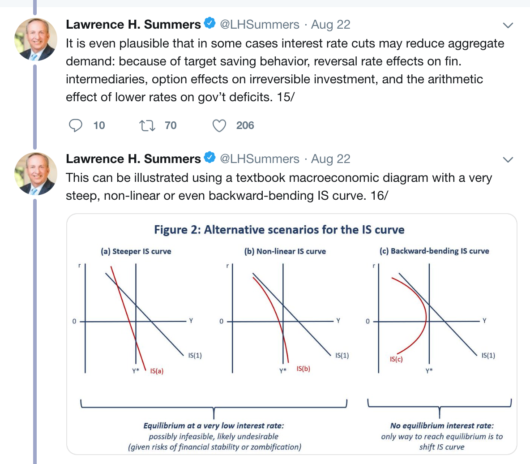

Larry Summers always has interesting things to say, and his new twitter thread on the current state of monetary policy is no exception. He begins with an argument made by many other economists, that low rates imply central banks have less ammunition. He goes on to argue that this casts doubt on the proposition that central banks can create inflation.

In my view, this gets things exactly backward, confusing cause and effect. The low rates are partly the result of contractionary monetary policies. Places with expansionary monetary policy have absolutely no difficulty keeping interest rates well above zero, and creating as much inflation as they wish.

Economists look at central banks that seem to have already done a lot, and have still fallen short, and then ask how much more they would have to do to get higher inflation. The actual answer is “much less”. Interest rates are not (primarily) a policy tool, they are an outcome. A more expansionary policy will lead to higher rates over time. A more expansionary policy will lead to a smaller central bank balance sheet as a share of GDP.

Because of this confusion, people are again calling for “helicopter drops” as if that will somehow “solve the problem”. But the Japanese tried that for many years, and the deflation ended only after they stopped doing a combined fiscal/monetary expansion. As David Beckworth points out, helicopter drops only work if the injections are expected to be permanent. But if helicopter drops were expected to be permanent, then monetary policy alone would work just fine.

The profession is finally beginning to reach the point that monetarists like Friedman reached decades ago—low rates don’t mean easy money. But instead of ending the practice of reasoning from a price change, they either wildly swing over to NeoFisherian (another form of reasoning from a price change), or they start adding epicycles to the flawed Keynesian model:

Summers talks about “interest rate cuts” without explaining what causes the interest rates to fall. The liquidity effect? The income effect? The Fisher effect?

This is so frustrating. Instead of looking for ever more convoluted explanations for why low rates don’t “work” in Europe and Japan, how about we do what we teach out students to do in EC101, and stop reasoning from a price change.

And while we are at it, stop reasoning from a quantity change. Stop suggesting that low unemployment should cause high inflation.

I am currently making my eighth trip to Beijing, 25 years after my first trip. In my previous seven trips I visited as a middle-aged man, and now I’m an old man. If you are an old guy considering your first trip to Asia, I’d suggest Japan.

While China is not an easy country for a foreigner to travel in, it is full of interest. And for the locals it’s definitely getting better. I expected the old people I spoke with to grouse about how much better things used to be (as old people do), but instead they were as enthused as Silicon Valley millennials gushing about their newest toy. “We Chat is so easy to use.” “You can get things delivered right to your door.” “There are many more trees in Beijing and you are again seeing animal life, especially birds.” “There are so many subway lines now.”

It’s been 7 years since I was last in Beijing, and the city has changed about as much as I would have expected. I am staying with in-laws in an apartment in the university district (Haidian). From the front door I see this in one direction:

These are kind of depressing looking apartment buildings, as you’d see in middle income countries. But don’t be fooled; the units are extremely expensive. (Roughly $10,000 per sq. meter, I believe.) It’s in an area with good schools, which is gold.

Turning in a different direction from the exact same spot, you see a typical high income country apartment complex (much more expensive), where my mother-in-law lives. The price/monthly rent ratios are insanely high (maybe 1000X?) as the Chinese prefer to own property.

This summarizes modern Beijing. Today, it’s basically a 1st world city, with lots of legacy buildings from earlier decades that look more like what you see in a developing country. But the proportion of modern buildings is significantly higher than in 2012.

Update: That’s not to say there aren’t still plenty of “middle-income country” neighborhoods, especially in outlying suburbs.

I find it hard to compare Beijing with cities in developed countries, as it’s always “apples and oranges”. Beijing is often very messy looking, and with your eyes closed it smells like a developing country. They seem to want to build lots of things quickly, without much thought to the detailed amenities that the Japanese are so good at. But it’s also pretty high tech, with the “We Chat” payments system being more advanced than American payments.

There’s also a huge distinction between indoors and outdoors. Where I live in Orange County, both indoors and outdoors are equally “nice.” In Beijing, the outdoors is dirty and messy, while the indoors are often the other extreme, especially in newer places. If you went from an American department store to one in Beijing, you’d feel like your vision suddenly jumped from 20-30 to 20-20. The white marble floors are polished, the goods are artfully arrayed and so well-illuminated as to appear almost hyperreal. In the inside, Beijing seems almost an order of magnitude more economically advanced than the street scenes.

Like many Asian cities, Beijing is a nightmare for pedestrians. But they are now developing European-style neighborhoods like Dashilan, which goes under the acronym “FUN”. This area has the most impressive Starbucks I’ve ever seen (including lots of alcohol drinks, although I tried a citrus iced coffee with ice cream for $10), and a really neat bookstore. Sebastian Edwards will be pleased to note that his book on the gold clause Supreme Court case was prominently displayed, but alas, no “Midas Paradox.” Overall, it had a nice mix of restored old buildings, fake old buildings, and ultra-modern buildings.

Ironically, “globalization” is making China turn from soulless western corporate monstrosities to quaint, 19th century-style, walkable Chinese neighborhoods. The Chinese travel to Europe, and then want to create the same thing at home. (Recall the T.S. Eliot line about seeing home again for the first time.)

Overall, it remains a mostly unattractive city on the outside, but with many places of high interest. The historical places have been nicely restored. (Fortunately, Asians care less about “authenticity”.) Unfortunately, right now those famous places are overrun with tourists. The Chinese tourists now completely dominate western tourists, perhaps by 100 to 1. I gather that tourist overcrowding is becoming a big issue all over the world.

Don’t be misled by the $10 coffee I cited. Two days ago, I bought an egg McMuffin and a cup of coffee for a total of 8 yuan at McDonalds. That’s about $1.12. Beijing is still very cheap; 42 cents for subway trips up to 6km and $2 taxi rides. In PPP terms this is relatively high income place. BTW, I only do stupid things like visiting McDonalds when out alone; with my family we go to spectacular Yunnan restaurants. China still has great food at very good prices. Later I’ll get my hair cut at the place I always go to, which I use to estimate PPP. It was $1.20 in 1994 and $4 in 2012. I predict $6.

Soon after I got off the plane I sensed that the western articles about the “social credit” system were probably misleading. China’s too vast and messy for the government to pay much attention to ordinary people. Yes, they can monitor you via your We Chat purchases if they choose, but so can our NSA. China’s government is a big problem if you are an activist on controversial issues (or a Muslim in Xinjiang), but otherwise I suspect it’s not really a 1984-type society for most people.

So far, the air has been unusually clear (see picture above), but of course there are still plenty of bad days (especially in winter). September and October are the best time to visit. I see lots of “e-bikes” and “e-scooters”, indeed most of them now seem to be electronic, not gas powered. So there’s a real effort in Beijing to reduce pollution (including noise pollution; these scooters are really quiet.) I believe the air will be much clearer in 20 years.

Later, we plan to visit relatively poor Guizhou, which will be an interesting contrast. But even Guizhou has spectacular infrastructure:

Infrastructure investment in Guizhou has grown 20 per cent annually over the past five years with the state adding high-speed railways, nearly half of the world’s 100 tallest bridges and a motorway network to rival France’s.

PS. The Chinese property market is complex. Many “owners” in the building where I am staying do not have the legal right to sell their unit, but can rent it out and can also bequeath it to their children. The public spaces (halls and elevators) in buildings with $1 and $2 million condos aren’t much better than what you’d see in a public housing project in Chicago. But the condo fee is only about $50/month.

PPS. China is now quite unequal, but in death there is still a lot of egalitarianism. In a large cemetery that we visited almost all the tombstones were the same size and shape.

PPPS. Lots of Chinese people ask to have their picture taken with my daughter. No one asks for a picture with me.

As well as uncertainty over the U.S.-China trade war, [Goldman Sachs economists Jan Hatzius and Sven Jari Stehn] rationalize their call by arguing the central bank is in a “hall of mirrors” in which officials place greater weight on bond-market pricing when making decisions than historically.

That’s because policy makers “worry more about the consequence of disappointing market expectations for cuts and partly because some of them put a significant amount of weight on bond-market signals (such as the slope of the yield curve and breakeven inflation) in gauging the outlook for growth and inflation,” according to the report.

The result is a “positive feedback loop” as bond traders push for looser monetary policy which prompts a more dovish central bank, they said, adding that the pattern only ceases when economic data suggest further easing is inappropriate.

The hall of mirrors is what Bernanke and Woodford (1997) called the “circularity problem”. The central banker looks at asset prices for guidance, and the asset markets set prices in anticipation of how the Fed will respond to those prices.

Note that Bloomberg says that “bond traders push for looser monetary policy”, when in fact they don’t “push”, they predict the Fed will want to lower rates in the future. Markets still get no respect; they are seen as bullies.

If Goldman Sachs believes the Fed is becoming more market monetarist, then that’s a good sign. But in my view the Fed still pays far too little attention to market forecasts.

In other news, I have a piece in the Washington Post that defends Trump from charges that he would be to blame for a 2020 recession. Some of my commenters (George, etc.) could only dream of writing such an unbiased piece.

Update: Also check out David Beckworth’s piece on the strong dollar, at National Review.

Speaking of unbiased people, Tyler Cowen is also skeptical of all this talk of a recession:

Do note, however, that I am not currently expecting a recession, I just don’t see enough pointers in that direction, and furthermore most of the time recessions do not happen.

That’s why you might never see me predict a recession until it has already begun. My goal here is to promote monetary regimes that sharply reduce the number of recessions, not to create magic formulas to predict them.

It’s hard to read here, but if you go to the link and click on the graph, you’ll see a much bigger version.

There are some technical issues with its construction, which are discussed in the article. But when I looked at the raw data it seems plausible to me that the yield curve really was inverted during most of the 40 years before WWI.

Tyler Cowen has an excellent Bloomberg piece on China, entitled “What if Everyone’s Wrong About China.” Here’s one observation:

It was also conventional wisdom, circa 2010, that China was due for an economic crack-up. That didn’t happen, either.”

Well, not everyone was wrong about that! In fairness, I didn’t expect China to turn in a more authoritarian direction during the 21st century, so I was wrong about that. But then I didn’t expect that to happen in Russia either. Or in India. Or Turkey. Or Hungary. Or Brazil. Or the Philippines. And of course I didn’t expect Trump. So I missed the entire global turn toward authoritarian nationalism.

Tyler asks us to consider whether the now fashionable pessimism about prospects for Chinese democracy will also prove to be wrong. I certainly expect so. Pundits are always excessively swayed by current trends. In 2015 and 2016, I recall reading all sorts of left leaning pundits telling us about Obama’s enduring legacy.

Here’s Tyler:

Or consider Hong Kong. Not long ago it was practically a cliché that Hong Kong was a territory of apathetic, spoiled wealthy people, not very committed to self-rule or democracy. That too has been shown to be false, as 1.7 million people took the risk of participating last weekend in a peaceful anti-government march.

I don’t know if I ever posted on that point, but I certainly did argue against the more general claim that East Asians were not interested in democracy, citing hotly contested elections in places like Taiwan and South Korea—areas that pundits used to tell us would never be democratic. Of course Taiwan is 98% Han Chinese. So Hong Kong doesn’t surprise me at all. Actually, Mainland China has thousands of demonstrations each year, mostly focused on local grievances. This is nothing new.

I also recall being told that certain Latin American dictators were “popular”, only to find out that they weren’t so popular when they finally did have elections.

I still think Fukuyama’s “End of History”, or utilitarianism, or liberalism, or democratic capitalism, or whatever you want to call it, is the megatrend, and all these forays into socialism, nationalism, etc. are mere epicycles. Democracy seemed to be dying in the 1930s, and in the 1980s not many predicted the collapse of the Soviet Union.

Here’s something I’m really confident in predicting:

In one hundred years, either China and Russia will be democratic or the US and UK and Japan will be nondemocratic. Two completely different political regimes in these big countries is not a long run equilibrium. In one hundred years, democracy will be seen as clearly the way to go, or clearly not the way to go. Here’s another prediction. The US/China trade war will eventually be seen as being just as misguided as the Japan-bashing of the 1980s now seems.

Welcome to a new blog on the endlessly perplexing problem of monetary policy. You’ll quickly notice that I am not a natural blogger, yet I feel compelled by recent events to give it a shot. Read more...

My name is Scott Sumner and I have taught economics at Bentley University for the past 27 years. I earned a BA in economics at Wisconsin and a PhD at Chicago. My research has been in the field of monetary economics, particularly the role of the gold standard in the Great Depression. I had just begun research on the relationship between cultural values and neoliberal reforms, when I got pulled back into monetary economics by the current crisis.

"Because the distributed lag effect of monetary flows, the proxy for inflation, is 24 months, the FED can tighten N-gDp after two consecutive quarters of greater than 5% growth rates?"

"Because the distributed lag effect of monetary flows, the proxy for inflation, is 24 months, the FED can tighten N-gDp after two consecutive quarters of greater than 5% growth rates?"

"Looking at the one-year rate of change in total reserves you see why stocks and commodities have recently risen. But that is only available since February. I.e., the FED eschews..."