Real GDP, employment, and demand shocks

I’ve argued that one should “never reason from a quantity change.” A fall in RGDP could be due to supply-side factors or demand-side factors. That’s also true of the unemployment rate, but as a practical matter the unemployment rate is usually preferable to RGDP as an indicator of demand shortfalls. If NGDP keeps growing at a steady rate, then wages should also grow at a relatively steady rate. In that case an adverse supply shock might be expected to reduce output but not employment. Workers would earn about the same nominal wage, but a lower real wage (or more precisely a lower W/NGDP.) That’s my “musical chairs” model.

I recently argued that the Keynesians are probably wrong about Britain, on the basis that the employment data is more reliable than real GDP data. Today I’ll argue the Keynesians are probably right about Iceland on the basis that the unemployment rate is more reliable than the real GDP data (as a indicator of demand shortfalls.)

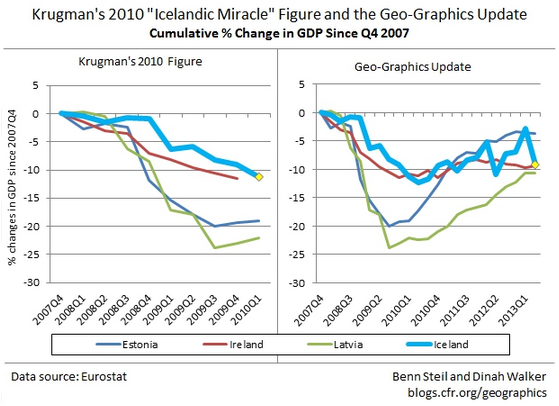

Ramesh Ponnuru sent me the following from Benn Steil and Dinah Walker:

Here it is, folks: Iceland, whose currency lost half its value against the euro in 2008, vs. Estonia, Latvia, and Ireland, all of which were euroized or pegged to the euro over the entire period . . .

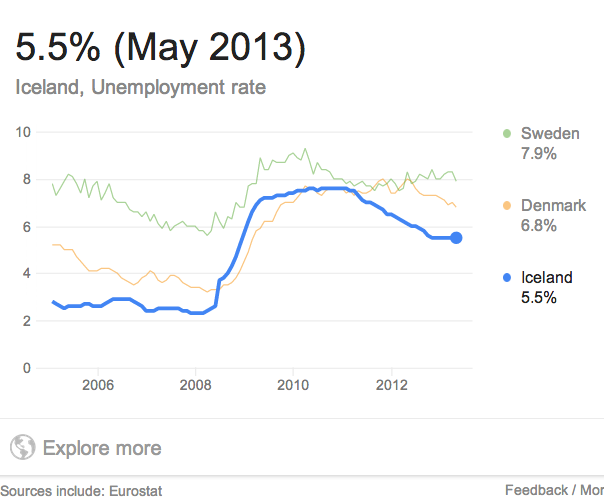

So Iceland is doing no better than Ireland, contrary to the claims of Paul Krugman. If Krugman has used my preferred indicator, however, he would see that Iceland has done far better on the unemployment front:

And now Ireland:

Even accounting for Iceland’s lower natural rate of unemployment, it looks like they’ve done better.

Now a few caveats:

1. The smaller the country the more subject to real shocks, and thus the harder to disentangle demand shocks. Look at the wild quarterly swings in Icelandic RGDP. Even Ireland, with only 4.5 million people, is 20 times larger than Iceland! Real shocks to Iceland’s major industries (fish, aluminum) could explain their erratic RGDP.

2. Smaller countries are also subject to employment swings via immigration and emigration, to a greater extent than large countries. So unemployment numbers are also flawed.

Nonetheless, I expect certain Republican-hating bloggers who thought my British post was garbage to proclaim this post a masterpiece, definitive proof that Krugman is right about Iceland.

PS. For those who don’t know, Iceland devalued and kept their NGDP rising, while Ireland, which was on the euro, saw its NGDP fall.

Tags:

9. October 2013 at 16:52

One of the proper powers of a democratic sovereign nation is the (currency) printing press.

If you are Irish, and you think monetary policy is rotten, how do you vote?

An indecipherable, opaque central bank is poor governance—made worse if that Olympian central bank is making monetary policy for a continental mean, and not your nation.

Central banks are key macroeconomic policy making agencies and need to be brought within the executive branch of each nation.

As we see in Iceland, democracy works, and if not that, is at least good governance.

9. October 2013 at 18:25

The contrast between Iceland’s and Latvia’s employment is especially striking. Iceland’s employment has fallen from 180,200 in 2008Q2 to 173,600 in 2013Q2 or by 3.7%. Latvia’s employment has fallen from 1,142,100 in 2008Q2 to 889,000 in 2013Q2 or by 22.2%.

Of course Iceland’s NGDP rose 16.4% from 2008Q2 to 2013Q2 whereas Latvia’s fell 2.2% over the same period.

This joins the UK in showing why the only way to measure aggregate demand (AD) is to simply measure AD (i.e. NGDP). Changes in RGDP are next to useless owing to the highly idiosyncratic nature of AS.

9. October 2013 at 21:25

Hi Scott,

Strangely, every econ article about Iceland, like yours, seems to include the phrase ” Iceland devalued” this phrase implies that the Seðlabanki evaluated options and after careful consideration….”took action” to effect a lower ISK on the interbank market, that’s not really the case though is it ? Shouldn’t we say that market forces on the interbank market lowered the ISK and the Seðlabanki, hunkered down in a fox hole, was unwilling to use scarce FX reserves to mount a defence. ( This turned out well for Iceland…..through luck, not design)

Have I got this wrong? THX in advance for responding!

9. October 2013 at 21:54

Scott,

Using Iceland as an example for macroeconomics seems a little shaky. Keep in mind that the population of the country is smaller than the Peoria metropolitan area. If you look at small population areas like North Dakota in the United States, they also have very low unemployment rates. In the case of North Dakota, their employment situation has to do with a local resource boom rather than U.S. aggregate demand. Is “demand” in North Dakota higher than “demand” in New York City?

9. October 2013 at 21:55

My point of that last post is that it is usually interesting to pick at macro data more closely because looking at broad statistical aggregates often misses the story entirely. I don’t see why macro exists at all quite frankly.

9. October 2013 at 22:11

National statistics in general are poor. This is not a bad thing. Can you imagine how controlling and bureaucratic a country with perfect national statistics might be? Be careful what you wish for!

Having been to Spain recently with its record high unemployment rate, now stabilising, no-one believes it is a true indicator. Most think real unemployment is half the stated 28%, such is the size of the black economy.

That’s why targeting of expectations is such a great idea.

9. October 2013 at 23:12

One more question for you on the subject of Iceland,

The prevailing wisdom on the exchange rate situation in Iceland is that it would be wildly inflationary….obvious right?

Here’s a little model: (certeris paribus,ok)

An icelandic lumberyard imports 1 container of Finnish timber each year at a cost of 1 million euros. In 2005 this importer paid 75 million ISK for the EUR needed to pay invoice. In 2012 this same container of Finnish wood costs him 160 million ISK. Obviously the importer needs to cover his costs and thus 2×4’s to the consumer are more than twice as expensive. ( voila! wild inflation)

Here is what I can’t get my mind around: The above importer, in his FX transaction, has removed much more ISK than normal from the domestic money supply. The Icelandic MPM has got to be off the charts, they have only fish and sheep, so every time anyone buys anything else they trigger another scenario like the one above. More and more ISK removed from the domesticate markets. macro 101…. would not a rapidly shrinking domesticate money supply be wildly deflationary ?

When I try to answer my own question, I come up with the fact that the 160 million ISK doesn’t cease to exist, it simply moves through the banking system eventually finding it’s way back to the Icelandic economy either through a fish processor or an investor seeking the high returns imposed by the IMF program ( 18% overnight at first), but in order to complete the cycle the banking institution that now has these ISK on it’s balance sheet has to lend to a creditworthy borrower in Iceland who is willing to pay interest equivalent to a 21% overnight…Impossible

( there was a big bump early on but according to publications by the Seðlabanki, Iceland has only experienced CPI inflation in the 5-6 % range over the last few of years)

10. October 2013 at 00:05

James in London,

I’d worry about a government with perfect statistics if that were even theoretically possible. You can’t really measure government spending in GDP because the prices government pay aren’t market prices which is the whole intellectual groundwork for the endeavor.

I agree that if you are going to try and target something, the best target is a market based measure of expectations. The caveat is that it has to be something that people can make money off of if they are right and the government misses the target. In this case though you have the problem of Goodhart’s Law. The variable targeted may not correspond to what you are trying to get anymore.

10. October 2013 at 05:38

krugman has often talked about icelandic unemployment doing better than ireland, e.g. in late 2010:

“Slightly worse (but within measurement error) GDP performance in Iceland, but substantially less bad employment performance.”

http://krugman.blogs.nytimes.com/2010/11/24/lands-of-ice-and-ire/

“Ireland, with 14 percent unemployment, has managed a small decline in wages from their peak. Icelandic wages are up in krona, but way down in euros, to an extent that seems almost unimaginable in a euro zone economy.”

http://krugman.blogs.nytimes.com/2011/10/21/why-not-the-worst/

“I think the interesting contrast is between Ireland and Iceland”

http://krugman.blogs.nytimes.com/2012/07/08/the-times-does-iceland/

search engine:

http://krugman.blogs.nytimes.com/?s=iceland+ireland+unemployment

10. October 2013 at 05:56

Scott, I think you’re right about UK – the pound had a decent devaluation and that helped inflation and employment. Krugman has often pointed out that we can’t all devalue against each other, so USA and UK and Japan and the Eurozone and everyone else can’t all engage in currency devaluation at the same time to create inflation and more employment. That is why he talks about fiscal stimulus I believe. If we’re all in a depressed state we can’t use currency devaluation, unless the inflation-prone emerging markets all try to strengthen their currencies against the wealthier nations. India might be about to do this because of legendary RR, and China has been doing it a bit. Brazilian gov has tried a lot to prevent its currency from strengthening.

PK does seem to have a blind-spot about UK employment – probably because of the Conservatives in power. I hate them too because of their nasty attacks on the poor and disabled, but of course UK employment is doing well because of central bank stimulus.

10. October 2013 at 07:15

Ben, I agree.

Mark, Thanks for the info.

Paul, I’ll take your word for it. I wasn’t even thinking about their motives.

John, You said;

“Using Iceland as an example for macroeconomics seems a little shaky. Keep in mind that the population of the country is smaller than the Peoria metropolitan area.”

As I said in my post, I agree.

James, Good point.

Paul, I don’t follow your example. CPI inflation is often less than the devaluation, as only a modest percentage of the CPI is imported.

dpaff, Krugman ignores the fact that all countries can depreciate against goods and services. Also, at times Krugman has claimed that countries in a liquidity trap cannot devalue at all–which is the implication of the liquidity trap model.

You know more about Britain that I do, but here are some questions:

1. How is it that Britain fails to take care of the poor when spending 48% of GDP, while Canada and Australia succeed in taking care of the poor while spending 35 to 40 percent? Where does all the spending go?

2. Is it true the left in Britain was outraged when the Tories suggested that no one should receive benefits exceeded the medium income?

3. When I lived in the UK I met able-bodied men aged 30 who simple choose not to work. Indeed I lived with one. In America you don’t get welfare in that situation, but under Thatcher they were getting welfare. Is that accurate?

10. October 2013 at 15:40

I often remind people when discussing unemployment in Ireland that the numbers are actually worse than the statistics show. Thousands of able bodies workers are leaving every year for greener pastures. In a country of only a few million that is a huge hit to the labor pool and still double digits.

http://www.irishexaminer.com/ireland/1000-irish-people-emigrate-a-week-241476.html

10. October 2013 at 15:46

Benny,

That article says the Irish emigrants are being replaced with new immigration, including “10,900 coming from eastern Europe, Cyprus, and Malta.”

10. October 2013 at 16:17

Geez Scott. This is another big milestone for me. You understand I can’t possible hate you with after the link?

Not to quibble but I never exactly said it was garbage I was trying to tease out your real positions. Whatever you may think of me I don’t have such a low opinion of your blog as you may think.

I don’t know if you have read Hegel-not assuming either way-but he spoke of the struggle in the world of ideas-the ‘daletic’ and that’s what I’m interested in.

Whatever you believe or not about my knowledge of economics I read you because I have learnt a lot from it.

Funny enough I just happen to have a new piece on our recent-rather pointed-discussion.

http://diaryofarepublicanhater.blogspot.com/2013/10/why-sumner-claims-im-ignorant-of.html

10. October 2013 at 16:27

I think the ‘Hegelian dialectic’ will finally disentangle all the varying econ views that have spouted up since the 2008 Crisis. Prior to it during the GM we had a lovefest-at least within mainstream Neoclassical econ.

Now since 2008 all these contradictory ideas have spouted up. I think you wrote about the Economists’ piece about the new ‘heterodox’ economic ideas.

They listed three: Market Monetarism, Internet Austrianism and-your favorite-the MMTers. It will be interesting to see how much-or little-economics absorbs from these ideas going forward.

I don’t know the answer but it wouldn’t shock me if NGDP becomes an indicator that a lot more people argue for-there may be a lot of people making the counterargument too that NGDP is not the best measure.

However, I admit I don’t agree with your animus about fiscal stimulus-time will tell whether economics agrees or disagrees with you in the future.

10. October 2013 at 16:42

Mike, try not to take the first reading of any philosopher, Hegel included, as “the” answer.

Hegel’s philosophy was resoundingly critiqued by subsequent philosophers, including his own followers, who reluctantly found out that history kept going even after Hegel died, as well as realizing the fundamental contradiction inherent in his philosophy, namely, if all ideas are historically contingent, that is, at best true at a stage in human history, then Hegelianism itself must either be a historial relic, destined to be usurped by a superior philosophy, in which case it isn’t the end of history philosophy it claims to be, or, it is the end, in which case it isn’t consistent with its own premises.

Hegelianism is a severe and cosmic solipsistic megalomania on a grand and massive scale. Robert Tucker had a good point:

“For Hegel alienation is finitude, and finitude in turn is bondage. The experience of self-estrangement in the presence of an apparent objective world is an experience of enslavement … Spirit [or the world-self], when confronted with an object or “other,” is ipso facto aware of itself as merely finite being, as embracing only so much and no more of reality, as extending only so far and no farther. The object is, therefore, a “limit.” (Grenze.) And a limit, since it contradicts spirit’s notion of itself as absolute being, i.e., being-without-limit, is necessarily apprehended as a “barrier” or “fetter” (Schranke). It is a barrier to spirit’s awareness of itself as that which it conceives itself truly to be “” the whole of reality. In its confrontation with an apparent object, spirit feels imprisoned in limitation. It experiences what Hegel calls the “sorrow of finitude.”

“The transcendence of the object through knowing is spirit’s way of rebelling against finitude and making the break for freedom. In Hegel’s quite unique conception of it, freedom means the consciousness of self as unbounded: it is the absence of a limiting object or non-self…. This consciousness of “being alone with self” … is precisely what Hegel means by the consciousness of freedom…. Accordingly, the growth of spirit’s self-knowledge in history is alternatively describable as a progress of the consciousness of freedom.”

10. October 2013 at 19:03

Steve,

“That article says the Irish emigrants are being replaced with new immigration, including “10,900 coming from eastern Europe, Cyprus, and Malta.””

The article Benny Lava linked to says 87,100 people left Ireland over 12 months and 55,900 entered for a net migration of 32,200. Given Ireland has a population of 4.58 million that means its net migration rate is (-6.8) per 1000, which is about the same level it has been since 2009. Here’s the net migration rates for the EU since 1990:

http://epp.eurostat.ec.europa.eu/tgm/table.do?tab=table&init=1&language=en&pcode=tsdde230&plugin=1

Note that Ireland had a net migration rate of +15.6 in 2006, which was more positive than any EU member. It fell to (-6.6) in 2009 and bottomed at (-7.5) in 2010. The only EU members with more negative rates of net migration since 2009 have been Latvia and Lithuania. (The most recent net migration rates for Cyprus and Malta are positive.)

Incidentally Iceland went from a net migration rate of +17.3 in 2006 to (-15.0) in 2009, but it was up to (-6.0) in 2010 and (-0.9) in 2012.

10. October 2013 at 19:17

“32,200” should read “31,200”

(The net migration rate of (-6.8) is correct.)

11. October 2013 at 01:57

Iceland’s credit rating:

http://countryeconomy.com/ratings/iceland

11. October 2013 at 02:01

Estonia’s credit rating:

http://countryeconomy.com/ratings/estonia

11. October 2013 at 02:45

Geoff your point is well taken but I don’t think that Hegel was ‘the’ answer to everything, just that he provided a useful way of looking at the war of ideas.

I’m not sure that I would agree with the idea that all ideas are totally historically contingent either.

Hegel was certainly an important philosopher but I wouldn’t say he’s the last word on everything by any stretch.

Arguably a much more relevant philosopher today is Descartes as we are living in his-digital-world. He had dreamed of the idea that moral questions too could be quantified and calculated on a kind of ‘morality calculator’

11. October 2013 at 02:48

you did hear a lot of talk during the 20th century-whether from the Right, Center or Left-about ‘being on the wrong side of history.’

The Marxists-as Hegelian followers used it first-but later conservatives were able to use it against the Marxists as history evidently has not turned out to be Marxist.

14. October 2013 at 15:48

“I’m not sure that I would agree with the idea that all ideas are totally historically contingent either.”

While I don’t agree with his politics, Leo Strauss had a good point about historicism:

“Historicism thrives on the fact that it inconsistently exempts itself from its own verdict about all human thought. The historicist thesis is self-contradictory or absurd. We cannot see the historical character of “all” thought “” that is, of all thought with the exception of the historicist insight and its implications “” without transcending history, without grasping something trans-historical.”

15. October 2013 at 17:48

Interesting quote from Strauss. I think he’s probably right.