Why Switzerland is such a great country (all’s well that ends well)

The Swiss National Bank did a very foolish thing last month. No, it was not foolish to stop pegging their currency to the euro. Fixed exchange rates are a bad idea. Central banks should target macro aggregates. Instead, the mistake was in letting the Swiss franc (SF) suddenly appreciate by 15% to 18% against the dollar and euro, at a time when Switzerland was experiencing mild deflation. There were two explanations offered, both completely bogus:

1. They feared the euro would depreciate sharply because of QE. Actually the EMH says it’s impossible to predict high frequency currency moves, or alternatively changes in real exchange rates, and hence the SNB was foolish to make that assumption.

2. They feared they’d have to buy lots of foreign assets to maintain the peg, leading to a larger balance sheet. But if it’s a small balance sheet you want then you don’t end the peg with a sharp revaluation, which just makes the SF even more attractive. You end it by devaluing your currency, to make it less attractive. They got things exactly backwards.

The good thing about the Swiss is that they are sensible people, and have mostly undone the damage of that foolish decision. The first thing they did is to start trying to depreciate the Swiss franc by buying foreign assets. Wait a minute, wasn’t that what they were (supposedly) trying to avoid doing by ending the peg? Yes, and it didn’t work. They were right back in the same mess as in mid-2011, before the peg.

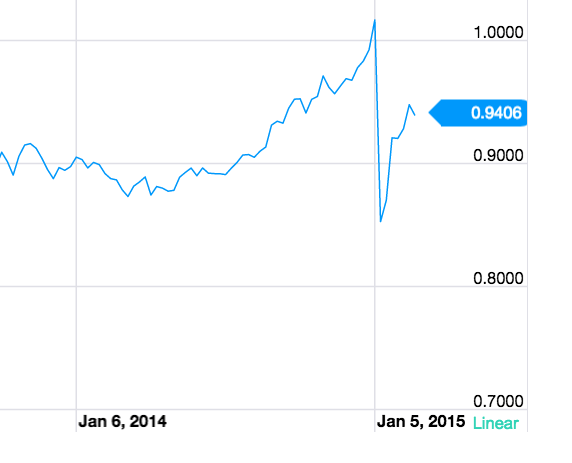

The following graph shows that the SF has fallen from rough parity with the euro after the de-pegging, to about 1.08 SF to the euro today:

And this graph shows that the Swiss stock market, which crashed on the decision that some claimed was “inevitable” (hint, markets NEVER crash on news that is inevitable), has regained most of its losses.

Indeed the recovery is even a bit more impressive than the recent fall in the SF. Why is that?

Obviously it’s partly because global markets have rallied with the Greece agreement. But it also reflects the recent fall in the euro against the US dollar. When the Swiss first pegged to the euro in September 2011 it traded at about $1.35 to $1.40/euro. It was still in that range in the first half of 2014. Today the euro trades at $1.13/euro. That means the SF has actually depreciated against the dollar in recent years. In trade-weighted terms the SF is probably up slightly, but less than the euro/SF exchange rate might suggest, and indeed far less than even a month ago. Here is the value of the dollar in terms of SF.

Given that the Swiss economy was doing fine a year ago at a euro/SF exchange rate about 10% lower than today and a dollar/SF exchange rate about 5% higher, it’s not surprising that stocks have recovered much of their losses, although they remain modestly below the levels of right before the float.

When the Swiss made this foolish decision I suggested that a revaluation of something like 5% might be defensible, but not the 15% to 18% revaluation that actually occurred. I’m pleased that the Swiss National Bank has seen the light, and that Switzerland has preserved its reputation as one of the best-run economies in the world.

Now they just need to nudge the SF a bit lower, and they’ll be fine.

Tags:

23. February 2015 at 16:36

OK, all well and good. But do not the Swiss people, through their central bank, now own a lot of assets they did not own before? Do not those assets throw off income? Is that not a big positive for the Swiss people?

Or would they have been better off declaring a tax holiday and just printing up Swiss francs to pay the tax man? That would have devalued the Swiss franc also and had real benefits for the average Swiss citizen.

24. February 2015 at 01:27

Dear Scott,

I am probably reading tea leaves here, but you write:

“The first thing they did is to start trying to depreciate the Swiss franc by buying foreign assets.”

Who is “they”? My reading is that you think of the SNB. I agree that there must have been interventions on the day of the announcement given how the rate suddenly flattened around parity.

However, since then presumably Swiss non-central bankers have undone some of the damage, no? European assets just got absurdly cheap. Or do private actors have too little weight in this game?

I also wondered if the ECB’s move has decreased safe haven demand more generally. Gold has lost around 7 percent since the ECB’s move as well. It was on a two month winning streak before that.

The SF and the Swiss stock exchange turned around with the ECB announcement. They were volatile but essentially flat in the week between the SNB and ECB announcements. Negative rates of .75 came into effect that day, too, but were obviously expected.

The SNB statistics for January will be released a month from now. Yesterday’s latest release shows an increase of 8% (SF 500 -> 540bn) in foreign reserves for December 2014. They hinted that they had bought another SF 50bn in January prior to the move.

24. February 2015 at 01:35

P.S. context for the last bit: the SF 500bn reserves were rouhgly the volume held ever since summer 2012. Hence the sense of urgency at the SNB.

24. February 2015 at 02:05

“Or do private actors have too little weight in this game?”

Those were exactly my thoughts when I read this. I remember commenting at the time the SNB would intervene to not let it go lower, but I commented the arbs were now rediculous.

It’s those arbs trying to close, by themselves, that should be moving the Swiss Franc back down. I know if I were in Geneve, I would be doing my grocery shopping in France. I myself book Christmas trips way in advance and just booked Lech instead of Switzerland. Really makes no difference to me but yet it was just such a ridiculous difference to Switzerland last month, booking Swiss just looked stupid fat priced.

The omnipotent CB, without whom nothing can move. Ya gotta be kidding me!

24. February 2015 at 02:24

Good to see the good professor recognizes the volatility and short term irrationality of markets. I hope he sees that a NGDP futures market will be as volatile, with damning implications for his NGDPLT proposal.

24. February 2015 at 05:00

“Good to see the good professor recognizes the volatility and short term irrationality of markets.”

No, he specifically insisted to me that markets are completely rational.

NGDP market would be pinned so it would have no volatility with the exception of instantaneous volatility on settlement date.

Insignificant questions really, when one realizes there are perfect winds today… time for some kitesurfing!!

24. February 2015 at 05:37

Johannes, You said:

“I agree that there must have been interventions on the day of the announcement given how the rate suddenly flattened around parity.”

Actually I meant just the opposite. I was not assuming interventions that day, but in the period since, which drove the SF down to 1.08. This is just based on press reports of intervention, no hard data.

Derivs, You said:

“No, he specifically insisted to me that markets are completely rational.”

I’m afraid Ray always gets things exactly backwards. He can’t help it.

24. February 2015 at 08:18

What is the last chart? I’m guessing a trade-weighted exchange rate for the SF, but a label or title or something like that would be very helpful. Good post

24. February 2015 at 08:51

First time poster here (although I have read the blog for about 2 years), and I am a recent college grad so go easy on my a little bit! I was an accounting, finance, and economics major in undergrad, and I think NGDP targeting is an interesting idea. I asked my financial derivatives professor (http://kelley.iu.edu/facultyglobal/directory/FacultyProfile.cfm?netid=zw25) about NGDP targeting and this was the interesting back and forth we had via email:

Me: “From your experiences working for the Fed, do you believe that the primary purpose of the Fed is to stabilize nominal GDP growth? If so, would creating a Nominal GDP Futures market and allowing the Fed to use this market to target the nominal GDP growth rate be better Fed policy than interest rate targeting?”

Professor: “In fact, such derivatives were created and traded for a while. The market was created in 2002 as a way for institutional traders to hedge risk or profit from economic data. Auctions of such derivatives were conducted in Chicago Mercantile Exchange and International Securities Exchange prior to the release of non-farm payrolls, the consumer price index, retail sales, and weekly initial jobless claims reports.

In 2005, Goldman Sachs and Chicago Mercantile Exchange announced that they partnered to enhance the auctions for economic derivatives, based on key U.S. and European economic indicators, through integrated clearing and trading solutions. The partnership extended to other financial products the auction framework that Goldman Sachs had been applying in derivatives markets since 2002.

On each day of 2006, NY Fed staff extracted the expectations of economic indices from these derivatives. For a period when I met with Timothy Geithner (former U.S. Treasury Secretary and then NY Fed President) every week to brief him on financial markets, I often presented to him these derivatives data and market expectations of economic indices extracted from them.

In 2007, however, the Chicago Mercantile Exchange and the International Securities Exchange decided to discontinue economic derivatives auctions. The main reason is the lack of investors’ interests. Low market participation (in the words of CME) made such operations not profitable for the exchanges and market makers like Goldman Sachs. Low market participation also made it more challenging to read the market expectations of economic indices because a huge risk premium and liquidity premium were part of the derivative security prices.

At a time, some researchers were optimistic about the usefulness of such derivatives. The thinking was in line of yours. To see such optimistic thinking, you can read the attached article.

Thank you for bringing up this interesting discussion.”

[He also sent me this link: https://resources.oncourse.iu.edu/access/content/attachment/SP14-BL-BUS-F421-30619/Forums/78d20960-3771-4945-a089-10bb21a3dd85/Economic%20Derivatives.pdf%5D

Another Student: “I read your response of economic derivatives. What is the reason that investors were not interested in this kind of derivatives that they can potentially use to hedge the risk of great economic recession? In other words, what do they prefer to use to hedge such market risk?”

Professor: “This is a good question, but I don’t have facts for the answer.

The exchange and Goldman Sachs didn’t tell people reasons for the lack of interest in these financial products they offered. We can only theorize several possible reasons. For example, (1) the fees are too expensive; (2) the setup of the financial instruments are not very convenient to use; (3) derivatives on macro indices are fundamentally less effective for various hedging purposes; (4) there are ample alternative derivative securities that are tied closely to macro economic news and easy/cheaper to use (fed fund futures, euro dollar futures, treasury futures, and options on these futures, etc.) If (1) and (2) are the reasons, I guess the exchange and GS would not tell the world. If (3) and (4) are the reasons, the exchange and GS made the incorrect judgement originally, which is also something they would keep quiet, I guess.

Bottom line, the exchange and GS have the data and might know the reasons. They simply say investors’ interest is thin but didn’t tell us why. I don’t know the answer either.”

[In my opinion, it doesn’t seem like he actually addressed NGDP targeting, but it was an interesting exchange nonetheless. Nevertheless, I am curious about everyone’s thoughts.]

24. February 2015 at 12:49

Krugman wrote a new column:

http://www.aei.org/publication/krugman-vs-piketty-inequality

My quick take: as long as FDIC/TBTF/Fannie/Freddie exist, then Krugman and Elizabeth Warren are right that we need heavy regulation of Wall Street + redistribution….

24. February 2015 at 15:28

[…] In a new post on Switzerland, Scott Sumner said (my emphasis): […]

24. February 2015 at 16:12

“I’m afraid Ray always gets things exactly backwards. He can’t help it.”

Ah, but his stories of being a 7th dan go champion and having a 14 year old ladyboy concubine can not be beat anywhere on the intertubes. Not even by MF’s explanation, yesterday, that he reached total economic consciousness while tripping out to Jerry jammin Dark Star at the Fillmore East.

24. February 2015 at 16:19

Scott:

Are you aware that Thee Economist magazine has endorsed NGDP level targeting in its February 21-27 issue? See page 14 at the top,right column, under “change the target”.

Holy cow, Batman! It only took 6 years to complete a revolution in thinking about proper conduct of monetary policy.

24. February 2015 at 16:44

Robert, Sorry, I added an explanation. It was the $/SF.

Marginal, Thanks for the info, I do recall that there was little interest in that market. Oddly, that’s actually a good thing as far as NGDP futures targeting is concerned. The problem of liquidity is discussed in my Mercatus paper on futures.

Thanks Travis.

Derivs, Yes, he provides lots of entertainment value.

Thanks Carl, Yes, I did see that.

24. February 2015 at 17:49

Nice

24. February 2015 at 19:27

Mike Darda:

http://www.aei.org/publication/market-monetarist-take-whats-happening-japan-2-charts

“Japan’s green eyeshade recession appears to be over. Despite two quarters of negative GDP associated with last year’s VAT tax hike, Japan’s labor market didn’t miss a beat with unemployment falling to new cycle lows. NGDP growth was not nearly as disturbed by the tax shock as was RGDP, which is exactly what one would expect with an adverse supply side shock. With NGDP growth trending near 2% on a year-to-year basis, Japan should be able to gradually pull out of deflation. Given poor demographics (a falling working age population), Japan may only need 1-2% NGDP growth to it a 2% inflation target over time. We continue to expect steady confidence and sustained NGDP growth to be associated with higher equity prices in 2015.”

24. February 2015 at 20:21

@Marginal Cost Man: excellent points, copied and pasted for future reference, and one reason that the unnamed professor did not mention that advantage of targeting NGDP is that there may be no advantage. Fads in monetarism come and go: for a while, when the Phillips curve was in vogue, the unemployment rate was targeted, then it was M1, M2, then it was interest rates, then it was a ‘plethora’ of factors (Greenspan era). In fact, money is largely neutral, as Fischer Black observed, and, absent Zimbabwe style accelerated printing of money, has no effect on the long term (as in greater than several days) real economy (no sticky wages, and certainly no sticky prices). My fears with Sumner’s NGDPLT is that it might, if taken to the illogical extreme, result in hyperinflation when the bank tries to ‘target’ something but ends up pushing on a string.

@Derivs–you are mendacious. I never said anything like that.

24. February 2015 at 22:27

Illogical extreme indeed. In order to get hyperinflation with NGDP targeting you’d have the Central Bank somehow actually destroying real goods, to truly staggering degrees.

Or, well, someone out there destroying real goods, again by staggering degrees.

I mean, if we go by the standard definition, although it’s arbitrary, to qualify as hyper rather than high inflation, you’d have to have an annualized inflation rate of ~13000% (that’s 50% monthly) So if we take a representative basket of goods the “equivalent number of baskets” of final goods being exchanged has to be dropping at about that same rate, since if you’re actually targeting NGDP at some low growth rate you shouldn’t let it get too high. I don’t know that there’s ever been a recession that bad in the history of planet Earth. Output would be halving every month. What are you concerned about, the extinction of the human race?

25. February 2015 at 00:22

O/T: On the right side of your blog, it shows 4.2% as the answer to “What will be the growth rate of U.S. Nominal GDP in 2015?” But when I go to the Hypermind site, it shows the current average prediction at 3.7%.

Is there an updating problem on your homepage, or are these figures referring to two different predictions?

25. February 2015 at 04:23

“@Derivs-you are mendacious. I never said anything like that.”

Poetic license???? Confused you with Nicholai Hel???

As for S+D and Price…

It is interesting that avg daily volume necessary to fulfill global demand of CL is only about 90,000 fu contracts, that about 1 million fu contracts trade daily in only WTI grade, that the OTC swap market tends to be about 3 times the size of the fu market. So basically physical transactions make up maybe 2% of daily volume. Funds looking at technical charts and thinking about how December support at $55 has now, in February, become massive resistance, are really the ones whose actions are on a day to day basis setting price.

25. February 2015 at 04:35

Scott,

Guess who just said the following:

“During the upward phase of the recovery, monetary policy just doesn’t matter that much”

…

You’ve got a lot of work left to do, Scott.

25. February 2015 at 05:54

Ray, You said:

“Fads in monetarism come and go: for a while, when the Phillips curve was in vogue, the unemployment rate was targeted, then it was M1, M2:”

You came through again! Monetarists favored targeting the unemployment rate?

John, There are a number of NGDP markets, are you sure you have the right one?

SG, I did a post already, I’ll put it up later.

25. February 2015 at 07:00

[…] Source […]

25. February 2015 at 07:35

@Andrew_FL – you are essentially positing the discredited “real bills doctrine” of monetarism, which says the Fed can never destroy wealth if it creates money in response to paper offered by banks that is based on actual customers. The fact the Fed has nearly 44% of its balance sheet in toxic mortgages puts paid to that lie. Either that, or you are not clear about what you are talking about (please explain). Put another way: if the Fed starts offering dollars to buy up kids lemonade stands, as NGDPLT could eventually require, bad things will happen.

@ssumner – are you not an expert on economic theory? “Federal Reserve chair Arthur Burns pushed back: “[The] Humphrey-Hawkins [proposal]… continues the old game of setting a target for the unemployment rate. ”

http://delong.typepad.com/sdj/2009/07/arthur-burns-in-the-1970s.html

See also references to monetary theory in: http://en.wikipedia.org/wiki/Humphrey%E2%80%93Hawkins_Full_Employment_Act

It’s embarrassing to me, much less the people reading this, when the author of this blog is shown to be less than knowledgeable about his area of expertise.

25. February 2015 at 09:32

Ray, Well now that’s even more hilarious—Humphrey Hawkins is now monetarist doctrine? Milton Friedman is rolling over in his grave.

Laughing.

25. February 2015 at 11:30

@Ray Lopez-I am not an advocate of the Real Bills Doctrine. I’m not even a Market Monetarist. But your belief that NGDP targeting could lead to hyper inflation is just loopy.

Hyper inflation requires prices are at least doubling every month. If your NGDP target is being met, if the growth rate of NGDP is close to say, 5% annually, that requires that real output decline, not just at a high rate, but an amazingly high rate! Slightly less than halving every month, in fact. I am not saying nothing bad can happen, I’m saying your scenario is of implausible magnitude.

Could such a thing happen? Only in the event of total civilization collapse, I’d say.

26. February 2015 at 21:29

Re: Hypermind–ok gotcha, the prediction on the main page is for US NGDP growth in Q1, not the full year. Thanks for clearing that up.

27. February 2015 at 05:37

First numbers are in: The SNB lost SF 51.5 billion in equity in January (10% of the balance sheet total), but increased bank sight deposits by the same amount. On the asset side, foreign reserves hardly move in SF terms despite the sharply lower exchange rate.

http://www.snb.ch/en/iabout/stat/statpub/balsnb/stats/balsnb

If sight deposits the thing to go by, the SNB spent SF 10 billion in the week of the decision, did most of its interventions in the week after the floating (SF 40 billion), and added another SF 5 billion in the last week of January.

However, they did not do anything on net in February.

http://www.snb.ch/en/iabout/stat/statpub/impdata/id/statpub_impdata_actual

27. February 2015 at 07:47

Thanks Johannes, That’s very interesting. I am particularly interested in the 16 billion increase in the week that ended on the 19th. It seems plausible to me that most of those occurred after the revaluation, especially given the much larger pace of purchases the following week. Is there anyway to know for sure?