 at 15:35

Excellent, excellent blogging.

And how about a big basic question: When was the last time the United States had a problem with inflation?

And when was the last time the United States had a problem with a recession and unemployment?

So why are central bankers constantly, even monomaniacally, yammering about inflation?

If the United States ran 3% inflation for a few years, would that be the end of the world as we know it?

13. February 2015 at 18:41

I enjoy reading posts from neutral money theorists who inadvertently concede that inflation does not affect everyone’s incomes equally.

Cantillon Effect bitchez.

13. February 2015 at 19:31

Anthony, I agree that wages can lag a bit, as they are sticky. But the problem I see is that even the leading indicators like TIPS spreads show very low inflation. And 30 year bonds show that very little inflation (and NGDP growth) is expected even over the longer term. I still think the US economy will do OK, as we can adjust to 1.5% inflation if that’s what the Fed gives us—the real problem is what will the Fed do in the next downturn. They don’t have a stable REGIME in place.

TravisV, Good point, although I’m not sure how much of that was Fed tightening, and how much was stronger NGDP growth expectations, perhaps produced by other factors.

Britonomist, Their previous rate cut was back in April. That’s why I mentioned that stretch of time.

Carl, I proposed that in a 1995 paper, but I shifted to NGDP for pragmatic and political reasons.

Nick, That’s kind of funny, especially the last line.

dbeach, I believe those “mistakes” are so tiny that they should count as success in the broader scheme of things. The period from 1984 to 2005 was as good as it gets for monetary policy. And that’s right in the middle. Of course with NGDPLT it will get even better. 🙂

13. February 2015 at 23:49

Good grief.

Just think if Bernanke had been able to teach Lacker some monetary economics, in addition to English grammar.

14. February 2015 at 04:07

Lacker responds, “Well there goes my credibility” and everyone laughs. Then they lose the thread of Lackers objection (‘closely monitor’ implies that there is a lesser ‘not closely monitoring’ state that the fed has been in and will adopt again once the crisis is passed) and decide on ‘carefully’–which is also an adverb, but also implies that usually the fed is not careful in its monitoring of the economy.

14. February 2015 at 04:52

dbeach,

I disagree. The 1994-1995 tightening was required to keep the growth of NGDP on a roughly 5% path-

http://research.stlouisfed.org/fred2/graph/?g=10ME

– while CPI inflation was over 2.5% and unemployment was falling. The tightening neither stalled the recovery nor pushd inflation below target nor lowered NGDP below 4% in any quarter. Also, the federal funds rate remained around the new level until after the 1998 financial crises, while the economy remained stable, so it looks to me like a sensible response to a rise in equilibrium interest rates after the low levels of the early 1990s.

14. February 2015 at 06:43

W. Peden,

Excellent analysis!

14. February 2015 at 08:44

Dear Commenters,

Is it really true that Krugman hasn’t spoken out against the War on Drugs (see post below)?

http://econlog.econlib.org/archives/2015/02/answering_paul.html

14. February 2015 at 09:07

Interesting new post by Bill Woolsey:

http://monetaryfreedom-billwoolsey.blogspot.com/2015/02/sumner-and-glasner-on-identies.html

14. February 2015 at 09:40

Being a young post-graduate economic major struggling to start a career in 1994, the Wall Street bloodbath of 1994 bond market hits me as a micro problem for bond buyers that they need to let go. So the Fed was 3 months behind the the great 1990s economy and the US government cutting deficit and short term interest rate changes adjusted accordingly. At this point in history it is awfully hard to say Fed actions in 1994 had serious consequences on the US economy.

14. February 2015 at 11:48

One difference between 1994 and today is that, in 1994, there was no TIPS market so the risk of the Fed falling behind the curve on inflation was greater. Today, there seems to be much less such risk since TIPS (and inflation swaps) provide an early warning of rising inflation expectations. Granted, the Fed must still distinguish between changes in inflation expectations and changes in risk premiums, but TIPS are still a vast improvement over no TIPS.

On TravisV’s point, is it possible that in 1994 the Fed actually was behind the curve, i.e., long-term rates were rising because the market did not think that the Fed was tightening enough (initially). That could also be why unemployment continued to fall, as the economy overheated. By 1995, the Fed finally caught up, and market worries over long-term inflation fell, bringing down long-term interest rates to “normal”. I don’t remember the chronology of all the events back then, but what would the world have looked like if indeed the Fed was behind the curve in keeping the economy from overheating before finally catching up?

Again, nowadays, there is much less risk of not knowing when to tighten thanks to the TIPS and inflation swaps markets. Admittedly, the Fed must still determine whether to watch these markets closely, or just carefully. 🙂

14. February 2015 at 12:02

Scott,

“I still think the US economy will do OK, as we can adjust to 1.5% inflation if that’s what the Fed gives us””the real problem is what will the Fed do in the next downturn. They don’t have a stable REGIME in place.”

Yes the mixed signals are confusing. They can’t be targeting inflation, because the lack of inflation would clearly have them explicitly saying that rate hikes won’t occur with inflation below target for most of the last several years. Maybe the default “regime” (scare quotes because I don’t think this is explicit) is a ceiling of 2% inflation, floor of 0%, and a ceiling of unemployment of x%. With both measures within parameters rates can be increased.

In the minds of Bullard and Plosser they are acting rationally. I just want to know explicitly what the rationales are.

14. February 2015 at 16:25

W Peden:

“I disagree. The 1994-1995 tightening was required to keep the growth of NGDP on a roughly 5% path”

That is rewriting history. The reason the Fed tightened in 1994 was not “to keep the growth of NGDP on a roughly 5% path”.

The Fed was not targeting NGDP in 1994.

14. February 2015 at 21:09

Benjamin: We had severe inflation in the 70s, along with recession.

If you are a 60-year-old policy maker today, you were probably formed in your thinking by that experience.

You remember the pain that it caused and how difficult it was to end that inflation. That’s why the Fed is so reluctant to risk inflation because policy makers know that it can get out of control and they don’t believe it can be stopped quickly.

14. February 2015 at 21:12

I would add that the Fed has evolved in order to keep inflation low, and policy makers believe the Great Moderation came about because they got inflation under control.

The idea that we would deliberately stoke inflation now alarms them.

As I said, they believe that a) once it starts, you can’t stop it, and b) if you have a recession and trigger inflation, well now you have a recession and inflation on top of it.

14. February 2015 at 21:37

We saw bond prices fall in 08-09 and the economy just went nuts.

When MBS were trading at 50 cents on the dollar, the Fed had to step in to buy them at par to keep major institutions from closing their doors.

We have a highly leveraged financial system and any fall in bond prices is going to break many participants and cause the Fed to step in again.

…

I think the Fed knew in 2008 that the shit was going to hit the fan so they tried to remain calm and hope firms didn’t start calling in their IOUs. Because when you have an insolvency crisis, the Fed is stuck. It works for the banking system, so it must rescue the banks, but must do it without letting the public know what’s going on. It may even be possible that the Fed couldn’t rescue the banks until the economy had tanked and then could pretend it was saving the economy.

15. February 2015 at 05:15

“I would add that the Fed has evolved in order to keep inflation low”

A bit of a weird statement, in that permanent inflation has never been an issue in the US until the era of the Fed. A better way of putting it might be that the Fed has become less inflationist over time.

16. February 2015 at 03:31

“The Fed was not targeting NGDP in 1994.”

I didn’t say that it was.

16. February 2015 at 06:03

Anthony, The Fed isn’t really an inflation targeter, as it has a dual mandate. The 2% inflation target is part of that mandate, but as long as you have a dual mandate you will generally aim for inflation rates above or below 2%, unless unemployment is right at the natural rate.