Lars Christensen on the euro disaster

Lars has a great new post on the euro disaster:

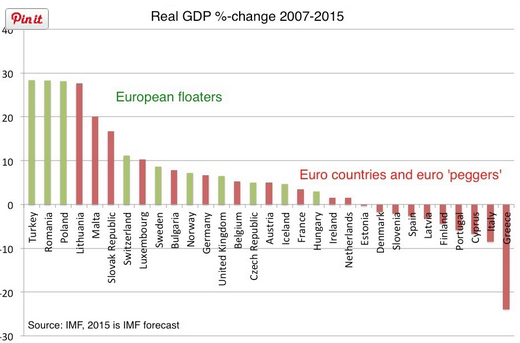

The graph below shows the growth performance for these two groups of European countries in the period from 2007 (the year prior to the crisis hit) to 2015.

The difference is striking – among the 21 euro countries (including the two euro peggers) nearly half (10) of the countries today have lower real GDP levels than in 2007, while all of the floaters today have higher real GDP levels than in 2007.

Even Iceland, which had a major banking collapse in 2008 and the always politically dysfunctionally and highly indebted Hungary (both with floating exchange rates) have outgrown the majority of euro countries (and euro peggers).

In fact these two countries – the two slowest growing floaters – have outgrown the Netherlands, Denmark and Finland – countries which are always seen as examples of reform-oriented countries with über prudent policies and strong external balances and healthy public finances.

When some of the best managed countries in the eurozone can’t even outgrow Iceland, you know that something is very, very wrong.

Tags:

15. July 2015 at 08:06

Can you produce the same graph for the full period (2001-2015). Which is the more cutest period for judging the effects of the Euro

15. July 2015 at 08:38

The recession in Europe started in late 2008, even 2009 for some countries.

I’m surprised to see such a huge difference between Lithuania and Latvia – Latvia is of course a star in austerian cicles.

15. July 2015 at 08:41

Iceland is interesting to watch as they were the one country that chose to let their banks fail.

It seems to me that the cost of keeping a dying bank alive is the cost of slower long-term growth.

15. July 2015 at 08:41

I think it would be even more interesting to remove core Eurozone countries from the set – as the Bundesbank actually runs the Euro. If you look at their inflation performance before the crisis they also sucked – its not as if the ECB would care for inflation in some medditarenean country.

15. July 2015 at 09:01

Doug M, In Ireland and Cyprus most of the bank activity was outside the country, so they could let banks fail.

When your banks power the economy, letting them fail means strangling liquidity out of your own economy, which is very costly

15. July 2015 at 09:11

Yep. This is why I keep saying the fatal flaw in the euro is the inability to do monetary offset that comes from delinking monetary and fiscal sovereignty.

15. July 2015 at 09:37

@TallDave, I don’t think that’s right. Nobody cares about Ecuador, El Salvador, Panama, Zimbabwe, Detroit, or Puerto Rico being on the dollar.

15. July 2015 at 09:48

Could free banking be worse?

15. July 2015 at 10:12

Jazi Zilber,

As I remember, Ireland did bail its banks out.

Cyprus had a somewhat curious “bail in.”

In 2007, Iceland was the most banking-centric of them all. But, as you point out, international banking, such that when they failed it was largely non-Icelanders who were left out in the cold.

15. July 2015 at 10:20

E. Harding — They certainly care. For an emerging economy dollarization may be preferable due to regime uncertainty and CB trust issues, but no developed economy should or does dollarize. Citizens of Detroit share a monetary and fiscal sovereign.

15. July 2015 at 10:25

I keep saying the fatal flaw in the euro is the inability to do monetary offset that comes from delinking monetary…

That’s one, but hardly the only one. How about this one that Cochrane has pointed out (my emphasis)…

http://johnhcochrane.blogspot.co.nz/2015/07/greece-again.html

Greece’s sovereign debt suddenly became … risk free! and injected by EU *regulation* throughout the entire banking system of the monetary union as if it really was. As was the debt of every other country that had an inferior rating before joining the euro. Just *as if* they really were risk free. Well, the real world has a way of turning on such “as ifs”.

Check the chart of what happened to country borrowing rate spreads upon the adoption of the euro…

http://seekingalpha.com/article/3310315-the-parody-of-errors-that-led-to-grexit

How was it not plainly visible at the time that that “convergence” to the benefit of so many then was setting up the disasters that started a few years later? When the necessary subsequent “de-convergence” started, with a vengeance.

Of course the Greek politicians enjoyed a huge debt-fueled boom for short-term gain when offered a deal like that. What politicians wouldn’t?

Risk-free debt-by-regulation was a great deal for *all* the sovereigns, in the short run….

Then, when the longer run arrived, add “no offset” monetary policy reminiscent of Great Depression days on top of that.

As to Greece, it committed suicide, no doubt — nobody forced its politicians to issue all that debt they knew they couldn’t carry to enjoy all the short-term fruits of a corrupt bogus boom. There’s a reason why they are so much worse off than everybody else in the same euro system.

OTOH, it surely was an “assisted suicide”, very amply incentivized, encouraged and aided by the EU.

15. July 2015 at 10:27

Just another example of someone comparing apples to oranges.

Did Mr. Christensen look at things like interest rates, Current Account Deficits/Surplusses, Debt to GDP ratios, etc. ?

E.g Turkey & Poland have borrowed LARGE amounts of money from foreign lenders. I personally expect those 2 countries to be the first to go down the deflationary drain in the coming week, months.

15. July 2015 at 10:51

In my opinion, treating sovereign debt as risk free was not quite the problem: it was allowing sovereign debt of different countries to act as perfect substitutes.

The risk of sovereign debt was not so much the problem as treating banks differently. Bailing out Greek banks is a problem because it means taking a loss on Greek sovereign debt.

Instead, consider if European banks could obtain direct funding from the ECB, but in exchange they were required to hold a synthetic “Eurobond” as collateral, consisting of debt from each Euro state weighted by population or GDP.

In this circumstance, the capital of all banks would be more or less equivalent. Bailing out a Greek bank would be no more a subsidy to the Greek state than would a bailout of a French or German bank. A sovereign crisis would be less likely to turn into a liquidity crisis, and Greece could default like Detroit.

In the meantime, fiscal austerity on the part of growing states would be rewarded. Bank equity requirements would impose a built-in inelastic demand for the national debt of Germany and such, which means that the state could profit from low or negative interest rates.

15. July 2015 at 10:54

Thanks Scott…more to come.

15. July 2015 at 11:55

Hidden variable: population / labor force growth?

Also, why 2007 as the start year? Why not post-crisis?

15. July 2015 at 12:35

Off topic

Prof. Sumner, this bloomberg article comments on rent costs in the US, I don’t know if it is interesting to relate this to monetary policy or other views you have on the housing market …

http://www.bloomberg.com/news/articles/2015-07-15/the-exact-moment-big-cities-got-too-expensive-for-millennials

15. July 2015 at 12:36

I would add that

– Lithuania adopted the Euro in 2015

– Slovakia adopted the Euro in 2009

Thus, some Euro members joined after the trauma of the Great Recession, or when expectations had already been reset.

The Euro vs non-Euro comparison serves as a principal bit of evidence for the importance of monetary policy in real GDP outcomes.

15. July 2015 at 12:41

To me, this doesn’t seem so much evidence that the concept of the Euro itself is wrong (though I think it probably is), but that ECB policy since 2007 has been far too tight. If the problem foreseen by Euro skeptics — asymmetric growth rates — were the main issue, you’d have some good performers and some bad ones. Instead, even Germany, with 6% growth in 9 years, has done poorly.

15. July 2015 at 12:43

Having a free floating currency gives a country much more policy flexibility – period. It is not foolproof, but there is inherent flexibility. Furthermore, it acts as a check and balance (canary in the coal mine) to sometimes force reform- again not foolproof. But the Euro setup was clearly going to be a problem, predicted by many. Problem is what is the bigger problem – inflation, unemployment and what is that balance.

15. July 2015 at 12:49

Here is a Bloomberg piece listing economists and their euro predictions/ opinion excerpts:

Nine People Who Saw the Greek Crisis Coming Years Before Everyone Else Did

http://www.bloomberg.com/news/articles/2015-07-15/nine-people-who-saw-the-greek-crisis-coming-years-before-everyone-else-did

15. July 2015 at 13:08

@Floccina- Your question does not make sense, so I think the most appropriate response is to unask the question.

Free banking is a broad money regime. It is not a base money regime.

If what you mean is “would a Gold Standard be worse,” that’s an entirely different question, and depends in part on A) how universal adoption of gold convertibility is and B) whether by “Gold Standard” you mean an actual Gold Standard, or a Gold Exchange Standard. It also depends on the banking regime, as well.

15. July 2015 at 13:15

Steven Kopits,

At the risk of undermining your point, I think it needs to be acknowledged that Slovakia pegged to the euro in May 2008, and Lithuania pegged to the euro in February 2002. Both countries experienced the full brunt of the recession thanks to their pegs, with Lithuania experiencing one of the largest downturns globally (along with Estonia, Ireland and Latvia).

This stands in sharp contrast to their immediate neighbor Poland, which is the only EU member that did not experience a recession in 2008-09. Among the EU members with flexible exchange rates, Poland also depreciated its currency the most (approximately 30%) with respect to the euro between July 2008 and February 2009.

I submit that the principal reason why Lithuania and Slovakia have done so well among the euro members since 2007 is their growth friendly tax policies. (The subject of my recently completed dissertation is in fact tax structure and growth in the EU.) In other words good supply side policies have allowed them to perform well despite dreadful Euro Area monetary policy. (And being proximate neighbors to Poland hasn’t hurt them either.)

15. July 2015 at 15:21

Suck them in with cheap debt, and then when you’ve got them hooked, chop off the head of socialism and big government. What’s not to like about this. No wonder PK and the NYT are wringing their hands.

(Think I might be saying the same thing as Morgan).

15. July 2015 at 15:45

http://krugman.blogs.nytimes.com/2015/07/12/killing-the-european-project/?module=BlogPost-Title&version=Blog%20Main&contentCollection=Opinion&action=Click&pgtype=Blogs®ion=Body

What do you think of this blogpost by Krugman, Scott?

15. July 2015 at 16:06

The best reason why a statist monopoly currency is a bad idea in Europe, is the same best reason why it is a bad idea for the US, indeed any sized geographical territory.

Every time I read Sumner trashing the Euro and praising the dollar, with all this gobbledygook about optimal currency areas, fiscal and monetary consolidation, blah blah blah blah, I am reminded that his entire economic worldview is predicated on national socialism.

15. July 2015 at 16:09

A lunatic obsession with inflation is not a monetary policy. And yes every sovereign nation should have its own central bank.

15. July 2015 at 20:51

While I agree that the ECB have been far too tight it would be interesting to do this chart weighted for (population*2007_GDP). As Germany and France are in the positive growth column and they were the most populous and richest countries in the Euro, there is an argument that the ECB is simply doing its job to avoid over-inflating the central economies. Again the Detroit argument might apply, no-one expects the Fed to run monetary policy based on the economy of Detroit.

16. July 2015 at 01:14

Wouldn’t it just be the reflection of the week Euro to USD effect? (I assume the graph is based on USD growth, or even if it is PPP the problem still prevail)

16. July 2015 at 03:12

Central banking is lunatic.

16. July 2015 at 04:35

The Worgl experiment.

http://www.lietaer.com/2010/03/the-worgl-experiment/

16. July 2015 at 04:49

@Mark S.,

Great comment, as usual. Another country that comes to mind as implementing supply slide reforms which allowed it to perform ok despite dreadful Euro Area monetary policy is Germany. Some one should tell them that even THEY could be doing better.

16. July 2015 at 05:36

Off topic, but here is a post outline for you:

1. Jeb Bush & Hillary Clinton both want to increase labour force participation [http://www.bloombergview.com/articles/2015-07-14/hillary-and-jeb-agree-but-are-both-mostly-wrong].

2. They should just end the marriage penalty or go full-Sweden and tax couples as individuals. Good for feminists (more women will be finantially independent), good for conservatives, good for LFPR. So unambiguously positive that [given it’s uncontroversial], nobody is pushing it.

3. Doesn’t this (now old[ish]) NYT piece on how scandinavia has high LFPR [http://www.nytimes.com/2014/12/18/upshot/nordic-nations-show-that-big-safety-net-can-allow-for-leap-in-employment-rate-.html?abt=0002&abg=1] despite high taxes neglect to mention that couples are taxed separately there, massively decreasing the marginal rate for the second earner, whilst increaing the mean rate? So, a woman married to a high-ish choosing to go back to work after a maternity break might well face higher taxes in the US than in Scandinavia.

16. July 2015 at 06:07

– Denmark has the highest mortgage debt to GDP ratio in the European Union. And this high debtload is burdening the danish economy.

– Eastern Europe & Turkey are basket cases. These countries have (high) Current Account Deficit and debts denominated in foreign currencies.

Especially Turkey is heading for deep, deep trouble.

Now I understand why one Scott Sumner posted this article from Christensen’s blog. Both like the (extremely flawed) idea of NGDP targeting by central banks.

16. July 2015 at 06:24

To be honest Scott, I do not understand why you endorse this article. I remember that on numerous occasions you criticized other economists talking about RGDP growth as opposed to NGDP or inflation when talking about monetary policy.

Now we have some RGDP comparisons of countries ranging from Turkey through Slovakia to Norway and Switzerland – and throwing claims that that if well managed countries like Denmark (which has own currency BTW and voluntarily pegs it to EURo) cannot outgrow Iceland in 8 years it is a failure of Euro. Is it? Denmark has unemployment of 6.2% which is way better than some of the leaders in the table like Poland with 7,8 or Romania with 7,1. There may be some slack there in Denmark maybe around 2% but beyond that what exactly does Lars expect from monetary policy?

I don’t like this approach – maybe now it pays off for Market Monetarists. But imagine we have 2025 and some countries that adopted MM policies will have recessions. Would you deem any research comparing growth of RGDP among vastly different countries albeit with different monetary policies as sufficient? This can quickly turn against you.

16. July 2015 at 06:38

Steven Koptis: “I would add that

– Lithuania adopted the Euro in 2015

– Slovakia adopted the Euro in 2009”

And as you maybe know, both of those countries had to keep what is basically a currency peg (or very narrow volatility) as part of Maastricht criteria to even be accepted into Eurozone. Lithuania went even further than Slovakia and pegged litas to Euro in 2002 – and and kept it for 13 years until they were admitted.

And since both these countries had very impressive RGDP growth I assume it had to be due to excellent monetary policy, right? (sarcasm)

16. July 2015 at 06:44

– The reason why Greece, Italy, Spain & Portugal didn’t see “too much growth” after 2009 is that in those countries interest rates rose during 2010 & 2011.

– The reason that Turkey, Poland & Lithuania grew much more was that investors were reaching for higher yields that were no longer available in other W.-European countries. But one day that meonyflow WILL reverse and then Eastern Europe + Turkey WILL be in trouble again (like in 2001, 2008 & 2009).

16. July 2015 at 07:04

Mark makes a critical point above: 2008-9 was when monetary policy had the largest impact — as MMs have been pointing out for a long time, that’s the time when NGDPLT looks very different than IT.

Poland is a great example of how maintaining smoother NGDP maximizes RGDP. Maybe we should start building some lists of empirical evidence like this and also making some concrete predictions…

16. July 2015 at 07:53

Jazi, Maybe Lars will do it.

Jim, Oddly, the markets also treated it as risk free.

DF, It makes more sense to compare to before the crisis. Those with deeper drops will generally have bigger rebounds.

dbeach, I’d say that is a problem with the euro, but one most of its critics didn’t anticipate

Edward, That post seems a bit over the top, I did a post over at Econlog that commented on it.

Chris, You said:

“As Germany and France are in the positive growth column and they were the most populous and richest countries in the Euro, there is an argument that the ECB is simply doing its job to avoid over-inflating the central economies.”

That’s completely wrong. the ECB’s “job” is to set a policy that is appropriate for the entire eurozone—individual economies should play no role in ECB deliberations–they should focus on eurozone data. Focusing on Germany and France would be as stupid as the Fed focusing on Detroit.

Cloud, Why would this be measured in US dollars? That makes no sense.

Luis, Yes, let people freely choose how they will file.

JV, Good point, but in fairness when I criticize others it’s when the NGDP and RGDP figures have different implications. But yes, Lars should provide both, NGDP to show the change in demand, and then RGDP to show that different growth rates in demand had implications for NGDP. In this case I think the results would hold up, you’d see similar patterns both ways.

16. July 2015 at 08:22

Scott: That’s the thing, I do not think the story would look the same if Lars did not use the RGDP metric. Then it would show that for instance that Romania started the recession with around 8% inflation and experienced relatively wild ride (up and down) ending up with deflation as of June 2015! And we are not even talking about Turkey with its double digit inflation throughout the period (albeit slowing down)

Are these really the countries that should exemplify virtues of recession-fighting abilities of monetary policy? And I have to say that I am no expert, I spend literally 5 minutes looking at those data. But I can see it does not paint the same picture as Lars tries to imply. Which is enough for me to not like his blog (Disclaimer: I like most of his blogs, his analysis of Russia for instance is superb.)

16. July 2015 at 08:34

JV, Inflation doesn’t matter. How much NGDP growth has Romania had since 2007, and how much has the eurozone had? That’s the question.

16. July 2015 at 08:59

Here’s Stephen Williamson’s brief comment.

16. July 2015 at 09:55

JV — Romania had 150% inflation as recently as 1998. They’ve been getting it under control since then as their CB gains credibility and regime uncertainty is less of a concern. Looks like they certainly had higher inflation than the euro during the 2008-9 period, so they would have had smoother NGDP growth during a critical period. By 2014 they’ve fallen to 1-2% inflation which is probably appropriate for 3-4% RGDP growth (although recent data is a little sparse).

http://www.tradingeconomics.com/romania/inflation-cpi

Would Romanians have been better off under the euro? Or would they have had lower inflation but also lower RGDP growth and worse employment?

http://www.tradingeconomics.com/euro-area/inflation-cpi

16. July 2015 at 10:29

Scott, O/T: what do you think of Senator Pat Toomey’s comments about the Fed? From the link:

“Republican Sen. Pat Toomey said Thursday it’s “unbelievable” that interest rates remain so low…”

(H/T Mike Sax)

16. July 2015 at 10:44

Bubble Monger,

“…E.g Turkey & Poland have borrowed LARGE amounts of money from foreign lenders…..Eastern Europe & Turkey are basket cases.These countries have (high) Current Account Deficit and debts denominated in foreign currencies…”

According to World Bank statistics, Poland’s gross external debt was 64.4% of GDP in 2014, That was lower than any euro member with the sole exception Lithuania (59.9%). Turkey’s gross external debt was only 49.9% of GDP. For comparison, Germany’s gross external debt was 144.9% of GDP, and several euro members (e.g. Austria, Belgium, France, Portugal etc.) have gross external debts over 200% of GDP. Netherlands’s gross foreign debt is over 300% of GDP.

The only non-euro Eastern or Central European countries with large gross external debts are Bulgaria (176.0%) and Hungary (132.7%). Other than those two countries, none of the non-euro Eastern or Central European countries on Lars’ chart have a gross external debt even as high as Poland’s (low level). Subdividing it into purely foreign currency denominated debt doesn’t really change the picture much because then it’s just a fraction of an already relatively small amount.

As for the current account balance (CAB), it’s true that Turkey’s CAB was 5.7% of GDP in 2014 (according to AMECO). But Poland’s CAB was only 1.4% of GDP. The Czech Republic’s CAB was only 0.9% of GDP, and Romania’s was only 0.5% of GDP. Hungary had a huge surplus equal to 4.4% of GDP.

And just for the record, Central and Eastern European euro members Estonia (0.1%), Lithuania (0.6%), Slovakia (1.9%) and Slovenia (5.3%) all had CAB surpluses. Only Latvia had a deficit (2.9%). And Latvia (120.6%) and Slovenia (106.1%) are the only Eastern or Central European euro members with a gross foreign debt of over 90% of GDP.

So no, generally speaking, Central and Eastern Europe are not burdened with huge amounts of gross foreign debt and unsustainable current account deficits.

16. July 2015 at 11:14

As J.V. Dubois points out, some “floaters” where in fact “peggers” de facto. Also, except for the Club Med basket case countries, the stats for floaters and peggers are about the same, which is what you would expect given that money is neutral. Nothing but data mining.

16. July 2015 at 11:52

Ray Lopez,

“As J.V. Dubois points out, some “floaters” where in fact “peggers” de facto.”

Wrong. J.V. Dubois is pointing out that some of the euro members were not floaters before they joined. You have it backwards (as usual).

16. July 2015 at 13:37

Tom — The right is just terrible at monetary policy sometimes. Maybe even generally.

Was reading today through a series of horrifying posts over the years at Forbes from some guy (forget his name) who went on and on about how Fed policy was so amazingly loose, because just look at the value of dollars in gold!

He stopped posting right when gold started falling again, because of course he did.

16. July 2015 at 13:54

@TallDave, was that guy at Forbes named John Tamny by any chance? Even I can see that guy is quite ignorant regarding what he writes about.

16. July 2015 at 15:01

A similar graph for other times would be more convincing, including choosing the year which makes the floaters best off.

16. July 2015 at 17:44

Tom, But how does he want the Fed to raise rates, with easier money or tighter money?

16. July 2015 at 18:37

@Sadowski who says:

Ray Lopez,

“As J.V. Dubois points out, some “floaters” where in fact “peggers” de facto.”

Wrong. J.V. Dubois is pointing out that some of the euro members were not floaters before they joined. You have it backwards (as usual).

//

at Sadowski:

I guess you don’t see the math: A = B implies B = A, so strip out these countries and you are left with the right-side tail of the curve. As I said, nothing but bogus data mining. This data mining can be summarized as: Greece, Italy, Cyprus, Portugal, Finland (Nokia), Latvia, Spain all had problems with their economy since 2007. Nothing more than that. Denmark was a surprise, but not a big deal since arguably (as another poster said the curve should go back further) Denmark did not drop as much in 2007 as other countries, so less recovery.

OT: Andrew_FL is smart: he understands (unlike Sumner, from another exchange with me last year here) that there’s a difference between a gold standard and a gold exchange standard. With the latter, it’s not much better than a fiat money standard, since ‘sterilization’ occurs. Food for thought: though money is neutral, businesses hate exchange rate risk and might Nixon’s 1972 taking the USA off the gold (exchange) standard of Breton Woods, with fixed exchange rates, have created instability in the form of inflation and lost productivity? Probably a coincidence though, but Mundell is right about the desirability of a ‘world currency’ (which is an attempt to create an artificial gold standard btw). Sumner: please get Simple Machines forum software so we will not bother with you with these sub-threads.

16. July 2015 at 23:56

Scott: “Inflation doesn’t matter. How much NGDP growth has Romania had since 2007, and how much has the eurozone had?”

Funilly enough the topic is covered by none other than Lars in an article entitled “It was monetary policy failure – also in Romania”:

http://marketmonetarist.com/2014/05/06/it-was-monetary-policy-failure-also-in-romania/

If I read the graph right, then Romania had to experience one of the most spectacular NGDP plunges from levels of around 25% to negative teritorry. Then the NGDP get to around 5% growth – a point that most MMs preffer for mature economies – but compared to pre-crisis trend line this is incredible slowdown. Certainly a puzzle for MMs to explain. However the graph in the article ends in 2013. Since then the situation got worse, Romania currently experiences sharp slowdown in both inflation (Romania is in deflation as of June) and RGDP growth is in 1-2% area.

But this is beside the point. My main point is not to discuss Romanian monetary policy. My point is that the comparison as done by Lars hides more than it reveals. He sees Euro as a nail and uses everything as a hammer – like RGDP data. This I think is both wrong and dangerous for further MM cause. This is stuff that cause me cringe while reading Krugman.

17. July 2015 at 00:31

Ray: Mark is right. I reacted to Steven Koptis’s implicit claim that the best Eurozone performers (Lithuania and Slovakia) in terms of RGDP growth were floaters at the time the crisis started – further strenghtening the point Lars made. Which is not true as both these countries kept peg to Euro by the start of the crisis.

17. July 2015 at 07:34

JV, I agree that Lars’s blog post is incomplete, and obviously more research is needed, as they like to say. So you make a fair point.

But I don’t think it’s worthless. These sorts of correlations are always leaving something out. But when you see a strong statistical pattern, then the things being left out need to correlate with the independent variable (monetary regime), in order to invalidate the results. I’m still not convinced they do.

I’d like to see the correlation between Romanian NGDP and RGDP growth. I’ll bet its fairly strong. (Your link shows NGDP and M1, not sure why that matters.) And do understand that like all monetarists, MMs understand that high inflation doesn’t lead to high RGDP growth, prices become much more flexible when inflation rates hit 30% or 40% year. There are diminishing returns from monetary shocks.

What would make me change my mind? If the stronger RGDP growth of non-euro countries was not associated with stronger NGDP growth. But I still believe they are probably correlated.

Have you left a comment on his blog, asking him to do the graph for NGDP?

And Ray is a clown. Best to ignore him, unless you enjoying mocking him like I do.

17. July 2015 at 08:01

Sumner: “And Ray is a clown. Best to ignore him, unless you enjoying mocking him like I do.” – the joke’s on you. Besides the fact that most of your audience wrongly assumes I’m a troll, and thus thinks poorly of you for ‘feeding the troll’, the fact is that you seem to do poorer in replying to me by skirting the issues I raise, and the more astute readers of this blog know this. You’re losing the argument Dr. Sumner. You’re getting your fanny handed to you by a guy who took Econ 101, 102 over 25 years ago, but maintains an amateur interest in economics. To use a chess analogy (and it happens all the time), you’re a grandmaster of economics, but you’re being beaten like a drum by a mere expert player.

17. July 2015 at 10:43

@Ray Lopez: Dunning-Kruger effect, with the money phrase, “inability of the unskilled to recognize their ineptitude“.

We all appreciate you providing a daily concrete example.

17. July 2015 at 11:59

Scott: Some of the things you say about RGDP vs NGDP correlations are quite interesting for me. Just some points:

1) Imagine that there was a country (or some time period like Great Moderation) where NGDP growth is stable exactly how MMs want it. Then by definition RGDP and NGDP growth are not correlated. NGDP is stable and RGDP reacts just to supply shocks. Having a list of 20 countries sorted by their RGDP growth during last 10 or 15 years shows nothing about efficacy of monetary policy.

2) If I am right about 1 then why devise/endorse test that does a thing that MM automatically rules out as a sensible way to gauge monetary policy effectiveness? This is why I say it is dangerous way to go. You can have a person who digs up these arguments in 2025 and says “See, MMs themselves created a test for how monetary policy should affect an economy. Now they fail their own test so we have to abandon their advice”. Ends sometimes really do not justify means.

3) Just as a side note, saying that Monetary Policy can impact medium to long term RGDP growth (I consider 8 – 12 years now according to Lar’s blogpost) is unusual. I happen to support this claim – in a sense for me ineffective monetary policy equates to bad supply side policy. If for instance some country will have monetary policy respond procyclically to AD shocks and lets RGDP fall as a result every time a cycle hits I would expect this country to have worse long term RGDP growth as opposed to the same country with better monetary policy arrangements.

But your claim goes even further. If I understand you correctly you say that higher RGDP growth is correlated with higher NGDP growth. This is much stronger claim – one that is refuted even by looking at countries on the list as there are some with double digit inflation and NGDP growth. I suppose that you yourself see any country running such an easy monetary policy to suffer lower RGDP growth long term (compared to counterfactual where they would have single digit NGDP growth).

So I assume that your stance is more nuanced than that (which is why you probably said more research is needed)

4) And even if everything that was said was correct in a way that ECB srewed up massively and run the worst monetary policy out of 20 countries in the list I still do not see this as a particular problem of Euro itself, but as a problem of incompetent central bank. This line of argument touches my critique of critique of Euro in earlier articles.

In other words, if let’s say in next recession FED has the worst record of recession fighting out of all developed world Central Banks would you call for dismantling the dollar and letting all US states run their own currencies with own monetary policies hoping the average monetary policy of that blob will be better next time?

We can run this game for a long time – calculating NGDP of US counties with 300,000 citizens (which is population of Iceland) and comparing it to cities with around 3 million of citizens (in the ballpark of population of Detroit Metro or Lithuania) and speculate if leaving the currency union would improve the NGDP growth.

I personally don’t agree with it and find this line of arguments flawed from economic standpoint. It is almost unsalvageable – you either say that stable NGDP is all-important for economic structures encompasing few hundreds of thousands of people and go hard with research and finding ways how to create new monetary arrangements that can replicate such a feat or it is just all nonsense. If it is the latter can we then please stop pretending that this whole Euro discussion is a serious technical issue and just openly admit that we are expressing our political views?

17. July 2015 at 19:14

I don’t believe I’ve ever been so embarrassed to be complimented in my life.

17. July 2015 at 19:23

@J.V. Dubois: “Imagine that … NGDP growth is stable exactly how MMs want it. Then by definition RGDP and NGDP growth are not correlated. NGDP is stable and RGDP reacts just to supply shocks.”

If you eliminate AD shocks, then what you have left are AS shocks. OK, seems to make sense.

“Having a list of 20 countries sorted by their RGDP growth during last 10 or 15 years shows nothing about efficacy of monetary policy.”

Not at all, because the point was whether monetary policy that results in unstable NGDP growth, suppresses RGDP growth. If you have currency areas functioning under different monetary policies, you can certain check whether areas with more stable NGDP growth had higher RGDP growth.

“higher RGDP growth is correlated with higher NGDP growth.”

Deflation, or even too-low inflation, suppresses RGDP growth (due to sticky wage resistance to nominal wage cuts). So, when NGDP growth isn’t sufficiently greater than (potential) RGDP growth, you’ll find that increasing NGDP growth will also increase RGDP growth.

However, once NGDP growth is both stable and also sufficient to provide ~2% inflation then greater NGDP growth is not expected to increase RGDP growth. (Instead, you’ll just get greater inflation.)

18. July 2015 at 06:41

Ray, Maybe it’s time to go back to those EC101 textbooks and learn the difference between AD and AS. You might be surprised to know that those picky distinctions are actually kinda important.

JV, Your comment mischaracterizes my views in all sorts of ways. Do recall me ever doing a post that said “Zimbabwe style rapid NGDP growth leads to faster RGDP growth”? If not, why pretend that I have? My views are much more nuanced than you suggest.

In other respects you are just repeating views I’ve already expressed. I’ve said the eurozone failure is both a one-size-fits-all problem, and a problem related to the fact that ECB policy has been way too tight for the eurozone as a whole. So please don’t bring that up as some sort of insight that undermines my claims.

More generally, I’ve constantly suggested I’m a supply and demand sider. It’s people like Krugman who seem to think NGDP explains all, that high unemployment is merely a demand side problem.

And yes, the “thermostat problem” in identification is well understood.

As far as the euro is concerned, the problems it created go far beyond a bad recession, it is undermining the entire European project, leading to an ugly resurgence in nationalism. The worst thing about the Great Depression was not high unemployment, it was nationalism and communism.

BTW, Lars’s data does not imply monetary policy has 8-10 year effects. Have your forgotten the ECB’s tight money policy of 2011-2012? Until 2011 the US and eurozone were doing equally well.

18. July 2015 at 07:21

Excellent post as usual (both this one and Lars’s).

Great comments too from TallDave, Jim Glass and Majromax on the problems of treating Sovereign bonds of member states as risk free by banks.

One possibility is if members could sell a limited amount of bonds backed by future dividends they get from ECB profits, then those could be considered risk free by regulators.

But as I commented on a previous post, I think the best solution would be similar to the one Hamilton implemented in the US. Give every member an equal amount of debt relief financed by Eurobonds – which would be the only asset considered risk free by regulators. They would sell like hotcakes, rivaling US Treasuries around the world almost immediately. The interest rate would likely be lower than every member pays now. Every taxpayer in the Euro area would benefit.

19. July 2015 at 04:46

Negation, How would Germany benefit if Greece borrows using eurobonds and doesn’t repay the debt?

19. July 2015 at 09:23

Scott –

I’m not sure which of my two proposals your question refers to so I’ll answer for both.

If Greece could borrow by selling “a limited amount of bonds backed by future dividends they get from ECB profits” then it would be impossible for them not to repay the debt. Greece’s ECB dividend would simply go toward their debt instead of Greece getting it in cash.

I recognize this may only allow a very small amount of bonds – some multiple of their annual ECB dividend. I’m not aware of how large the ECB dividend to Greece is. In the US, the Fed pays the Treasury about $100 Billion a year.

If you’re talking about the second proposal – it was a partial debt assumption by the federal entity, not a loan. An equal amount of debt assumption by population for Greece, Germany and the rest of the Euro members. Then the Eurobonds could be paid out of future ECB profits, and/or a tiny Euro-area tax, or it could simply be rolled over like we do in the US.