I just listened to a very interesting Macro Musings podcast—with David Beckworth interviewing Tyler Cowen. Tyler sees the Fed passivity during the last decade as part of a broader increase in risk aversion across American society, part of what he calls the rise in complacency. I like that hypothesis, and look forward to reading his new book on my vacation next week.

I’m less convinced by his argument that this also explains the public’s obsession with low inflation, and refusal to contemplate NGDP targeting. I would argue that the public is not opposed to NGDP targeting, indeed they’ve never even heard of the idea. So let’s try to disentangle what Tyler had in mind in his comments on this subject:

1. The public might prefer the specific policy of inflation targeting to the specific policy of NGDP targeting.

2. The public might prefer the outcome (in terms of economic performance) of inflation targeting over the outcome produced by NGDP targeting.

The first interpretation is a complete nonstarter. If you asked the average American to discuss strict inflation targeting, flexible inflation targeting, symmetric inflation targeting, asymmetric targeting, growth rate targeting, level targeting, etc., you’d produce a glazed look on their faces. And even that understates the problem. Most people only understand the concept of supply side inflation; they have absolutely no understanding of demand side inflation. Hence they think inflation is bad because it lowers their real income, but that’s only true of supply side inflation. Even worse, the Fed only controls demand side inflation, so Fed policy has no impact on the only kind of inflation the public understands. I used to ask my class whether the cost of living had actually increased if both wages and prices rose by exactly 10%. And over 95% always got it wrong, claiming that the cost of living had not actually increased. (Actually, it rose by 10%.)

And even that understates the problem, because very few Americans even understand that the Fed can choose between 2% and 4% trend inflation like someone choosing between massaman curry and pad thai for their entree. They don’t know that that is what the Fed does. How many Americans know that the Fed’s tight money caused the Great Recession?

So I’m going to assume that what Tyler meant was that Americans would be happier with the outcome of inflation targeting as compared to the outcome of NGDP targeting. I doubt that. People might say they prefer 0% inflation to 2% inflation, but I doubt that they’d say they prefer America’s 2009 economy to its 2007 economy. But the 2009 economy is what you get when you reduce inflation to 0%. Actually, we were much closer to NGDP targeting in the period before 2007 than in the years immediately after 2007. And yet Americans seemed much more unhappy with the post-2007 economy. Now of course it’s entirely possible that if the Fed had kept NGDP growing at 5% after 2007, the public would have been even angrier than they were with the actual policy (a fall of 3% in NGDP between mid 2008 and mid-2009.) But I doubt it. I think they would have been a bit disgruntled by the stagflation, but nothing more.

Both David and Tyler believe that the Fed now views 2% inflation as a ceiling, not a symmetrical target. I’m still not convinced; let’s look at this again in 10 years. If it’s still a ceiling, I’ll throw in the towel. It was clearly a symmetrical target before 2007—why would the Fed have suddenly changed?

PS. David and Tyler also discussed the declining rate of innovation in the arts. Here’s a quote from a different Tyler Cowen interview:

If you think about Renaissance Florence, at its peak, its population, arguably, was between 60,000 and 80,000 people. And there were surrounding areas; you could debate the number. But they had some really quite remarkable achievements that have stood the test of time and lasted, and today have very high market value. Now, in very naive theories of economics, that shouldn’t be possible. People in Renaissance Florence, they didn’t produce a refrigerator that we’re still using or a tech company that we still consult.

But there’s something different about, say, the visual arts, where that was possible, and it was done with small numbers. So there’s something about the inputs to some kinds of production we don’t understand. I would suggest if we’re trying to figure out, like what makes Silicon Valley work, actually, by studying how they did what they did in the Florentine Renaissance is highly important. You learn what are the missing inputs that make for other kinds of miracles.

That’s an interesting point–future generations will be more interested in our art than our technology.

Here’s another question to consider. In the arts, there are periods of rapid innovation (the Renaissance), followed by periods of stasis. In David’s interview, Tyler cites the rapid innovation in pop music during the 1960s, relative to the slower innovation today. Is that different from the observation that explorers no longer discover as many new lands as they did in the heyday of Portuguese and Spanish exploration? Are we less talented at exploration, or are there simply fewer as yet undiscovered lands? Perhaps the analogy is silly, but let’s take it a step further. The discovery of new planets, and the technology that allows us to get there, would presumably lead to another Golden Age of discovery. Doesn’t the invention of new art forms (the novel, film, electronic music, etc.) open up vast new fields for artistic discovery? Isn’t Robert Gordon’s argument that innovation in existing fields has diminishing returns, and that we need to develop entirely new fields to supercharge innovation? Thus we understand the physics of the non-microscopic world so well that it’s getting really hard to radically improve our houses, cars, airplanes, ships and washing machines. The only area of rapid innovation is at the microscopic level (biotech, computer chips, etc.), which opened up only in the past 50 years or so. Gordon doesn’t expect more such fields to open up, and thus predicts diminishing rates of innovation in the fields that we already have. (I’m agnostic on that claim.)

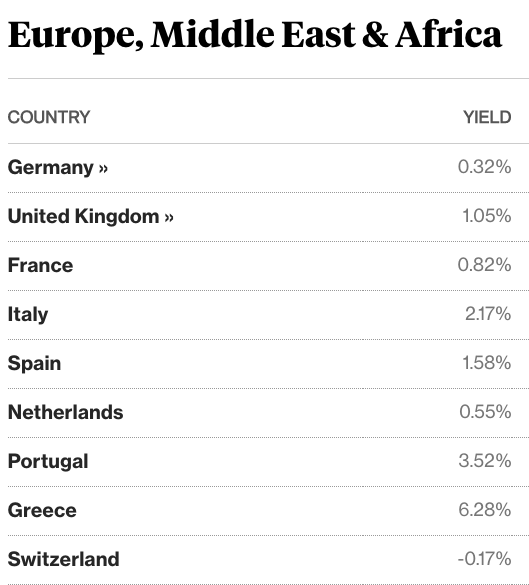

As you can see, Italian 10-year bonds offer considerably higher yields than German, French and Dutch bonds, and even higher yields than Spanish bonds. Italy has a massive public debt (third largest in the world), an economy that has shown almost no growth since 2000, and a very dysfunctional political system (which the voters recently decided not to reform.)

As you can see, Italian 10-year bonds offer considerably higher yields than German, French and Dutch bonds, and even higher yields than Spanish bonds. Italy has a massive public debt (third largest in the world), an economy that has shown almost no growth since 2000, and a very dysfunctional political system (which the voters recently decided not to reform.)