From the blogosphere

Today I’ll link to some other interesting posts:

1. Market monetarism is not haram

Left Outside has a fascinating post on Iranian monetary policy and the Islamic prohibition on “interest.” Because I’d like to ban discussion of all the “I-words” (interest rates, income, inflation, etc.), his post made me slightly more sympathetic to the Islamic religion.

This is cool! [1] Hassan Rouhani talking about monetary policy? Could I be any more excited? No.

Despite inventing zero, arabs have no use for it, [2] at least not when it comes to central banking. Lending money at interest is haram in Islamic finance so the use of interest rates to control demand as is normal in the west doesn’t apply. So does this also means that unlike in the UK and the US there is no danger of interest rates going to zero and the economy entering the liquidity trap?

. . .

Sukuk is also an important concept too. This is similar to a bond in which interest is regularly paid on a principal. However, because riba is haram in Islam it cannot be structured like this. Instead sukuk imply a transfer of ownership and can look like a form of repurchase agreement. You agree to repurchase something at a certain price over a certain period of time. This echoes previous posts of mine of what saving really is. Interest rates are just symbolic, what is really happening is people buying durable things today with an expectation they will be able to sell them on for more in the future. Interest rates are our way of expressing that, Murabahah or Sukuk are another. The latter seems clearer and more honest on the mechanism actually.

(At this point, I do want to point out to all the snooty economists, engineers, mathematicians who mock post-modernism…who’s laughing now?)

. . .

As Lorenzo tells me, actually the Indians invented zero as a concept, the Arabs were miles behind. More here.

PS. When I said I wanted to ban all discussion of “income,” I was referring to the microeconomic concept that includes things like “capital gains,” which are not a part of “national income.”

2. Monetary offset

Yichuan Wang has a really nice Quartz piece on monetary offset. Here’s an excerpt:

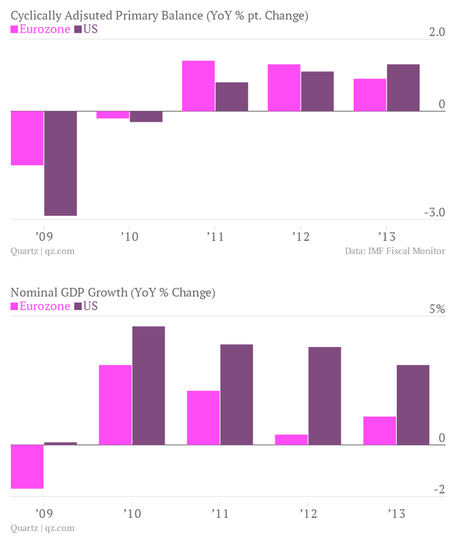

To get an idea of how bad it could have been, one need only look to the Euro zone. As measured by changes in Cyclically Adjusted Primary Balances, a measure of whether of government spending that adjusts for the business cycle, both the US and Europe have endured savage government austerity. Yet nominal GDP growth in the US has been steady while Europe’s has collapsed.

The biggest difference? Monetary policy. While the Fed been a proponent of holding down interest rates throughout the recovery, the European Central Bank actually raised rates in response to inflation fears in 2011, and just recently lowered its benchmark interest rates to 0.25%.

This experience has also shown that deleveraging isn’t a roadblock to monetary policy. From the peak of the crisis, the ratio of household liabilities to annual consumption fell around 26 percentage points from its peak of 1.44 in the second quarter of 2004. Theoretically, this should have meant that the drawdown in federal spending should have been a double whammy””both by directly lowering spending as well as hurting balance sheets. Yet the recovery barely budged, showing that even when people are paying down their debts, monetary policy can still help.This experience has also shown that deleveraging isn’t a roadblock to monetary policy. From the peak of the crisis, the ratio of household liabilities to annual consumption fell around 26 percentage points from its peak of 1.44 in the second quarter of 2004. Theoretically, this should have meant that the drawdown in federal spending should have been a double whammy””both by directly lowering spending as well as hurting balance sheets. Yet the recovery barely budged, showing that even when people are paying down their debts, monetary policy can still help.

3. Are the Obamacare cost controls “good deflation?”

Greg Ip has an interesting piece at Free Exchange:

Therefore, a decline in the price of health services may help consumers at the expense of producers. Ordinarily, this would not be a macroeconomic issue. But it is when inflation is already too low, in which case this deceleration in prices is potentially bad.

I say “potentially” because in some circumstances, lower prices are a net positive for the economy. For example, higher productivity would enable providers to lower prices with no loss of income. Obamacare contains many incentives to raise efficiency, such as penalizing hospitals for high readmission rates, but there’s little evidence productivity as a whole has risen enough to tip the overall trend. Most of Obamacare’s impact on spending has been through brute reduction in payments: to Medicare Advantage plans and to hospitals who treat Medicare patients. The Administration hopes providers will cope with lower payments by finding new efficiencies; but they may instead simply accept lower profit margins, though over time that could drive providers out of the market, reducing supply; or they may negotiate lower input costs. And since health care is labour intensive, that means wages.

At first glance he seems to be assuming that all deflation is demand-side deflation, and hence contractionary. On closer inspection he does draw a distinction between productivity improvements that leave NGDP unchanged and fiscal austerity that reduces Medicare/Medicaid reimbursement.

In my view this sort of reduction in transfers (lower reimbursements) is either a wash, or slightly expansionary. If the Fed targets NGDP then lower inflation means higher RGDP. If the Fed targets inflation then more aggregate supply is expansionary. The question is whether or not a reduction in Medicare reimbursements boosts AS. I.e., whether or not it is a nominal wage cut, when wages are sticky. I think so, but am not certain.

I am indebted to Michael Darda and Saturos for pointing me toward the issues raised by Greg Ip’s post.

4. Reading between the lines

When reading financial articles always try to think about what you are reading from a monetary policy/expectations perspective. Here’s a great example from the FT:

“The signal from the Federal Reserve is driving home the point that ‘tapering’ is not tightening,” says Marc Chandler, strategist at Brown Brothers Harriman. “This seems to imply a willingness to see curve steepening, where the long-end retreats some, but that the short-end does not bring forward a Fed Funds rate hike.”

Translation: Effective monetary stimulus will lead to higher long-term rates. The key is to make sure those long-term rate increases reflect the impact of policy on growth, and not monetary tightening. You do that by committing to hold short rates low for an extended period, or better yet until certain macro benchmarks are met.

As recently as late September, with benchmark 10-year US government bonds yielding 3 per cent, the Fed was forced to rule out a widely expected taper as financial conditions had tightened too much, pressuring housing and the economy. A key test is whether forward guidance can keep equities and other asset markets buoyant once the taper is imminent.

“Long-term yields are always central to any measure of financial conditions, but if the mix of other variables such as equities, front end yields and the dollar are behaving, then it’s less of an issue to see a higher 10-year yield,” says Mr Ruskin.

Translation: Effective monetary stimulus will lead to higher long-term rates. The key is to make sure those long-term rate increases reflect the growth impact of policy, and not monetary tightening. That’s why you focus on other asset markets like equities and forex rates. If equity prices are falling and the currency is strengthening, then the higher rates may reflect tighter money. As always, an NGDP futures market would be a HUGE help. The Fed’s failure to create and subsidize trading in a NGDP prediction market represents inexcusable laziness on their part.

5. Fed misinformation (no pun intended)

I strongly recommend everyone look at this video of George Selgin’s informative and highly entertaining demolition of Fed misinformation on the history of American banking. I also spoke at the same Cato event, but George was the star of the show.

6. All hail Mark Carney

Travis sent me the following:

Mark Carney is moving the Bank of England in a direction it hasn’t taken in more than six years.

The governor took steps yesterday to head off a potential housing bubble by diluting a credit-boosting program, two weeks after raising growth forecasts and signaling interest rates might increase sooner than previously projected.

. . .

Carney’s measures coincide with evidence that demand and prices are rising. Lenders granted 67,701 mortgages in October, the most since February 2008, the BOE said today. Home values increased 0.6 percent in November, Nationwide Building Society said. They climbed 6.5 percent from a year earlier, the fastest pace since July 2010.

For economists at HSBC Holdings Plc (HSBA) and ING Bank NV, the measures may allow the BOE to keep interest rates lower for longer. That’s because the action by its Financial Policy Committee shows it can use macro-prudential tools to target specific problems in the economy.

“Today’s report is not particularly hawkish,” said Simon Wells, an economist at HSBC in London. “The BOE wants to use new macro-prudential tools to calm the housing market, rather than deploy the blunt instrument of higher interest rates.”

Carney has said he won’t consider raising rates until there is sustainable economic growth. He said yesterday the housing curbs will help him keep that pledge.

That’s right, use monetary policy for NGDP and more targeted policies for housing distortions.

7. The wisdom of Paul Krugman

Simple doesn’t mean stupid. Thinking that it does, does.

Tags:

30. November 2013 at 08:40

George Selgin’s speaking style eerily reminds me of Milton Friedman; is this a coincidence?

30. November 2013 at 08:53

If as Selgin says “the claims of Fed independence are much exaggerated” then doesn’t that suggest that the real job is to educate Obama, more than the economists?

30. November 2013 at 09:04

Saturos, Yes, that would be an implication, but I feel they are fairly independent.

30. November 2013 at 09:26

Looking at your speech, once again, it would help if you used the term “nominal spending” more than nominal GDP, as the former makes people think of money supply and demand whilst the latter seems like you’re making tautological claims about real gdp + inflation… But I guess you’re too associated with NGDP by now for those who know you.

30. November 2013 at 09:28

Most people just don’t get that NGDP is a purely nominal quantity.

30. November 2013 at 09:33

Musical chairs model is similarly unclear: holding the price level and nominal wages constant, if we see NGDP and unemployment move together, is that because there is “less NGDP to pay works” or couldn’t it just as easily because a “real shock” has thrown workers out of the economy and then of course NGDP, which is merely RGDP plus inflation, falls too, because inflation is just a separate thing which the Fed controls and has chosen to hold constant?

30. November 2013 at 10:00

LOL to the Q&A after Scott’s speech though. Simply LOL. ROFL, even.

30. November 2013 at 11:00

What would Thanksgiving be without a little schadenfreude. Emmanuel Saez discovers that high tax rates are defeated by labor mobility;

http://www.nber.org/papers/w16545.pdf?new_window=1

‘…we find that location elasticities are largest at the top of the ability distribution and negative at the bottom due to ability sorting effects, and that cross-tax location elasticities between foreign and domestic players are negative due to displacement effects. To our knowledge, the paper provides for the first time compelling evidence of a link between taxation and international migration. As shown in the case of Denmark, football players are likely to be a particularly mobile segment of the labor market, and our study therefore provides an upper bound on the migration response for the labor market as a whole. The upper bound we find is large, suggesting that mobility could be an important constraint on tax progressivity.’

All is not lost though; he suggests making it up on the volume of lower skilled, home grown players without options like Beckham.

30. November 2013 at 11:34

The Fed, since the 1980s, has been plenty independent. Indeed, the independence of the world’s major central banks—BoJ, ECB and Fed—first resulted in a secular decline in inflation, but is now resulting in monetary asphyxiation. A fascinating topic is how central bank economic staffs became influential in monetary policy circles and the rising prestige of Fed regional bank economic staffs…

30. November 2013 at 16:38

Saturos, You said:

“Musical chairs model is similarly unclear: holding the price level and nominal wages constant, if we see NGDP and unemployment move together, is that because there is “less NGDP to pay works” or couldn’t it just as easily because a “real shock” has thrown workers out of the economy and then of course NGDP, which is merely RGDP plus inflation, falls too, because inflation is just a separate thing which the Fed controls and has chosen to hold constant?”

Possible, what what sort of “real shock” would cause unemployment to suddenly double between 2008 and 2009? In addition, there have been previous falls in NGDP that we know were caused by contractionary monetary policies, so Occam’s razor suggests . . .

But I see your point. The musical chairs model is for people who already understand that demand shocks matter. For those who don’t, well God bless them.

And of course inflation is just a number concocted by a bunch of government bureaucrats—not even clear what it is supposed to measure.

Thanks for the link Patrick.

30. November 2013 at 18:04

Benjamin Cole’s remark concerning what I had to say about the Fed’s independence neglects the point (which I actually did squeeze into my 15 minute talk) that it was only thanks to public disgust with high inflation, and the support of government leaders who responded to it (Carter, Reagan and Thatcher among them), that central bankers were able to take steps to reign in inflation. The broad postwar record makes it perfectly plain that central bankers generally did only what the executive either let or encouraged them to do. (Martin and Burns were particularly candid about this.) My forthcoming paper supplies the details and sources.

30. November 2013 at 19:12

“That’s right, use monetary policy for NGDP and more targeted policies for housing distortions.”

Scott, what’s the different between a “distortion” and a “bubble”.

I would again reiterate my suggestion that the ability of a CB to flexibly set minimum and maximum asset/equity ratios by asset class for banks would be a useful policy tool.

1. December 2013 at 02:05

Actually I think that even Keynesians, such as people at the Financial Times, were having trouble understanding market monetarism because they thought that NGDP was just a composite of a real variable RGDP and a nominal variable P, the latter being what the Fed actually controls via interest rates and affecting Y via a circuitous route. “Previous falls in NGDP caused by interest rates” to a Keynesian intuition sounds like falls in P due to falls in AD (which is not NGDP but “effective demand”) which affects Y via a circuitous route. Hence people like Krugman saying that NGDP targeting is just a sneaky way to get the central bank to be looser on P by targeting the real-nominal composite “NGDP” when the real variable Y which they don’t directly control is being intransigently low.

1. December 2013 at 06:40

Saturos, There may be some people who don’t understand that M affects AD, but Krugman certainly is not one of them. He understands that AD affects Y directly.

As far as “composites,” RGDP is just a composite of goods production and services production, whereas P is just a composite of goods prices and services prices. Does that make them less interesting than the individual components?

dtoh, A distortion would be caused by a bad government policy, a bubble might not be. In this case the original policy was bad, so eliminating it is a no-brainer.

1. December 2013 at 07:21

Scott,

So now your view on bubbles is much more understandable. Got it.

And….just think of all the possibilities for the Fed to fix bad government policies if they could set asset/equity ratios for banks by asset class. Government subsidizes student loans > Fed requires 100% equity against all student loans. Gov’t gives a tax break to Hollywood > Fed jacks up the equity requirement for film financing. Government gives grants to economists for research > Fed requires 200% equity against all mortgage loans for houses in which economists live.

The possibilities are endless.

1. December 2013 at 17:48

George Selgin—

I hope you are still reading this post…I will post something soon on Marcus Nunes blog…I hope you read it mostly because I always put some jokes in my posts but also for the perspective that the Fed has come to dominate monetary economics…also, what about Volcker? He drove the Reaganauts crazy….PS even tho we disagree I enjoy your writing…

1. December 2013 at 19:28

Benjamin, I’m still reading and I will look out for your remarks on Marcus’s blog.