Bubble world is here

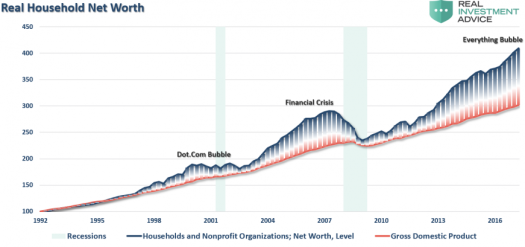

Lance Roberts has a new post with a neat graph:

I like the term “everything bubble”. For a number of years I’ve been claiming that the 21st century would be full of “bubbles” that were not actually bubbles. In other words, asset valuations would be higher than expected based on traditional valuation methods, but nonetheless justified. This is from the spring of 2015:

I like the term “everything bubble”. For a number of years I’ve been claiming that the 21st century would be full of “bubbles” that were not actually bubbles. In other words, asset valuations would be higher than expected based on traditional valuation methods, but nonetheless justified. This is from the spring of 2015:

In the 21st century, pundits will be unable to see anything other than recessions and “bubbles.” There will no longer be periods of stable growth without “bubbles,” like the 1960s. Of course bubbles don’t actually exist, but low interest rates as far as the eye can see means that asset prices will look bubble-like unless artificially depressed by a tight monetary policy that drives the economy into recession.

Of course we were told back in 2015 that this was all an artificial bubble due to QE, which is now being withdrawn as the Fed raises rates. And yet asset prices keep rising.

Back in 2011 I challenged Robert Shiller’s pessimistic take on stock prices:

But (seriously) are stocks now overvalued? Because I’m an efficient markets-type, the only answer I can give is no. So why does Robert Shiller say yes? Apparently because the P/E ratio is relatively high by historical standards. And he showed that for much of American history investors did better buying stocks when P/Es were low than when P/E ratios were high. Of course hindsight is 20-20.

I’d rather not get into the minutia of all the various ways of calculating P/E ratios. And I have no idea where stocks are going from here. Instead I’d like to focus on three arguments for relatively high P/E ratios in the 21st century American economy (however you’d like to measure them):

Of course I was careful not to predict rising stock prices, as if I had been successful it would lower my reputation. I’m an EMH guy who claims it’s impossible to forecast stock prices. But I did challenge Shiller’s claim that P/E ratios were too high in 2011. That judgement may have been valid in the 20th century, but performance in past centuries is no guarantee of performance in the current century.

Again, the 21st century is the “bubble” century.

PS. I was amused by this exchange in a recent NPR interview of Jay Powell:

Ryssdal: Let me ask you then about inflation and about prices which are as you say starting to tick up to where the Federal Reserve wants it to be. I’ll note here that we’re talking at 8:24 in the morning on the day that consumer prices come out. They come out in six minutes. With the caveat that this is going to air now in five, six hours from now, whatever it is, you have the number in your back pocket, you know what the number is. Inflation CPI?

Powell: Well, let’s just say that I do get a look in advance at these things. Yes.

Ryssdal: You’re not going to tell me what it is even though we are not going to air this until —

Powell: Definitely not. Definitely not.

Ryssdal: Score one for the chairman’s adherence to the rules.

Powell: Not going to say anything that would suggest what it might be.

Not even a tweet?

HT: Pat Horan

Tags:

15. July 2018 at 16:10

Scott Sumner had an interesting post recently about a Fed that would monitor and adjust policy on a daily basis, as new information came in.

Seems to me that BLS could adjust the CPI accordingly. That is, we would have a daily reading on the CPI as information came in, from many new sources as well which would be obtained through the web.

In general, the less secrecy in government, the better,

15. July 2018 at 16:18

Good post, but in general, it’s pretty easy to predict stock prices will be up in the long-run, as long as economic growth remains positive in the long-run.

15. July 2018 at 17:48

Isn’t the prediction that 21st century would/will be full of bubbles an implied prediction that real rates of return will remain low? And if so, do we have sufficient information to know that will be true? For example, could the further aging of the ever-richer Chinese population and the expected rapid growth of the African population lead to a relatively rapid rise in real rates?

15. July 2018 at 18:23

Trump didn’t “say or suggest” anything about the jobs report before it was released, ever.

15. July 2018 at 18:43

Rajat, Possible, But I’d bet against that happening.

15. July 2018 at 18:53

Scott,

Bubbles go both ways, right? I’ve reworded your sentence to reflect this:

“In other words, asset valuations would be higher AND LOWER than expected based on traditional valuation methods, but nonetheless justified. “

15. July 2018 at 23:36

In the depths of the financial crisis, asset prices didn’t get “cheap” based on historical averages. They just got down to average (and only briefly).

But they were cheap. It’s just that the definition of cheap has shifted up.

16. July 2018 at 01:56

OT but interesting:

Sovereign fund gears up to invest at home — CHINA Investment Corp. (CIC), the nation’s US$941 billion sovereign wealth fund, wants permission to invest in domestic stocks and bonds for the first time, as per reports, as it tries to end restrictions on its mandate following government moves to open up financial markets.

—30—

A trillion-dollar soveriegn wealth fund.

16. July 2018 at 06:06

“Of course I was careful not to predict rising stock prices, as if I had been successful it would lower my reputation.”

I think I know what you are getting at, but I’d be careful with this type of statement. There are equity level returns to be had in them thar stock markets. Predicting rising stock prices is a no brainer.

16. July 2018 at 07:44

There’s a bubble in calling bubbles

I’m still shocked at the number of people who are scared of buying stocks

16. July 2018 at 08:07

Equity premium puzzle will be sloved!

16. July 2018 at 08:15

Ah.. I remember some kind of the EMH idea were spreaded in market participants at 2006 to 2007.

17. July 2018 at 10:44

I recently had reason to look back on historical mortgage rates. Having done all of the mortgaging post-2000, I did not realize how much higher rates used to be. That alone is a reason for 21st Century valuations to be different.

17. July 2018 at 12:43

A few years ago Bernanke suggested that rising asset prices be considered in setting Fed policy and not just consumer prices. You’d have thought he suggested we worship the devil. Does Sumner worship the devil?

20. July 2018 at 15:31

Off topic, but …

It’s hard to imagine a better argument for prediction-market-driven NGDP level targeting than this:

https://money.cnn.com/2018/07/20/investing/trump-interest-rates-fed-tweet/index.html

If monetary policy was systematized, then ….

21. July 2018 at 14:50

I’m not sure why this blog is called ‘the money illusion’ as that implies the author has a good grip on the reasons for high asset prices. Instead, the author supports the idea that high asset prices are justified by low rates (unless I’m missing something here?). This theory is a complete crock and has been debunked a thousand times.

There are bubbles in virtually every asset that produces a cash flow, the bubbles are huge by historical standards and they are a serious threat to both the financial system and the global economy. If you understand finance (properly) you’ll know this statement to be true.

21. July 2018 at 17:55

Kenneth, Yes, I’ll do a post on that, maybe over at Econlog.

22. July 2018 at 13:00

TheLege, Bubbles do not exist—it’s a cognitive illusion. I sympathize, as even to me it looks like the world is full of bubbles. But they do not exist.

22. July 2018 at 13:29

Ok got it. Basically EMH says that the markets are in equilibrium at all times (or something to that effect)? That being the case, in your world, what causes sudden crashes in price?. It seems to me that disequilibrium would always lead to small and constant adjustments in prices but sudden and sharp falls suggest more serious structural issues in markets.

22. July 2018 at 16:23

@TheLege: Nothing in the EMH has any limit on how new information could affect prices. There is no requirement at all that price adjustments be “small and constant” and never “sudden and sharp”.

Asset prices are always relative to expectations about the future of the economy. Expectations can change arbitrarily quickly, in an arbitrarily widespread manner. The consequence of changed expectations on asset prices is not limited.

23. July 2018 at 01:01

Thanks Don. I was just curious. EMH is not for me though – the theory runs contrary to my Austrian sensibilities 🙂

25. July 2018 at 17:24

TheLege, Big price changes are not easily explained, but anti-EMH theories don’t have any better explanations.

26. July 2018 at 17:38

Scott,

The big price and valuation change in Facebook is easy to explain. The public became aware that its expectations of the company’s future value were unrealistic. And with that awareness the Facebook bubble popped.

Now if in ten years Facebook is valued higher than it was yesterday, you will say there was no bubble in Facebook stock! And sure you can. If you get to define what is a financial bubble I’m confident you can create a definition that supports your claim that bubbles don’t exist.

But those who define a bubble popping as a rapid price decline in valuation due to a resetting of expectations will have plenty of evidence supporting their definition.