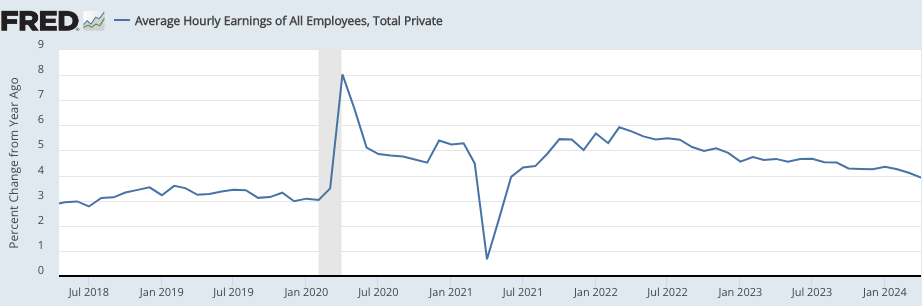

As you may know, the actual Phillips Curve is about the relationship between unemployment and wage inflation. That’s the relationship A.W. Phillips actually identified, and it’s still the correct version. Price inflation doesn’t correlate well with unemployment. Painful disinflation is and always has been about getting wage inflation down.

Forget payroll employment, the big news in today’s job report is the decline in 12-month wage inflation, to a rate slightly below 4% (and only 2.8% over the past three months):

It’s ironic that the thing that may well cost Biden the election (a surge in undocumented immigration) is the very thing that might (and I emphasize might) allow the first recession-free disinflation. The first American soft landing.

PS. The ultimate goal should be around 3.0% to 3.4% wage inflation.

PPS. It looks to me like wages are about 8% above pre-Covid trend and NGDP is about 10% above trend. I suppose the gap is unexpectedly high immigration. So Fed policy has been roughly 8% to 10% too expansionary over the past 5 years.

1. Commenter Floccina directed me to a video showing Matt Yglesias’s ideal city.

2. A back issue of Harpers had an article discussing the possibility of legalizing drugs. This comment caught my eye:

At the time, I was writing a book about the politics of drug prohibition. I started to ask [former Nixon aide] Ehrlichman a series of earnest, wonky questions that he impatiently waved away. “You want to know what this was really all about?” he asked with the bluntness of a man who, after public disgrace and a stretch in federal prison, had little left to protect. “The Nixon campaign in 1968, and the Nixon White House after that, had two enemies: the antiwar left and black people. You understand what I’m saying? We knew we couldn’t make it illegal to be either against the war or black, but by getting the public to associate the hippies with marijuana and blacks with heroin, and then criminalizing both heavily, we could disrupt those communities. We could arrest their leaders, raid their homes, break up their meetings, and vilify them night after night on the evening news. Did we know we were lying about the drugs? Of course we did.”

3. AP has an interesting story on the origins of Covid. Here’s one tidbit:

Governments in Asia are pressuring scientists not to look for the virus for fear it could be traced inside their borders.

And this is even more interesting:

The first publicly known search for the virus took place on Dec. 31, 2019, when Chinese Center for Disease Control scientists visited the Wuhan market where many early COVID-19 cases surfaced.

However, WHO officials heard of an earlier inspection of the market on Dec. 25, 2019, according to a recording of a confidential WHO meeting provided to AP by an attendee. Such a probe has never been mentioned publicly by either Chinese authorities or WHO.

In the recording, WHO’s top animal virus expert, Peter Ben Embarek, mentioned the earlier date, describing it as “an interesting detail.” He told colleagues that officials were “looking at what was on sale in the market, whether all the vendors have licenses (and) if there was any illegal (wildlife) trade happening in the market.”

A colleague asked Ben Embarek, who is no longer with WHO, if that seemed unusual. He responded that “it was not routine,” and that the Chinese “must have had some reason” to investigate the market. “We’ll try to figure out what happened and why they did that.”

4. According to the FT, English speaking countries seem to attract the best people, according to a wide range of metrics including being law abiding:

International comparisons find that people with immigrant backgrounds are generally imprisoned at similar or higher rates to the native-born, except in the US, UK, New Zealand and Australia where they are under-represented in the prison population, a sign of successful integration.

However, these are relative crime rates. Recall that the absolute rate of imprisonment in the US is higher than for most other countries. The following graph is interesting:

I’m actually surprised that the immigrant situation in Sweden isn’t much worse. Given the stories I’ve read about immigrant crime in Sweden, I didn’t expect to see that country so close to the 45 degree line.

5. Chinese audiences used to go for dramas with rich, successful, and arrogant leads. Now beta males are in fashion:

They might work in an office setting in which they are treated as nobodies, but at home and in front of women, they show their husbandly charm. Far from undermining their manliness, the loser label highlights not merely their “worthlessness” but also their willingness to sacrifice. Under enormous professional and personal pressures, young people have no choice but to endure and compromise — to be “losers” — in order to make ends meet. Audiences, able to empathize, are falling hard for men who reflect this reality.

6. Dumb and dumber. The exceedingly dumb Donald Trump is seeking a VP that’s even dumber, who will not overshadow him. Apparently Elise Stefanik is among the finalists. She certainly seem to fit the bill:

Job opening: Vice President of the United States of America (serving behind a nearly 80 year old man). Only complete morons need apply.

7. Nate Silver has a good piece on the ways that people form political opinions. This nugget caught my eye:

And sometimes the desire for social signaling can lead people to confused positions. Here, for instance, was a statement made by a protester at a “Queers for Palestine” rally in January.

“Palestine could be the most homophobic place in the world—which it’s not, it’s literally better than here—but it could be, and does that mean all these people need to be killed?” Yaffa asked. “A third of those are children. The children are the homophobes?”

Emphasis mine. The protestor was claiming that Palestine — where same-sex sexual activity is illegal and has sometimes been subject to execution — was literally less homophobic than the place where the rally was held. The punchline is that the rally took place in Northampton, Massachusetts, which is sometimes considered the lesbian capital of the world. You have to be engaged in an extraordinary degree of motivated reasoning to think that Northampton is literally more homophobic than Gaza. The sort of motivated reasoning that comes when there are social rewards both for being pro-Palestine and for being pro-LGBTQ+, enough that nobody in your bubble is really pressing you on the details.

One area where the horseshoe theory applies is that the extreme left and the extreme right are both dumb as rocks.

You: What do you mean? I asked for your view on the situation.

Me: My view is that the question you asked is the problem. The problem is that we are asking questions about Gaza. If we were not asking those questions, there would be no problem.

You: Please explain.

Me: You asked me about Gaza because your mind is infected with “identity politics virus”. If you are a leftist, it takes the form of oppressor (Israel) — oppressed (Palestinians). If you are a rightist, it takes the form of civilization (Israelis) — barbarism (Palestinians). Either way it’s bad. Identity politics is the cause of the crisis. The model for a successful world is Switzerland, which is (mostly) free of both right and left identity politics, at least compared to most other places. The German, French and Italian speakers mostly get along fine.

You: But why can’t I ask you for your views on Gaza?

Me: Because you should be asking me about more important conflicts, such as Sudan, Ukraine, Yemen, Burma, etc. The Arab-Israeli conflict has been going on for my whole life. It’s tragic, but nothing new. It’s boring, and relatively small. The fact that you asked me about Gaza shows that your view of what’s important has been distorted by identity politics, which is exactly the same factor that causes the problem. Hence your question is itself part of the problem.

It’s easy for Americans to look at a country like India, and say, “Tsk, tsk, the caste system is obviously bad, why don’t they get rid of it and treat everyone equally?” But Americans fail to see the problem in their own country. Indeed, we are constructing our own caste system, which is just as evil as the Indian system.

White, black, Hispanic, Asian, male, female, gay, straight, trans, Christian, Muslim, Jewish, etc. People are people. Stop viewing them as part of a group. No Muslim travel bans and no affirmative action for Muslims. And no shaming of people for switching race, gender, religion, etc.

Then, in 2023, the Immigration Control Agency was dissolved, ostensibly in response to an extremely uncharacteristic display of violence where, in March 2020, two officers beat a Ukrainian man to death in the airport of Lisbon.

No protests followed the unjust death of this man on Portuguese soil. This makes for an illustrative contrast to when, three months later, the June 2020 Black Lives Matter protests were, just in Lisbon, attended by over 5000 people, decrying the death of an African-American man 6000 kilometers away on New World soil.

2. Is there a double standard in the US attitude toward human rights? Is the Pope Catholic?

Consider this: In 2023, suspicion swirled that the Indian government was connected to the killing of a Canadian citizen on Canadian soil and a plot to kill a U.S. citizen on U.S. soil—a remarkable set of allegations. Yet even more remarkable than the allegations were the reactions. The U.S. government opted to douse the potentially incendiary fallout, saying little, merely allowing the case to wend its way through the courts. In other words, Indian hubris was accommodated, not chastised. It was a testament to India’s newfound political standing.

What if it had been China?

3. East Asian governments have a new interest in boosting stock markets. I wonder why? Here’s the FT:

Rekindled investor interest in China’s state-owned behemoths would also reflect their continued economic prominence and an ongoing campaign by Beijing to improve financial performance. As their biggest shareholder, the central government stands to benefit from higher valuations and larger dividends.

“SOEs used to have lower revenue growth, lower returns on equity and much higher balance sheet leverage than private companies. But after 2020, we’ve seen SOEs improving,” said Winnie Wu, a strategist at BofA Securities in Hong Kong.

There are parallels with government campaigns in Japan and South Korea to improve stock market valuations, she said, noting that buying into SOEs might suit fund managers with benchmarks that require exposure to China.

4. Disney bought a huge area in central Florida out of frustration that urban development in Anaheim had hemmed in their original Disneyland. But it turns out that even in Anaheim they had much more land than they thought, and plan a 50% expansion into their vast parking lots.

The development agreement the city is agreeing to maps out where new theme park construction could occur over the next 40 years, giving Disney flexibility to determine what exactly would be built – though all still within the footprint of its current properties. The goal, Disney officials say, is to use underutilized land around the resort to build immersive experiences in Anaheim as the company has done elsewhere around the world.

Because of high land prices, suburban parking lots in Orange County have become gold mines.

5. Perhaps our immigration policy should steer clear of whites, and focus on cultures that are more likely to be entrepreneurial, like Hispanics, Asians, and blacks. From the WSJ:

6. The new right faces a problem. If they ever succeed in taking over our institutions, they lack an elite capable of running these institutions. As a result, they might be better off moving away from their current infatuation with government power, and switch to classical liberalism. Here’s John McGinnis:

As a result of the New Right’s mismatch problem, an intensification of the classical liberal program may paradoxically be more likely to achieve indirectly the objectives of the New Right than its own misguided program for more state power. For instance, if the momentum of school choice programs continues, competition may naturally deliver a more patriotic and family-friendly education than government schools, because that is what most parents want. The policy matches sociology: school choice empowers a group more friendly to the New Right (parents) and disempowers a group (teachers—who are more hostile to it).

Similarly, a program of deregulation disempowers bureaucracy and groups within a corporation that are hostile to conservative views. The result is likely to be a less woke corporate world.

The U.S. economy last year expanded by 2.5%, and while the rest of the press missed it, fossil-fuel producing states led the way. These include North Dakota (5.9%), Texas (5.7%), Wyoming (5.4%), Oklahoma (5.3%), Alaska (5.3%), West Virginia (4.7%) and New Mexico (4.1%). Mining contributed about two to three percentage points to GDP growth in these states.

GDP growth in most other states was sluggish, especially those in the Northeast like New York (0.7%) and New Jersey (1.5%) and the Great Lakes region. Mr. Biden boasts about a Midwest manufacturing boom, but folks aren’t feeling it in Wisconsin (0.2%), Ohio (1.2%), Illinois (1.3%) Indiana (1.4%) and Michigan (1.5%).

Biden’s industrial policy looks like a dud, and the energy states are not the swing states that he needs to win.

8. According to a recent article in the FT, relatively affluent Hong Kong is less technologically advanced than Beijing, capital of a middle income country:

I moved to Beijing this month, one of a trickle of correspondents recently granted entry to mainland China after expulsions and the pandemic drained our numbers. On my first evening, I ordered some paracetamol on the popular delivery app Meituan. It arrived in 20 minutes, brought to my hotel room by an affable, metre-tall white robot. “Thank you, see you again soon,” it chirped before rolling away.

This was a novelty for someone who had come from the technological backwater of Hong Kong, where newspaper stands, trams, diesel engines and cash keep you firmly rooted in the last century. Suddenly, I was thrown into the dazzling array of apps and automation that eases friction in this sprawling metropolis — from services such as ride hailing, housekeeping and food delivery to a hotel elevator equipped with facial recognition technology that automatically whisks me to the correct floor.

Not sure what to make of this, but it’s interesting. (I’d still prefer to live in Hong Kong.)

9. America’s first high speed rail will go from Las Vegas to the bustling metropolis of Rancho Cucamonga. Your tax dollars at work:

Eventually, I’ll get to price indices. But first, a long boring digression on why I don’t want to be “rich” (but do want to have a billion dollars.)

I recently read a WSJ story about how a $200 million St. Louis skyscraper had sold for only $4 million. That got me wondering what house prices looked like in that area. Through the miracle of Zillow, all of our curiosity can be satisfied at the push of a button.

On the north side of town, houses sell for less than $50,000. The most expensive homes I could find were in the fashionable area near Forest Park, Washington University, and major hospitals. One Florentine palace has an interior that looks like the sort of place that Queen Elizabeth might have inhabited. The asking price is just under $2 million, and it contains 12,847 sq. feet (or roughly 1200 sq. meters for you foreigners.)

You can see this sort of house in old black and white films from the 1930s. The owner is a balding fat guy with a cigar and top hat. Probably a banker. When I was young, this was my vision of being really, really rich.

And then it hit me—I could afford this house.

[No, I don’t have the sort of income required to buy this house, nor did I before I retired. Rather I bought a normal house in Boston in 1991, saw it rise rapidly in value during the Boston boom, and then switched to a roughly equal Orange County house in 2016, which proceeded to rise in value far faster than houses back in Boston over the past 8 years. I’ve been very lucky.]

Thus I could live in a fabulous mansion similar to those I grew up watching in the movies. OK, I would not have servants, but they make me uncomfortable. I hate luxury hotels where they stop by once an hour and ask if you need anything. Just leave me alone!

But I have decided not to buy this mansion. Unlike when I was young, the thought of living there now seems kind of depressing. And I’d go even further. While I would not turn down Versailles if the French government offered to give me that monstrosity, I’d honestly rather live in a 3500 sq. foot mid-century modern house on a hill in Laguna Beach overlooking the Pacific—which unlike the St Louis mansion, is a home that I definitely cannot afford. I’d even prefer a 4000 sq. foot Tuscan style home with a half acre perched on a hill in Turtle Rock, Irvine, also unaffordable.

In other words, I have no interest in being rich, as the term “rich” was defined 100 years ago. But I do want lots of money. As Danny DeVito once said:

Everyone needs money, that’s why they call it money.

[An illustration of why David Mamet is our greatest screenwriter.]

I suspect that most people don’t want to be rich in the sense of what being rich meant back in 1910; rather they want to have lots of money so that they get to choose how to be rich today.

In that case, what are we actually trying to measure with price indices? Does revealed preference suggest that I’m richer than that fat cat banker from the 1920s? He would not think so. And think about archaic phrases like “fat cats” and “jet setters”. These are people rich enough to get fat and fly on airplanes. A group we now call “working class”.

Part 2: An Elegy for the Midwest

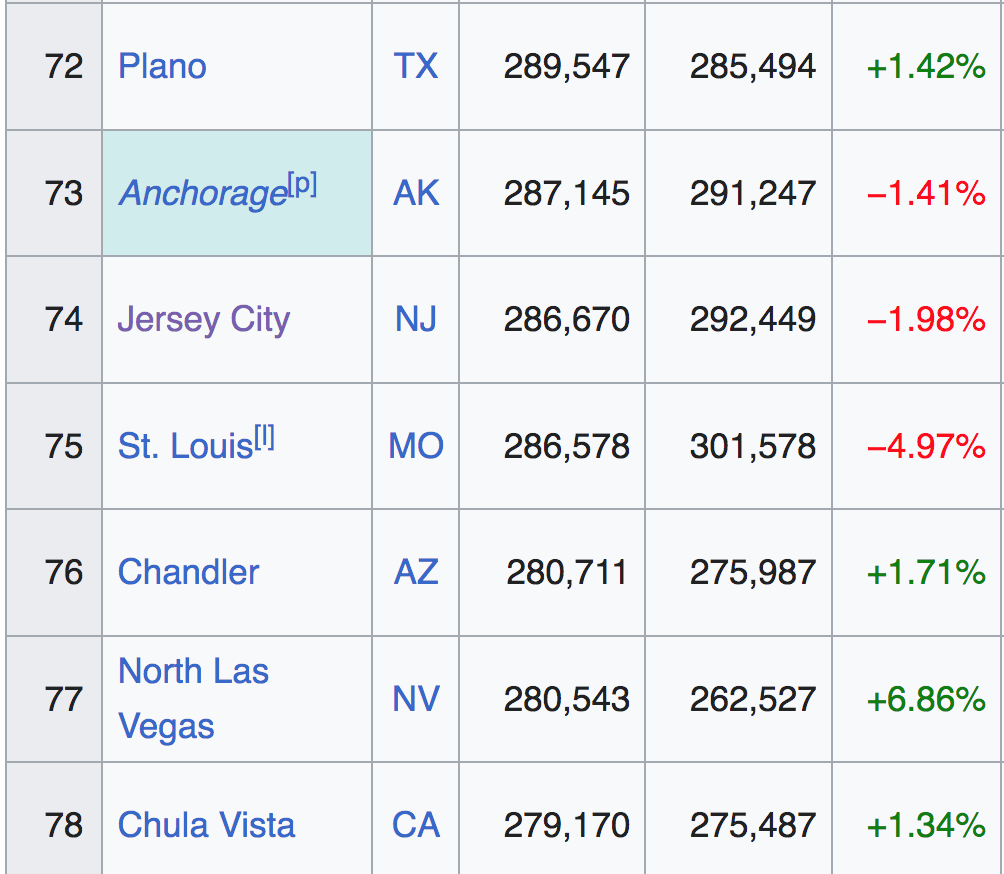

I found my Zillow exploration of St Louis to be a bit depressing. Back in 1900, this was America’s 4th largest city. Now it’s number 75:

St Louis had a spectacular World’s Fair back in 1904, in Forest Park. It’s also depressing that world’s fairs are no longer interesting. “Stuff” no longer matters, only “information”. When was the last time you were excited to see the new models at an auto show?

The WSJ article suggests that the downtown is nearly dead, but there are some gentrifying neighborhoods just west of downtown. Zillow shows that they’ve converted a number of grand old office buildings from the golden age of commercial architecture (1890-1940) to loft style residential units that sell at prices far below what you’d pay in New York, or even in Chicago. That’s good.

But look more closely and you’ll see that the interior design is a bit amateurish. This is a depressing reminder that the Midwest is losing a lot of its talent to the two coasts (and Texas.) When I was born in 1955, the upper midwest was America’s richest region. More importantly, talent was distributed fairly evenly from the northeast through the midwest to the west coast. (Perhaps the South was a bit behind.) Now the industrial Midwest is slowly emptying out.

The people who design modern condos in New York or the Bay Area would look down their noses at the design quality of the loft condos in these up and coming St Louis neighborhoods. Unlike in 1955, it now almost feels like these regions are part of two different countries. But 100 years ago, America’s best architecture was being produced by the “Chicago School”.

PS. My fondest memory of St Louis is seeing Sullivan’s magnificent Wainwright building. Not the first skyscraper, but probably the first beautiful skyscraper:

Welcome to a new blog on the endlessly perplexing problem of monetary policy. You’ll quickly notice that I am not a natural blogger, yet I feel compelled by recent events to give it a shot. Read more...

My name is Scott Sumner and I have taught economics at Bentley University for the past 27 years. I earned a BA in economics at Wisconsin and a PhD at Chicago. My research has been in the field of monetary economics, particularly the role of the gold standard in the Great Depression. I had just begun research on the relationship between cultural values and neoliberal reforms, when I got pulled back into monetary economics by the current crisis.

"Scott, "..as you may know, the actual Phillips Curve is about the relationship between unemployment and wage inflation..." Isn't the relationhip unemployment and "real" wage inflation? As far as I..."

"Scott, "...It’s also human nature to rape and murder and enslave, and these things have been going on for millennia. But we need to stop..." These things were eliminated (in..."

"This is actually the MAGA position. Nobody cares if you get plastic surgery to change your genitals, just don't ask me to pay for it, or ask me to call..."