Graph of the day

This is from Britmouse:

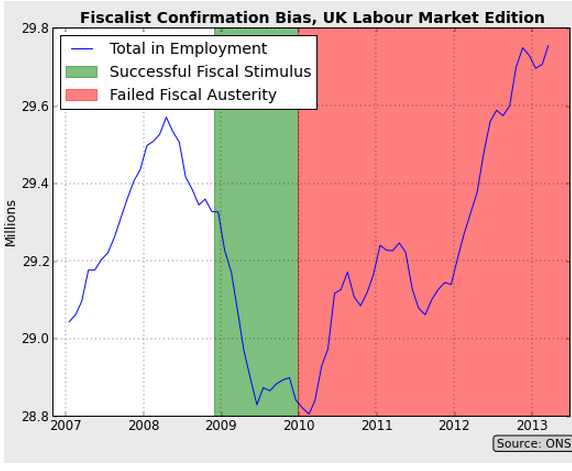

And while we are at it, here’s another interesting graph from Britmouse:

Deflation is bad if it comes from the demand side, and causes firms to cut output because they see falling profits as prices fall. Thus if you focus on inflation (not a good idea!), at a minimum you should be looking at prices net of VAT. In Europe the austerity has involved VAT tax increases, which cause the ECB to tighten policy, driving NGDP even lower. You see the demand shock in the inflation rate net of VAT.

Note that I’ve always argued fiscal austerity can reduce output if the central bank is stupid, for all you people who think I’ve been an ideologue on the issue.

HT: W. Peden

Tags:

17. July 2013 at 05:11

How about that taper?

“U.S. housing starts and permits for future home construction unexpectedly fell in June, further evidence of a sharp slowdown in economic activity in the second quarter.

The Commerce Department said on Wednesday housing starts dropped 9.9 percent to a seasonally adjusted annual rate of 836,000 units. That was the lowest level since August last year.”

http://www.cnbc.com/id/100892237

17. July 2013 at 05:13

[…] Here is the answer to both questions, in one graph, from Britmouse (via Scott Sumner): […]

17. July 2013 at 05:33

Meanwhile, Bernanke is going from creditism to fiscalism:

Fed Chief Calls Congress Biggest Obstacle to Growth

By BINYAMIN APPELBAUM

WASHINGTON “” The Federal Reserve’s chairman, Ben S. Bernanke, said Wednesday that Congress is the largest obstacle to faster economic growth, and he warned that upcoming decisions about fiscal policy could once again undermine the nation’s recovery.

“The economic recovery has continued at a moderate pace in recent quarters despite the strong headwinds created by federal fiscal policy,” Mr. Bernanke said in the opening line of his prepared remarks to a Congressional committee.

http://www.nytimes.com/2013/07/18/business/economy/fed-chairman-points-finger-at-congress.html?_r=0

17. July 2013 at 06:13

I have some interesting graphs too:

http://capitalmarketsu.com/wp-content/uploads/2011/01/swedish_monetary_policy.png

http://www.adamsmith.org/sites/default/files/japanflation.png

http://graphics8.nytimes.com/images/2012/04/28/opinion/042812krugman1/042812krugman1-blog480.jpg

But hey, continue trying to prove that decreasing spending increases spending. It is fun to watch.

17. July 2013 at 06:22

OhMy,

Your charts would be more interesting if they weren’t followed by mocking a strawman.

17. July 2013 at 06:36

W Peden,

Someone is grasping at straws not to draw conclusions from the charts.

17. July 2013 at 06:47

Anyways there is something else to have from the last graph. How come that between 2011 – 2013 unemployment in Greece increased from 15% to 26% all the while experiencing only 1 percentage point of disinflation (from 0 to -1%)?

It seems that Central Banks targeting inflation “close but below 2%” – like in range of 0-2% is perfectly consistent with Great Depression level of unemployment.

17. July 2013 at 06:51

J.V. Dubois,

Alternative explanation is that CBs lost control of the situation (if they ever had it) and due to nominally denominated contracts and sticky prices inflation doesn’t fall much even in a deeply depressed economy. If they “targeted” inflation or not, it would still be around 0%.

17. July 2013 at 06:57

Scott,

I recently had a long back in forth in comments at Noah Smith’s post on Inflationistas with an antistimulus Portuguese economist of the Austrian school. The conversation ironically supported my argument that even in the Mediterranean they are heavily influenced, subconsciously or not, by German Ordoliberalism. In short things are truly bizarre in the eurozone.

While researching my comments I noticed that Portugal experienced year on year GDP implicit price deflator deflation in 2012Q1-2012Q3:

http://research.stlouisfed.org/fred2/graph/?graph_id=129380&category_id=0

Deflation hasn’t shown up in HICP at constant taxes in Portugal yet.

Note also that Ireland first started experiencing year on year deflation all the way back in 2007Q3, perhaps something of an early warning.

17. July 2013 at 07:17

HICP includes VAT, but excludes housing. Housing prices are down in all those economies.

17. July 2013 at 07:18

I am still amazed that the higher final prices due to a VAT increase are considered inflation.

17. July 2013 at 08:29

Off topic, but you might be interested in:

http://www.project-syndicate.org/blog/the-seduction-of-ben-bernanke-by-christopher-t–mahoney

17. July 2013 at 08:35

Luis, the housing market has so much unsold inventory it’s pretty hard to evaluate housing prices at all. In most of Spain, for all intents and purposes, there’s no housing market, as nobody wants to sell unless they are forced to, because they don’t want to take a nominal loss: Money Illusion doesn’t happen only in wages.

Besides, given how Spanish mortgages are set up, if someone is underwater, defaulting on the loan will make them eat the loss with their assets: The mortgage issuing bank only takes a loss if the former owner of the house has no assets whatsoever. This feature doesn’t lead to a very liquid market when house prices fall: A formerly well off Spaniard could end up losing their primary residence because he can’t afford his summer house anymore. You can imagine what having people servicing mortgages they can’t really afford and can’t get rid of does to a retail sector.

17. July 2013 at 08:37

We don’t know what the size of the underlying AD shock is (something that is completely model dependent).

By this graph, it seems the UK unemployment rate only went up ~3% at the depths of the recession (as a comparison the US unemployment rate doubled, increasing by 5%).

Google pops up a nice graph!

http://www.google.com/search?q=uk+unemployment+rate

The UK unemployment rate has also remained constant since 2009 … so it appears that fiscal stimulus blunted the impact of the recession and that “austerity” has made no change since that point.

But that is just one interpretation. I mean the UK monetary base went up by 4x while the US only went up by 2x at the start of 2009. Maybe monetary stimulus blunted the impact of the recession. Another plausible mechanism.

Cherry picking data, indeed! It appears we know nothing more than we did before.

17. July 2013 at 09:01

“Note that I’ve always argued fiscal austerity can reduce output if the central bank is stupid, for all you people who think I’ve been an ideologue on the issue.”

Prof. Sumner, my understanding is that your position is that, given the authority and autonomy of CBs, it makes no sense to consider the effect of fiscal policy without taking the central bank’s response into account. The obvious implication is that when a CB is doing its job, any fiscal policy that moves the economy away from the preferred track will be counteracted with monetary action. Is this an accurate understanding of your position? I’d like to make sure I have the right idea when I am arguing about the whole “Sumner is an austerian who doesn’t think fiscal policy can do anything ever” thing. Thanks.

17. July 2013 at 09:31

OhMy. You deserve a Nobel Prize for discovering that the demand for base money slopes downward.

rbl. The multiplier is zero when they are doing their job as I see their job, not necessarily as they see their job. They might think their job is to stabilize a price index including VAT. Of course all this assumes they have a central banks, which many European countries do not.

Jason, I agree that there are lots of valid ways of looking at the data.

Everyone, Sorry, That’s all I have time for right now. Will be on Bloomberg radio soon.

17. July 2013 at 10:14

ssumner,

QE has nothing to do with demand for base money. This demand is satiated anyhow without QE, that is the point of having the CB.

17. July 2013 at 15:24

“Deflation is bad if it comes from the demand side, and causes firms to cut output because they see falling profits as prices fall.”

Not all “output” should continue, and not all “employment” should remain where it is.

To complain that deflation reduces aggregate “output” and/or aggregate “employment” overlooks the details within each category, where it is possible, indeed likely, that whole economies are structured in an unsustainable way where deflation is the only way to uncover which projects are most urgently in need of readjustments.

The tide moving back is the only way to reveal who isn’t wearing a bathing suit.

17. July 2013 at 19:22

Off-thread topic: Bloomberg Radio, the Hays Advantage:

Bentley’s Sumner Says Markets Disagree with Fed Outlook (Audio)

http://media.bloomberg.com/bb/avfile/Economics/On_Economy/vqVzXN.Vs.oE.mp3

IMO, Prof. Sumner sounded more comfortable during this radio interview than previous sessions. Good job!

17. July 2013 at 19:34

http://www.theglobeandmail.com/report-on-business/economy/housing/vancouvers-million-dollar-divide/article13242548/

Unrelated, just an infographic of real estate market of vancouver.

18. July 2013 at 00:00

[…] Source […]

18. July 2013 at 02:12

OhMy: In so far as I can infer a point, it seems to be a stinging refutation of quantity monetarism c.1970. And who around here is defending that?

Surely Britmouse’s underlying point is that analysing fiscal stimulus/austerity without considering monetary policy is pointless. If fiscal stimulus “works” then so does monetary stimulus, and vice versa. Indeed, the argument for fiscal stimulus is precisely that monetary stimulus is blocked. If you don’t believe that, then monetary stimulus is clearly cheaper and more efficient than fiscal stimulus.

18. July 2013 at 06:51

OhMy, The demand for base money is always “satiated,” the question is at what price level, what NGDP?

Thanks Ricardo.

Edeast–interesting map.

19. July 2013 at 00:21

[…] Here is the answer to both questions, in one graph, from Britmouse (via Scott Sumner): […]

21. July 2013 at 01:50

And here are the census maps for vancouver, showing where immigrants settle, looks like asian culture hypothesis. http://www.vancouversun.com/life/Vancouver+maps+ethnic+makeup+Metro+Vancouver/5546566/story.html

english scotts germans a little over to the right

12. June 2015 at 04:03

[…] Here is the answer to both questions, in one graph, from Britmouse (via Scott Sumner): […]