Is NGDP a useful way of thinking about monetary shocks?

In a recent post I discussed 4 possible interpretations of Tyler Cowen’s post on risk-based recessions:

Perhaps the claim is that we might have a recession this year due to risk, despite 3% plus NGDP growth. If so, I very strongly disagree. (This could be viewed as a version of real business cycle theory.)

Perhaps the claim is that if there is a recession, then NGDP growth will slow, but that this will not be the cause. In other words, even in a counterfactual world where the Fed kept NGDP growing at 3% plus, there would still be a recession for non-monetary reasons. If so, I very strongly disagree. (Again, an RBC-type claim.)

Perhaps the claim is that falling NGDP growth is a necessary condition for a recession this year, but it will be caused by growing risk and there is nothing that monetary policymakers can do about it. If so, I strongly disagree. (A traditional Keynesian claim)

Perhaps the claim is that falling NGDP growth is a necessary condition for a recession this year, but it will be caused by growing risk that monetary policymakers are too cautious to do anything about. If so, I mildly disagree. (A New Keynesian claim.)

Tyler has a new post that discusses some of these issues. He does not refer to this list, but as far as I can tell he has a fairly eclectic view of business cycles, and thus probably doesn’t want to get pinned down to any single hypothesis. I’ll go further and speculate that he believes both the RBC and the Keynesian explanations may each apply in some cases. That is, sometimes recessions are caused by real shocks, and could not be prevented even if the Fed were able to stabilize NGDP growth. And sometimes there are shocks that it is more useful to think of as “non-monetary” even though they work at least partly through the channel of causing NGDP changes that destabilize the economy. Perhaps because of some problem such as policy lags or the zero bound, the central bank may not be able to prevent those NGDP shocks, and if they are ultimately caused by some other factor, such as financial distress, then it makes more sense to see the recession as being caused by the financial distress, not the “tight money” label that MMs pin on falling NGDP.

I’m not certain I’ve interpreted his views exactly right, but I’ve tried to state them in a way that I think is quite defensible.

The post also has an extensive critique of areas where market monetarism may overreach, i.e. make claims that are unsupported by evidence, if not borderline tautological. As I read though this criticism I kept coming back to an observation that seems central to me, but perhaps not to Tyler. I see his strongest criticism as boiling down to something like “Market monetarism is flawed because we lack a real time indicator of NGDP expectations.” (My words not his.) That is we lack a NGDP futures market. And that is indeed a big flaw.

Right now lots of smart market analysts, like Jan Hatzius, suggest that financial conditions have recently tightened enough to slow growth by 1% to 1.5%. But it would be better if we had a NGDP futures market. Indeed even last year at this time we had the Hypermind prediction market, which although flawed, was good enough to give ballpark NGDP estimates. It showed that no recession was expected in 2015. But now we lack even that.

This is important because MM theory says NGDP expectations are the proper measure of the stance of monetary policy. Lacking that market, we sometimes fall back on actual NGDP. And Tyler points out that if the central bank targets inflation, then NGDP and RGDP shocks would be perfectly correlated, even if there were no causal link.

So far I’ve been trying to describe his argument in as positive a way as possible. Now I will start disagreeing:

Here is a recent Scott Sumner post, mostly about me. It’s basically taking the other side of what I have been arguing, and I would suggest simply disaggregating the ngdp terminology into a more causal language of nominal and real shocks. Surely there are other independent, ex ante signs for judging the tightness of monetary policy, rather than waiting for ngdp figures to come in, which again is citing a transform of the real gdp growth rate as a way of explaining real gdp.

I find these issues come up many, many times in market monetarist writings. I think they have basically the right policy prescription, and could provide the world with billions or maybe even trillions of dollars of value, if only policymakers would listen. But I also think they are foisting a language of causality on the business cycle problem which the rest of economic discourse does not easily absorb, and which smushes together real and nominal shocks into a lower-information accounting variable, namely ngdp, and then elevating that variable into a not entirely deserved causal role. We ought to talk in terms of ex ante, independent measures of monetary policy looseness, not ex post measures which closely resemble indirect transforms of real gdp itself.

My focus when estimating the stance of monetary policy has generally been NGDP forecasts, not actual NGDP. And NGDP forecasts are available in real time, and hence not subject to the “waiting for ngdp figures to come in” critique above. This point can be made much more effectively by focusing on the past two months. Tyler says money is not that tight:

I say [monetary policy is] “not that tight,” while leaving room open for the possibility that it should be looser.

What metrics might we look at? Federal funds futures no longer expect imminent further rate hikes from the Fed. Expected rates of price inflation have been very close to two percent. No matter what you think about the structural component of labor supply, cyclical unemployment has recovered a great deal over the last few years. And that is through the period of “taper talk” of almost two years ago. Consumer spending is doing OK, not spectacular but not cut off at the knees. And while in very recent times price expectations are headed downwards away from two percent, this seems to stem from negative real shocks, to which the Fed has responded passively (perhaps unwisely). That’s different than the Fed tightening. There was a quarter point rate hike from December, which is a small tightening for sure, but I don’t see much more than that.

Here’s where I strongly dissent from the thrust of Tyler’s argument.

1. The fact that markets now expect zero Fed funds rate increases this year, not the two expected (or 4 promised) in December, is not a sign that money is getting looser, it’s more likely a sign it’s getting tighter. While on any given day a rate increase is tighter than not increasing rates, over a 12-month period policy is highly endogenous. If a crystal ball told me rates would be at zero for another 20 years, I’d take that as evidence that money is currently way too tight.

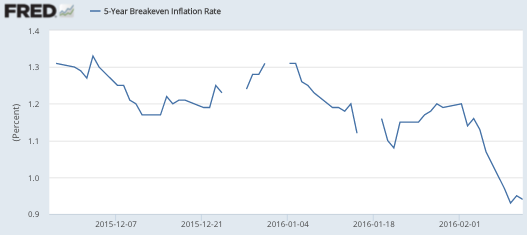

2. Tyler’s claim that expected inflation is 2% is linked to an earlier post, which discusses not market forecasts, but the forecasts of economists. Two months ago the consensus of economists called for about 1.8% to 1.9% PCE inflation over the next few years. But even then, 5 year TIPS spreads showed about 1.2% to 1.3% CPI inflation, which is about 1.0% PCE inflation. And as the following graph shows, market inflation forecasts have fallen much further in the past two months, so even if policy was roughly on target in December 2015, it’s too tight now.

3. A quarter point rate increase in December may or may not be a “small tightening”. The size of the rate increase is not a reliable gauge of the degree of tightening, because monetary policy affects rates in two partially offsetting ways (the liquidity effect vs. the income/Fisher effects). Important recessions (US 1937, Japan 2001, eurozone 2011) have been caused by very small rate increases.

4. The recovery in the labor market doesn’t tell us much about the risk of recession, other than that we aren’t in one yet.

5. Any “real shock” that reduces NGDP expectations because the Fed responded passively is also a monetary shock. It could be both monetary and real. If frightened Venezuelans started hoarding US currency and the Fed didn’t print any more currency, and NGDP fell, I’d call that a tight money policy even if it was “passive.” In any case “passive” is a meaningless concept in monetary policy, as change can occur along many dimensions; fed funds target, reserve requirement, the monetary base, IOR, exchange rates, price of gold, TIPS spreads, etc., etc. At any give moment, policy will be active along some dimensions and passive along others.

My views on current business conditions are pretty similar to those of Tyler, AFAIK. I think we both see a modest risk of recession this year, but less than 50-50. So suppose there is a recession this year—can I say, “I told you so”? I certainly didn’t think the rate increase in December would lead to recession (although some other MMs were more pessimistic.) But that misses the point. Sorry to be so long winded, but wake up here, this is the key point.

The Fed needs to always keep the “shadow NGDP futures price” close to target. If at any time they let it slip, as they did in September 2008, and if MMs point out that it is slipping, and if the Fed does not take aggressive actions that it clearly could take to prevent if from slipping, then yes, it’s the Fed’s fault.

That italicized statement does not involve any Monday morning quarterbacking. I’m not going to blame them for anything that they cannot prevent in real time. But recall that currently they are not even at the zero bound. Let’s explain this with a simpler example. We do have TIPS spreads, so we don’t need shadow prices for inflation expectations. MMs claim that even with the liquidity bias in TIPS spreads, the current ultra-low 5-year spread suggests money is too tight for the Fed’s 2% inflation target. That doesn’t mean we’ll have a recession, but if the Fed wants to hit their 2% inflation target they need to ease policy. If they don’t, and if they fall short of their inflation target, then MMs will have been right.

Now I think it’s possible that the Fed will luck out here, and perhaps even hit their inflation target. But on balance I believe markets are right more often than not, and the Fed will once again fall short.

Note that if we had a good NGDP futures market I could have reduced the length of this post by 80%. It would be easy to address Tyler’s various points by referring to NGDP futures prices. Either they predict recession or they don’t. Either they are controllable at the zero bound or they are not. They would be real time indicators, with no Monday morning quarterbacking involved. But we don’t have that market, so the best we can do is estimate a shadow price of NGDP futures by looking at TIPS spreads, bond yields, stock indices, commodity prices, and a zillion other factors, and construct the best estimate we can of the current market NGDP forecast. That’s the key variable for me, not actual NGDP.

Actual NGDP comes in to play when we consider level targeting. MMs believe not just that level targeting would make recessions shorter, we also think it would make them less likely in the first place. So the one area where we are justified in criticizing the Fed based on actual NGDP numbers is the level targeting issue; are they trying to get us back to the trend line? If they don’t level target, then recessions are more likely to occur, and will be deeper.

PS. I’m not sure what Tyler means by saying NGDP is a transform of RGDP. Does this mean NGDP * (1/p) = RGDP? If so, isn’t that true of any variable?

M * (V/P) = RGDP

In general,

X * (RGDP/X) = RGDP, where X is the price of a can of tomato paste.

Nor do I understand the “tautology” remark attributed to Angus. Obviously it’s not a tautology for Zimbabwe. The only way I can make sense of this complaint is that the Fed actually does target inflation, so it makes sense to assume P is stable, whereas it doesn’t make sense to assume V/P or (RGDP/X) is stable. And if we assume P is stable then NGDP and RGDP become highly correlated. Fair enough. But as Nick Rowe recently point out, what matters is the counterfactual where NGDP is kept stable. Which brings us back to the list at the top of this post. I think MM critics need to think long and hard about exactly which of those four critiques is the most important, and what sort of empirical evidence we’d use to evaluate that critique.

PPS. I also have a new post over at Econlog.

PPPS. I will be doing a “Reddit” on the 23rd at 1 pm, whatever the heck that is. “Ask me anything.”

Tags:

16. February 2016 at 18:52

Cowen’s post shows why the “tight money” vs. “passively tight” semantics are more distorting than he realizes. One argument for NGDP is that it provides a picture of how the Fed is reacting to circumstance, as opposed to just describing changes in Fed behavior. This argument from Cowen is revealing:

“Ngdp is an accounting summation, so I still want to know the real cause of the slower growth in real gdp. Let’s unpack at the most basic level whether the active cause was Fed tightening on the nominal side, or instead a negative real shock, followed perhaps by excess Fed passivity. That is one reason why I think of it as information-destroying to cite ngdp as a cause of developments in rgdp.”

If you start with the prior that monetary policy is always in relation to the economy, and not something that can be judged in isolation, then that quote is wrong. It seems to confuse the questions, “Does NGDP tell more about policy stance”, and “Does inflation and RGDP require more modelling than NGDP?”

16. February 2016 at 18:53

Ugh, my messy comment shows how more writing can be information destroying for the relevant question.

16. February 2016 at 19:07

I’ll ask you something Sumner. Have you read this short post on NGDPLT, and what do you think of it?

http://mungowitzend.blogspot.com/2014/08/the-tools-of-ignorance.html

16. February 2016 at 19:09

@myself – I second “A’s” argument above.

16. February 2016 at 19:19

Excellent blogging.

Tyler Cowen is a intelligent man, and tries to be open-minded.

Yet it certainly seems obvious that monetary policy is very tight. How else to explain the outlook for PCE inflation and interest rates?

As Milton Friedman said, low interest rates are a sign monetary policy has been tight. We have 10-year Treasuries trading at 1.6% or so.

Volcker never even dreamed of this.

I wonder if the USA entered long-term deflation, would even then some people admit money was tight?

Beyond that, what would be the harm of monetary policy erring on the side of growth for a few years? Do we end up like Venezuela, or more like the 1980s-1990s USA?

I suspect more like the 1980s-1990s USA. Not so bad.

16. February 2016 at 19:35

Scott, corporate bond spreads are a pretty good proxy for NGDP – thousands of people laying out billions to figure out whether the cash flows for the corporate sector will suffice to make debt payments. There is plenty of incentive to get it right, and they often do.

https://research.stlouisfed.org/fred2/graph/?g=3ub1

If monetary policy is easy, then long interest rates rise. If monetary policy is tight, the long rates fall. QED.

I really would have thought that the whole NGDP/BASE = I thing would have cleared this up. If rates are fixed, then BASE=NGDP. If NGDP is slow, it’s the Fed’s fault. How does Cowen feel about Japan’s monetary stance, anyhoo? Clearly extraordinarily tight?

16. February 2016 at 19:50

The combination of RGDP and inflation forecasts seem to be as close as we can get to an NGDP forecast right now (I was disappointed the NGDP futures market didn’t catch on, but I had predicted that there was not enough interest, at least not yet). Knoema has a collection of both but I can’t seem to link to them here or at MR, though it’s easy enough to Google.

I noticed you didn’t stake out a position on the current stance of monetary policy, which I think is a fair request on Tyler’s part. Here was my reasoning, ymmv: I believe nominal GDP growth of 5% is the optimal policy for the United States in 2016 (to support a 4.5% path in the long run), so I would say right now money is a little too tight, because inflation/TIPS spread + GDP estimates (in effect, the market/expert prediction of NGDP) is less than 5% (and mostly has been). I believe GDP is currently forecast at around 2.5% and inflation at about 1.75%, so monetary is too tight by about ~.7% of NGDP (1.025*1.0175-1.05).

But I think the larger point that Tyler misses is that NGDPLT has a lot more consequences during a recession or a boom than in middling periods where it is very similar to inflation targeting, so if there is a recession, then these statements on the stance of monetary policy will be important.

16. February 2016 at 21:09

Scott, off topic but I thought you might find it interesting that Ben Bernanke is still giving the party line in defending IOR:

http://www.brookings.edu/blogs/ben-bernanke/posts/2016/02/16-fed-interest-payments-banks

If the monetary policy transmission mechanism is the fed funds rate, how does he explain the effectiveness of QE3?

As for Reddit, being invited to do an AMA is the big time of social media. People will post questions to something similar to the comments section of your blog. One difference is that replies to each comment/question will show up directly below that comment. So as the Reddit moderator handles your responses to specific questions, they’ll show up directly below the question. Given that you’ll likely be dealing with an audience of lay persons (much like myself), it might help to get people to understand that aggregate spending equals aggregate income to start with. I suspect that if I had known this early on when I first started educating myself, I probably would have appreciated NGDPLT more quickly.

16. February 2016 at 23:05

Haha yes, you’re doing an AMA on Reddit! It means you are an internet celebrity now! Reddit is a web of discussion forums populated by hardcore internet denizens, and the AMA is a regular feature. Many famous actors and other luminaries (Snowden, Musk, Obama) have been on there before. You don’t have to answer all the questions, but prepare for them to be fairly irreverent. If you get humorous sequences of responses (to your own responses) it means you’re doing well.

17. February 2016 at 03:03

[…] has been noted already by Market Monetarists and others that George Osborne and his UK Treasury team are concerned about the low level of […]

17. February 2016 at 04:12

Isn’t RGDP a transform of NGDP ? Which one is estimated more directly ?

17. February 2016 at 04:44

J.R. Robazzi asks: “Isn’t RGDP a transform of NGDP ? Which one is estimated more directly ?” – yes it is. NGDP = RGDP + Inflation. But there’s NO causation between NGDP and RGDP. More inflation does NOT increase RGDP, nor does somehow pumping up NGDP affect RGDP in any way. See the link above on my first post on how Sumner is confusing a backwards looking accounting identity (with NO predictive power) with some sort of predictive equation. The ignorance is appalling.

17. February 2016 at 04:52

@Ray, you’re implying too much. All I said is that NGDP is the only thing we can measure (actually, estimate), and the other two are ideas dependent on models (price indexes, deflators, real output, etc)

17. February 2016 at 05:59

I think we both see a modest risk of recession this year, but less than 50-50.

At this point of the global economy, don’t you have to identify where the recession is occurring? There are recessions in Russia, Brazil, and oil producing Middle East countries. (Or even local recessions in Oklahoma.) However on the US or China, I agree with you that it is less than 50 – 50%.

Additionally, with a falling population, should the definition of recession change for Japan? A decrease in GDP might not signal a true recession in living standards. (Also, with Japan falling population/GDP, does that possibly change the 1970 recession definitions as well? I tend to think the entire 1974 – 1982 period as a long term recessionary period.)

17. February 2016 at 06:39

Although you can’t get a good estimate of future NGDP, you can get a good estimate of real-time NGDP by combining the 5 year TIPs breakeven rate with the Atlanta Fed’s GDP Now tracker. Using this measure, the real-time estimate for Q1 2016 NGDP is 3.7%. That isn’t recession territory.

17. February 2016 at 07:11

Scott,

This morning economic data came out showing PPI excluding food and energy up 0.4% v. a forecast of 0.1%. This probably means that Yellen & FOMC will be more prone to lift rates in March despite all of the other signs of lower GDP expectations.

I have heard two economic commentators on Bloomberg radio in the last week comment that market signals should be discounted or even ignored when trying to determine the trajectory of the economy. They argued that only macroeconomic factors should be observed. This belief contradicts your guidance from Mishkin and all market monetarists. If Yellen and the FOMC are in this camp, and I’m starting to believe they are, then this also raises the likelihood of a March rate increase.

I think a March increase would be even more damaging to the economy and Fed credibility.

Lastly, is a policy of raising the short term interest rate AND lowering IOR to 0% a way of meeting policy goals for both market monetarists and the Neo-Fisherians? I read all of your posts on the Neo-Fisherian topic and your post arguing that higher rates are expansionary (I’ve been too busy to post much the last few months). Lowering the IOR from .5% to 0 would certainly be expansionary by getting rid of the opportunity cost of holding cash. I’m trying in my mind to figure out how that policy coupled with an increase to .75% to Fed Funds would affect the economy in practice and what the initial market reaction would be.

17. February 2016 at 08:24

You know, I think Anthony’s idea about lowering IOR and raising FFR may be more interesting than it seems at first. I mean, my first thought is that it would just empty the balance sheet, because banks would simply exchange reserves for T-Bills, and the Fed would be selling them T-Bills in order to try to keep the target yield up. Eventually, I suppose, the banks would get rid of all their reserves, and the net result of keeping FFR at .75% would be a tightening.

But, the Fed doesn’t have any T-Bills to sell them. They only have notes and bonds. I don’t think the Fed has any direct mechanism available to push up the Fed Funds Rate. So, the banks would exchange reserves for T-Bills in the private market. That cash would need to go somewhere. The Fed would be selling T-bonds, which would be an imperfect substitute for that cash. I’m not sure where the cash would go or what the ramifications would be.

17. February 2016 at 08:58

A, Yes, I don’t quite understand how NGDP is information destroying. I see it as a useful indicator of the value of money. Of course there are other (supply-side) things going on, but NGDP is an excellent indicator of demand shocks.

Ray, The fact that NGDP collapsed does not prove that it caused a collapse in RGDP, I agree with that claim. But of course there is a mountain of evidence that NGDP causes RGDP, which you choose to ignore. Bernanke’s written entire books explaining how tight money caused the Great Depression.

Thanks Ben.

jknarr, They are correlated, but so are lots of other things. An NGDP futures market would be best.

Talldave, You said:

“I was disappointed the NGDP futures market didn’t catch on”

The experiment went as well as I expected, I don’t think it’s accurate to say it didn’t “catch on”. Only $5000 was at stake—suppose it had been $5 million? What would trading have looked like?

You said:

“I noticed you didn’t stake out a position on the current stance of monetary policy, which I think is a fair request on Tyler’s part.”

It’s too tight, I’ve said that a number of times in recent posts.

You said:

“I believe GDP is currently forecast at around 2.5% and inflation at about 1.75%, so monetary is too tight by about ~.7% of NGDP (1.025*1.0175-1.05).”

I think you are too optimistic, I’d say 3% NGDP growth is more reasonable, or even 2.5%.

Thanks Gordon. And yes, Bernanke underestimates the impact of changes in the quantity of base money.

Thanks Saturos.

Anthony and Kevin, If you are going to lower IOR to zero, how do you propose raising the fed funds rate? Remember, if you do so by reducing the monetary base, that’s contractionary.

17. February 2016 at 09:20

Sumner: “Ray, The fact that NGDP collapsed does not prove that it caused a collapse in RGDP, I agree with that claim. But of course there is a mountain of evidence that NGDP causes RGDP, which you choose to ignore. Bernanke’s written entire books explaining how tight money caused the Great Depression.”

But if NGDP collapse does not prove a collapse in RGDP (during the Great Recession, presumably, since past tense is used by Sumner) how can we have a “mountain of evidence” that NGDP causes RGDP? The Great Recession is a huge boulder in your ‘mountain’ A mountain is comprised of a bunch of rocks, case by case. If you can’t prove the Great Recession collapse in NGDP affected RGDP (which should be a slam dunk), then how are you going to get your “mountain”?

Seriously, is Sumner conceding that the Great Recession was indeed a ‘structural’ recession as T. Cowen claims, in that a collapse in NGDP just happened to coincide with the fact a bunch of baby boomers decided to retire shortly after Lehman collapsed, and a bunch of 20-55 year olds decided not to work so hard since then? Wow. So Sumner is conceding the strongest case that the Great Recession was ‘lack of AD’ induced, and real GDP is affected by nominal GDP? Oh-Kay…kooky.

17. February 2016 at 09:24

That’s partly what I’m saying. I don’t think the Fed has any direct mechanism to push FFR up with other than ior. They don’t have any bills to sell.

17. February 2016 at 09:26

What happens in a context where the liquidity effect of a tightening policy is to steepen the yield curve?

17. February 2016 at 09:52

NGDP does not destroy information. Cowen cannot presume that RGDP / IGDP is de facto lower information. Aggregation can add value, because it uncovers correlated systemic effects.

Besides, we all like in a nominal world. RGDP is a tool, not a reification.

The biggest nominalworld hurdle IMHO is debt. Debt deflation can have RGDP consequences. In short, because of debt intermediation with the future, NGDP and RGDP converge to unity at extremes. This suggests to me the preeminence of NGDP, and hence the importance of NGDPLT.

17. February 2016 at 10:19

[…] is Scott’s lengthy response, do read the whole […]

17. February 2016 at 10:34

I just don’t see how Tyler can keep talking about if we have a recession it is caused by increased perception of risk. Whether or not monetary policy is “tight” perhaps depends on your point of view, but it is certainly tighter than it was, that was the whole point of the Fed raising rates – they did it to tighten monetary policy. So the Fed just tightened monetary policy and low and behold inflation estimates fall and the markets go into a tail spin. I know correlation doesn’t equal correlation but come on.

17. February 2016 at 12:49

Ray,

It is astounding how arrogant you are for someone who admits they are only IQ 120 and can only support their 3rd world chicken farming lifestyle by mooching off of sort-of rich parents. Then you have the gall to accuse humble academics like Sumner of arrogance.

All he said is that the mere fact that NGDP collapsed does not prove that it caused RGDP to collapse. You have to have some other information also (which we do). He has said many times that tight money caused the great recession so it’s absurd and idiotic to claim otherwise.

17. February 2016 at 14:25

Noah Smith: “Free Trade With China Wasn’t Such a Great Idea for the U.S.”

http://www.bloombergview.com/articles/2016-01-26/free-trade-with-china-wasn-t-such-a-great-idea

17. February 2016 at 15:38

If it’s a one off thing, as Noah guesses, isn’t it more likely that the domestic issues of the last 15 years have more to do with it than China? What’s more likely – that China is somehow different than other trading partners, or that dislocations hurt more when they come in the middle of a depression?

17. February 2016 at 18:25

@Cliff- only (?!) 120 IQ? are you kidding me? That’s high, I’m old, I once tested 140 in a more informal test, and this test was a UK test so I missed a bunch of UK specific questions. What is your IQ, idiot? lol

As for your fix of Sumner’s answer, think it through (IQ matters): (you) “All he said is that the mere fact that NGDP collapsed does not prove that it caused RGDP to collapse. You have to have some other information also (which we do).” So, NGDP collapsing is not necessarily the cause of RGDP to collapse, OK. You must have “other information” to confirm NGDP was the cause. OK. So the “other information” is what Sumner’s NGDPLT should be targeting, not NGDP! And what is this ‘other information’? You cannot, as the Crusher nim pottymouth says in another thread, use the occult ‘Wickesian’ (sic) natural rate, since that’s not observable. Nor can you selectively pick and choose a plethora of variables whenever you want to, and say “this time the collapse of RGDP due to NGDP is due to causes ‘XYZ’, the last time it was due to ‘ABC’, and when NGDP collapse did not affect RGDP (such as periods of beneficial deflation) it was due to ‘123’”, as that’s ex post fallacious reasoning and unscientific. Ball back in your court Einstein.

17. February 2016 at 18:51

Ray, I do not believe for a second your IQ is higher than in the 120s, due to a still-growing pile of evidence (including the very comment I’m replying to). I think Sumner’s stretches into the 140s, though I can’t be certain. I’m confident Scott the psychiatrist’s does.

17. February 2016 at 22:07

Ray, you’re a moron, who doesn’t understand what words mean. Let me help you try to concentrate on your latest fallacy:

Cliff said: “the mere fact that NGDP collapsed does not prove that it caused RGDP to collapse”

You attempted to rewrite this in your own words, and you said: “So, NGDP collapsing is not necessarily the cause of RGDP to collapse, OK.”

Sorry, no. Those two sentences mean very different things. You have failed to understand what Cliff’s sentence meant, and your attempted “equivalent” rewriting has exposed your confusion for all to see.

Before you continue to criticize everyone here, you might want to try hiring a tutor to help you with basic reading comprehension. A good high school student would probably be sufficiently qualified.

18. February 2016 at 02:33

“That is we lack a NGDP futures market. And that is indeed a big flaw.”

“A. It’s simple! You just declare an NGDP path target, set up a prediction market, tell an intern to do whatever the prediction market says, and then go on vacation for the rest of your life as a central bank!

Q. This is madness!

A. Madness? THIS… IS… MARKET MONETARISM!

LikeShare”

https://www.facebook.com/groups/674486385982694/permalink/896559330442064/#

18. February 2016 at 07:28

Ray, Your reading comprehension hits new lows every day.

Kevin, You said:

“I don’t think the Fed has any direct mechanism to push FFR up with other than ior. They don’t have any bills to sell.”

I don’t understand, they have lots of bonds to sell.

Travis, Donald Trump could have written that.

18. February 2016 at 08:00

Scott,

Re: increasing FFR and lowering IOR, this would decrease the base but, hopefully, increase velocity by more ultimately having an expansionary effect. What I don’t know is the relative effects of changes in the base versus changes in velocity or rather changes in IOR are more or less effective than changes in FFR.

As to how the Fed would increase the FFR I think it has substantial assets to sell to achieve that.

18. February 2016 at 08:15

Scott, they are going to sell 10 year bonds in order to manipulate the overnight lending market? How would that work? If the Fed Funds Rate falls to .25% and they are targeting .75%, how do they bridge that gap by selling 10 year bonds? Those securities don’t have very much to do with banks borrowing for a few days.

18. February 2016 at 09:00

Scott — OK, interesting, so you feel monetary policy is too tight because you believe inflation/RGDP in 2016 are on the low end of current estimates. That seems reasonable, but I wonder if Tyler is working from different assumptions.

18. February 2016 at 09:43

Kevin:

“If the Fed Funds Rate falls to .25% and they are targeting .75%, how do they bridge that gap by selling 10 year bonds? Those securities don’t have very much to do with banks borrowing for a few days.”

That’s a good point. Maybe the expectation of a lower base causes rates to creep up even at the short end of the curve? Or maybe the Fed sells long bonds, those yields increase due to price drops from increasing supply and that leads to the short part of the curve to increase too as investors borrow short term to invest in the now higher yielding bonds? Or some combination of the two?

Maybe.

18. February 2016 at 09:55

Anthony, Selling assets in contractionary.

Kevin, It makes no difference what they sell, the Fed targets the interest rate by changing the quantity of base money. They could target rates by selling copper, or wheat. Under the gold standard they sold gold. It’s all about the Fed’s liabilities, the assets hardly matter.

Talldave, It makes no difference what I think or what Tyler things. Money is too tight if the market expects sub-target growth in NGDP.

18. February 2016 at 10:15

Scott, I agree. But that’s because you are thinking of MP in terms of the monetary base. That is the right way to think about it. But the Fed thinks about it in terms of interest rates. I think if they were selling bonds instead of bills, they might have to shrink the base a lot more to get the short term rate to move. The liquidity effect would be taking place in long duration bond markets, not short duration markets.

The effects of rate targets are interesting here. Is there any research on this? Normally, the idea is that by selling bonds the Fed temporarily pushes interest rates up because of market inefficiencies. Right? But with IOR, it seems like the process is more passive. They are setting the price and the market comes to them. Do we understand how the dynamics change if the Fed is still defining the process with rate targets?

18. February 2016 at 10:33

Scott,

“Anthony, Selling assets in contractionary.”

Yes but a higher FFR is expansionary and so is lower IOR. Net net I don’t know if the combination is contractionary or expansionary.

18. February 2016 at 11:29

@Kevin Erdmann: “Normally, the idea is that by selling bonds the Fed temporarily pushes interest rates up because of market inefficiencies.”

I don’t think so. That’s not the monetary policy transmission mechanism. The #1 change comes through communication and expectations. The #2 change comes through consequences from the change in the money supply. Your proposed “market inefficiencies” transmission mechanism is trivial compared to those two.

18. February 2016 at 13:38

Don, I agree with you. In fact, it might be the case that the only way the Fed would be able to move short term rates to .75% with no IOR would be to engage in large scale bond purchases enough to create very high inflation expectations. I doubt there is any way to get a rising FFR without IOR with any sort of monetary tightening, whether through expectations or actual trades.

18. February 2016 at 19:50

Kevin, I am almost certain that they see the liquidity effect as resulting from changes in the base, not the type of asset they sell.

Anthony, It’s contractionary in net terms.

19. February 2016 at 06:13

Kevin – The FF rate is the price for overnight borrowing/lending of bank reserves. The supply of bank reserves is inelastic and is determined by the Fed through open market operations. Prior to QE, the Fed could set the supply of reserves at a level such that supply and demand for bank reserves clear around the FF target rate. Typically the amount of reserves demanded by banks (required reserves) is around $100B or so.

But the Fed has added another $3T in bank reserves through bond buying operations (“QE”). Since the supply of reserves is now far in excess of demand, the FF rate will fall until it hits (actually trades below by about 10-15 bps) the floor set by the IOR, be it zero or 0.50% or whatever.

To visualize this, imagine a reserve demand curve that interects a price (i.e. FF rate) at around quantity $150B, a vertical supply curve at around $3T, and a price floor at IOR=0.50%.

So at the moment the only way to raise the FF rate is by increasing the floor set by the IOR. Either that or completely unwind the QE by selling $3T in bonds and shifting the supply of reserves far to the left.

19. February 2016 at 12:17

Scott,

Apologies if this has been asked before, but if there were

an NGDP futures contract, would you not have the same issue

you have elsewhere, namely backing out the risk premium in order to actually infer an ‘expected’ NGDP. Obviously there would be a pretty big bid for low NGDP outcome payoffs just due to the negative correlation with other risk assets. This would bid the contract down well below ‘expected’ NGDP. But how much ? Who knows — every model gives a different answer, just like interest rate term premia papers do now.

(In fact there is a paper out now, which I have not read carefully,from some Atlanta Fed economists which attribute most of the very low level of 5y5y breakevens to risk premia effects. A bit of a stretch it seems to me but shows the range of risk premia that models can come up with)

Thank you

19. February 2016 at 19:11

Andy, Good question. You said:

“Obviously there would be a pretty big bid for low NGDP outcome payoffs just due to the negative correlation with other risk assets. ”

Actually, I don’t think this is true, because there currently is no NGDP futures market. If there actually were interest in hedging against NGDP risk, someone would have created such a market.

Second, comparisons with TIPS spreads are misleading, because a lot of that reflects the different liquidity premium on TIPS vs. regular T-bonds. This is a single asset.

Third, research on commodity futures suggests that any risk premium is likely to be small, probably not of macroeconomic signficance.

Fourth, Only the time varying risk premium matters in the long run.

Nonetheless, the Fed should move slowly here, first setting up and running an NGDP market for a while before letting it influence policy directly.

20. February 2016 at 03:46

Scott

Thank you. In my first point, I meant that natural interest in the “offer side”, i.e. getting paid when NGDP comes in below the contracted level would dwarf interest in the bid side. Someone who could sell this contract at ‘expected NGDP’ has almost certainly just lowered his overall portfolio risk at zero expected cost, much better than equity puts, low strike inflation options, low strike rate options, all of which are generally seen to trade ‘rich’ to expected value. So I don’t think it would trade anywhere near there.

The problem (and perhaps this is why attempts at these contracts haven’t taken off) is enticing people onto the bid side…who wants to do that unless you’re getting a massive expected value advantage ? In any stress event eg 2008-9 you get blown out of the water.

I sort of agree with your fourth point, if the time variation in the risk premium were small , and it was agreed what it was, one could simply add it back and infer the ‘expected’ NGDP. But doesn’t all of Cochrane et al’s research show that there is huge time variation in risk premia?

I think your overall framework is extremely powerful, and doesn’t necessarily all sink or swim depending according to whether we can read off ‘expected 2017 NGDP’ from a futures contract…the notion of expected 2017 NGDP does exist, we might just have to use econometric techniques, or surveys etc to infer it, and its changes as policy changes and shocks arrive…but I suppose that slightly weakens the ‘market’ component in the name.

In fact if I could ask, what would be your favourite method to infer market expected 2017 NGDP using tradeable instruments?

20. February 2016 at 06:35

David:

“The problem (and perhaps this is why attempts at these contracts haven’t taken off) is enticing people onto the bid side…who wants to do that unless you’re getting a massive expected value advantage ? In any stress event eg 2008-9 you get blown out of the water.”

I don’t follow this at all. If there was hedging interest the market would have been created. There is always a market price where bids equal asks. I would be happy to trade either side of the market, and no, 2008-09 would not have blown me out of the water. I would never devote more than 2% of my wealth to this market.

If the price were pegged at 4%, do you seriously think the market expectation would ever exceed 5%, or fall short of 3%?

In any case, even if you were right, my current proposal (based on a Bill Woolsey suggestion) is to have the Fed be free to ignore the market when setting policy, but always stand willing to take bets to keep the price drifting outside the 3% to 5% range. That policy would not be susceptable to any of your criticisms.

20. February 2016 at 07:12

Scott

My point is indeed that there would be some hedging interest,

but that would be relatively strongly concentrated on the ‘offer

side’ of the contract. Those with equity positions, real estate,

in fact most risk assets, would lower their risk at zero expected cost IF THE CONTRACT TRADED AT EXPECTED NGDP.

So therefore it wouldn’t, in order to bring the other side in. So the contract would trade somewhat under expected NGDP. I don’t think this point is very controversial at all, most of asset pricing is about risk premia, and in something as absolutely central to the economy as NGDP (as you yourself have argued so convincingly! ) it would be significant. And NGDP risk would certainly come under the category of an undiversifiable risk.

You might say, (as you did in your first reply), I don’t care we can simply adjust for that , back out this effect etc. and that is fine, agreed. But then you are in the realm of dueling models for risk premia, which is a major industry in academic finance, particularly in rates and equities. And those are not 3rd decimal place arguments the variations are massive!

So ‘reading off’ the markets expectation of ‘expected NGDP’ will not be trivial, even if a free market futures contract started trading in high volumes.

I wasn’t talking at all about the case where the government pegs the contract by permanently bidding it. That would be interesting, according to my points above if they did so at the true ‘expected NGDP’ they would get filled in in very very big size. This in turn would expand the risk taking capacity of the economy, since it is a government risk subsidy, as it would be if the government was an off market bid for equity puts, or bank credit paper, or CLO equity. So I think on this point we are back to agreeing.

Thank you for your responses.

Andy Morton

20. February 2016 at 15:53

Sorry for getting your name mixed up. We’ll have to agree to disagree on the hedging issue, I say there is no interest, and if there were the market would exist. You have not offered any persuasive arguments otherwise, and saying someone would have to take the other side is not an argument.

In any case, there are versions of NGDP futures targeting where risk premia make no difference, such as Woolsey’s index futures convertibility approach, which I now lean towards, partly to avoid the (perceived) problems you mention.

21. February 2016 at 05:09

Fair enough, but to be clear what we are disagreeing on, my main point is the risk premium one, namely that if a 2017 NGDP contract did exist and it closed Friday at 3.7, I and I think many people in markets would conclude that roughly 4.2 is the ‘expected NGDP’ ie that there is 0.5% of risk premium. I’m not sure what you are saying on this but it sounds like you would just read off the 3.7 as ‘expected NGDP’.

I think this point, and the fact that most people in finance believe in risk premia, is quite important to your own agenda — in a thought experiment of rerun of 2008 but where NGDP futures existed, in the fall of 2008 the 2009 future would be crashing, and you would be saying “LOOK LOOK monetary policy is too tight the NGDP future is crashing it’s down to 1.5 !!!”, the Fed would just say “relax Scott it means nothing it’s just widening risk premia, we are studying the issue carefully”. This is pretty much what they are doing now with 5y5y breakevens about 100bp below their target, once you adjust for PCE/CPI.

As to why these contracts don’t exist, that’s a much more minor point, and hard to debate. The Chicago Mercantile Exchange people say that only 1 out of 10 contracts they start (even after lots of study on their part) succeed.

Cheers

21. February 2016 at 07:00

Andy, I agree that when the NGDP contracts shows 4.2% the actual expectation might be 3.7%, and I’ve said that’s possible in my papers on the subject. But I’ve also claimed that the finance literature suggests that any risk premium is unlikely to be of macroeconomic significance. Certainly 0.5% is not a problem.

Also recall that under a futures targeting regime periods like 2008 never happen, i.e. the price never moves sharply.

And again, onl;y time varying risk premia matter, so if there is usually hedging against declines, that bias doesn’t matter.

21. June 2016 at 13:27

[…] has been noted already by Market Monetarists and others that George Osborne and his UK Treasury team are concerned about the low level of […]