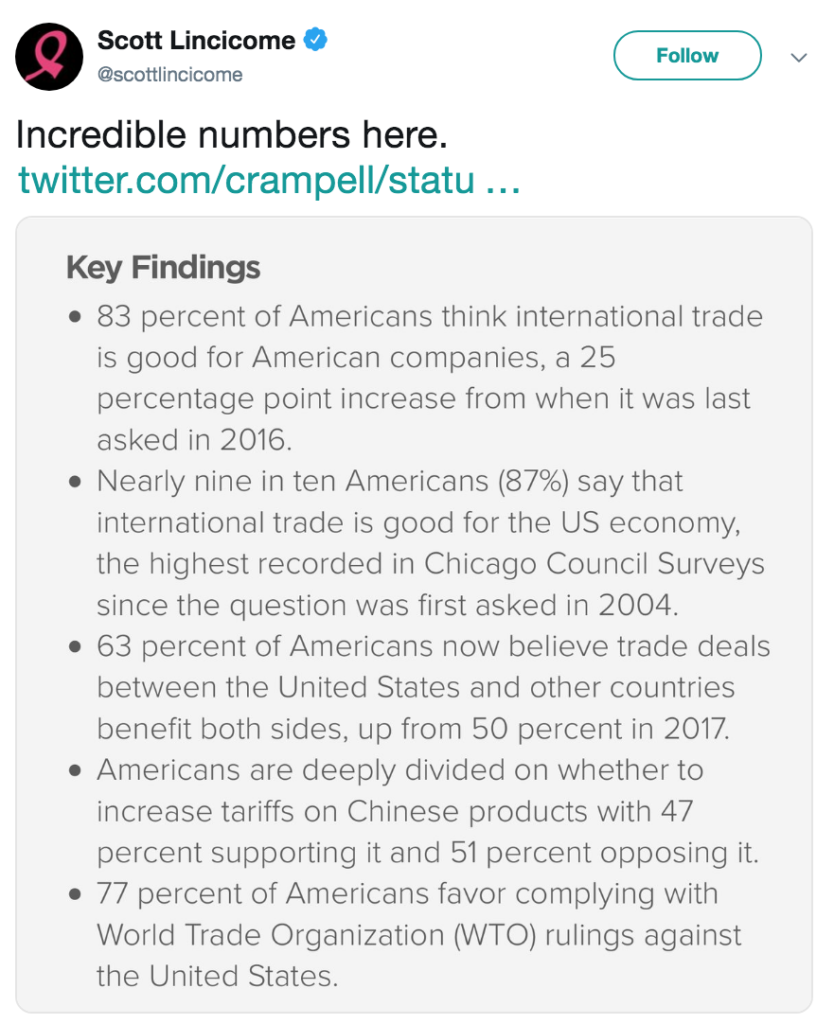

Back in 2016, I pushed back against the conventional wisdom that Americans were opposed to trade and that this explained the rise of Trump. Even then the polls didn’t show that. Of course I was viewed as naive—the zeitgeist was all about the China shock, deindustrialization in the Rust Belt, the rise of populism, etc. Didn’t I know that neoliberalism was passé, it had failed us? OK, so how do things look today?

So do you guys still believe that Trump’s views on trade (“trade wars are good, and easy to win”) represents the wave of the future? Am I just an old foggy who doesn’t understand how bad globalization has been for average people?

The estimates imply that trade with China increased U.S. consumer surplus by about $400,000 per displaced job, and that product categories catering to low-income consumers experienced larger price declines. [emphasis added]

I bolded the low income part, because if trade is good for efficiency then equity is the only issue at stake here.

PS. I notice that the current zeitgeist is all about “progressive” ideas like wealth taxes and fiscal stimulus. Unlike certain publications, I don’t swing with the political winds. Taxes on capital income always have been evil, and always will be. All taxes are consumption taxes. The only difference is that some consumption taxes tax future consumption at higher rates than current consumption. Those bad consumption taxes are called “income taxes”, “capital gains taxes”, “wealth taxes”, etc. Instead we should tax higher levels of consumption at higher rates. That’s a truly progressive agenda.

Stick to your principles when the rest of the world is losing its head. In the long run, they’ll come back to you. Stable NGDP growth, free markets, free speech, free trade, progressive consumption taxes, externality taxes. Those principles aren’t going to change.

President Donald Trump said in a Twitter post that he plans to meet with Liu on Friday, adding that it’s a “big day of negotiations with China. They want to make a deal, but do I?”

Wait, isn’t that the exact opposite? Yes it is. But Trump always says the exact opposite of what’s true. A perfect phone call is a disastrous phone call. A traitor is a patriot. The man who respects women more than any guy other actually respects them less than any other guy. The wisest leader is the least wise. I could go on and on.

You have to know how to read Trump, then it’s as easy as reading the mood of a 4-year old child.

I suppose the North Korean leader is the best example of someone who frequently demands that his subjects kowtow. But that’s basically for domestic consumption. What about governments that try to get foreigners to kowtow? In that class, there are only three countries that matter.

Number two and three are obviously China and Russia, in whatever order you choose. Russia demands subservience from former members of the Soviet Union, such as the Ukraine and Georgia. China demands that foreign companies censor speech that annoys the Chinese government. And they occasionally demand technology transfers as the price of investment.

But the US is far and away the biggest abuser of kowtow. We demand kowtow in so many different areas that I could write a book on the subject:

1. Sanctions. We sign an arms control agreement with Iran. Other countries cooperate. Then we elect a new president who abandons the agreement and then insists that all other countries follow his whim, despite the lack of expert opinion in his favor. No other country in the world is so arrogant in demanding that everyone agree with their foreign policy.

2. FATCA. We demand that other countries provide all sorts of private information on overseas Americans, or even people that aren’t actually Americans but happened to be born in the US. But when other countries ask us to reciprocate, we often refuse to share private information about their citizens. We are now the world’s leader in providing international tax shelters, often using state-registered dummy corporations. We demand the Swiss do what we say, but refuse to do the same. No other country is so hypocritical on tax issues.

3. Exchange rates. We demand that other countries set their exchange rates at a level that we approve of. When the Japanese tried to devalue in the early 2000s in order to escape from deflation, the Bush administration told them to stop. We get to tell the Japanese where to set their exchange rate, but they don’t get to tell us where to set our exchange rate. No other country in the world does this.

4. Industrial policy. We have all sorts of candidates, in both parties, advocating this or that industrial policy. From the discussion, you’d almost think that a country has the right to determine its own industrial policy. But that’s only true of the US. In the 1980s, we complained about Japan’s industrial policy, and today we complain about China. But how would we react if China started telling us how to run our economy? In this case, other countries do occasionally follow the US lead, but mostly in WTO-type disputes. The US is unique in demanding changes in industrial policy that are essentially unrelated to trade.

There are dozens of similar examples. It’s only fitting that the King of Kowtow has a new president who actually thinks he’s a king. Trump was enraged when a few “disloyal” Republicans had the temerity to criticize his obviously corrupt actions. But now even silence is not enough. No matter what he does, he wants GOP members of Congress to affirmatively praise his actions, regardless of how appalling they are. The level of obsequiousness that he demands would make a medieval despot like Tamerlane blush.

There are plenty of countries that are worse than Russia and China, and many more that are worse than the US. But these three countries stand out for their combination of power and arrogance. Look for India to join the club over the next few decades—they’re well on their way.

PS. Still don’t think Trump is worse than Nixon? How about this:

DOJ lawyers sought to invalidate that request for documents on Tuesday by claiming that a key legal ruling from 1974, which paved the way for the House to prepare impeachment articles against President Richard Nixon, should no longer apply, the outlets said.

The argument reportedly stunned Judge Beryl Howell, the chief district judge for Washington, DC.

Patrick Cotter, a former federal prosecutor who was on the team that convicted the Gambino crime family boss John Gotti, said he’s struck by the parallels between Trumpworld’s handling of the impeachment controversy and the mafia’s playbook on pushing back against charges leveled against it. . . .

Michael Cohen, Trump’s longtime former lawyer, testified to Congress in February that the president runs his operation “much like a mobster would do.”

Former FBI director James Comey has frequently compared the president to a mob boss and said that when he first met Trump, he couldn’t shake the feeling that he felt he was dealing with the Cosa Nostra.

“It’s not about anything else except the boss,” Comey said while giving a talk at the 92Y in New York City last year. “It’s a fear-based leadership.”

Some of you thought my comments about Trump in 2016 and 2017 were hysterical, but everything I suggested is becoming obvious to anyone that isn’t blind. This is going to be fun.

The UK government is about to appoint a new Governor of the Bank of England, as Mark Carney’s term is expiring. Oddsmakers have made Gerard Lyons the even money favorite to be picked, partly because he’s the only candidate who supported Brexit and partly because he’s known and liked by Boris Johnson.

Commenter wlb directed me to a Bloomberg interview where Lyons suggested that it was time to re-examine the BoE’s remit, particularly the question of whether they should stick with inflation targeting or consider a “money GDP” target. I can’t be certain, but listening to him talk it’s hard not to reach the conclusion that he finds the latter option more appealing. Otherwise, why suggest the need for reconsidering the BoE’s remit?

Meanwhile, in the US there are rumors that St. Louis Fed President James Bullard might be picked to replace Powell in 2020, assuming Trump is re-elected. Bullard has recently argued that NGDP targeting has several important advantages over inflation targeting.

It’s often said that the Keynesians didn’t win by convincing the economic establishment of the 1930s, rather they convinced a younger generation of economists who were open to their ideas. Those economists took over the reins of power after WWII.

I see something similar happening with NGDP targeting. It will succeed gradually, as more and more younger economists (who have no experience of the high inflation 1970s) see its advantages over inflation targeting.

PS. Over at Econlog, I give the Fed advice on how to implement NGDP targeting.

I’ve focused on advocating three major policy changes:

1. Target the market forecast.

2. Level targeting.

3. Do “whatever it takes” to achieve the target.

Obviously the Fed is now relying more heavily on market forecasts than in the past. In addition, average inflation targeting is being considered as part of the Fed’s review of its policy regime—that’s sort of like level targeting. So the other major challenge is getting Fed people to think in terms of a “whatever it takes” approach to policy, especially at the zero bound.

This is from a recent speech by Charles Evans, president of the Chicago Fed. I decided to bold the good parts:

In terms of a broad monetary policy strategy, I favor a powerful, full-throated commitment to follow outcome-based monetary policies aimed at achieving maximum employment and symmetric 2 percent inflation within a reasonable time. The best tactics to achieve these outcomes may change over time. For example, at times this approach could prescribe forward guidance with thresholds that need to be met before changing rates. At other times, it could prescribe overshooting our 2 percent inflation objective with momentum. The point is to focus on our objectives—and not on the specific operational tools used to obtain them.

Importantly, in a world where monetary policy is challenged by low equilibrium rates and elevated odds of hitting the ELB, outcome-based policy calls for a relentless focus on our symmetric 2 percent inflation objective throughout the cycle. We have to have a “do-whatever-it-takes” attitude toward policy all the time—in a downturn, when we are constrained by the effective lower bound, as well as in an expansion, if inflation remains stubbornly below our objective.

I recognize and accept that monetary policy will never be a panacea to all the negative shocks hitting the economy. But when it comes to price stability, the monetary authority has the sole responsibility for achieving an inflation objective. For us, that is symmetric 2 percent inflation.

My God! I could have bolded almost the entire quotation. It’s all “good parts”.

My favorite part is where Evans suggests that fiscal policy should play no role in achieving the inflation objective.

Welcome to a new blog on the endlessly perplexing problem of monetary policy. You’ll quickly notice that I am not a natural blogger, yet I feel compelled by recent events to give it a shot. Read more...

My name is Scott Sumner and I have taught economics at Bentley University for the past 27 years. I earned a BA in economics at Wisconsin and a PhD at Chicago. My research has been in the field of monetary economics, particularly the role of the gold standard in the Great Depression. I had just begun research on the relationship between cultural values and neoliberal reforms, when I got pulled back into monetary economics by the current crisis.

""I’m willing to take a big hit to my living standards in order to live in a place that I find beautiful." How much of a hit? I'm currently considering..."

"Justin, you said, "The talk of WWIII with respect to Russia as an instigating factor is Pravda-level propaganda" I agree that it's not Putin's goal to attack NATO, but it..."

"1. The talk of WWIII with respect to Russia as an instigating factor is Pravda-level propaganda. Russia is too weak to enforce its will against Ukraine, the idea that it..."