The inflation hawks are so wrong that it’s not even funny anymore

I am constantly annoyed by reading inflation hawks warn that all this so-called “monetary stimulus” will hurt the Germans, or the elderly in Japan, or Americans that save. Meanwhile, in the real world:

Over the past 12 months, inflation has risen just 0.7 percent, the smallest gain since October 2009 and pushing further below the Federal Reserve’s 2 percent target. The index had increased 1.0 percent in the period through March.

Core prices were up 1.1 percent, the smallest rise since March 2011 and slowing from 1.2 percent in March.

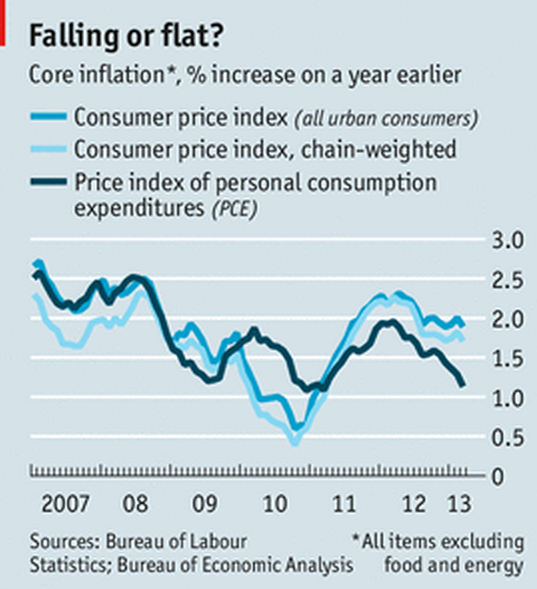

The fact of the matter is that if the Fed did actual monetary stimulus beyond my wildest imagination they’d still be unlikely to get the inflation rate up to their legal mandate for the period from 2008 to 2016. That’s right, inflation will almost certain run under 2% during that 8 year period, even if the Fed does what I want them to do (and money is still too tight.) Take a look at the PCE core rate, which is the one the Fed targets:

Notice that it was above 2% before the recession, and has been consistently below 2% ever since. And yet the Fed’s legal mandate calls for exactly the opposite pattern. They are required to focus on both inflation and employment, which means higher than 2% during periods of high unemployment and vice verse. As George Selgin points out in this video, the rate of inflation should be lower during periods of strong growth than otherwise. (Although George prefers a policy that would lead to a lower average rate of NGDP growth than I prefer.)

In Japan, prices continue to fall despite a massive depreciation of the yen. That means that without Abenomics the rate of deflation would be even greater, as we know that (at a minimum) a sharp currency depreciation will boost import prices.

I really want to pull my hair out when I hear pundits warn of high inflation. All they are doing is discrediting whatever macroeconomic philosophy they espouse. Unfortunately for me, most of the inflation Cassandras (albeit not all) are on the right. They share my views on many other issues. When the high inflation does not happen (and it won’t) their views will be even more discredited than they were after the failure of “austerity” to boost growth in Europe.

The good news is that inflation doesn’t matter, NGDP growth matters. So as long as Abenomics boosts NGDP growth, it really doesn’t matter what happens to inflation.

Prediction: At some point in the next 12 months the ECB will realize that the eurozone NGDP is not going to recover on its own, and they will launch a program of monetary stimulus. The Germans will squeal, but inflation will continue to run BELOW the ECB’s legal mandate. In other words, everyone will claim the Germans are being screwed, whereas the truth will be the exact opposite.

PS. George missed a golden opportunity to point out that there has been a lot of “demand destruction” in both Japan and southern Europe.

PPS. Not only do the Europeans pay no attention to NGDP, but they don’t even report the data. I kid you not. The first quarter NGDP for the eurozone is not yet available, and it’s the last day of May! What are all those bureaucrats in Brussels doing?

PPPS. And of course that means RGDP isn’t really available either; instead some bizarre proxy for RGDP is being reported, as you cannot compute RGDP w/o NGDP.

HT: Lorenz

Tags:

31. May 2013 at 06:42

A minor correction. The Fed does not target core PCE. The Fed targets headline PCE.

Fed’s Longer Run Goals and Policy Strategy (25 January 2012)

“The inflation rate over the longer run is primarily determined by monetary policy, and hence the Committee has the ability to specify a longer-run goal for inflation. The Committee judges that inflation at the rate of 2 percent, as measured by the annual change in the price index for personal consumption expenditures, is most consistent over the longer run with the Federal Reserve’s statutory mandate.”

http://www.federalreserve.gov/newsevents/press/monetary/20120125c.htm

Here’s Bullard explaining why it is headline PCE:

“In a targeting context, inflation refers to headline (rather than core) inflation, Bullard said. The headline PCE price index is targeted, he explained, because “it does not make sense to ignore some inconveniently volatile prices, like those for gasoline and food” (as is the case with core inflation).”

http://www.prnewswire.com/news-releases/st-louis-feds-bullard-discusses-inflation-targeting-us-economy-housing-and-monetary-policy-141254773.html

31. May 2013 at 07:05

“What are all those bureaucrats in Brussels doing”

Does this answer your question:

http://www.guardian.co.uk/world/2013/may/19/eu-banning-olive-oil-jugs-restaurants

31. May 2013 at 07:13

Im really puzzled that prices still dont seem to be rising in Japan. Yes, NGDP growth is what matters, I agree. And RGDP is looking good (so monetary stimulus is definitely worth it). But given that they promised to hit 2% within 2 years I think we should at least be seeing some upward pressure on inflation.

Japanese expectations might be stickier than I presumed.

31. May 2013 at 07:52

Scott, Yes, Short term they target the core, long term the headline. Same result either way.

ChargerCarl, More likely they are just as inept at measuring inflation as we are. The yen depreciation is causing soaring prices for imports like oil and LNG. Domestic prices will be slower to respond.

31. May 2013 at 08:11

Professor Sumner,

What boggles me most is the reporting of RGDP and inflation without NGDP and the complaints that NGDP targeting is impractical because NGDP is too difficult to measure. NGDP is the only one of those three that can be reasonably measured.

31. May 2013 at 08:12

Perhaps somehow that misconception is related to all the misconceptions about inflation.

31. May 2013 at 08:23

There is nothing magical about 2%. I can remember Greenspan talking about this in the 90’s. If he could squeeze inflation to 1% or 0% without upending the rest of the system, I think he would have.

The Fed does not “target” inflation. The may have a goal, but they are not explicit inflation targeters.

To the degree that they do have a goal for inflation, it is next year’s inflation, not last years inflation. Implied inflation in the TIPS market is a little bit below 2%. It has been above 2% as recently as a couple of months ago. But TIPS has been suggesting a higher implied inflation that realized inflation for some time now.

To the degree that the Fed is “falling down” on their employment mandate, employment has been increasing for 36 consecutive months. Unemployment is falling as fast as it ever does.

I hear more from inside the Fed talking about a 2% target in the context that inflation is too low and they are undershooting this target.

I read very few economists talking about fears of high inflation. I hear Rush Limbaugh talk about it, but he is not an economist. Kudlow was talking about runaway inflation a couple of years ago, but he seems to have moderated. At least, he used to be an economist.

31. May 2013 at 08:31

What do you mean, prices are falling in Japan?

inflation was up 0.3% last month and 0.2% the month before that. Abe has only been talking about his monetary stimulus plan for since the beginning of the year. You can’t hold the deflation from the back half of 2012 against him. Since the beginning of the year inflation is on a pace for +1.2%. Perhaps still below Abe’s stated target, but certainly greater than the -1% last year.

31. May 2013 at 08:34

ChargerCarl,

If the Japanese have any sort of spare capacity, shouldn’t the initial effects of an expansion in demand in Japan be primarily on RGDP rather than inflation?

31. May 2013 at 08:37

And that Selgin video is brilliant. His “Less Than Zero” pamphlet is what converted me to mild deflation as the best price trend and soothed many of my doubts about NGDP targeting & free banking. I see that he’s got very good at explaining the underlying theory to a more general audience since LTZ.

31. May 2013 at 08:42

Prof. Sumner,

You wrote:

“In Japan, prices continue to fall despite a massive depreciation of the yen.”

David Glasner wrote a new post about that last night that has me very worried:

http://uneasymoney.com/2013/05/30/is-japan-a-currency-manipulator

31. May 2013 at 08:52

Japanese RGDP growth in Q1 2013 was about 3.5% PA, while prices fell at about 0.5% PA, implying a NGDP growth rate of 3%. Assuming that 1.5% is a reasonable estimation of the rate that Japanese RGDP can consistently grow now (i.e. slightly about the rate over the past 20-odd years) then NGDP in Japan is CURRENTLY on track to meet their 2% target for 2015.

A 2-year lag from an increase in the quantity of broad money to an increase in prices was Friedman’s rule of thumb for the “long and variable lag” between money and inflation.

31. May 2013 at 09:03

Doug M,

Employment is not rising as fast as it ever does; look at recoveries from previous recessions before the low-interest rate period of the past couple decades. Unemployment is not falling particularly quickly, especially considering that the recession ended long ago, and much of the fall in unemployment has been due to reductions in the labor force, not increased employment.

Also, 0% or 1% inflation is not ideal. We do not want 2% inflation because it is easier to hit 2% than 1% but really 1% would be better. Positive inflation has advantages such as helping us avoid the ZLB and easing frictions due to nominal rigidities.

31. May 2013 at 09:16

“Although George prefers a policy that would lead to a lower average rate of NGDP growth than I prefer.”

How many people here realize that the only way Dr. Sumner and Dr. Selgin can settle this dispute is through initiations of force, not reason and respect for property rights?

Dr. Sumner wants to devalue Selgin’s income and put more money in wealth consumption activity by X%, through force, whereas Dr. Selgin wants to devalue Sumner’s income and put more money in wealth consumption activity by Y%, through force.

Whoever can convince the state that their plan is “better” than the other’s, meaning better at promoting the central bank to the public, meaning better at maintaining the central bank’s control over the money, “wins” the dispute. The central bank will reward he who does a better job of this.

31. May 2013 at 09:22

@ Scott N

It´s because of the Bullards that there´s no progress:

http://thefaintofheart.wordpress.com/2011/05/20/from-bullard%C2%B4s-presentation-it-comes-out-that-%E2%80%9Cinflation-targeting-is-rotten%E2%80%9D/

31. May 2013 at 09:22

“The Germans will squeal, but inflation will continue to run BELOW the ECB’s legal mandate. In other words, everyone will claim the Germans are being screwed, whereas the truth will be the exact opposite.”

This is truly warped thinking.

It does not matter what the ECB’s self-imposed law happens to be. If they want 2% or 10%, it does not relate to the fact that inflation will indeed HURT many German’s lives.

It is no argument to reply those who correctly identify how and why their circumstances are worsened, that the institution responsible is acting within or below its own laws. What, would it make any sense to argue that as long as the state kills or spies on fewer than 100 civilians a year, as per law, that there is no justification in (what you churlishly call) “sqealing”?

You’re a socialist, plain and simple. That’s how you think. You think politically. You believe, for some reason, people have no justification in defending their own liberties and economic interests against aggression, as long as that aggression is “legal”. Just step back and think about that one for a moment.

You’re not annoyed because you’re right and they’re wrong. Your’e annoyed because they constantly point out to you the destructive effects of your own advocacies, and the only recourse you have in reply is effectively “It’s the law, deal with it.”

Pathetic.

31. May 2013 at 09:39

I hope your prediction is comes true sooner rather than later.

31. May 2013 at 09:43

Zero consideration for what individual property owners prefer regarding their own property.

It’s all arrogant pretensions of what’s allegedly best for millions of other people, and they have to shut their yapping.

31. May 2013 at 09:52

So are we becoming like Japan? If the Fed is okay with inflation between 0-1% as long as most people have a job, then how is that different than Japan? That is a scary thought.

31. May 2013 at 10:07

I just listened to a Bloomberg interview (from this week!) of William Poole, where he criticized Bernanke for caring too much what markets think, and cited the interest rate cut for January 2008 as a mistake because it was a reaction to a rogue trader at SocGen.

31. May 2013 at 10:08

P.S. I bet if we adopted NGDP targeting, some inflation hawk would observe that growth is higher whenever inflation is lower and conclude we should aim for lower inflation.

31. May 2013 at 10:35

Geoff,

How did you make that bold ‘HURT’?

31. May 2013 at 11:04

The ECB has some NGDP data out for 2013Q1:

here’s the chart for the eurozone

http://sdw.ecb.europa.eu/quickview.do?node=9484571&SERIES_KEY=119.ESA.Q.I6.Y.0000.B1QG00.1000.TTTT.L.U.A

And here are the individual series for some EZ members

http://sdw.ecb.europa.eu/browse.do?node=9484571

31. May 2013 at 11:33

… sorry. that must be the weird estimate you referred to. It’s at market prices (2005), not all countries seem to report, and I cannot find the deflator or non-adjusted inflation rates. Byzantine.

31. May 2013 at 13:53

J, Good point.

Doug, All sort sof conservative economists have warned about high inflation. But even those that don’t predict inflation, warn that if market monetarist policies were adopted we’d get lots of inflation.

The Fed forecasts below 2% inflation. That’s basically a violation of their mandate, and they are doing it intentionally.

The Japanese GDP deflator was down 2% in Q1.

Travis, I had trouble following David’s post. What exactly is he worried about? I don’t think the Japanese are manipulating their currency, but so what if they were?

W. Peden, That’s funny, I was told NGDP rose only 1.5% in Q1.

I believe the lag is much shorter than Friedman thought.

Steve, Good point.

31. May 2013 at 17:45

Geoff,

you are being a fool as usual.

There is no property right to a guaranteed return on your cash, only to the cash itself.

31. May 2013 at 18:27

The inflation hawks being wrong has never been funny or fun, particularly since 2007. It would be nice if both hawks and doves would be come extinct because the conversation shifts away from inflation to nominal stability instead.

31. May 2013 at 19:31

bonnie,

you’re right

31. May 2013 at 19:44

The public should be outraged—that the Fed has obtained less than 1 percent inflation, five years after the worst recession since the Great Depression, and in such a lousy job “recovery.”

I have little to contribute, in terms of economic insights, to Market Monetarism. But I will say this: MM’ers have not seized the language and framed the issues the way right-wing dogmatics have.

Try this on: “The Fed has been indecisive, feeble, and shown a lack of resolve in its bid to boost economic growth.”

We must associate Fed “strength” with “economic growth.” Instead, when we hear now about Fed “resolve,” it is always in fighting inflation.

MM’ers must define the Fed as being “weakling and unpredictable” in its current “maybe QE-maybe not” policies.

The sad thing is, not only am I advocating PR, but my characterizations of the Fed are actually accurate.

1. June 2013 at 02:26

This is remarkably deja vu. The euro is an artificial gold standard, Austrians are still burbling on about the years-ago boom and credit expansion while too many folk who should know better are worrying about inflation despite the utter lack of any evidence that it is, or is likely to be, an issue. Though Bernanke is more competent than Roy Young or Eugene Meyer, the Fed is shackled to a damaging conception of its purpose. It IS the 1930s rerun.

History does not repeat itself, but it does rhyme, to quote old Sam Clemens.

I blame Hayek and Keynes. Their flashy brilliance got in the way of of seeing the contemporary issues clearly and economics has been paying for it ever since.

(It is also a pity that Friedman did not quite believe enough in his expectations analysis of the Phillips Curve to realise that it also operated against relying on monetary quantities. But he did a lot to get economics out from under how the Hayek-Keynes imbroglio framed macro.)

1. June 2013 at 04:11

“Unfortunately for me, most of the inflation Cassandras (albeit not all) are on the right. They share my views on many other issues. ”

Does it worry you that you disagree with your side in the field you are an expert in (inflation and monetary problems), but agree with them in the fields you are less knowledgeable in? (It’s a related issue to the feeling you get when you read an article in your favorite magazine about your particular field of expertise and they get it wrong, and you suddenly wonder what else they’re getting wrong.)

1. June 2013 at 06:35

F. Lynx Pardinus,

There’s at least two big differences between (i) most inflation Cassandras being on the right and (ii) all people on the right being inflation Cassandras.

1. June 2013 at 07:30

Lynx, As long as my free market views are similar to the very best free market macroeconomists (Friedman, Fisher, etc) I’m not too worried. There are more and more conservatives coming over to the MM side. So I think it’s the conservatives that have not yet seen the light that should be worried.

But I do see your point, and it’s a good one. On the other hand I also think the left has a highly flawed model of money/macro, so I have no where to turn.

1. June 2013 at 07:31

Lorenzo, Very insightful comment.

1. June 2013 at 09:35

@ssumner Thanks for your response. I wish you well in your struggle for the minds of the right. (I feel the same way about my particular field, not too thrilled about the right, but the left seems worse)

2. June 2013 at 07:51

Though agnostic about flations I have run across two points recently. Flation is probably not binary,look at the prices of super tchotchkes (art) going into the nine figures. How many cartoons of a scream does the world need?

For the government’s idea of humor look at the hedonic adjustment tables. Four decimal places on women’s shoes. The major categories all run in the same direction. This despite the economy,as part of the slightly larger ecology going downhill in a non-linear direction( specifically say Mauna Loa CO2 and the arctic ice in September). A couple of percent should be added to the CPI for hedonics(overall lower quality). Ahh,the last meal before my execution was 25.333% better than the previous meal.

3. June 2013 at 19:36

[…] on his blog, responding to a commenter who indicated that he was worried by my suggestion that Japan might be engaging in currency manipulation, Scott […]

4. June 2013 at 21:36

I guess your maids do the shopping. But I assure you, as a mainstreeter ALL of my costs have gone UP. I am still buying $100 worth of groceries, but now that makes 3 bags instead of 4. My health insurance premium has doubled in the last 2 yrs. My utility bills have gone way up. Gasoline for the car….way too much. You might not call that “inflation”…but I do.

20. March 2017 at 05:16

[…] http://www.themoneyillusion.com/?p=21472#comments […]