The first step is admitting you have a problem

That is, the first step toward NGDP targeting. Marcus Nunes has a new post that quotes a Jon Hilsenrath story in the WSJ:

JACKSON HOLE, Wyo.””Central bankers aren’t sure they understand how inflation works anymore.

Inflation didn’t fall as much as many expected during the financial crisis, when the economy faltered and unemployment soared. It hasn’t bounced back as they predicted when the economy recovered and unemployment fell.

The conundrum challenges much of what central bankers thought they understood about the world, as well as their ability to do their job. How will they know when to raise or lower interest rates if they’re unsure what causes consumer prices to rise and fall?

“There is definitely less confidence, a lot less confidence” about how inflation works,James Bullard, President of the Federal Reserve Bank of St. Louis, said in an interview here Friday.

The mysterious path of inflation during the crisis and post-crisis era is the main topic at the Federal Reserve Bank of Kansas City’s annual economic symposium here, where Fed officials, academics and global central bankers gather every August to discuss economic issues.

Inflation dynamics are more than an academic issue. Fed officials are considering whether to raise short-term interest rates from near zero, where they have been since December 2008. The Fed’s main sticking point is that inflation has run below its 2% target for 39 straight months. Inflation is lower than central bank objectives throughout the developed world, despite exceptionally low interest rates and other extraordinary measures aimed at driving it higher.

Before raising rates, Fed officials want to be confident inflation will rise to 2%. They have a theory it will. Unemployment is falling””reaching 5.3% in July””and slack in the economy appears to be diminishing. As supplies of labor and productive capacity become more constrained, officials believe wages and prices will rise.

So far, however, there are few indications that’s happening. The Commerce Department reported Friday that U.S. consumer prices rose 0.3% in July from a year earlier, well below the Fed’s goal. Stripping out volatile food and energy categories, officially measured inflation also runs below 2%.

The economy’s performance has “really challenged” the notion of a strong link between unemployment and inflation, Mr. Bullard said on the sidelines of the conference. The existence of such a link was also challenged in the 1970s, an era of high inflation and high unemployment.

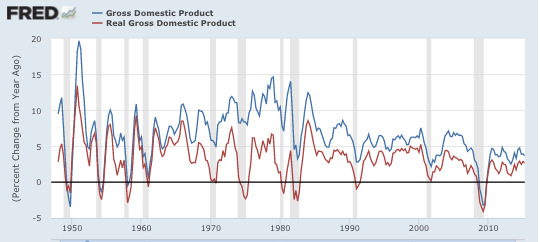

Fortunately, there another nominal variable that still does track the business cycle very closely:

Marcus’s post also has some interesting graphs.

Marcus’s post also has some interesting graphs.

PS. I have a new article on Milton Friedman and the euro, published in Reason magazine. (Subscribers only, but why wouldn’t you already be a subscriber?)

Tags:

29. August 2015 at 07:17

Yellen ally pours cold water on rule-based monetary policy http://news.yahoo.com/yellen-ally-pours-cold-water-rule-based-monetary-140746018–business.html

Anyone have the paper?

29. August 2015 at 07:30

The best indicator which tracks changes in the unemployment rate is Real GDP. 🙂

29. August 2015 at 08:00

‘How will they know when to raise or lower interest rates if they’re unsure what causes consumer prices to rise and fall?’

Perfect. That’s like some prehistoric engineer asking, ‘Wonder what would happen if I eliminated the sharp edges on the wheels of my cart? You know, made them round.’

29. August 2015 at 08:49

This reminds me of Cool Hand Scott (The Fed has a failure to communicate);

http://www.themoneyillusion.com/?p=14039

———–quote———-

I strongly believe that interest rates are the wrong policy instrument. But most people disagree with me. Even when the Fed does QE, they justify it as an action that will reduce long term rates. They seem completely unable to communicate to the public in any non-Keynesian language. OK, then why not keep talking Keynesian?

Here’s my suggestion: If the Fed is committed to communicating in terms of the fed funds rate, why not continue to have the Fed set a “shadow fed funds target.” The proposal would work as follows. The FOMC would continue to meet every six weeks and vote on the fed funds target that would be most effective in communicating their macro policy goals. For instance, this might be the number that results from the Taylor Rule formula. No consideration would be given to whether this was a positive or negative number. Then the Fed would announce the target, and instruct the New York trading desk to get as close as possible (which would be zero, or perhaps the IOR rate.)

…. Under my plan the 2010 meeting that led to QE2 might have gone as follows: The FOMC meets and sees that NGDP growth is slower than they’d like. They vote to cut the shadow fed funds target by 1/2%, from negative 2.75% to negative 3.25%. This sends a signal to the markets that the Fed will engage in future policy actions to raise NGDP slightly faster than the markets previously expected. Interestingly, that’s exactly how monetary policy works in normal times, or at least that’s 99.9% of how it works.

———–endquote————

29. August 2015 at 09:02

Isn’t the shift to a service economy the likely culprit? Wages are a lot stickier than industrial goods.

Plus, (measured) real output is now a balancing item; if I lack confidence, I eat at home instead of at a restaurant, I DIY instead of hiring a contractor, and I skip doctor’s appointments. But the waitress, contractor, and doctor do not adjust prices.

It seems obvious to me. What am I missing?

P.S.

If I’m right, this would support NGDP targeting. If inflation is following NGDP with loonnnngggg and variable lags, then it is important to have 4-5% NGDP trend.

29. August 2015 at 09:18

Sumner seems to lack the ability to think critically, but you readers don’t have to be wedded to his ideology.

NGPD = RGPD + inflation, but only EX POST, not EX ANTE. Meaning (pay attention here Don Geddis): after the data is in, at the end of the year, it is clear that the above equation, an accounting identity not unlike the accounting identity of the quantity theory of money, is true. However, before the data is in (in the beginning of the year), there’s no telling how RGDP and NGDP will correlate. People may hoard money despite the central bank printing it; or they may spend it faster than normal; money is neutral in any event, and the velocity of money is not constant. All these things make ‘targeting NGDP’ as futile as ‘targeting inflation’.

Only diehards of the neo-Sumerian cult of Sumner believe otherwise. These wild and wide-eyed fanatics are like zombies, immune to reason. For the rest of you–is anybody out there?–I offered this comment.

29. August 2015 at 09:21

The lag for inflation is precisely 2 years (for the last 100 + years). So money flows would have to accelerate beyond (or decelerate beyond), this time frame to have any impact on the domestic “price-level”.

The only time the 2 yr roc in the proxy for inflation fell below zero was in the last qtr of 2010. However, R-gDp’s volatility has been pronounced (due to stop-go monetary mis-management). I.e., there’s absolutely no conundrum.

The current deceleration in the economy is alarming. Never has the proxy for inflation collapsed to the extent that it will (without massive gov’t intervention), at this year’s end (expect a DEC commodity carnage).

29. August 2015 at 09:27

Lots of good comments, except . . .

Ray, NGDP does not equal RGDP plus inflation. But let’s give you the benefit of the doubt, and assume you meant NGDP growth and RGDP growth. Even then your comment makes no sense, as the equality also holds ex ante.

Tell me again how you know money is neutral in the short run? Oh yeah, changes in NGDP have no impact on RGDP.

29. August 2015 at 09:27

Ray Lopez:

Economic prognostications are infallible. I.e., R-gDp, N-gDp, and inflation are all known well in advance. That means their path can be corrected and fine tuned. That also means economists should not target N-gDp, but that the target should be R-gDp.

29. August 2015 at 09:33

ssumner:

Why doesn’t N-gDp = R-gDp + a deflator, viz., inflation? An inconsequential difference.

29. August 2015 at 10:04

I can’t wait for the possibility of the Fed missing an NGDP target for 39 straight months and then reading Monetarists saying that the Fed should try yet another, different but not all that different, rule.

Sumner wrote:

“Fortunately, there another nominal variable that still does track the business cycle very closely:”

Unfortunately you keep making the mistake that the Lucas critique does not apply to NGDPLT. Lucas wrote:

“Given that the structure of an econometric model consists of optimal decision rules of economic agents, and that optimal decision rules vary systematically with changes in the structure of series relevant to the decision maker, it follows that any change in policy will systematically alter the structure of econometric models.”

In other words, the reason prices becoming intentionally targeted by a central bank renders any previous seeming causal relationship between prices and “good times” all but moot, is the very same reason spending becoming targeted by a central bank will render any previous seeming causal relationship all but moot.

Perhaps a better way to put the same idea is from Goodhart:

“Any observed statistical regularity will tend to collapse once pressure is placed upon it for control purposes.”

29. August 2015 at 10:09

Ray,

Money is not neutral even by your own professed standard of Bernanke’s findings.

You continue to contradict yourself over and over.

If a commodity were neutral, it could function as a tool of economic action. Money is valued. More money in one person’s hands has a different effect than more money in another person’s hands. Since inflation always affects relative spending, it therefore always affects relative, and hence total, productivity.

The Fed could not have adversely affected the economy as it has in the past 100 years without hyperinflation, unless money were not neutral.

A neutral money is a contradiction in terms.

29. August 2015 at 10:10

Ray you are eliciting a zombie mentality, repeating the same contradicting of yourself over and over.

29. August 2015 at 10:33

“Fortunately, there another nominal variable that still does track the business cycle very closely:”

The reason the graph shows what it shows is because of the following:

As Lucas and Goodhart pointed out, since prices are being targeted by governments, prices cannot now be (not that they ever were) a measure of success or health. Any statistical correlation brought about by causation collapsed.

OF COURSE it will be the case that if central banks targeted prices, there will arise a strong correlation between NGDP and RGDP. This because NGDP and RGDP are mathematically related to prices.

Just because there has been up until now a strong correlation between NGDP and RGDP, on account of price targeting, it does not mean that moving towards targeting NGDP will keep that correlation the same, or even similar. That is precisely the false reasoning that Lucas and Goodhart warned against.

Production does not become stable when spending is stable. Both production and spending become stable when there is stable coordination. Stable coordination requires unhampered economic calculation, which socialist currency hampers.

29. August 2015 at 10:51

Speaking of Milton Friedman AND Reason;

https://www.youtube.com/watch?v=_rYPp4ofXAs

29. August 2015 at 11:54

Stanley Fischer: These 7 charts give me ‘good reason to believe’ inflation will move higher’

http://www.businessinsider.com.au/stanley-fischer-jackson-hole-inflation-speech-transcript-august-29-2015-2015-8#/#fischer-acknowledged-that-inflation-as-measured-by-the-pce-price-index-was-indeed-running-cold-1

29. August 2015 at 12:51

Stanley Fischer reasons from a price change:

“…the drop in oil prices over the past year, on the order of about 60 percent, has led directly to lower inflation…”

http://www.federalreserve.gov/newsevents/speech/fischer20150829a.htm

I thought those guys are supposed to be smart.

29. August 2015 at 13:16

Does anyne know how much was NGDP growth rate for the 2nd Quarter realeased yesterday?

29. August 2015 at 13:17

Ah, December oil carnage for more consumer spending lol, this board doesn’t get it.

(whispering, its the baby boomers stupid). When you have 40 years of reduced public consumption and investment, you get little investment growth. Even Calvin Coolidge would nod his head.

Without the Boomers to drive investment, 1975-2005 growth would have struggled outside the 95-00 period. Yet, lets mumble NGDP garbage.

30. August 2015 at 12:56

“When you have 40 years of reduced public consumption and investment”

-LOL.

“you get little investment growth”

-Investment as a percentage of GDP averaged higher in the U.S. after 1973 than before. Go back to your cave, garbage man.

30. August 2015 at 13:50

Ben Groves,

That is hilarious. Hey, did you know that when production declines, there is less goods to be stolen?

Clearly we should agree with your logic that the reason production rates have declined is because there is less being stolen.

Correlation equals causation FTW!

Please tell us more about how North Korea is wealthier than us because their “public” consumption is adequate.

30. August 2015 at 16:26

@scott,

Monetary policy is not anything like quantum mechanics. It’s trivial but is misunderstood by the public (and policy makers) for three main reasons.

1) For ideological reasons, some economists (e.g. PK) are loathe to reject fiscal policy (i.e. increased government spending) as an economic policy tool, and therefore disingenuously question the efficacy of monetary policy.

2) The transmission mechanism for monetary policy is not properly understood by economists, and therefore, explanations of monetary economics come across as voodoo economics.

3) There is a failure to distinguish between MB and MB-ER. People conclude that since there was a huge increase in MB which had little impact on economic growth that therefore monetary policy is ineffective. Economists need to strongly make the point that increases in reserves have no impact on the economy.

30. August 2015 at 17:43

@sumner – flow5 put you in your place. Run away.

Sumner: “Ray, NGDP does not equal RGDP plus inflation. But let’s give you the benefit of the doubt, and assume you meant NGDP growth and RGDP growth. Even then your comment makes no sense, as the equality also holds ex ante. ” no it does not. You cannot “determine” NGDP and inflation then get RGDP. In short, ex ante, you cannot say: RGDP = NGDP – ‘inflation’ (deflator), and get whatever RGDP you want simply by specifying NGDP and targeting inflation. Prove me wrong if you disagree. No ‘thought experiments’ but hard data.

31. August 2015 at 04:34

Ray, Flow5 attacked you, and you need to respond. It would be like a refrigerator debating a stove.

31. August 2015 at 08:00

@sumner – once again, you show you don’t understand irony nor jokes. No wonder you so badly flubbed the veiled insults that Bob Murphy of Australia lobbed your way, mistaking them as compliments.

Flow5 said: “Economic prognostications are infallible”…meant as irony, not as fact. Re-read his posts. He’s attacking you, not me.

2. September 2015 at 07:29

Ray, The fact that you thought I was serious in my Vindication post is priceless. You are like a child.