China: More of the same?

I recently listened to a very good interview of Tyler Cowen by Erik Torenberg. For me, it was 80 minutes of bliss. I tend to agree with the vast majority of his views (even one’s where I had no opinion until I heard his reasoning), with one notable exception—China. Tyler seemed very pessimistic about China’s short-term prospects, and seemed to think they were headed into recession.

I’m not sure the last time China had a recession; the last time they experienced sub-5% economic growth was 1989-90, and growth was still about 4% in each of those two years. I guess you could call that a growth recession. But I’m fairly confident that Tyler expects something considerably worse.

My general view is that most types of recession are almost unforecastable, and that the least bad prediction is always “more of the same.” (Here I’m thinking of ordinary demand shocks or financial crisis; a recession caused by something like the Syrian civil war can be predicted once the war begins.) Thus people who in 2007 didn’t predict a recession for 2008 were making sensible predictions, and those who did predict it were making foolish predictions, and just got lucky. So I’m going to predict no recession for China, this year or next.

Some might argue that there are good reasons to predict a recession, and that it’s not just a wild guess:

1. The Chinese stock market has collapsed.

2. The Chinese yuan has been devalued.

3. The Chinese macro data is ugly.

I say no, those three statements are all inaccurate. The Chinese stock market is about 20% below its recent peak, but still far higher than a year or two ago. There is nothing in stock prices to indicate a recession. You might respond that Chinese government intervention has made Chinese stock prices meaningless. Fine. Then let me rephrase that; there is nothing in Chinese stock prices to indicate a recession, because they are meaningless.

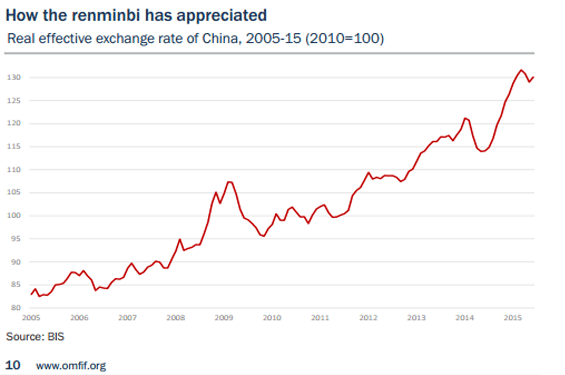

It’s also not accurate to say the Chinese yuan has recently been devalued. The value of the yuan against a basket of currencies has been trending higher for many years. Nothing significant has changed in that regard in recent weeks. The yuan is still higher than a year or two ago, still very strong against almost all currencies around the world. (Indeed too strong, and if a recession does occur it will be due to tight money.)

And the macro data does not indicate a recession. The Chinese economy has been growing at about 7% per year, and while I expect it to slow a little bit next year, I doubt the slowdown will be dramatic.

People often forget that with all its problems China still has enormous momentum. Let me just give you one example. China is building infrastructure at a very rapid pace, all over the country. The construction of infrastructure is itself a part of GDP. But the whole point of building infrastructure is that it provides services. Last year Beijing’s subways provided 3.41 billion rides, more than any other system in the world. But their subway system is still very inadequate, and is often extremely crowded. Many more lines are being built, and they’ll be busy too. Now think about the flow of services from the subway. In terms of Beijing prices it’s pretty low, as they price tickets at around 50 cents a ride. But at New York prices it would be closer to $10 billion/year. I can recall when Beijing’s entire GDP was about $10 billion. (Yes there’s been inflation, but still . . . )

That flow of subway services is much bigger than the year before and next year it will be much bigger still. And the same is true of 100 other examples I could cite. Despite what you read about “ghost cities”, there is still a enormous flow of people from rural shacks to modern urban apartments, yielding a massive and increasing flow of housing services—also part of China’s growing GDP.

China is still less that half as rich as Greece is at the bottom of Greece’s depression. Yes, China has lots of inefficiencies, such as state-owned enterprises, but they also have a labor market that’s dramatically more flexible than any labor market in Southern Europe, and which provides reasonably full employment and fast rising wage rates. Here’s Ambrose Evans-Pritchard:

It is worth remembering that the authorities are no longer targeting headline growth. Their lode star these days is employment, a far more relevant gauge for the survival of the Communist regime.

On this score, there is no great drama. The economy generated 7.2m extra jobs in the first half half of 2015, well ahead of the 10m annual target.

Few dispute that China is in trouble. Credit has been stretched to the limit and beyond. The jump in debt from 120pc to 260pc of GDP in seven years is unprecedented in any major economy in modern times.

For sheer intensity of credit excess, it is twice the level of Japan’s Nikkei bubble in the late 1980s, and I doubt that it will end any better.

At least Japan was already rich when it let rip. China faces much the same demographic crisis before it crosses the development threshold.

It is in any case wrestling with an impossible contradiction: aspiring to hi-tech growth on the economic cutting edge, yet under top-down Communist party control and spreading repression.

That way lies the middle income trap, the curse of all authoritarian regimes that fail to reform in time.

Yet this is a story for the next fifteen years. The Communist Party has not yet run out of stimulus and is clearly deploying the state banking system to engineer yet another mini-cycle right now.

One day China will pull the lever and nothing will happen. We are not there yet.

I’m a bit more optimistic, as I think the reform process will continue. They’ll avoid the middle-income trap. But they haven’t yet even reached the trap—a lot more growth is ahead. If you want to know when that day of reckoning will finally arrive in China, don’t come here looking for answers. I will miss the collapse, blinded by the EMH, just as I missed every other dramatic economic shock in my entire lifetime. My predictions are boring, and always the same:

More of the same ahead

My predictions are usually right, but they get no respect, and don’t deserve any.

PS. I just talked to a Beijing resident who told me that people who cook and clean now make about $4/hour. That sounds low to Americans. But that figure’s been doubling every 5 or 10 years for many decades; 25 cents, 50 cents, $1, $2, and now $4. One more doubling and it would exceed the US minimum wage. Yes, I’d say within about 15 years something’s got to give in China. I don’t know when it will be, or whether there’ll be a soft landing, but I can’t see this blistering growth going on much longer.

Tags:

15. August 2015 at 12:48

-For every U.S. recession after 1968: inverted yield curve. With zero false positives (or false negatives). The last false positive was in 1966-7 (which had a slowdown) and the last false negatives were in the 1930s-1950s. I believe recessions to be very much forecastable. Also, real M1 is almost as good as the inverted yield curve, but had a false positive in the 1990s.

“Thus people who in 2007 didn’t predict a recession for 2008 were making sensible predictions, and those who did predict it were making foolish predictions, and just got lucky.”

-Gary North, among other people, read the signs of tight money in 2006-7 as indicating recession and disinflation. I don’t see how you can call wrong predictions “sensible”.

“People often forget that with all its problems China still has enormous momentum.”

-Bingo. According to one of Cowen’s recent posts, China has the largest difference in urban-rural productivity among all developing countries, with urban productivity three times rural. Simple Stalin-style urbanization could work there for years to come.

“That sounds low to Americans.”

-Well, from the pictures I’ve seen of Shanghai and Beijing, it looks like your estimates of their RGDP per capita were right (as I remember it, around $30K per year). $4 per hour would be higher than in Russia.

“They’ll avoid the middle-income trap.”

-Did Russia? My current prognosis for China is similar to what it is for Russia -about 1-2% trend real growth after hitting Russia’s 2007 per capita income level.

15. August 2015 at 13:12

@E. Harding: “I don’t see how you can call wrong predictions “sensible”.”

Then you should read more about how to evaluate the accuracy of predictions. Is a good decision in a poker hand determined solely by whether you win the hand? No, it’s by whether you correctly play the odds, given the data you had at the time. A good probabilistic prediction can still fail to match some particular real-world outcome.

And, on the other side, a prediction which is based on a flawed model, but which happens to match the real-world outcome, is properly labelled “lucky”, not “good”.

15. August 2015 at 14:45

E. Harding, You said:

I don’t see how you can call wrong predictions “sensible”.”

Surely you can’t believe that.

If I roll a die, and predict it will be 1 through 5, and it comes up 6, I still say it was a sensible prediction, even though wrong.

I’ve studied the yield curve as a recession predictor and you are wrong. It has not always been accurate since 1968, and it’s forecasting ability seems to be getting worse. The consensus of economists missed the last three recessions, despite knowing all about the yield spread.

China is nothing like Russia. I don’t know where China will end up, but probably closer to Taiwan and South Korea than Russia, which is a horrible comparison. Russia relies on natural resources and China relies on physical and human capital, their economies are nothing at all alike.

Don, Exactly.

15. August 2015 at 15:31

Scott,

First, good post. I agree (including your comment).

I think you should get on longbets.org, and take on these predictions, seriously. For example, you have one right here in the comments. The per capita GDP (PPP) of Russia in 2007 is 20128. This is 56% higher than the 2014 number for China, or 46% higher than the 2-15 estimate. In other words, we will likely know in only a few years.

Data from https://en.wikipedia.org/wiki/List_of_countries_by_past_and_projected_GDP_%28PPP%29_per_capita

15. August 2015 at 15:32

“2-15” above should be “2015”. Not used to this new keyboard …

15. August 2015 at 15:40

The Shanghai Stock Exchange composite index is up 75 percent YoY.

Well, there was a day when people thought that market valuations were an acid test of successful government policies. Today, all we hear is that market appreciation is a bubble.

Curiously enough, the right wing has turned darkly suspicious of asset appreciation and prosperity.

I gather today the sentiment on the right wing is that any market appreciation is phony and besides that when you get robust growth you get inflation, an evil that must be extirpated at all costs.

Tyler Cowen is a smart guy. However, he recently blamed Singapore’s deflationary recession on China, and China is growing at 7% a year.

Singapore’s monetary authorities were not mentioned. The right wing has a long, long way to go.

By the way, if state planning and control always fail, please explain America’s agriculture sector, widely lionized as the best in the world in all regards.

I prefer free markets. But it may be that state planning and control, intelligently done, will result in good long-term growth.

15. August 2015 at 16:13

Scott:

Agree with this post that growth will continue because China needs more of everything (OK, maybe less smokers). Even without the new subway lines, the country will need more doctors, nurses, hospitals to function as a true middle income country. Then it needs more managers for these services. Then it needs more lawyers to handle billing, disputes etc.

On debt, does anyone have a breakdown of how much debt is owed by state enterprises, and how much of the state enterprise debt is pension obligations? My gut hunch (based on observations and conversations) is that most of the debt is state enterprise obligations for employment and pension, but couldn’t find a nice breakdown of each. Last Mackenzie study I saw stated most debt is corporate debt, but didn’t have a breakdown of categories, i.e. state enterprises vs private etc.

Some other points I’d like to make after recent trip and stay as a local:

1. Most of the housing stock will have hit their mid-life cycle by 2030, and most of these would be considered sub-standard housing in America. Most Chinese kitchens are smaller than American walk in closets. The water pressure in most homes are not consistent and adequate and bathrooms don’t have adequate ventilation or proper sewage connection (the Chinese bathroom odor is bad in homes also). So I think the upgrade and build out cycle will continue. The Beijing roads also have lots of flooding problems after a heavy summer storm. Lots of infrastructure issues and build outs that need to happen.

2. Regarding pensions and debt, most of the older generation are seeing pension increases, but these are from very low levels. (There are stories in Chinese press of old farmers saying 60Yuan per month pension is the best thing in their lives). The newer generation will expect more and better services and pay. It will be harder to deliver to these expectations.

3. The $4 per hour pay for Beijing cook and cleaning seem high. People I talked to in Beijing say most basic service workers (hotel maids, restaurant cleaners etc) make half that. Pay in Shanghai area is higher than Beijing, BTW.

4. Everyone complains about Chinese government efforts to hold up the stock market, but no one complained about the original Chinese government attempt to burst the stock market “bubble”. One silver lining is the financial professionals are now more confident in dealing with markets. The downside is political interference may produce a political crisis down the road.

5. Everyone I talked to agree that political reform is needed, but no one knows what kind of path to achieve that reform. The situation is strangely reminiscent of the late Ching period, when everyone wanted reform and catch up to West, but there were so many pathways and divergent interests that nothing really happened until sufficient pressure (from Great Powers, defeats in wars) broke the system.

6. One worrying point is the blatant sexism in Chinese work place. Now the 1 child policy has been relaxed, I have heard tales of companies (both state enterprises and private companies) not hiring young women of child bearing age for fear of paying maternity leave. This is something China could ill afford to do.

7. My biggest worry is the erosion of respect and admiration for America. It used to be that I see American movie stars, pop singers all over billboards and ads in China, but I didn’t see any this time. (One ad with Reed Hoffman for Linked In did show up in Shanghai subway.) America remains popular, as I still see people with American flag in their dresses, car dashboards or even scooters painted in entirety with American flag. However, people aren’t as interested in American political process anymore. Instead, America is becoming a nice place to see and visit- like Switzerland, not a model to be emulated. This could be due to many things- our reputation got shredded in Iraq, TPP (or the Second Chinese Exclusion Act), our navy’s need to have an enemy in SCS for bigger budgets. I suspect support for Chinese government activities such as cyber attacks will drop if people held America in higher regard. It does not bode well for our role in the future evolution of China.

Every time I visit, I am encouraged by somethings in China, disturbed by other things, and still remain puzzled by many other things. This time was no different.

15. August 2015 at 16:17

Add on: how China will fare in the future, as it has in the past, depends much upon the People’s Bank of China. The People’s Bank has been growth-oriented in the last decades. Presently it has an inflation target or ceiling of 3.5 percent or it might be 4 percent. They are well under target. They are failing now.

Going forward, it will be fascinating to watch the People’s Bank and if Chinese central bankers have succumbed to the Western banker disease of inflation-obsession.

Fortunately for the People’s Bank, they have the example of the Bank of Japan and Japan’s woes with a deflationary mire from 1992 to 2012.

15. August 2015 at 16:25

LC: Bathroom smell. For reasons that escape me, in Thailand the S shape pipe underneath a sink or drain is usually absent. That shape creates a water trap which limits smells.

Why this simple technique is not adopted….

15. August 2015 at 16:42

“America remains popular, as I still see people with American flag in their dresses, car dashboards or even scooters painted in entirety with American flag.”

LC, I don’t know how well you know Chinese or Chinese culture, but the flags of countries have very different meanings in China (including Hong Kong), and Japan. Having the US flag on things doesn’t mean the person likes the US. Of course chances are he doesn’t dislike the US, but really, it’s very different. If you were to ask them why, what they think the flag represents to them, and so on, the real answer, which you’ll probably never get, is that, for many, there’s nothing behind it. It just looks cool.

This doesn’t mean the US isn’t still popular. The point is the flags don’t tell you much other than that the US isn’t widely hated. The same is true of crosses, particularly in Japan. People wear crosses, prominently, but they’re not Christian. The same is true of the Playboy Bunny. I can go on.

“However, people aren’t as interested in American political process anymore. Instead, America is becoming a nice place to see and visit- like Switzerland, not a model to be emulated.”

This is exactly correct.

15. August 2015 at 19:19

@ssumner

“It has not always been accurate since 1968, and it’s forecasting ability seems to be getting worse.”

-Examples? Citations? I haven’t seen any evidence for this, except for the fairly flat yield curve during the 1990s (which is weak evidence). It was very accurate in 2006-7. If the “consensus of economists” ignored the yield curve, it was the consensus of economists that was wrong, not the yield curve.

http://research.stlouisfed.org/fred2/graph/?g=1Dvv

“If I roll a die, and predict it will be 1 through 5, and it comes up 6, I still say it was a sensible prediction, even though wrong.”

-That is a sensible (though wrong) prediction for a randomly-determined event. It was sensible to expect Russia to have no recession in 2014 if the price of oil did not significantly drop. But it was not sensible to expect the price of oil to not significantly drop. If the price of oil was determined totally by random factors, and only dropped suddenly once every forty years (on average), it would be OK to predict “no recession” for Russia in 2014. Indeed, if a sudden burst of innovation occurred rendering oil obsolete, it would be sensible to predict “no recession” for Russia in 2014. This is because innovation is much less predictable than a continuing rise in oil supply from the Western Hemisphere. My “I don’t see how you can call wrong predictions “sensible”” was not meant to apply totally random events, but ones at least moderately predictable. You don’t know what’s going on in the die-roller’s brain when he rolls the die. If you had a good and reliable neurological and physical model of what would happen when the die rolled, and it predicted 6 among the three or four highest possible alternatives, it would not be sensible to not select 6 out of your five picked numbers. And the recession-yield curve link over the last forty-seven years is far more than moderately predictable. When the Treasury yield curve flips the next time (2016?), I’ll know what to expect.

“Russia relies on natural resources and China relies on physical and human capital, their economies are nothing at all alike.”

-Sure, Russia’s exports are mostly natural resources. But their economies are not “nothing at all alike”. Both of them overachieve given their institutions. Both of them score roughly the same on Heritage’s Index of Economic Freedom, and used to score similarly on the World Bank’s Ease of Doing Business rankings (Russia is now far ahead). Both of them have a legacy of Communism and have dominant-party states (though in China it’s a one-party; in Russia, it’s simply a dominant party). Both of them were great beneficiaries of the 2003-7 boom. Both of them have higher manufacturing as a percentage of GDP than the U.S., especially if natural resource rents are excluded from GDP. China will only end up like South Korea or Taiwan if it makes significant reforms. If not, it’ll end up like Russia. You see, I’m assuming that China’s economic freedom will not significantly improve from now until 2030. I think that’s a pretty reasonable thing to expect.

BTW, my current forecast for China’s growth rate, assuming last year’s was 6%, is 5-7%.

15. August 2015 at 19:38

Or even better:

http://research.stlouisfed.org/fred2/graph/?g=1DvJ

15. August 2015 at 22:21

Not entirely OT: the Atlanta Fed just projected real USA GDP Q3 at 1% (positive).

China is growing at perhaps 6% to 7%.

But remember the Fed must tighten to avoid overheating—inflation inflation overheating!

And China is dying dying dying!

Danger, Will Robinson!

15. August 2015 at 22:44

Prof. Sumner:

I think market monetarists need to address concerns that further China devaluation would trigger massive capital flight out of the country.

David Beckworth touched on that some in his latest post but I’d like to see more.

15. August 2015 at 23:02

Update:

Atlanta Fed just revised Q3 real GDP forecast to…0.7%.

We need a rate hike!

PLease a rate hike!

Inflationary pressures are building to explosive levels!

15. August 2015 at 23:12

TravisV-

I ghosted a long piece on this topic a few months back.

Lots of doom and gloom. The real author was right; and the yuan devalued.

But…Westerners do not understand the People’s Bank of China. They can print money, and are not loth to do so. They can (effectively) capitalize or re-capitalize banks or other lenders. And in coordination with the CCP, direct lending to business or infrastructure projects.

So, some capital leaves China? The PBoC prints more. They are below their inflation targets, and in fact the PPI has been sinking for years. Printing a lot more money is the least of their worries. And the yuan sinks more? Given their export markets, that is bad?

I do not know if the PBoC is mutating. I fear that it is; becoming Westernized.

The old-line nutty CCP’ers were actually better central bankers. As long as inflation was below 5%, they hardly cared. Growth was the target.

I would like to know more about who sits on the PBoC governing board, or if the board just rubber-stamps a CCP plan.

Years back, I read a Hong Kong Monetary Authority paper on the PBoC, that concluded the PBoC had a “revealed preference for growth.” This insightful study does not seem to be online anymore.

It may be that the Hong Kong Monetary Authority, or the Taiwanese central bankers, have good insights into the PBoC. I will check around on the web.

16. August 2015 at 04:45

“Thus people who in 2007 didn’t predict a recession for 2008 were making sensible predictions, and those who did predict it were making foolish predictions, and just got lucky. So I’m going to predict no recession for China, this year or next.”

A number of things wrong here.

First, that is a non sequitur. It does not follow logically from the previous comments. Merely declaring recessions cannot be predicted (other than war caused, and we can add plagues and natural disasters to the list) does not justify “Thus” there.

Second, Austrians who argue that recessions caused by the very inflation you support and write is sustainable, are not merely throwing a dart at a dartboard, or saying the sky will fall tomorrow, and then when it doesn’t, to say the sky will tomorrow again, and again until they are right.

That is not what Austrians are saying. They are saying that inflation of the kind you support, as “normal”, is the cause for why recessions MUST take place. Sure, there could be other more proximate causes, such as war, plagues, and yes, even central banks refraining from continuously accelerating inflation, which would logically eventually go towards hyperinflation, can do it.

But even if all of those things did not take place, if for the example the central bank did not refrain from continuously accelerating inflation, the Austrian argument is that a recession MUST occur. That it must occur because the central bank caused a distortion to relative prices, relative interest rates, and relative spending and profitability, which then caused economic calculation errors vis a vis the absolute real material world that ultimately constrains everything we can do at any given time (but is subject to change by the right human activity).

There is no need to give precise or even imprecise timelines for this. I don’t have to give you a timeline for when a homebuilder will himself realize he doesn’t have enough now and won’t have enough bricks going forward. That is up to the home builder.

Just because I can’t tell you when another person is going to learn something, that does not mean that the cause for why he is wrong doesn’t exist, nor does it mean that understanding the cause, and arguing we all ought to avoid bringing about that cause, and studying the cause in more detail, is all “not useful”.

If the truth is not useful to you, then the truth will win. Every single time. Merely ignoring it isn’t going to make it go away. It isn’t going to magically transform ones ignorant belief into truth. Truth is not what most people believe. Rorty has brainwashed himself and you fell for it.

Truth is the reality of what is regardless of what anyone believes. This of course includes the very important set of truths that are present in your own person when you think about and write about Rortyism. There are objective, albeit tacit, presumptions in those arguments, you just lack the mental tools to know them and work with them correctly.

Remember when you made the (fallacious) comment that inflation could not have been a cause for the 1920s boom and 1929 bust, on the basis that the Fed was not looking at M2 or M3 at the time?!

This is what I mean. What you advocate carries with it events and phenomena that cause other events and phenomena that your tools misdiagnose.

The real reason, I mean the reason that is actually leading you to say “Thus” predicting no recessiom is the default “sensible” one to make, is that your theory compels you to find a way, any way, no matter how horribly flawed it is, to defend central bank existence under your personally preferred mode of activity.

That since you have staked your life’s work in a socialist enterprise of inflating so that aggregate spending keeps growing, you have to attack or ignore all arguments about causes of recessions that themselves tacitly critique the existence of central banks.

See, you feel “safe” in criticizing central banks for lack of inflation during recessions, because that “criticism” (which is akin to “criticizing” a mafia don for not using enough bullets…oooo…so harsh you are!) does not itself constitute a criticism of the existence of central banks. That you are in effect encouraging it by criticing it. That works in both your advantage and the central bank’s advantage. It does not work to my advantage or anyone else’s advantage who knows a much better way.

The environment was already one of how to increase the power of central banks and governments in general. NGDPLT serves as ammo, because it serves as a different intellectual front that people can waste time learning while ignoring what it is that refutes it.

So when you write on your blog “Saying a recession will arrive on the basis of anything other than war or famine or a natural disaster”

I know that you are actually saying:

“You better not blame the Fed for any unsustainable boom if they inflate according to MY personally preferred rate, because even giving a little thought to that whole idea would risk me having to reject my life’s work, and I cannot tolerate such a prospect.”

Ergo the self-fulfilling Rortyist “Truth is what people believe.”

Must be that right?

16. August 2015 at 04:59

Ben, When you compare East and West Germany, or North and South Korea, or Taiwan and Mainland China, it sure doesn’t look to me like state control boosts growth.

LC, Just to be clear I’m not saying that China will grow because it needs more of everything, but rather because it will boost the supply of almost everything. Failed economies that don’t grow also “need” more of everything.

Lots of good comments, I’ve noticed many of the same things that you have noticed. The maid/cook was working in someone’s home, which may be different from another job site. The drop in respect for Americans (which I’ve also noticed) is a healthy sign. When China was very poor American visitors were treated like VIPs. Now it’s not so poor.

I do think the construction quality is gradually getting better, based on personal observation. The new apartment blocks built in Beijing are much better than the garbage built in the 1980s and 1990s.

Ben, The S-shape pipe is sometimes missing in China as well. Very odd.

Absolutezero, Agree about flags. I’d add that as is true elsewhere in the developing world, America (as a place to visit or move or buy property) is far more popular than the American government.

E. Harding, You said:

“You see, I’m assuming that China’s economic freedom will not significantly improve from now until 2030. I think that’s a pretty reasonable thing to expect.”

Given the massive reforms over the past 40 years, I’d say that’s an extremely unreasonable assumption. I expect many more reforms.

The yield curve did not accurately forecast recent recessions. As I recall the YS inverted in 1988, 1998 and 2006, and in none of those three cases did a recession start within 12 months, which was the accepted criterion at the time. Given that no expansion in American history has lasted more than 10 years, it’s pretty bad when forecasts more than 5 years into an expansion can’t get it within 12 months.

Travis, I think the bigger danger is that expectations of devaluation would trigger capital flight.

16. August 2015 at 05:50

Gotta say that broad reaction to the yuan “devaluation” is filled with irony to me. So many believe China’s adjustment towards more of a market based pricing mechanism automatically signals panic and looming disaster. We’d apparently prefer that China blindly manage its way into a ditch…. to slavishly chase the dollar? Somewhere Deng Xiaoping isn’t sure whether to laugh or cry…..

16. August 2015 at 06:16

@Benjamin Cole: Yes, the S-shaped pipe thing is odd, and I don’t know why. From my observations, it seems China needs three things badly: 1. better bathroom designs 2. better parking garage designs (more cars can be parked in very tight spaces 3. some way to reduce the number of smokers who are addicted. Any one of these is a billion dollar market (easily). Now where is the American ingenuity to help solve these problems and make the world better…..

@Absolute Zero, I don’t know about Japan, but I have spoke to some of the people in China, and the flag design does evoke more than just something looks nice. For example, I see lots of American flag designs being used in photo props also, followed by Korean, British and Australian flags. There are exactly zero Japanese flags I saw. Also, several years ago, a Chinese actress was seen modeling a dress with Japanese rising sun, and she was pilloried badly in social media and press and had to apologize for her apparent “ignorance”. So the public is aware of flag symbolism.

@Scott, I see your point. I also think the role of expectations is different in China than Mexico or Russia. In China, the expectations for achieving developed status is much higher because of 1. nationalistic pride 2. Chinese people elsewhere (Taiwan, Singapore) have achieved developed status. However, I’d like to hear more on why you’re more optimistic on China given the debt and bad macro data points Evans-Pritchard pointed to.

@Travis V, some of the “capital flight” out of China are Chinese investments going elsewhere to seek better returns. David Beckworth pointed to some of the twitter debates on Chinese Yuan devaluation, and some of Pat Chaovanec’s comments are just plain bad (a Chinese Yuan devaluation will lead to deflationary shock in the world- really?)

16. August 2015 at 06:21

Wow, for a market monetarist to dismiss the massive market manipulation by saying that, hey, it’s meaningless, is a bit surprising. Especially, when you follow that with a reference to emh.

The fact that Chinese growth is slowing considerably is pretty obvious by looking at commodity markets. They’ll not be building infrastructure at the past pace. The only chance for further growth is a change in the development model. This requires a government that knows how to engineer such a transition. However, the same government has just shown that they have no clue how markets work, rendering their stock market meaningless.

16. August 2015 at 07:25

[…] 3. Scott Sumner makes the bull case for China. […]

16. August 2015 at 07:27

LC, I don’t believe that debt causes recessions–indeed I see almost zero evidence of that. Recessions tend to be caused by tight money.

The most comprehensive macro data shows 7% RGDP growth, which is gradually slowing. I’d expect that to continue, unless someone can give me a good reason to expect something else. Evans-Pritchard also thinks they’ll avoid recession now, but maybe not in 15 years. That seems plausible to me.

Krzys, You said:

“Wow, for a market monetarist to dismiss the massive market manipulation by saying that, hey, it’s meaningless, is a bit surprising. Especially, when you follow that with a reference to emh.”

Yes, that would be pretty stupid, if someone made that claim. I did not.

I said Chinese stock prices might or might not be meaningless, due to market manipulation. The market manipulation itself is very meaningful, it shows government incompetence.

16. August 2015 at 07:32

Scott,

“The drop in respect for Americans (which I’ve also noticed) is a healthy sign. When China was very poor American visitors were treated like VIPs. Now it’s not so poor.”

“I’d add that as is true elsewhere in the developing world, America (as a place to visit or move or buy property) is far more popular than the American government.”

Agree completely. Extremely important observations. Sadly too many people don’t realize this.

LC,

Re: flags. No disagreement in general. That’s why I said “for many”. It’s not a case of either they’re aware of flag symbolism or they’re not. That’s binary thinking. If anything, that’s precisely what East Asia is NOT about.

For Chinese people, the Japanese flag is very much a special case. It is absolutely associated with Japan and everything else that goes along with it. And yes, all the major Western flags are popular, chief among them the US and UK flags. I’m not so sure about the Korean flag. Can you point me at some examples, or at least describe them? For Chinese people, the attitude regarding Korea and the Korean people is, well, interesting, and it’s certainly far less one-sided than anything to do with Japan.

Bottom line, all I’m saying is, it’s very different compared to how a typical American views flags in general, and his own country’s flag in particular. As I said, seeing the design used or worn often does not by itself mean what that country (in this case the US) represents (to its own people, in this case Americans) is popular. It might, just not necessarily so. And, indirectly related to what Scott pointed out, what the US represents to Chinese people is very Very VERY different from what a born-and-bred American thinks his own country represents to him and to the world.

I have to be careful here so I apologize in advance in case this is offensive, but there’s a reason I said the answer “you probably won’t get…” If a person only has a US flag on his shirt because he thinks it looks cool, chances are, if you ask him, he won’t tell you that, ESPECIALLY if he knows or assumes you’re American.

There is always a wall. This is true even if your Chinese is native-level good. Do you have any close Chinese friends with whom you can share, completely comfortably, your deepest most personal thoughts and opinions in religion, politics, and sex?

And the really interesting thing is, a version of this wall can exist even within one individual. You can’t know this unless you’ve grown up with more than one language and culture (and you’re a very self-reflective person), or you’ve learned another language well enough that you can not only think but feel in it. I have opinions and beliefs that my Chinese side finds abhorring, but I can comfortably think about them in Japanese, even talk about them, but only to certain people. And I have thoughts I can only have in Chinese, thoughts my Japanese side finds ridiculous. When I’m thinking and talking purely in English (with an American accent, yes, this makes a difference, as I was brought up by Brits), I’m more extroverted and aggressive than my Chinese and Japanese selves (yes, selves). It is extremely weird, but this happens. Now imagine how it is with different people from entirely different cultures.

16. August 2015 at 08:55

Reform seems to have reversed over the last few years, and the ongoing environmental catastrophe is measurably the worst in the history of industrialization. Still a lot of low-hanging fruit in terms of services, but we have to remember the real question in China like everywhere else is how can they add more value.

Until now the answer was simple: stop being basket-case Maoists. Now that they’ve reached corrupt banana republic income levels, the answer is: stop being a corrupt banana republic. But a hundred countries can tell you, that’s a lot more difficult because the incentives to those in power are much less obvious, or even reversed entirely — even in democracies.

I cannot believe for a moment the Chinese powers-that-be will accept Greece’s political system in exchange for Greece’s income. They are not principled free marketers, they are venal Communists.

16. August 2015 at 09:06

For instance, even aside from the fact no one can even say for sure what was actually being stored at Tianjin (!), the way they’re handling the incident is extremely disappointing — and sadly typical.

https://en.wikipedia.org/wiki/2015_Tianjin_explosions

16. August 2015 at 09:29

Of course China will one or another at some point in time as everybody has their own road to hell. It happens to every economy and the better the economy, the bigger the bust will be. (Were there ever better economies the the US Roaring Twenties, 1980s Japan Inc. or the US during the Dotcom heyday?)

When this happens is anybody guess as it could 2016, but I expect it to be ~2022 as other nations will go first. There are a lot things that go wrong. China has so many people it can avoid the Middle Income trap but the demographics look like Japan in 1990. China is brimming with national pride and has enormous investments in other nations. Will Valenzuela (or African nation) default on their Chinese debt and China gets suck into a terrible Mission Creep war in South America? (And Valenzuela is likely to sell all assets or default.) Could China lose lots manufacturing dominance with higher wages in 2020 and stagant US wages?

Not to get all religious, but does God have the Babylon index? The nation building the tallest buildings is going to evidently fall.

16. August 2015 at 10:18

Benjamin Cole,

Thanks!

16. August 2015 at 11:49

@ssumner

“Given the massive reforms over the past 40 years, I’d say that’s an extremely unreasonable assumption. I expect many more reforms.”

-And Russia hasn’t? Russia’s done a fair amount of reforms too, in the past few years. Doesn’t significantly affect my prospects for the country.

As regards to the yield curve, look at my graphs. The yield curve has been consistently reliable since 1968 (though sometimes not within 12 months, as in 1989, but always within 20).

16. August 2015 at 12:32

China is already in a (deep) recession. See:

http://www.debtdeflation.com/blogs/2015/07/09/will-we-crash-again-ftalphaville-presentation/

16. August 2015 at 12:59

“LC, I don’t believe that debt causes recessions-indeed I see almost zero evidence of that. Recessions tend to be caused by tight money.”

No, debt doesn’t cause recessions. But when the rate of change of debt decreases then that causes recessions. And the rate of change in chinese debt is decreasing. So, China is already in recession. So, debt dynamics DO cause recessions.

And deleveraging makes money tight. See Steve Keen.

16. August 2015 at 15:28

I agree, there is no particular reason to see major economic risks regarding China.

Political risk is much more iffy. President Xi’s anti-corruption campaign (apart from obvious consolidating power elements) seems to be targeting the major risk for command-and-control regimes, which is corruption consuming resources, alienating the populace and undermining the rulership’s control over its agents.

Makes me wonder if he or his aides have read some of the recent political economy papers on Chinese history. Such as

http://www.princeton.edu/politics/about/file-repository/public/Sng_Oct04_2011.pdf

Though massive capital expansion will not reproduce quite the dynamics outlined in the paper, there is the problem of foreign examples. Such as, say, Taiwan.

Of course, traditional Chinese history is full of “corruption led to fall of dynasty” narratives.

The regime has essentially adopted the Mussolini option. The regime’s take on Mao, for example, seems to be very similar to Mussolini’s July 1920 take on Lenin:

“Lenin is an artist who has worked men, as other artists have worked marble or metals. But men are harder than stone and less malleable than iron. There is no masterpiece. The artist has failed. The task was superior to his capacities.”

The Mussolini option is that you accept Lenin’s updated model of totalist politics (no limit on the range or means of political action) but without the command-and-control economics and use national greatness as the motivating political project. But national greatness of that ilk is not good neighbour material. (Ask Albania, Ethiopia, Greece …) And if things get stressed internally, there is the temptation to reach for the foreign conflict option.

At which point, unfortunate miscalculations are likely. If we are lucky, it will just be a nasty border war with Vietnam. If we are not lucky …

And yes, Russia is a terrible analogy to China. Russia is an oil state with some extras.

Also, with Gorbachev’s (to them terrible) example before them, they are not likely to ever put the political cart before the economic horse. Nor be so naive as to try and marry Lenin’s politics with Rosa Luxemburg’s critique thereof. Or create some “Deep State” on the Iranian model (which Gorbachev may have been trying to do). Irony of ironies, neither Leninism nor nationalism has the power of Islam for that purpose.

http://lorenzo-thinkingoutaloud.blogspot.com.au/2015/08/lenin-luxemburg-and-gorbachevs-failure.html

16. August 2015 at 18:21

Benjamin Cole,

Any chance you could provide a link to the article on China you mentioned above? Thanks.

16. August 2015 at 18:34

Travis—

I am hunting around the Hong Kong Monetary Authority….I think some items may no longer be online…

16. August 2015 at 19:03

Benjamin Cole,

Oh well, thanks for trying!

16. August 2015 at 19:39

Travis—

http://www.hkma.gov.hk/media/eng/publication-and-research/research/working-papers/HKMAWP08_06_full.pdf

Here you go.

This paper is a puzzler. First, it suggests the PBoC targets inflation (although high, by Western standards) and monetary aggregates–but not output gaps. My memory of another paper was the opposite. That the PBoC hated output gaps.

Then, the above-cited paper says, “PBoC proposes but the State Council disposes.”

Again, my memory of the State Council is that they want growth, end of story.

Adding to the murk, this paper is seven years old.

It is worth nothing that nearly alone among major nations, China sailed through the 2008 GFC (Israel and Aussies did well; but they are hardly major).

The 2008 China economic performance again suggests to me the State Council said to the PBoC, “Pour it on, bubelah, this is no time for fancy-panting around.”

Too bad the CCP=State Council didn’t run the Fed in 2008.

But, there you have it Travis, a report on a central bank in CCP-land. The HKMA and the PBoC have ongoing relations btw—I do not not know if such relations compromise what is printed.

16. August 2015 at 19:54

Listening to someone who mostly agrees with you is bliss?

17. August 2015 at 04:07

[…] from Scott Sumner, not an […]

17. August 2015 at 04:48

Absolutezero, Very interesting comment.

Talldave, You said:

“Reform seems to have reversed over the last few years, and the ongoing environmental catastrophe is measurably the worst in the history of industrialization.”

I strongly disagree with this, indeed hardly a week goes by that I don’t read about another reform.

I’ve spent a lot of time in Beijing, and while the air pollution is bad, it’s not catastrophic. Shanghai is not as bad. Do you think Beijing’s pollution is worse than London when London relied on coal?

Lorenzo, Very good comment.

Chuck, Yes, if they are much smarter than me, and see all sorts of things I don’t see.

17. August 2015 at 05:40

Scott — Right, Beijing and Shanghai are not that bad, but they’re increasingly service-oriented — it’s the heavy industrial zones that have the worst air quality in the world.

http://aqicn.org/map/china/

This is the 21st century. Most of the industrialized world still relies on coal but doesn’t have these problems. Heck, just scroll over to South Korea or Taiwan or Japan and compare.

17. August 2015 at 05:51

As for reforms, Communist regimes generally announce a lot of pleasant-sounding reforms, but it’s very hard to tell how many of them actually amount to anything meaningful. Meanwhile, in July they locked up up hundreds of human rights activists.

17. August 2015 at 09:24

Benjamin Cole,

Interesting, thank you very much!

17. August 2015 at 09:26

“At which point, unfortunate miscalculations are likely. If we are lucky, it will just be a nasty border war with Vietnam. If we are not lucky…”

Maybe they’ll invade Iraq.

17. August 2015 at 13:58

@Absolute Zero: Yestar cosmetics is Korean and big in Shanghai. Here’s their website (in Chinese): http://www.yestar1992.cn. The Shanghai 3D museum has a photo prop for scaling the Himalyas. There are flags that one can pick for the summit: Chinese, Korean, US, UK, Australia. Most people have Chinese and then Korean flags. My kids had their photos taken at a photo studio. The popular background is Korean signs and flag.

@Lorenzo, the Chinese Communists will do many stupid things, but a foreign incursion militarily is not on the table. They know the Chinese military is not up to Western professional standards. Most of their militaristic propaganda is for internal purposes and is laughably bad (example, see their latest military film: Wolf Warrior). I would say both the Chinese police and military are bordering on incompetence in their real duties, i.e. fight wars and solve crimes. There are lots of reasons for this, but the biggest is economic incentive: The police don’t have much incentive to be responsive to public complaints, and the military don’t have much incentive to fight. (They do have strict top down hierarchy, but the top leaders only have public opinion as one of the priorities.)

@Tall Dave: Yes, the Communist regimes usually announce lots of reforms, but the top policy could be watered down or even delayed by mid-level mis-management. (Example, the reform to allow more civil air space instead of military air space has been slow in roll out and causes all sort of air traffic chaos in China.) However, as to whether thy actually produce something meaningful, one can actually check. For example, the Zhejiang Government Report Gazette is freely available in libraries, and lists specific goals. In the section for pollution, it actually has several pages of tables on specific factories and specific emission elimination targets. Someone could go and then measure whether they have hit their targets by 2017, the stated timeline for the goal. (It’s definitely not market driven in this respect). Also, Chinese government publishes specific journals on economic reform and progress. Much of it reads like Western critique of Chinese economy. Finally, when the administration in power feels insecure, they lock up dissidents. Deng did it, Jiang did it, Hu did it and now Xi is doing it. It’s a measure of fear by these in power. If they fail (and they might fail due to tight monetary policy) in market oriented reforms, the next administration will definitely be more leftist and state oriented.

17. August 2015 at 14:51

Talldave, I travel to China every few years, and the country is changing dramatically, in many ways. The reform process continues.

You say that Beijing is not one of the more polluted cities, and then provide a map that suggests exactly the opposite, that it’s right in the middle of the most polluted part of China, the Hebei region.

17. August 2015 at 15:25

Talldave, You said:

As for reforms, Communist regimes generally announce. . . ”

China’s CP is a CINO regime. Communist in name only.

17. August 2015 at 18:35

Scott,

The issue is that you use emh to argue no recession is in the offing. The question is what market do you take your efficient info from?

17. August 2015 at 19:16

Scott — Well, they still have five year plans and dictatorial powers. I guess you could say they’re limited-market Communists.

http://aqicn.org/map/beijing

Beijing itself has been cleaned up compared to its neighbors, to the point most readings are below 100, but there’s 200+ readings ringing the capital.

17. August 2015 at 19:25

LC — The success of reform always depends on whose ox is being gored. That’s why the air quality is incredibly bad in some areas — e.g. Kashi has four separate readings over 500 today, and one actually pegged the meter at 999 — the people who own all that industry also run the government, and will not accept the costs to clean it up (and perhaps cannot while remaining profitable).

17. August 2015 at 20:23

Lived in China for 7 yrs. Look, any country that feels its necessary to block an ever increasing number of websites, or arrest private citizens for reporting corruption, or imprisoning increasing numbers of lawyers is not doing well. Perhaps Scott is enamoured with the shiny high speed rail and skyscrapers. I was at one point too. Then the veneer starts to fade when you see the rottenness underneath. I think there’s no evidence that the political system will automatically remain stable going forward.

And it’s impossible to envision China achieving Taiwanese levels of prosperity without Taiwanese standards of rule of law. To achieve this, the party needs to loosen the reins, when its currently doing exactly the opposite, intimidating lawyers and forcing them to swear oaths of loyalty to the party. Economists give Chinese politics short shrift but that’s the most important part of the equation.

17. August 2015 at 22:55

LC,

Yes, of course many Korean things, including brands, not to mention shows, music, and stars, are popular in China, but we were specifically talking about flags. Didn’t know about the Himalayas thing and the flags at the museum. Interesting. Now I know what to pay attention to and what to ask. Thanks.

18. August 2015 at 02:47

Kryzs, I believe if there was going to be a recession the Chinese stock market would be much lower.

Talldave,, Beijing has been cleaned up? You mean the US media is inaccurate in their reporting on China? Hmm, I wonder what else they are inaccurate about.

Andao. I actually agree with you that China’s not doing well, in an absolute sense. But I also think imprisoning a bunch of reporters is better than killing 30 million people. And that a per capita income of $10,000 (while low) is better than $400. But that’s just me, you are free to disagree.

I’ve said many times that China must do lots more reforms to catch up to Taiwan.

How often did you visit China in the 1980s and 1990s? I’m just trying to get a sense of your point of comparison.

18. August 2015 at 10:25

Scott,

Agree. A few things.

Binary thinking. Or, discrete and quantized thinking. Things are put into buckets. B is “good”. A is far worse than B. If the difference is big enough, A is just dismissed. A continues to be dismissed even as it improves. When A has improved enough, it becomes “bad” compared to A. This label stays even as A continues to improve further. A has to become very close to B, then it’s “good”. The truth is, usually, some things are better, some are worse, some are better and worse at the same time. The important thing, the only important thing, is the change is on net positive.

Bias in data and perception. Example: a person sees someone peeing in the subway. He’ll notice, tell his friends, take a picture, and so on. But he doesn’t notice all the other people not peeing. This applies to everything. Many Hong Kong people are mad at mainland people’s bad behavior. But if a mainland person behaves normally, he won’t even be noticed. If anything, reporting corruption is encouraged. There’s even an app for it.

Non-iterative thinking. Someone initially believes A. Later he has new experience and he realizes A is completely wrong, it’s B. Now he believes B. But then he stops. Why? If A can change to B, why is he so convinced about B now? This happens a lot with people who go and live in another country for a while. A lot of their prior beliefs are overturned, and now they think they know. But even newer experience can overturn what they now believe just as new experience overturned their original beliefs.

Andao: “… without Taiwanese standards of rule of law.”

I almost fell out of my chair at this. Do people know how corrupt Taiwan was in the 1970s, 80s, and 90s? Back then in Hong Kong people (including some from Taiwan) used to joke that it’s better there weren’t elections in Hong Kong, at least people couldn’t buy votes. Do people know their legislators had fist fights? (This also happened a lot in South Korea. Do people know that?) Do they know that the DPP, when it was founded, was an illegal political body?

18. August 2015 at 13:22

[…] pessimistic about China’s economic prospects. No doubt you’ve seen many of them. Here’s a different take. Economist Scott Sumner is bullish on China, or at least not bearish on it. He says the bears […]

18. August 2015 at 13:27

I doubt the Chinese political system is much worse than other developing countries that have similar socioeconomic development. Also, China is a large country. It’s not hard to image that Beijing and Shanghai will reach the prosperity of Taiwan, and the population in these areas are two times greater than those that are in Taiwan. While some areas in China will be trapped in middle income trap, all of China will not.

18. August 2015 at 14:10

Scott,

The meaningless market should be much lower?

20. August 2015 at 04:24

Absolutezero, Very good comment.

Chu, The middle income trap is often associated with ethnic diversity–which is not an issue in China. I see no plausible equilibrium where Shanghai is a developed country and Chengdu is middle income. It just doesn’t seem plausible to me, although I admit I can’t prove it.

Kryzs, Good point. In the US, recessions have been almost unforecastable, but the EMH isn’t necessarily the best explanation. I probably should have made a different argument.

23. August 2015 at 10:41

[…] Scott Sumner is less pessimistic on China and has more on the perils in attempting to forecast recessions. […]

24. August 2015 at 07:21

[…] Scott 9 days ago, talking about China, but then he […]

24. August 2015 at 11:12

Care to temper your statements a bit? Or just retire in disgrace…

27. August 2015 at 19:10

[…] what things look like in three years, etc., that’s fine. But come on, don’t act like predicting “more of the same” two weeks ago is consistent with what just […]